Satellite Photography Service Market Size

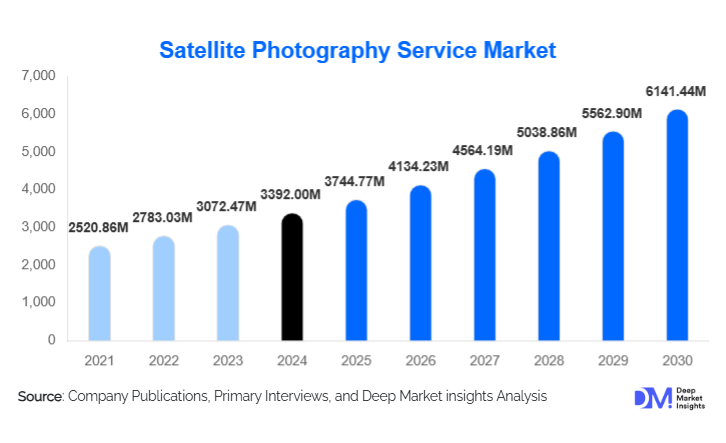

According to Deep Market Insights, the global satellite photography service market size was valued at USD 3392.00 million in 2025 and is projected to grow from USD 3744.77 million in 2026 to reach USD 6141.44 million by 2031, expanding at a CAGR of 10.40% during the forecast period (2026–2031). Market expansion is driven by the rapid proliferation of low-cost smallsat constellations, rising enterprise adoption of AI-powered geospatial analytics, and substantial growth in sovereign earth-observation investments across North America, Europe, and Asia-Pacific.

Key Market Insights

- Shift from raw imagery to intelligence-as-a-service (IaaS) is reshaping monetization models, with enterprises demanding automated insights over standalone imagery.

- Analytics and API-based subscriptions are the fastest-growing revenue streams, supported by cloud-native delivery and increasing revisit frequencies.

- North America dominates the global market due to strong defense procurement, commercial adoption, and technological leadership.

- Asia-Pacific is the fastest-growing region, propelled by national EO programs, private satellite launches, and expanding industrial use cases.

- SAR and hyperspectral imaging capabilities are gaining traction, enabling all-weather monitoring and new applications in mining, forestry, and disaster management.

- Government investments in sovereign earth observation continue to accelerate, creating long-term demand for tasking services, secure imagery delivery, and national constellations.

Satellite Photography Service Market Trends

AI-Driven Earth Intelligence Becoming the Core Product

The market is witnessing a decisive shift toward AI-powered insights that transform satellite imagery into automated, decision-ready intelligence. Enterprises increasingly rely on models that detect changes, classify objects, quantify environmental impacts, and forecast risk. Insurance providers use AI-enhanced satellite data for claims triage and exposure modeling, while agriculture firms depend on vegetation indices and yield forecasts derived from multi-sensor imagery. This trend is redefining value creation, moving from pixel sales to full-stack intelligence ecosystems where imagery, analytics, and APIs are tightly integrated. As a result, verticalized SaaS platforms offering agriculture, energy, ESG, or logistics intelligence are becoming industry-standard.

Multi-Sensor Fusion: SAR, Hyperspectral & Optical Integration

Satellite operators are rapidly deploying multi-sensor constellations that merge optical, SAR, and hyperspectral data streams. SAR adoption is accelerating because of its ability to capture images through cloud cover, smoke, and nighttime conditions, critical for maritime monitoring, disaster response, and infrastructure surveillance. Hyperspectral imaging is enabling new applications in mineral analysis, forestry health diagnostics, carbon measurement, and chemical detection. Multi-layered fusion of sensors provides analytics providers with richer data for training AI models, allowing them to offer more accurate insights and expand the monetizable use cases across energy, mining, and environmental industries.

Satellite Photography Service Market Drivers

Proliferation of Smallsat Constellations

Dramatically reduced satellite manufacturing and launch costs have enabled operators to deploy large smallsat constellations capable of sub-daily revisit rates. These advancements have transformed the economics of imagery collection, making high-frequency monitoring accessible to industries that previously relied on infrequent or costly datasets. Improved revisit rates also support mission-critical applications such as port congestion tracking, supply chain visibility, and real-time disaster assessment. As constellation density increases, service providers can offer more granular intelligence at competitive pricing, expanding the market’s addressable customer base.

Growing Enterprise Adoption of AI & Cloud-Based Analytics

Enterprises increasingly prefer end-to-end solutions that convert raw satellite photos into actionable insights. Cloud-native architectures, automated workflows, and scalable APIs have made satellite data easier to consume, integrate, and operationalize. Sectors such as insurance, energy, agriculture, and urban planning now rely on geospatial intelligence for routine decision-making. The ability to deploy models at scale, detect anomalies, automate asset monitoring, and generate sustainability metrics is a major growth catalyst, turning satellite imagery into an essential data layer for modern digital ecosystems.

