Fuel Cards Market Size

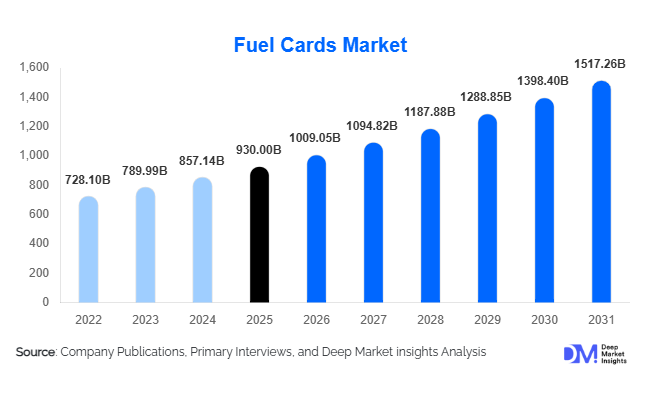

According to Deep Market Insights, the global fuel cards market size was valued at USD 930.0 billion in 2025 and is projected to grow from USD 1,009.05 billion in 2026 to reach USD 1,517.26 billion by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The fuel cards market growth is being driven by increasing commercial fleet operations, rising demand for centralized fuel expense management, growing digitalization of fleet payment systems, and the integration of telematics with payment platforms. Fuel cards have evolved from simple fuel payment tools into comprehensive fleet management solutions capable of tracking fuel consumption, vehicle maintenance expenses, toll payments, driver behavior, and operational efficiency. The rapid expansion of e-commerce logistics, last-mile delivery networks, and cross-border freight transportation is further strengthening market demand globally. Moreover, the emergence of hybrid mobility cards that support both conventional fuel purchases and electric vehicle charging is creating new growth opportunities as fleet operators transition toward sustainable transportation models.

Key Market Insights

- Transportation and logistics remains the largest end-use sector, accounting for more than 35% of total fuel card spending globally.

- Universal fuel cards are rapidly gaining market share, driven by their acceptance across multiple fuel station networks and value-added fleet management features.

- Europe dominates the global market, supported by mature commercial transport networks, regulatory compliance requirements, and widespread fleet card adoption.

- Asia-Pacific is the fastest-growing region, fueled by expanding logistics infrastructure and rising commercial vehicle fleets in China, India, and Southeast Asia.

- Digital fleet management integration, including telematics, AI-driven analytics, and mobile payment capabilities, is transforming fuel card functionality.

- Hybrid fuel and EV charging cards are emerging as a major innovation area as corporate fleets adopt electrification strategies.

Fuel Cards Market Trends

Integration of Fuel Cards with Fleet Telematics Platforms

Fleet operators increasingly seek integrated solutions that combine payment processing with real-time vehicle monitoring. Fuel card providers are partnering with telematics companies to offer consolidated dashboards capable of tracking fuel consumption, route optimization, driver behavior, maintenance schedules, and fraud detection. This trend is helping fleet managers reduce operational costs while improving regulatory compliance and asset utilization. Advanced analytics derived from integrated platforms are enabling predictive maintenance and fuel efficiency improvements, creating substantial value for large fleet operators. The growing adoption of cloud-based fleet management systems is expected to further accelerate demand for connected fuel card solutions.

Expansion of Multi-Energy Mobility Cards

The global transition toward low-emission transportation is reshaping the fuel cards market. Fleet operators increasingly require payment solutions capable of supporting diesel, gasoline, LNG, CNG, hydrogen, and EV charging transactions through a single platform. As a result, fuel card issuers are launching multi-energy mobility cards that facilitate seamless payments across traditional fueling stations and electric charging networks. These products are particularly attractive to mixed fleets undergoing gradual electrification. The trend is expected to strengthen significantly as governments implement stricter emissions regulations and corporate sustainability initiatives gain momentum.

Fuel Cards Market Drivers

Growth of Commercial Transportation and Logistics Fleets

The expansion of global logistics, e-commerce fulfillment networks, and freight transportation activities continues to drive demand for fuel cards. Transportation companies increasingly rely on centralized payment systems to manage fuel expenditures across geographically dispersed fleets. The growing complexity of fleet operations, combined with rising fuel prices, is encouraging businesses to adopt fuel cards to improve spending visibility, reduce administrative burdens, and negotiate volume-based fuel discounts. Rapid growth in cross-border trucking and regional distribution networks further supports long-term market expansion.

