Fish and Seafood Market Size

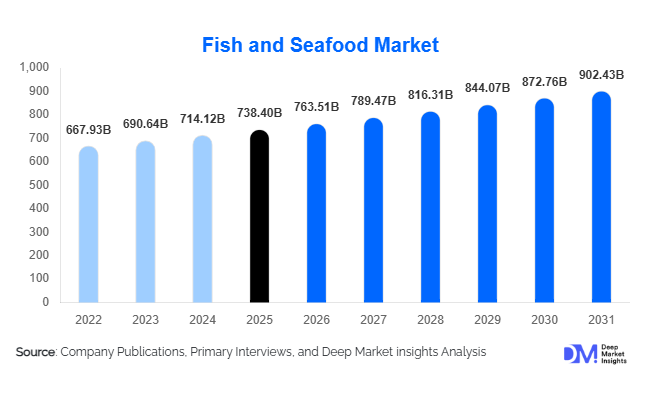

According to Deep Market Insights, the global fish and seafood market size was valued at USD 738.4 billion in 2025 and is projected to grow from USD 763.51 billion in 2026 to reach USD 902.43 billion by 2031, expanding at a CAGR of 3.4% during the forecast period (2026–2031). The fish and seafood market growth is primarily driven by rising global protein consumption, increasing demand for healthy and nutrient-rich diets, rapid expansion of aquaculture production, and advancements in cold-chain logistics infrastructure. Growing consumer awareness regarding omega-3 fatty acids, lean protein benefits, and sustainable seafood sourcing continues to strengthen demand across retail, foodservice, and industrial applications globally.

Key Market Insights

- Aquaculture production is increasingly replacing dependence on wild-catch fisheries, helping stabilize global seafood supply while supporting sustainability objectives.

- Frozen and value-added seafood products are witnessing strong demand growth, supported by urbanization, convenience-oriented lifestyles, and improvements in refrigeration technologies.

- Asia-Pacific dominates the global fish and seafood market, led by China, India, Vietnam, Indonesia, and Japan due to high seafood consumption and export-oriented aquaculture industries.

- North America remains a premium seafood consumption market, driven by rising health-conscious diets and strong demand for salmon, shrimp, crab, and lobster.

- Digital traceability and sustainability certifications are becoming key purchasing factors, especially in Europe and developed retail markets.

- Technological integration across aquaculture and processing operations, including AI-driven fish monitoring, automated feeding systems, blockchain traceability, and smart cold-chain management, is transforming the industry.

Fish and Seafood Market Latest Trends

Sustainable Aquaculture Expansion Accelerating

The global fish and seafood industry is rapidly transitioning toward sustainable aquaculture systems as governments and companies seek alternatives to overexploited wild fisheries. Advanced farming technologies such as recirculating aquaculture systems (RAS), offshore fish farming, AI-based water quality monitoring, and automated feeding systems are improving productivity and reducing environmental impact. Companies are increasingly investing in disease-resistant fish breeding programs, sustainable feed ingredients, and low-emission production systems to comply with tightening environmental regulations. Retailers and consumers are also prioritizing responsibly sourced seafood, driving greater adoption of certifications such as MSC and ASC across export-oriented markets.

Growth of Value-Added and Convenience Seafood Products

Changing consumer lifestyles and increasing urbanization are driving strong demand for ready-to-cook and ready-to-eat seafood products. Frozen seafood, marinated fish, breaded shrimp, seafood snacks, and portion-controlled packaging formats are gaining traction across supermarkets and online retail platforms. Foodservice operators are also expanding premium seafood menus with customized preparation formats to meet convenience-focused dining trends. Innovations in IQF freezing technology, vacuum skin packaging, and modified atmosphere packaging are improving shelf life and preserving nutritional quality, making seafood products more accessible across inland and export markets.

Fish and Seafood Market Drivers

Rising Health-Conscious Protein Consumption

Consumers globally are increasingly shifting toward healthier dietary habits, significantly boosting seafood demand. Fish and seafood products are rich in omega-3 fatty acids, lean protein, vitamins, and essential minerals, making them preferred alternatives to red meat. Rising prevalence of obesity, cardiovascular diseases, and diabetes has encouraged consumers to adopt balanced diets incorporating seafood products. Premium fish categories such as salmon, tuna, and trout are benefiting particularly from strong demand among health-conscious consumers in North America, Europe, Japan, and South Korea.

Expansion of Global Aquaculture Production

Aquaculture has become one of the fastest-growing food production industries globally. Countries including China, India, Vietnam, Norway, Indonesia, and Chile are significantly expanding aquaculture investments to improve seafood supply stability and export competitiveness. Government support, technological advancements, and rising seafood demand are encouraging large-scale fish and shrimp farming operations. Automation, precision feeding systems, and digital monitoring technologies are improving operational efficiency and reducing mortality risks, supporting long-term market growth.