Rising Government Demand for Sovereign Geospatial Capabilities

Governments worldwide are investing heavily in earth observation infrastructure to enhance national security, environmental monitoring, and disaster resilience. Dedicated satellite tasking, secure image pipelines, and sovereign data centers are becoming strategic priorities. Long-term defense and civil contracts provide stable, high-margin revenue for providers. The surge in national satellite programs, particularly in Asia-Pacific and the Middle East, is reshaping global procurement patterns and strengthening demand for commercial tasking, hosting, and analytics services.

Satellite Photography Service Market Restraints

Data Fragmentation & Complex Licensing Models

The satellite imagery landscape remains fragmented across optical, SAR, hyperspectral, and open-data sources, often distributed under varying licensing restrictions. Enterprises face challenges in understanding usage rights, integrating heterogeneous datasets, and achieving consistent quality. Complex pricing structures and inconsistent licensing frameworks slow procurement cycles and increase onboarding friction. Providers must simplify licensing, unify platforms, and offer transparent pricing to unlock broader enterprise adoption.

Regulatory & Export Control Limitations

High-resolution satellite imagery is subject to export controls, national security restrictions, and localized data-protection policies. These constraints can limit market access, restrict the distribution of sensitive datasets, and create compliance burdens for providers serving international clients. Additionally, some regions require imagery to be stored or processed within national borders, raising infrastructure costs. These regulatory hurdles represent a significant constraint for scaling global operations.

Satellite Photography Service Market Opportunities

Subscription-Based Earth Intelligence Platforms

The most significant opportunity lies in transitioning from one-time image sales to recurring intelligence-as-a-service platforms. Providers offering vertical solutions, such as crop monitoring dashboards, ESG risk scoring, or infrastructure surveillance, can unlock higher ARPU and long-term customer retention. SaaS-based delivery also deepens integration with enterprise workflows, making satellite-derived insights indispensable for daily operations across insurance, agriculture, and logistics sectors.

National Constellations & Sovereign Tasking Partnerships

Emerging economies are accelerating investments in earth observation infrastructure, creating strong demand for hosted payloads, dedicated tasking agreements, and turnkey constellation deployments. Satellite operators can capitalize by offering build-and-operate models, secure data channels, and in-country analytics nodes. Nations across APAC, the Middle East, and Latin America seek greater autonomy in geospatial intelligence, opening multimillion-dollar long-term contract opportunities.

Integration of SAR & Hyperspectral Analytics

Advanced sensors unlock new high-margin applications. SAR enables all-weather surveillance for maritime, defense, and disaster response, while hyperspectral imaging supports mineral mapping, vegetation diagnostics, and pollution detection. Companies developing AI models that fuse these datasets with optical imagery can dominate emerging markets such as carbon verification, precision mining, and large-scale habitat monitoring.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3392 Million |

| Market Size in 2026 | USD 3744.77 Million |

| Market Size in 2031 | USD 6141.44 Million |

| CAGR | 10.40% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Premium analytics-driven satellite services dominate the market as enterprises increasingly demand intelligence rather than raw imagery. High-value offerings include orthorectified mosaics, multi-sensor composites, and automated object detection models that support actionable decision-making. Mid-range solutions such as API-accessed image feeds and standardized monitoring subscriptions are expanding rapidly due to their affordability and ease of integration into cloud environments. Budget-oriented offerings, primarily archive imagery and open-data enhancements, attract smaller organizations and research institutions that require historical insights without real-time constraints. The growing availability of SAR and hyperspectral products is also elevating market sophistication, allowing providers to differentiate through advanced spectral and temporal capabilities.

Application Insights

Infrastructure and asset monitoring represent one of the fastest-growing applications as utilities, energy companies, and logistics firms adopt satellite analytics for routine surveillance. Agricultural applications remain foundational, with crop health analysis, yield forecasting, and soil-moisture tracking driving widespread subscription adoption. In insurance, rapid damage assessment and claims validation have become essential use cases following natural disasters. Defense and security continue to generate high-value demand for high-resolution tasking and near-real-time monitoring. Emerging applications include ESG compliance, carbon accounting, biodiversity mapping, and supply-chain verification, areas where satellite data provides independent and auditable evidence for global sustainability initiatives.

