Nitrile Gloves Market Size

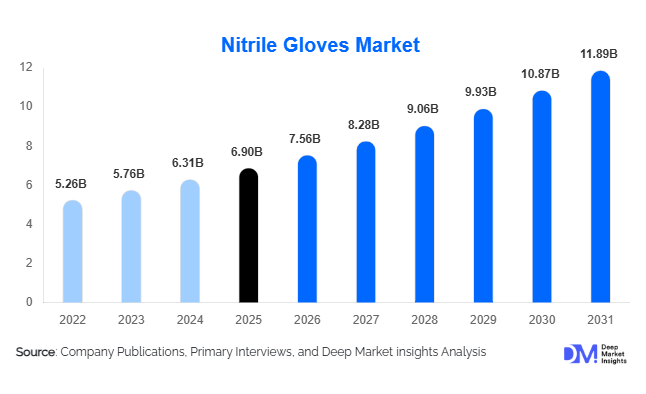

According to Deep Market Insights, the global nitrile gloves market size was valued at USD 6.9 billion in 2025 and is projected to grow from USD 7.56 billion in 2026 to reach USD 11.89 billion by 2031, expanding at a CAGR of 9.5% during the forecast period (2026–2031). The nitrile gloves market growth is primarily driven by increasing healthcare expenditures, stringent workplace safety regulations, growing pharmaceutical manufacturing activities, and rising adoption of latex-free personal protective equipment (PPE) across healthcare and industrial sectors. Nitrile gloves have become the preferred protective solution due to their superior chemical resistance, puncture protection, durability, and reduced risk of allergic reactions compared to natural rubber latex gloves. While healthcare applications continue to account for the majority of global demand, expanding usage in food processing, electronics manufacturing, biotechnology, automotive maintenance, and chemical handling is creating new growth opportunities. In addition, governments worldwide are strengthening healthcare preparedness programs and strategic PPE stockpiling initiatives, further supporting long-term demand. As manufacturers invest in automation, sustainable production technologies, and regional supply-chain diversification, the nitrile gloves market is expected to witness stable and broad-based growth throughout the forecast period.

Key Market Insights

- Healthcare and medical applications account for nearly 80% of global nitrile glove demand, supported by infection prevention protocols and rising surgical procedures worldwide.

- Powder-free nitrile gloves dominate the market, representing approximately 75% of total revenues due to stricter contamination-control requirements and lower allergy risks.

- North America remains the largest consumption market, accounting for approximately 37% of global demand in 2025.

- Asia-Pacific is the fastest-growing region, driven by healthcare expansion, pharmaceutical manufacturing investments, and industrialization across China, India, and Southeast Asia.

- Malaysia continues to dominate global nitrile glove manufacturing, supported by established production infrastructure and integrated supply chains.

- Automation, sustainable production technologies, and biodegradable nitrile formulations are emerging as key competitive differentiators among leading manufacturers.

Nitrile Gloves Market Trends

Growing Adoption of Sustainable and Eco-Friendly Gloves

Environmental concerns regarding single-use PPE waste are encouraging manufacturers to develop biodegradable nitrile gloves, recyclable packaging solutions, and low-carbon manufacturing processes. Healthcare providers, pharmaceutical companies, and multinational industrial customers are increasingly incorporating ESG criteria into procurement decisions. Leading manufacturers are investing in renewable energy-powered production facilities, water recycling systems, and sustainable raw material sourcing initiatives to reduce environmental impact while maintaining product performance. As regulatory scrutiny regarding industrial waste and carbon emissions intensifies, sustainability is expected to become a major purchasing criterion across developed markets.

Automation and Smart Manufacturing Transforming Production

The nitrile gloves industry is witnessing significant investments in automated production lines, AI-enabled quality inspection systems, and robotic packaging technologies. Automation enables manufacturers to improve product consistency, reduce labor dependency, lower production costs, and increase operational efficiency. Major glove producers are increasingly integrating Industry 4.0 technologies to enhance production monitoring and predictive maintenance capabilities. These advancements are particularly important in maintaining competitiveness amid pricing pressures and ongoing labor shortages in key manufacturing regions. Automated facilities also allow producers to rapidly scale production during periods of elevated demand while ensuring compliance with stringent quality standards.

Nitrile Gloves Market Drivers

Rising Healthcare Expenditure and Infection Prevention Standards

Healthcare remains the largest consumer of nitrile gloves globally. Rising hospital admissions, increasing surgical procedures, expanding diagnostic testing volumes, and heightened infection-control protocols continue to drive demand across developed and emerging economies. The growing prevalence of healthcare-associated infections has reinforced the importance of disposable protective equipment, making nitrile gloves an essential component of modern healthcare operations. Additionally, increasing government investments in healthcare infrastructure and strategic medical stockpiles are supporting long-term market expansion.

