Kenaf Market Size

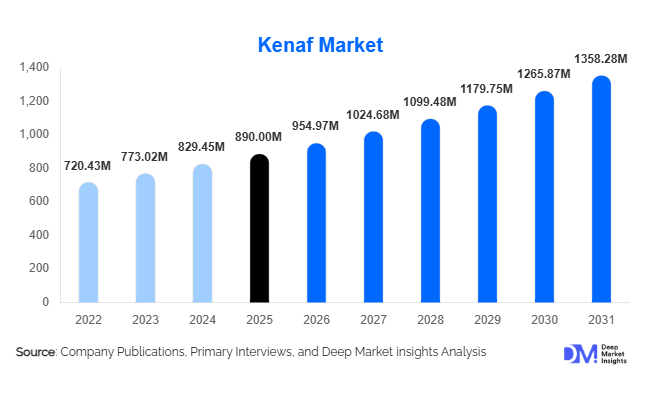

According to Deep Market Insights, the global kenaf market size was valued at USD 890 million in 2025 and is projected to grow from USD 954.97 million in 2026 to reach USD 1,358.28 million by 2031, expanding at a CAGR of 7.3% during the forecast period (2026–2031). The market growth is primarily driven by increasing adoption of sustainable natural fibers across automotive, construction, packaging, and industrial applications. Growing environmental regulations, rising demand for lightweight bio-composites, and the global transition toward circular economy practices are encouraging manufacturers to substitute synthetic materials with renewable alternatives such as kenaf. The crop’s high biomass yield, rapid growth cycle, and carbon sequestration capabilities make it an attractive raw material for industries seeking lower-carbon production processes.

Key Market Insights

- Automotive composites remain the largest applicati, on segment, accounting for nearly 28% of global kenaf demand owing to increasing use of lightweight interior vehicle components.

- Processed kenaf fiber dominates product consumption, representing approximately 42% of market revenue due to its suitability for industrial manufacturing processes.

- Asia-Pacific leads the global market, accounting for approximately 44% of total demand, supported by large-scale cultivation and processing capacity in China, India, Malaysia, and Thailand.

- Construction applications are emerging as the fastest-growing segment, driven by demand for green building materials, sustainable insulation products, and low-carbon infrastructure solutions.

- Bio-based packaging is creating new growth opportunities, as manufacturers increasingly replace petroleum-based packaging materials with biodegradable fiber-based alternatives.

- Technological advancements in fiber treatment and composite engineering are improving the mechanical properties and commercial viability of kenaf-based products.

Kenaf Market Trends

Growing Adoption of Natural Fiber Composites in Automotive Manufacturing

Automotive manufacturers are increasingly incorporating kenaf-based composites into vehicle interiors, door panels, package trays, dashboards, and trunk liners. The shift toward electric vehicles has further accelerated demand for lightweight materials that improve energy efficiency and extend battery range. Kenaf fibers offer favorable strength-to-weight characteristics while supporting sustainability goals established by automotive OEMs. Manufacturers across Europe, North America, China, and Japan are expanding the use of natural fiber composites to reduce overall vehicle weight and comply with stringent carbon reduction regulations. As vehicle electrification accelerates globally, demand for renewable fiber reinforcements is expected to continue growing throughout the forecast period.

Expansion of Sustainable Packaging Applications

The global packaging industry is increasingly adopting biodegradable and renewable materials to reduce dependence on petroleum-derived plastics. Kenaf pulp and fibers are gaining attention for use in molded packaging, paperboard products, protective packaging, and reinforced bioplastics. Government regulations restricting single-use plastics, combined with rising consumer preference for environmentally responsible packaging solutions, are accelerating adoption. Food packaging manufacturers, consumer goods companies, and e-commerce firms are actively evaluating kenaf-based materials as part of broader sustainability initiatives. This trend is creating new revenue opportunities for fiber processors and pulp manufacturers globally.