Rising Need for Fuel Cost Optimization and Fraud Prevention

Fuel remains one of the largest operating expenses for fleet operators worldwide. Fuel cards provide real-time transaction monitoring, spending controls, driver authentication, and fraud detection capabilities that help organizations minimize unauthorized purchases and fuel theft. Advanced reporting functions enable businesses to identify inefficiencies and improve budgeting accuracy. As organizations prioritize operational cost control amid volatile fuel prices, adoption of fuel card programs continues to accelerate across commercial fleet segments.

Fuel Cards Market Restraints

Cybersecurity and Data Privacy Concerns

As fuel cards become increasingly digitized and integrated with fleet management platforms, cybersecurity risks have emerged as a significant concern. Fuel card issuers must invest heavily in payment security, fraud detection systems, and data protection infrastructure to prevent unauthorized access and financial losses. Compliance with evolving data privacy regulations across multiple jurisdictions also increases operational complexity and costs.

Transition Toward Fully Electric Mobility

While fuel cards are adapting through EV charging integration, the long-term transition toward fully electric transportation presents challenges for traditional fuel card business models. Some fleet operators may gradually reduce conventional fuel purchases, requiring providers to diversify service offerings and invest in broader mobility payment ecosystems. Companies that fail to adapt to evolving fleet energy requirements may experience slower growth over the coming decade.

Fuel Cards Market Opportunities

Hybrid Fuel and EV Charging Ecosystems

The global electrification of transportation represents one of the largest growth opportunities for fuel card providers. Commercial fleets are increasingly operating mixed vehicle portfolios that include internal combustion engines, hybrid vehicles, and battery-electric vehicles. Multi-energy cards capable of handling both fuel purchases and EV charging transactions provide a unified expense management platform. Providers that establish partnerships with charging network operators and fleet electrification service providers are expected to capture significant market share as EV adoption accelerates globally.

Expansion Across Emerging Logistics Markets

Rapid industrialization, infrastructure development, and e-commerce expansion in Asia-Pacific, Latin America, and the Middle East are creating substantial opportunities for fuel card issuers. Many fleet operators in these regions still rely on manual reimbursement systems and cash-based fuel payments. Digital fuel card adoption offers significant efficiency gains while improving transparency and regulatory compliance. Governments investing in transportation corridors and logistics modernization programs further support market penetration opportunities.

AI-Driven Fleet Analytics and Predictive Management

Fuel card providers are increasingly leveraging artificial intelligence and machine learning to deliver advanced fleet optimization capabilities. AI-powered platforms can identify fuel consumption anomalies, optimize routes, forecast maintenance requirements, and reduce operating expenses. As fleet operators seek data-driven decision-making tools, value-added analytics services are becoming a major source of differentiation and recurring revenue generation for market participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 930.0 Billion |

| Market Size in 2026 | USD 1009.05 Billion |

| Market Size in 2031 | USD 1517.26 Billion |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Card Type Insights

Universal fuel cards dominated the global fuel cards market in 2025, accounting for approximately 42% of total market revenue. Their leadership position is primarily driven by the increasing need for operational flexibility among fleet operators managing vehicles across multiple geographies and fuel networks. Unlike branded cards, universal fuel cards can be used across numerous fuel stations, allowing fleet managers to optimize route planning, reduce refueling downtime, and negotiate better fuel procurement strategies. The growth of third-party logistics (3PL) providers, long-haul trucking companies, and multinational transportation fleets has further accelerated adoption, as these operators require unrestricted fueling access across regional and national boundaries.

The segment has also benefited from the growing integration of value-added services, including telematics connectivity, fuel fraud monitoring, maintenance expense tracking, toll management, and digital reporting capabilities. Universal card providers increasingly offer centralized fleet dashboards that enable businesses to analyze fuel consumption patterns and improve operational efficiency. Meanwhile, hybrid mobility cards are emerging as the fastest-growing card category, supported by the electrification of commercial fleets and increasing demand for unified payment solutions covering diesel, gasoline, LNG, CNG, and EV charging transactions. The transition toward multi-energy transportation ecosystems is expected to significantly expand the addressable market for universal and hybrid card providers over the forecast period.

Application Insights

Fuel purchasing remained the largest application segment, accounting for nearly 58% of total market demand in 2025. The segment's dominance is directly linked to the fundamental role of fuel expenditure within fleet operating costs, which typically represents between 25% and 40% of total transportation expenses for commercial operators. Fuel cards enable businesses to centralize fuel procurement, improve expenditure visibility, implement driver-level spending controls, and secure volume-based fuel discounts, making them an essential operational tool for fleet-intensive industries.