Expanding Industrial Safety Compliance Requirements

Industries including chemicals, automotive manufacturing, food processing, oil and gas, electronics, and heavy manufacturing are increasingly adopting nitrile gloves to comply with occupational safety regulations. Compared to latex and vinyl alternatives, nitrile gloves provide superior resistance to chemicals, oils, solvents, and punctures. Governments worldwide continue to strengthen workplace safety standards, encouraging employers to adopt higher-quality protective equipment and driving sustained industrial demand.

Nitrile Gloves Market Restraints

Volatility in Nitrile Butadiene Rubber Prices

Nitrile gloves are manufactured using nitrile butadiene rubber (NBR), a petrochemical-derived material subject to fluctuations in crude oil prices and feedstock availability. Variations in raw material costs can significantly impact manufacturing expenses and profit margins. Smaller producers often face greater challenges in managing these fluctuations due to limited purchasing power and lower economies of scale.

Persistent Industry Oversupply and Pricing Pressure

Significant manufacturing capacity expansions during the pandemic resulted in excess production capabilities across Asia. Although demand remains healthy, ongoing oversupply in certain product categories has intensified price competition among manufacturers. As a result, average selling prices have normalized substantially from pandemic-era peaks, creating margin pressures and encouraging consolidation among industry participants. Maintaining profitability while balancing production utilization remains a key challenge for many manufacturers.

Nitrile Gloves Market Opportunities

Expansion of Pharmaceutical and Biotechnology Manufacturing

The rapid expansion of pharmaceutical production, biologics manufacturing, vaccine development, and biotechnology research presents substantial opportunities for nitrile glove suppliers. Cleanroom-compatible, sterile, and low-particulate nitrile gloves are increasingly required in highly regulated production environments. Manufacturers capable of offering premium products that meet stringent contamination-control requirements can benefit from higher margins and long-term supply agreements with pharmaceutical companies.

Localization of PPE Manufacturing and Supply Chains

Governments worldwide are encouraging domestic PPE manufacturing to improve supply chain resilience and reduce dependence on imports. Programs supporting local production in the United States, India, Saudi Arabia, Brazil, and Europe are creating opportunities for both established manufacturers and new market entrants. Investments in regional production facilities can help companies secure government procurement contracts while reducing transportation costs and supply chain risks. As healthcare systems prioritize supplier diversification, localized production strategies are expected to become increasingly important.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.9 Billion |

| Market Size in 2026 | USD 7.56 Billion |

| Market Size in 2031 | USD 11.89 Billion |

| CAGR | 9.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Disposable nitrile gloves dominate the global market, accounting for approximately 87% of total revenue in 2025. Their widespread adoption across hospitals, diagnostic laboratories, pharmaceutical manufacturing facilities, food processing plants, and industrial workplaces supports their leadership position. Demand is driven by infection prevention requirements, contamination control standards, and workplace safety regulations. Reusable nitrile gloves represent a smaller but growing segment, particularly within chemical processing, heavy manufacturing, and oil and gas applications where enhanced durability and chemical resistance are required. Manufacturers continue to innovate within disposable glove categories through improved tactile sensitivity, enhanced comfort, and biodegradable formulations that address environmental concerns while maintaining protective performance.

Application Insights

Examination procedures represent the largest application segment, accounting for approximately 38% of global market demand. Rising volumes of patient examinations, diagnostic testing, outpatient procedures, and infection-control activities continue to support growth. Surgical procedures constitute another significant application area, particularly for sterile nitrile gloves. Beyond healthcare, chemical handling, food processing, automotive maintenance, and electronics manufacturing are experiencing strong adoption rates due to increasing occupational safety standards. Cleanroom applications within semiconductor and biotechnology industries are emerging as particularly attractive growth opportunities, driven by stringent contamination-control requirements and expanding advanced manufacturing activities globally.

Distribution Channel Insights

Direct institutional sales account for the largest share of global nitrile glove distribution, representing approximately 45% of total revenues. Hospitals, healthcare systems, pharmaceutical companies, and industrial enterprises increasingly prefer direct procurement contracts to ensure supply security and favorable pricing. Medical and industrial distributors continue to play a critical role in serving small and medium-sized customers through established logistics networks. E-commerce platforms are gaining importance, particularly among smaller healthcare facilities and industrial users seeking efficient procurement options. Digital procurement platforms are increasingly offering inventory management tools, subscription purchasing models, and real-time product availability tracking, enhancing purchasing convenience and transparency.

