Matcha Biscuit Market Size

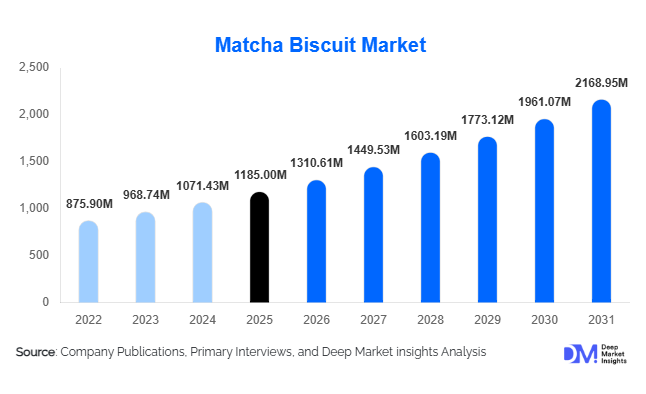

According to Deep Market Insights, the global matcha biscuit market size was valued at USD 1,185 million in 2025 and is projected to grow from USD 1,310.61 million in 2026 to reach USD 2,168.95 million by 2031, expanding at a CAGR of 10.6% during the forecast period (2026–2031). The matcha biscuit market growth is primarily driven by rising consumer demand for premium functional snacks, increasing adoption of matcha-based food products, growing health consciousness, and the expansion of Asian-inspired bakery products across global retail channels. Matcha biscuits have evolved from a niche Japanese confectionery category into a mainstream premium snack segment supported by clean-label trends, antioxidant-rich ingredient positioning, and premiumization across the global biscuit industry.

Key Market Insights

- Functional snacking is becoming a key purchasing driver, with consumers increasingly seeking biscuits containing natural antioxidants, plant-based ingredients, and reduced sugar formulations.

- Premium and artisanal matcha biscuit products are expanding rapidly, supported by consumer willingness to pay higher prices for authentic Japanese matcha ingredients and specialty formulations.

- Asia-Pacific dominates the global market, led by Japan, China, and South Korea, where matcha consumption is deeply embedded within food culture.

- North America represents the fastest-growing regional market, driven by wellness-focused consumers and increasing penetration of Asian-inspired snacks.

- E-commerce channels are becoming critical growth engines, enabling specialty manufacturers to access premium consumers directly through digital platforms.

- Product innovation in vegan, gluten-free, and protein-fortified biscuits is reshaping competition and expanding addressable consumer segments globally.

Matcha Biscuit Market Latest Trends

Premiumization and Authentic Japanese Matcha Positioning

Manufacturers are increasingly differentiating products through the use of premium Japanese matcha sourced from regions such as Uji, Nishio, and Shizuoka. Consumers are becoming more knowledgeable about matcha quality grades, leading to greater demand for biscuits made with ceremonial-grade and premium culinary-grade matcha. Premium packaging, artisanal production methods, limited-edition flavors, and gift-oriented formats are gaining popularity across developed markets. This trend is particularly strong among urban consumers seeking unique snacking experiences and products with authentic origin stories. Brands are leveraging geographical sourcing certifications and transparency initiatives to strengthen premium positioning and command higher margins.

Health-Oriented Product Innovation Accelerating

The market is witnessing significant innovation in health-focused biscuit formulations. Manufacturers are launching low-sugar, sugar-free, high-protein, vegan, gluten-free, and organic matcha biscuit variants to address evolving consumer preferences. Functional ingredients such as collagen, probiotics, plant proteins, dietary fibers, and adaptogens are increasingly being incorporated into product portfolios. Matcha's association with antioxidants, natural caffeine, and wellness benefits aligns strongly with consumer demand for healthier indulgence products. As regulatory scrutiny surrounding sugar content intensifies globally, health-positioned matcha biscuits are expected to capture an increasing share of new product launches.

Matcha Biscuit Market Drivers

Growth of Functional and Better-for-You Snacking

Consumers are increasingly replacing traditional indulgent snacks with products offering perceived nutritional benefits. Matcha biscuits benefit from matcha's reputation as a natural source of antioxidants and wellness-supporting compounds. Health-conscious consumers actively seek snacks that combine taste with functionality, positioning matcha biscuits favorably within premium biscuit categories. This shift is especially visible among millennials and Generation Z consumers who prioritize ingredient transparency and health-focused food choices.