Kenaf Market Drivers

Rising Demand for Sustainable Raw Materials

Governments and corporations worldwide are implementing aggressive sustainability strategies aimed at reducing carbon emissions and improving resource efficiency. Kenaf offers several environmental advantages, including rapid renewability, high carbon absorption rates, and reduced reliance on non-renewable resources. Industries such as automotive, packaging, construction, and consumer goods are increasingly adopting kenaf-based materials as alternatives to synthetic fibers and wood-derived products. Sustainability commitments by multinational corporations continue to support long-term demand growth.

Growth of Green Construction and Sustainable Infrastructure

The construction sector is increasingly utilizing bio-based insulation materials, fiberboards, and composite reinforcement products. Kenaf-based construction materials offer thermal insulation benefits, reduced embodied carbon, and improved sustainability credentials compared to traditional alternatives. Government investments in green buildings, energy-efficient infrastructure, and net-zero construction initiatives are driving demand. The increasing adoption of green building certification programs across developed and emerging economies further supports market expansion.

Kenaf Market Restraints

Limited Processing Infrastructure

Despite growing commercial demand, processing infrastructure remains underdeveloped in several key cultivation regions. The availability of decortication facilities, fiber treatment plants, and advanced composite manufacturing capabilities remains limited outside major producing countries. This creates supply chain inefficiencies and increases transportation costs, affecting market competitiveness. Expanding processing capacity remains a critical requirement for future market development.

Competition from Alternative Natural Fibers

Kenaf competes directly with hemp, jute, flax, sisal, and other established natural fibers that benefit from mature supply chains and broader market recognition. Buyers often evaluate multiple natural fiber options based on price, performance, and availability. As a result, market participants must continuously improve fiber quality, processing efficiency, and application development to maintain competitiveness against alternative materials.

Kenaf Market Opportunities

Electric Vehicle Lightweighting Initiatives

The rapid expansion of electric vehicle production presents significant opportunities for kenaf suppliers and composite manufacturers. Vehicle manufacturers are under pressure to reduce component weight to maximize battery performance and driving range. Kenaf composites can reduce component weight while maintaining structural integrity and sustainability requirements. The growing adoption of electric mobility across Europe, China, and North America is expected to create substantial new demand for high-performance natural fiber composites.

Green Building Materials and Infrastructure Development

Governments worldwide are increasing investments in sustainable infrastructure and environmentally friendly construction materials. Kenaf-based insulation products, composite panels, and reinforcement materials offer attractive environmental benefits and align with green building standards. Urbanization in emerging economies, combined with stricter environmental regulations in developed markets, is expected to support long-term demand growth within the construction industry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 890 Million |

| Market Size in 2026 | USD 954.97 Million |

| Market Size in 2031 | USD 1358.28 Million |

| CAGR | 7.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Processed kenaf fiber represents the largest product segment, accounting for approximately 42% of total market revenue in 2025. Demand is primarily driven by automotive composites, nonwoven materials, and industrial applications requiring consistent fiber quality and enhanced mechanical performance. Raw kenaf fiber remains an important segment, particularly in agricultural and low-cost industrial applications. Kenaf pulp continues to gain traction in paper manufacturing and sustainable packaging applications, while kenaf-based composites are witnessing rapid growth due to increasing adoption across automotive and construction industries. Biomass products, including absorbents, animal bedding, and biofuel feedstocks, provide additional value-added opportunities for producers seeking to maximize crop utilization.

Application Insights

Automotive components constitute the largest application segment, representing approximately 28% of global market demand. Vehicle manufacturers continue to incorporate kenaf fibers into interior trim components, door panels, and acoustic insulation systems to achieve weight reduction targets. Construction materials are emerging as the fastest-growing application area, supported by demand for eco-friendly insulation, reinforcement panels, and sustainable building products. Pulp and paper applications maintain a strong market position, while growing demand for biodegradable packaging solutions is creating new opportunities. Agricultural applications, including mulch materials and animal bedding, remain important contributors to overall market demand.