End-Use Industry Insights

Healthcare and medical applications remain the dominant end-use segment, accounting for nearly 80% of global nitrile glove consumption in 2025. Hospitals, clinics, laboratories, ambulatory surgical centers, and emergency medical services continue to generate substantial demand due to strict infection-control requirements. Pharmaceutical and biotechnology industries represent the fastest-growing end-use segment, supported by increasing biologics manufacturing, vaccine production, and laboratory research activities. Food and beverage processing, automotive manufacturing, electronics production, and chemical processing industries are also expanding their use of nitrile gloves as occupational safety regulations become more stringent. Semiconductor manufacturing and cleanroom operations are emerging as high-value application areas requiring premium glove products.

Explore more data points, trends and opportunities Download Free Sample Report

Nitrile Gloves Market Segmentations

By Product Type

- Disposable Nitrile Gloves

- Reusable Nitrile Gloves

By Formulation Type

- Powder-Free Nitrile Gloves

- Powdered Nitrile Gloves

By Application

- Examination Procedures

- Surgical Procedures

- Laboratory & Research Activities

- Chemical Handling

- Food Processing & Handling

- Automotive Maintenance

- Manufacturing Operations

- Cleanroom Operations

- Janitorial & Sanitation Activities

- Emergency Response & Public Safety

By End-Use Industry

- Healthcare & Medical

- Pharmaceutical & Biotechnology

- Food & Beverage Processing

- Automotive

- Oil & Gas

- Chemicals & Petrochemicals

- Electronics & Semiconductor Manufacturing

- Metal & Machinery

- Government & Defense

- Waste Management & Sanitation

By Distribution Channel

- Direct Sales / Institutional Contracts

- Medical & Industrial Distributors

- Specialty PPE Suppliers

- E-commerce Platforms

- Retail Stores

Regional Insights

North America

North America accounted for approximately 37% of global nitrile glove demand in 2025, making it the largest regional market. The United States dominates regional consumption due to extensive healthcare spending, stringent OSHA regulations, and strong pharmaceutical manufacturing activity. Canada contributes through healthcare sector expansion and increasing adoption of high-quality PPE. Mexico is experiencing rising demand from automotive manufacturing, industrial production, and export-oriented assembly operations. Strategic stockpiling initiatives and healthcare preparedness programs continue to support long-term market growth throughout the region.

Europe

Europe represented approximately 28% of global market revenues in 2025. Germany remains the largest market due to its advanced healthcare infrastructure, pharmaceutical production capacity, and industrial manufacturing base. The United Kingdom, France, Italy, and Spain also contribute significantly to regional demand. Strict worker safety regulations and growing pharmaceutical investments continue to support market expansion. Increasing emphasis on sustainable procurement practices is accelerating adoption of environmentally friendly nitrile glove solutions across Europe.

Asia-Pacific

Asia-Pacific accounted for approximately 24% of global demand while serving as the primary global manufacturing hub. China represents the largest regional consumer due to its extensive industrial sector and expanding healthcare infrastructure. Malaysia remains the world's leading production center, while India is emerging as the fastest-growing market with forecast growth exceeding 13% annually. Japan and South Korea generate substantial demand through healthcare services, electronics manufacturing, and semiconductor production. Rapid industrialization and increasing healthcare investments continue to drive strong regional growth.

Latin America

Latin America accounted for approximately 5% of global demand in 2025. Brazil remains the dominant regional market due to its large healthcare system, pharmaceutical sector, and food processing industry. Mexico benefits from strong manufacturing activity and export-oriented industries, while Argentina and Chile continue to witness steady growth in healthcare-related demand. Improving occupational safety standards and healthcare modernization initiatives are expected to support future expansion.

Middle East & Africa

The Middle East & Africa region represented approximately 6% of global market revenues in 2025. Saudi Arabia and the UAE are driving demand through healthcare infrastructure investments, industrial diversification programs, and pharmaceutical manufacturing expansion. South Africa remains the largest African market due to its developed healthcare system and industrial base. Increasing healthcare access and government investments in medical infrastructure are expected to create additional growth opportunities throughout the region.

Key Players in the Nitrile Gloves Market

- Top Glove Corporation

- Hartalega Holdings Berhad

- Kossan Rubber Industries Bhd

- Supermax Corporation Berhad

- Ansell Limited

- INTCO Medical Technology Co., Ltd.

- Medline Industries, LP

- Cardinal Health, Inc.

- YTY Group

- Riverstone Holdings Limited

- Semperit AG Holding

- AMMEX Corporation

- Superior Glove Works Ltd.

- Unigloves (UK) Limited

- Globus Group