The segment continues to benefit from rising freight transportation volumes, expanding e-commerce delivery networks, and increasing commercial vehicle utilization globally. Additionally, volatile fuel prices have heightened the importance of fuel consumption monitoring and procurement optimization, encouraging fleet operators to adopt sophisticated fuel card programs. While fuel purchasing remains the core application, fleet expense management is gaining traction as organizations seek consolidated management of maintenance costs, parking fees, toll payments, and vehicle servicing expenses. Furthermore, EV charging payments represent the fastest-growing application category as commercial fleet electrification accelerates across Europe, North America, and parts of Asia-Pacific.

Vehicle Type Insights

Heavy commercial vehicles (HCVs) accounted for approximately 38% of global fuel card demand in 2025, making them the leading vehicle category. The segment's dominance stems from exceptionally high fuel consumption levels and extensive operational mileage associated with long-haul freight transportation. Trucking operators, logistics providers, and freight carriers rely heavily on fuel cards to manage large-scale fuel expenditures, improve route efficiency, and monitor driver spending across extensive transportation networks.

The continued expansion of international trade, cross-border transportation corridors, and e-commerce fulfillment infrastructure has strengthened demand from heavy commercial fleets. Additionally, stricter emissions regulations and fuel efficiency requirements are encouraging fleet operators to utilize fuel card data analytics to optimize vehicle utilization and reduce fuel wastage. Light commercial vehicles (LCVs) represent the fastest-growing vehicle segment due to the rapid expansion of urban delivery services, same-day delivery models, and last-mile logistics operations. Growth in parcel delivery and food delivery services is creating new opportunities for fuel card providers targeting smaller commercial fleet operators.

Fleet Size Insights

Large fleets with more than 500 vehicles represented approximately 46% of global fuel card spending in 2025. This segment remains the largest customer category because large enterprises derive the greatest financial benefits from centralized fuel management, fleet-wide reporting, telematics integration, and automated expense reconciliation. Organizations operating large vehicle fleets typically face substantial administrative burdens associated with fuel procurement, making fuel cards a critical tool for cost control and operational efficiency.

The segment is also benefiting from increasing investments in digital fleet management technologies, including AI-based route optimization, predictive maintenance systems, and driver performance monitoring platforms. Fuel cards serve as an important data source within these broader fleet management ecosystems. Furthermore, multinational logistics providers and transportation companies increasingly require integrated payment solutions capable of supporting operations across multiple countries and fuel networks. While large fleets continue to dominate market revenue, adoption among small and medium-sized fleets is accelerating due to the availability of cloud-based fuel card platforms that reduce implementation costs and simplify fleet administration.

End-Use Industry Insights

Transportation and logistics remained the largest end-use industry, contributing approximately 35% of total fuel card market demand in 2025. The sector's leadership position is primarily driven by rising global freight movement, increasing cross-border trade activity, and the continued expansion of e-commerce fulfillment networks. Fuel cards provide transportation companies with centralized visibility into one of their largest operating expenses while enabling effective management of geographically dispersed vehicle fleets.

The rapid growth of third-party logistics providers, warehousing operators, courier services, and last-mile delivery companies continues to generate substantial demand for advanced fuel management solutions. In addition, transportation companies increasingly leverage fuel card data to improve fleet productivity, optimize routing strategies, and enhance regulatory compliance. Construction and infrastructure represents another significant demand segment due to the extensive use of fuel-intensive heavy equipment and commercial vehicles. Government infrastructure investments across North America, Asia-Pacific, and the Middle East are expected to support fuel card adoption among construction contractors and equipment operators throughout the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Fuel Cards Market Segmentations

By Card Type

- Branded Fuel Cards

- Universal Fuel Cards

- Merchant Fuel Cards

- Hybrid Mobility Cards

By Application

- Fuel Refueling

- Vehicle Maintenance & Repair

- Toll Payments

- Parking Payments

- Fleet Expense Management

- EV Charging Payments

- Roadside Assistance Payments

- Vehicle Washing & Ancillary Services

By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles (LCVs)

- Medium Commercial Vehicles (MCVs)

- Heavy Commercial Vehicles (HCVs)

- Buses & Coaches

- Mixed Commercial Fleets

By Fleet Size

- Small Fleets (1–50 Vehicles)

- Medium Fleets (51–500 Vehicles)

- Large Fleets (501–5,000 Vehicles)

- Enterprise Fleets (Above 5,000 Vehicles)

By End-Use Industry

- Transportation & Logistics

- Retail & E-Commerce Delivery

- Construction & Infrastructure

- Oil & Gas

- Government & Municipal Fleets

- Mining

- Utilities

- Manufacturing

- Agriculture

- Passenger Transportation

- Emergency Services

- Corporate Mobility Fleets

Regional Insights

Europe

Europe accounted for approximately 34% of global fuel card market revenue in 2025, making it the largest regional market. The region's leadership is supported by a highly developed commercial transportation ecosystem, extensive cross-border freight activity, and one of the world's most mature fleet management industries. The United Kingdom, Germany, France, Italy, Spain, and the Netherlands collectively represent the largest demand centers due to their large commercial vehicle populations and advanced logistics networks.