Expansion of Asian-Inspired Food Consumption Globally

The globalization of Asian food culture continues to support demand for matcha-based products across North America, Europe, and Latin America. Japanese-inspired flavors have gained mainstream acceptance through cafés, specialty bakeries, and retail chains. Matcha's growing presence in beverages, desserts, confectionery, and bakery products has significantly improved consumer familiarity, encouraging trial and repeat purchases of matcha biscuits. International tourism, social media exposure, and cross-border food retailing have further accelerated category awareness.

Rapid Development of Premium Retail and E-Commerce Channels

Digital retailing has transformed accessibility for specialty snack products. Premium food brands can now reach niche consumer segments directly through online platforms without relying exclusively on traditional retail distribution. Subscription snack boxes, direct-to-consumer websites, specialty food marketplaces, and premium grocery delivery services have expanded visibility for matcha biscuit products. Improved logistics and cross-border e-commerce capabilities are enabling international brands to access previously underserved markets.

Matcha Biscuit Market Restraints

Volatility in Premium Matcha Raw Material Prices

High-quality matcha production remains concentrated within limited agricultural regions, particularly Japan. Weather variability, labor shortages, agricultural land constraints, and rising cultivation costs can create supply-side volatility. These factors directly affect manufacturing costs and profit margins for premium biscuit producers. Smaller manufacturers often face challenges securing long-term supply contracts for premium-grade matcha powder.

Limited Consumer Awareness in Emerging Markets

Despite increasing global popularity, matcha remains a relatively unfamiliar ingredient in many developing economies. Consumers may not fully understand the taste profile, health benefits, or premium value proposition associated with matcha products. Educational marketing investments are often required to stimulate demand, creating additional costs for market entrants and limiting rapid category adoption in certain regions.

Matcha Biscuit Industry Key Opportunities

Expansion of Functional Nutrition Product Lines

The growing functional food industry presents significant opportunities for manufacturers to develop advanced matcha biscuit formulations targeting specific health benefits. Products enriched with protein, probiotics, collagen, fiber, adaptogens, and plant-based nutrients are expected to attract wellness-focused consumers. The convergence of confectionery and functional nutrition categories could substantially increase average selling prices and improve profitability. Functional matcha biscuits are increasingly being positioned as meal supplements, healthy snacks, and on-the-go nutrition solutions.

Emerging Demand Across Developing Asian Markets

Rapid urbanization, increasing disposable incomes, and premium food adoption across India, Indonesia, Vietnam, Thailand, and the Philippines create substantial growth opportunities. Rising middle-class populations are demonstrating greater willingness to experiment with premium international food products. Retail modernization and growing café culture across these markets further support demand expansion. Localized product development strategies could significantly accelerate market penetration throughout emerging Asian economies.

Corporate Gifting and Premium Seasonal Packaging

Premium matcha biscuits are increasingly being positioned as gifting products during festivals, holidays, and corporate events. Luxury packaging, limited-edition collections, and premium assortments are helping manufacturers enter high-margin gifting segments. This opportunity is particularly attractive in Asia-Pacific markets where premium food gifting represents a significant cultural and commercial practice. Seasonal product launches can generate incremental revenue while strengthening brand visibility.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1185.00 Million |

| Market Size in 2026 | USD 1310.61 Million |

| Market Size in 2031 | USD 2168.95 Million |

| CAGR | 10.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Matcha cookies continue to dominate the global product landscape, accounting for approximately 31.8% of the market in 2025. Their leadership is primarily driven by strong consumer familiarity with cookie formats, ease of mass production, and their ability to balance premium positioning with mainstream affordability. Manufacturers benefit from established baking infrastructure and scalable supply chains, enabling consistent product quality across large retail networks. Growing demand for fusion snacks that combine traditional Japanese flavors with Western-style baked goods further reinforces the dominance of this segment across global markets.Matcha cream-filled biscuits hold a notable share of approximately 17.4%, supported by increasing consumer preference for indulgent, texture-rich snacking experiences. Their growth is driven by premiumization trends in the biscuit category, where consumers are willing to pay more for layered flavors and enhanced sensory appeal. Matcha wafer biscuits account for nearly 14.2% of demand, particularly supported by strong consumption in Asian markets where lighter, crisp textures are preferred in everyday snacking occasions. Matcha chocolate-coated biscuits continue to gain momentum within premium retail channels, driven by rising demand for multi-flavor combinations and confectionery-style indulgence. Shortbread-based matcha products are expanding at a faster pace in Europe and North America, largely due to their association with premium tea culture, café-style consumption, and gifting occasions where rich, buttery textures align well with consumer expectations.