Fiber Source Insights

Bast fiber dominates the market with approximately 63% share of global revenue owing to its superior tensile strength, durability, and suitability for composite reinforcement applications. The segment is widely utilized in automotive, industrial, and construction applications where mechanical performance is critical. Core fibers represent a significant secondary segment, finding application in absorbents, animal bedding, and lightweight composite materials. Whole stem utilization is increasingly gaining attention as manufacturers seek to improve raw material efficiency and reduce processing waste through integrated utilization approaches.

End-Use Industry Insights

The automotive industry remains the largest end-use sector, accounting for approximately 27% of total market demand. Increasing adoption of lightweight natural fiber composites in conventional and electric vehicles continues to support growth. Construction follows closely as one of the fastest-growing industries due to rising investment in sustainable building materials. Paper and packaging industries are increasingly utilizing kenaf pulp as a renewable fiber source, while textile manufacturers are exploring applications in industrial fabrics and nonwoven products. Emerging demand from consumer goods and bioenergy applications is further diversifying market opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Kenaf Market Segmentations

By Product Type

- Raw Kenaf Fiber

- Processed Kenaf Fiber

- Kenaf-Based Composites

- Kenaf Pulp

- Kenaf Biomass & By-products

By Application

- Automotive Components

- Building & Construction Materials

- Pulp & Paper

- Textiles & Nonwoven Products

- Agriculture & Horticulture

- Bioplastics & Sustainable Packaging

- Others

By Fiber Source

- Bast Fiber

- Core Fiber

- Whole Stem Fiber

By Processing Method

- Mechanical Processing

- Chemical Processing

- Enzymatic/Biological Processing

By End-Use Industry

- Automotive

- Construction

- Paper & Packaging

- Agriculture

- Textile & Apparel

- Consumer Goods

- Energy & Biofuels

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global kenaf market with approximately 44% share of total revenue in 2025. China represents the largest national market, accounting for nearly 18% of global demand due to extensive cultivation capacity, strong manufacturing activity, and growing adoption of natural fiber composites. India contributes approximately 8% of global demand, supported by government initiatives promoting natural fibers and sustainable agriculture. Malaysia and Thailand remain important producers and exporters of kenaf fiber, supplying both regional and international markets. Rapid industrialization and expanding automotive production continue to support regional demand growth.

Europe

Europe accounts for approximately 24% of global market revenue and remains one of the most technologically advanced markets for natural fiber composites. Germany leads regional consumption due to its large automotive manufacturing base and strong focus on sustainable materials. France, Italy, and the United Kingdom also contribute significantly to demand. Stringent environmental regulations and circular economy initiatives continue to encourage adoption across automotive, construction, and packaging industries.

North America

North America represents approximately 20% of global market demand, with the United States accounting for nearly 16% of worldwide consumption. Growth is driven by automotive composite applications, sustainable packaging initiatives, and increasing investment in green building materials. Research and development activities related to natural fiber composites continue to strengthen regional market competitiveness.

Latin America

Latin America currently accounts for approximately 6% of global demand, led primarily by Brazil. The region is witnessing growing interest in sustainable agricultural products and renewable industrial materials. Expanding bioeconomy initiatives and increasing industrial diversification are expected to support future market growth.

Middle East & Africa

The Middle East & Africa region represents approximately 6% of global market revenue and is projected to register the fastest growth rate during the forecast period. Growing investments in sustainable agriculture, green construction, and industrial diversification programs are driving demand. Countries such as South Africa, the UAE, and Saudi Arabia are increasingly exploring bio-based materials as part of broader sustainability initiatives.

Key Players in the Kenaf Market

- Kenaf Fiber Industries Sdn Bhd

- Procotex Corporation

- HempFlax Group

- Bast Fibers LLC

- International Kenaf Partners

- Ecofibre Limited

- Kenaf Eco Fibers Malaysia

- Shenyang Beijiang Kenaf

- Guangxi Sunhe Biotech

- Hubei Huiyao Kenaf Industrial

- Hunan Sunshine Bio-Tech

- Advance Bio Material

- The Natural Fibre Company

- Wild Fibres Ltd

- China Hemp Industrial Investment Holding