Several structural growth drivers continue to support market expansion in Europe. These include stringent fleet compliance regulations, increasing fuel tax reporting requirements, rising adoption of telematics systems, and widespread implementation of digital fleet management solutions. Furthermore, Europe is leading the global transition toward sustainable transportation, encouraging fuel card providers to develop integrated fuel and EV charging solutions. The region's aggressive decarbonization targets, expanding charging infrastructure, and corporate sustainability commitments are expected to further accelerate demand for multi-energy fleet cards during the forecast period.

North America

North America represented approximately 29% of global market value in 2025. The United States remains the dominant contributor, supported by one of the world's largest trucking industries, extensive interstate freight transportation networks, and high commercial fuel consumption levels. Canada also contributes significantly through cross-border trade activities and increasing fleet digitization initiatives.

Key growth drivers include rising freight transportation demand, expansion of e-commerce logistics operations, increasing adoption of fleet telematics, and growing demand for data-driven fuel optimization solutions. Fleet operators across North America are increasingly integrating fuel cards with route optimization software, predictive maintenance systems, and driver performance monitoring platforms. The region is also witnessing strong adoption of mobile payment technologies and contactless fueling solutions, which continue to enhance operational efficiency and strengthen market growth prospects.

Asia-Pacific

Asia-Pacific accounted for approximately 24% of global market demand in 2025 and remains the fastest-growing region, with annual growth exceeding 11%. China represents the largest regional market due to its vast logistics sector, extensive manufacturing base, and rapidly expanding freight transportation network. India is emerging as one of the fastest-growing national markets, supported by increasing highway infrastructure investments, rising commercial vehicle registrations, and growing adoption of digital payment platforms.

Regional growth is primarily driven by industrialization, urbanization, e-commerce expansion, and government investments in transportation infrastructure. Major initiatives such as China's logistics modernization programs and India's highway development projects are creating substantial demand for commercial fleet management solutions. Additionally, rising fuel costs, increasing fleet sizes, and growing awareness of operational efficiency benefits are accelerating fuel card penetration across emerging Asian economies. Southeast Asian countries are also experiencing rapid adoption as regional supply chains continue to expand.

Latin America

Brazil, Mexico, Argentina, and Chile remain the primary fuel card markets in Latin America. Although overall market penetration remains below levels observed in Europe and North America, the region offers considerable long-term growth potential due to ongoing modernization of transportation and logistics operations.

Market expansion is being driven by increasing investments in freight transportation infrastructure, growth in agribusiness logistics, rising adoption of digital payment systems, and stronger regulatory focus on fuel expense transparency. Brazil leads regional demand owing to its extensive road freight network and large agricultural transportation sector. Mexico continues to benefit from manufacturing growth and cross-border trade with the United States, while Chile and Argentina are increasingly adopting fuel management solutions to improve fleet efficiency and reduce operational costs.

Middle East & Africa

The Middle East and Africa region is experiencing steady growth, led by the UAE, Saudi Arabia, South Africa, and emerging Gulf logistics hubs. Although market penetration remains relatively lower than developed regions, ongoing infrastructure investments and transportation sector modernization are creating favorable conditions for fuel card adoption.

Key growth drivers include large-scale government infrastructure projects, expanding logistics corridors, increasing commercial vehicle fleets, and economic diversification initiatives across Gulf Cooperation Council countries. Saudi Arabia's Vision 2031 and major logistics development projects across the UAE are stimulating demand for advanced fleet management solutions. In Africa, growth is supported by mining operations, expanding transportation networks, and increasing adoption of digital financial technologies. The region's growing focus on fleet efficiency, fuel cost control, and transportation digitization is expected to support sustained market expansion over the coming years.

Key Players in the Fuel Cards Market

- WEX Inc.

- Fleetcor Technologies (Corpay)

- Shell plc

- BP plc

- TotalEnergies SE

- Exxon Mobil Corporation

- Circle K

- DKV Mobility Group

- U.S. Bancorp Voyager Fleet Systems

- Edenred

- FLEETMAXX Solutions

- Radius Payment Solutions

- Allstar Business Solutions

- Fuelman

- Comdata Inc.