Fish and Seafood Market Restraints

Overfishing and Sustainability Concerns

Overfishing and depletion of marine fish stocks remain major challenges for the fish and seafood market. Several commercially important species are facing sustainability pressures due to excessive harvesting and environmental degradation. Governments are introducing stricter fishing quotas, marine conservation laws, and traceability requirements, which may limit seafood supply and increase price volatility. Climate change and ocean warming are also affecting marine ecosystems and altering fish migration patterns, creating long-term supply uncertainties.

High Operational Costs and Disease Risks in Aquaculture

Aquaculture operations require substantial investments in infrastructure, water treatment systems, disease management, oxygenation equipment, and feed procurement. Disease outbreaks such as sea lice infestations in salmon farming and viral infections in shrimp aquaculture can significantly disrupt production and profitability. Rising feed costs, particularly fishmeal and soybean-based ingredients, continue pressuring operating margins across seafood farming operations globally.

Fish and Seafood Industry Key Opportunities

Digital Traceability and Smart Seafood Supply Chains

Blockchain-enabled traceability systems and digital seafood monitoring platforms are creating significant opportunities across the global seafood industry. Retailers and consumers increasingly demand transparent information regarding seafood origin, sustainability practices, and cold-chain integrity. Companies implementing digital traceability technologies can secure premium retail contracts, improve compliance with international regulations, and strengthen consumer trust. Smart logistics systems using IoT sensors and AI-driven inventory management are also improving efficiency across seafood exports and distribution networks.

Growth of Marine-Based Nutraceuticals and Functional Foods

The expanding nutraceutical and preventive healthcare industries are increasing demand for fish oils, omega-3 supplements, marine collagen, krill extracts, and seafood-derived proteins. Aging populations and rising health awareness are driving greater consumption of marine-based nutritional products globally. Seafood companies are increasingly diversifying into high-margin nutraceutical ingredients and pharmaceutical-grade marine extracts to improve profitability and reduce dependence on commodity seafood pricing.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 738.40 Billion |

| Market Size in 2026 | USD 763.51 Billion |

| Market Size in 2031 | USD 902.43 Billion |

| CAGR | 3.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fish remains the dominant product category within the global fish and seafood market, accounting for nearly 52% of total market value in 2025. Salmon, tuna, tilapia, cod, and pangasius continue leading global demand due to widespread consumer acceptance and strong retail penetration. Crustaceans such as shrimp, prawns, lobster, and crab represent a high-value segment supported by premium foodservice demand and export-oriented aquaculture production. Mollusks including oysters, mussels, clams, scallops, squid, and octopus continue gaining popularity across Mediterranean and Asian cuisines. Value-added seafood products such as marinated fish, breaded shrimp, smoked seafood, and ready-to-cook formats are witnessing strong growth due to changing consumer lifestyles and increasing convenience food demand.

Application Insights

Human consumption remains the dominant application segment and accounted for more than 82% of total fish and seafood market demand in 2025. Seafood products are increasingly integrated into healthy diets, premium restaurant offerings, and convenience food categories globally. Nutraceutical applications are rapidly expanding due to rising use of marine-derived omega-3 oils, collagen, and protein concentrates in preventive healthcare products. Animal feed and aquafeed applications also represent an important segment, particularly for fishmeal and marine protein ingredients. The pharmaceutical and cosmetics industries are increasingly utilizing seafood-derived bioactive compounds, marine collagen, and fish oil extracts for specialized formulations and skincare products.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for nearly 34% of global seafood sales in 2025. Large retail chains benefit from strong cold-chain infrastructure, packaged seafood offerings, and growing consumer preference for one-stop shopping experiences. Online seafood retail is expanding rapidly due to digital grocery adoption and direct-to-consumer delivery models. Specialty seafood stores continue attracting premium consumers seeking fresh and traceable seafood products. Foodservice channels including restaurants, hotels, cruise lines, and institutional catering remain major demand drivers, particularly for high-value seafood categories such as salmon, shrimp, lobster, oysters, and crab.

Source Insights

Aquaculture or farm-raised seafood accounted for approximately 56% of the global fish and seafood market in 2025 and continues gaining market share due to scalable production capacity and improved supply consistency. Farm-raised shrimp, salmon, tilapia, and pangasius dominate international seafood trade. Wild-caught seafood remains important for premium fish species and specialty seafood categories but faces increasing sustainability regulations and fishing quota restrictions. Integrated multi-trophic aquaculture systems and offshore fish farming technologies are emerging as important innovations within sustainable seafood production.