Ingredient Positioning Insights

Conventional matcha biscuits maintain market dominance with approximately 73.5% share in 2025, primarily driven by cost efficiency, widespread availability of raw materials, and strong penetration across mass retail channels. The leading driver for this segment is its ability to cater to price-sensitive consumers while maintaining acceptable flavor authenticity, making it the default choice for large-scale commercial production and private-label offerings across supermarkets and hypermarkets globally.Organic matcha biscuits, while smaller in share, represent the fastest-growing ingredient category, supported by accelerating demand for clean-label, minimally processed, and certified organic food products. Growth is driven by increasing consumer awareness of food provenance, sustainability concerns, and health-oriented purchasing behavior, particularly among urban millennials and high-income households. Strengthening organic certification standards across North America, Europe, and parts of Asia-Pacific are further reinforcing trust in organic labeling, allowing manufacturers in this segment to command premium pricing and expand shelf presence in specialty retail environments.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate distribution, accounting for approximately 38.7% of global sales. Their leadership is driven by high product visibility, one-stop shopping convenience, and strong supply chain integration with both international and domestic biscuit manufacturers. The ability to offer a wide assortment of price tiers, from mass-market to premium imported matcha biscuits, makes these channels the most influential point of purchase globally.Online retail channels represent the fastest-growing distribution segment, contributing nearly 19.6% of total market revenue. Growth in this channel is primarily driven by expanding digital penetration, rising consumer comfort with cross-border e-commerce, and increasing demand for niche and premium imported products that are not always widely available in physical stores. Subscription-based snack models and direct-to-consumer brand ecosystems are further accelerating online sales, particularly among younger, digitally engaged consumers seeking convenience and product variety.Specialty food stores continue to play a strategic role in the distribution ecosystem by catering to premium, artisanal, and organic product categories where expert curation and product storytelling influence purchase decisions. Direct-to-consumer platforms are also gaining traction as brands invest in digital storefronts to improve margins, strengthen customer relationships, and build brand loyalty through personalized engagement and limited-edition product offerings.

End Use Insights

Household consumption remains the dominant end-use segment, accounting for approximately 67.2% of global demand in 2025. This leadership is driven by rising consumer inclination toward premium snacking at home, increased adoption of convenience-oriented food products, and the growing integration of matcha-based biscuits into daily dietary routines. The shift toward at-home indulgence, particularly following lifestyle changes in urban populations, continues to reinforce household dominance in the market.Cafés and coffee chains represent the fastest-growing commercial end-use segment, supported by the expanding global café culture and increasing incorporation of matcha-flavored products into beverage pairings and snack menus. The leading driver for this segment is the synergy between premium beverages and complementary baked goods, which enhances customer experience and increases average transaction value. Hotels, restaurants, and premium hospitality establishments are also expanding their use of matcha biscuits across dessert menus, afternoon tea services, and in-room dining offerings, driven by the growing demand for differentiated and culturally inspired culinary experiences. Airlines and travel retail operators are emerging as additional growth avenues as premium packaged snacks gain traction among international travelers seeking high-quality, portable food options.