Packaging Insights

Frozen packaging formats dominate global seafood trade due to their longer shelf life and export flexibility. Vacuum skin packaging and modified atmosphere packaging are increasingly adopted across premium seafood categories because they improve freshness retention, reduce leakage, and enhance product presentation. Sustainable and recyclable seafood packaging solutions are also gaining traction as retailers and governments strengthen environmental sustainability targets. Smart packaging technologies incorporating freshness indicators and temperature tracking systems are further improving seafood quality monitoring during transportation and storage.

End-Use Insights

Household consumers remain the largest end-use segment for fish and seafood products, driven by growing health awareness and expanding retail accessibility. The HoReCa sector is among the fastest-growing end-use industries and is projected to expand at a CAGR exceeding 4.5% through 2031. Hotels, restaurants, premium sushi chains, and seafood-focused dining concepts continue increasing seafood procurement volumes globally. Nutraceutical manufacturers and pet food producers are also emerging as important end users due to rising demand for marine proteins, fish oils, and seafood-based functional ingredients.

Explore more data points, trends and opportunities Download Free Sample Report

Fish and Seafood Market Segmentations

By Product Type

- Fish

- Crustaceans

- Mollusks

- Cephalopods

- Others Seafood

By Source

- Wild-Caught Seafood

- Aquaculture/Farm-Raised Seafood

- Mariculture

- Inland Fisheries

- Integrated Multi-Trophic Aquaculture (IMTA)

By Form

- Fresh/Chilled

- Frozen

- Canned

- Dried

- Smoked

- Ready-to-Cook

- Ready-to-Eat

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Seafood Stores

- Online Retail/E-commerce

- Foodservice

- Industrial Buyers

By Application

- Human Consumption

- Nutraceuticals & Supplements

- Animal Feed & Aquafeed

- Pharmaceuticals

- Pet Food

- Cosmetics & Personal Care

Regional Insights

North America

North America accounted for nearly 18% of the global fish and seafood market in 2025, led primarily by the United States and Canada. The U.S. remains one of the world’s largest seafood importing countries due to high domestic demand for salmon, shrimp, tuna, lobster, and crab products. Health-conscious consumers, strong restaurant demand, and growing premium seafood consumption continue supporting market growth. Canada plays a major role through its lobster, crab, and salmon export industries, particularly supplying North American and Asian markets.

Europe

Europe represented approximately 23% of global market value in 2025. Norway remains a critical seafood production and export hub, particularly for salmon. Spain, France, Italy, and the United Kingdom continue driving seafood demand through Mediterranean diets, premium shellfish consumption, and strong retail penetration. European consumers increasingly prioritize sustainably sourced seafood products, accelerating demand for certified and traceable seafood. The region also remains highly dependent on seafood imports to meet domestic consumption requirements.

Asia-Pacific

Asia-Pacific dominates the global fish and seafood market with nearly 46% market share in 2025. China leads both seafood production and consumption globally due to its extensive aquaculture industry and massive domestic market. India and Vietnam continue strengthening their positions as major shrimp and seafood exporters supported by government incentives and expanding processing infrastructure. Japan and South Korea remain premium seafood consumption markets with high demand for sushi-grade fish, shellfish, and frozen seafood products. Indonesia and Thailand are also major regional seafood suppliers benefiting from strong marine resources and export-oriented aquaculture industries.

Latin America

Latin America is strengthening its position within global seafood exports, particularly through Chile, Ecuador, Peru, and Brazil. Chile remains one of the world’s leading salmon exporters, while Ecuador has emerged as a dominant shrimp exporting country. Regional seafood production benefits from extensive coastal resources and increasing investments in aquaculture modernization. Domestic seafood consumption is also gradually increasing due to rising urbanization and dietary diversification across major Latin American economies.

Middle East & Africa

The Middle East and Africa represent emerging growth markets for seafood products. Saudi Arabia and the UAE are investing heavily in domestic aquaculture development to improve food security and reduce import dependency. Tourism expansion and premium hospitality demand are increasing seafood consumption across Gulf countries. South Africa remains one of Africa’s most established seafood markets due to its fishing industry, export activities, and growing retail seafood penetration. Intra-regional seafood trade and aquaculture investments are also increasing across several African coastal economies.

Key Players in the Fish and Seafood Market

- Mowi ASA

- Thai Union Group

- Maruha Nichiro Corporation

- Nippon Suisan Kaisha (Nissui)

- Dongwon Industries

- Trident Seafoods

- Cooke Inc.

- Leroy Seafood Group

- High Liner Foods

- Clearwater Seafoods

- Austevoll Seafood

- Cermaq Group

- Pacific Seafood

- Grupo Nueva Pescanova

- AquaChile