Explore more data points, trends and opportunities Download Free Sample Report

Matcha Biscuit Market Segmentations

By Product Type

- Matcha Cookies

- Matcha Sandwich Biscuits

- Matcha Wafer Biscuits

- Matcha Shortbread Biscuits

- Matcha Cream-Filled Biscuits

- Matcha Chocolate-Coated Biscuits

- Matcha Crackers & Savory Biscuits

- Other Specialty Matcha Biscuits

By Matcha Grade Used

- Ceremonial Grade Matcha Biscuits

- Premium Culinary Grade Matcha Biscuits

- Standard Culinary Grade Matcha Biscuits

By Ingredient Positioning

- Organic Matcha Biscuits

- Conventional Matcha Biscuits

By Nutritional Positioning

- Regular Matcha Biscuits

- Low-Sugar Matcha Biscuits

- Sugar-Free Matcha Biscuits

- High-Protein Matcha Biscuits

- Functional & Fortified Matcha Biscuits

- Gluten-Free Matcha Biscuits

- Vegan Matcha Biscuits

By Packaging Format

- Single-Serve Packs

- Multi-Pack Retail Packs

- Family Packs

- Premium Gift Packs

- Bulk/Foodservice Packs

Regional Insights

Asia-Pacific

Asia-Pacific leads the global matcha biscuit market with approximately 46.3% share in 2025, supported by deep-rooted cultural familiarity with matcha-based products and strong domestic consumption patterns. Japan remains the dominant country market, driven by longstanding tea traditions, high per-capita consumption, and continuous product innovation within the confectionery sector. China represents a major growth engine, with expansion fueled by rapid urbanization, rising disposable incomes, and increasing adoption of café-style lifestyles that incorporate premium snack consumption. South Korea continues to demonstrate strong demand for innovative bakery and fusion products, supported by a highly trend-sensitive consumer base. India is emerging as a high-potential market, driven by a growing middle class, expanding café culture, and increasing openness to international flavors. Across Southeast Asia and Australia, growth is supported by tourism, premium retail expansion, and rising interest in Japanese-inspired food products.

North America

North America accounts for approximately 24.8% of global revenue, with the United States serving as the primary demand center. Growth in the region is driven by rising health and wellness awareness, increasing preference for premium and functional snacks, and expanding consumer interest in Asian-inspired food categories. Canada contributes steadily, supported by strong demand for organic, natural, and clean-label bakery products.The leading driver of regional expansion is the premiumization of snacking behavior, where consumers are increasingly willing to experiment with global flavors while prioritizing perceived health benefits and ingredient transparency. The region is expected to maintain one of the highest growth rates globally due to continued innovation in functional foods and strong e-commerce penetration.

Europe

Europe contributes approximately 21.2% of global demand, with key markets including the United Kingdom, Germany, France, Italy, and the Netherlands. Growth is supported by strong demand for specialty bakery products, increasing popularity of tea and coffee pairing snacks, and rising consumer preference for clean-label and natural ingredient formulations.The primary regional driver is the shift toward premium artisanal bakery consumption, where consumers value authenticity, ingredient quality, and sustainable sourcing. Retailers across Western Europe are increasingly expanding their assortments of matcha-based products, particularly in premium supermarket chains and specialty food outlets, reinforcing steady market expansion.

Latin America

Latin America remains a developing market with steady growth potential, led by Brazil, followed by Mexico and Argentina. Market expansion is primarily driven by increasing exposure to international food trends, rising urbanization, and gradual growth of premium imported snack consumption.The key growth driver in the region is the rising influence of globalized food culture among urban middle- and upper-income consumers, who are increasingly seeking differentiated snack experiences. Expansion of modern retail infrastructure and growing penetration of e-commerce platforms are further supporting category visibility and accessibility.

Middle East & Africa

The Middle East & Africa region is emerging as a premium consumption hub, with the United Arab Emirates and Saudi Arabia leading regional demand due to high disposable incomes and strong demand for imported specialty food products. South Africa remains the most developed market in Sub-Saharan Africa, supported by urban retail expansion and a growing affluent consumer base.Regional growth is primarily driven by luxury food consumption trends, strong gifting culture, and increasing tourism inflows that promote exposure to international snack categories. Premium retail environments in Gulf countries are particularly influential in shaping demand, as consumers increasingly seek high-quality imported confectionery products aligned with lifestyle-oriented consumption patterns.

Key Players in the Matcha Biscuit Market

- Ezaki Glico Co., Ltd.

- Bourbon Corporation

- Morinaga & Co., Ltd.

- Lotte Corporation

- Meiji Holdings Co., Ltd.

- Weee!

- Mondelez International, Inc.

- Yoku Moku Co., Ltd.

- Ito En Ltd.

- Nissin Foods Group

- LOTTE Wellfood Co., Ltd.

- Walker's Shortbread Ltd.

- Biscuiterie de Provence

- Shirakiku Foods Inc.

- The Matcha Reserve