Distribution Channel Insights

Cloud-based APIs and data platforms dominate distribution, enabling seamless integration into enterprise systems. These channels support scalable consumption models and allow developers to embed satellite data directly into AI workflows. Enterprise sales teams remain crucial for securing large defense and government contracts that require custom SLAs and secure pipelines. Marketplace integrations with hyperscalers are expanding reach among developers and data scientists. Direct-to-enterprise SaaS products are rapidly emerging as providers package vertical intelligence modules for agriculture, insurance, and urban planning. As customer sophistication grows, subscription models increasingly replace traditional per-image licensing.

End-Use / User Type Insights

Large enterprises, including insurers, agribusinesses, energy utilities, and logistics firms, constitute the highest-value user segment due to their continuous need for monitoring and analytics. Government agencies represent a major revenue base, relying on satellite intelligence for national security, environmental assessment, and disaster management. Small and medium-sized businesses are expanding adoption through API-based platforms and lower-cost monitoring subscriptions. Research institutions, NGOs, and climate organizations increasingly rely on satellite imagery for conservation, humanitarian response, and environmental reporting.

Explore more data points, trends and opportunities Download Free Sample Report

Satellite Photography Service Market Segmentations

By Product / Service Type

- Raw Imagery Licensing

- On-Demand Tasking Services

- Processed Imagery Products

- Analytics & Intelligence Services

- API & Platform Subscriptions

- SAR & Hyperspectral Imaging Services

- Geospatial Integration & Consulting Services

By Application

- Agriculture & Forestry Monitoring

- Defense & Intelligence Surveillance

- Insurance & Disaster Assessment

- Energy & Utilities Asset Monitoring

- Infrastructure & Urban Planning

- Environmental & Climate Analysis

- Maritime & Logistics Tracking

- ESG & Carbon Accounting Applications

By End-User / Industry Vertical

- Government & Defense Agencies

- Agriculture & Agritech Firms

- Insurance & Reinsurance Companies

- Energy, Oil & Gas, and Utilities

- Logistics, Shipping & Supply Chain Providers

- Mining & Natural Resources Companies

- Environmental and Climate Research Organizations

- Enterprise SaaS & Cloud-Based Data Consumers

Regional Insights

North America

North America is the largest regional market, driven by strong adoption in defense, agriculture, insurance, and energy sectors. The U.S. leads global spending on satellite tasking, multi-sensor analytics, and sovereign geospatial capabilities. Commercial enterprises in the region increasingly rely on satellite APIs and cloud-based intelligence platforms for operational decision-making. Canada contributes additional demand through environmental monitoring and Arctic surveillance programs. Overall, North America accounts for approximately 40% of the global market in 2025.

Europe

Europe represents a mature satellite imagery market with robust participation from defense, civil-government, and commercial buyers. Strong regulatory frameworks supporting sustainability, climate reporting, and environmental monitoring drive demand for high-frequency monitoring solutions. Countries such as Germany, France, and the U.K. maintain significant investments in both national EO capabilities and commercial analytics services. Europe’s commitment to green transition initiatives further accelerates the adoption of satellite data across infrastructure, forestry, and ESG-related applications.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, supported by large-scale national space programs and rising private-sector investment. China, India, Japan, and South Korea are deploying increasingly sophisticated EO assets and expanding commercial demand for agri-intelligence, infrastructure monitoring, and maritime security. India’s rapidly growing private satellite ecosystem and strong agricultural footprint make it one of the region’s most dynamic markets. Southeast Asian nations are also accelerating the adoption of urban planning, disaster resilience, and environmental management.

Latin America

Latin America shows rising adoption driven by agriculture, forestry, and mining applications. Brazil leads demand through large-scale monitoring programs for the Amazon, agricultural surveillance, and environmental compliance. Chile and Argentina exhibit strong use cases in mining and climate analytics. Although the market size is smaller relative to major regions, demand is strengthening as governments modernize geospatial infrastructure and enterprises embrace digital transformation.

Middle East & Africa

The Middle East is expanding rapidly due to strong investments in sovereign EO capabilities, national security monitoring, and infrastructure management. The UAE and Saudi Arabia lead demand for high-resolution tasking and analytics platforms. Africa, while home to diverse environmental monitoring needs, is a developing market where adoption is driven by agriculture, climate resilience, and conservation projects. South Africa, Kenya, and Nigeria are key adopters of geospatial analytics for agricultural planning and environmental protection.

Key Players in the Satellite Photography Service Market

- Maxar Technologies

- Airbus Defence & Space

- Planet Labs PBC

- BlackSky Technology

- ICEYE

- Capella Space

- Satellogic

- Spire Global

- Thales Group

- L3Harris Technologies

- ImageSat International

- European Space Imaging

- EOS Data Analytics

- SkyWatch

- EarthDaily Analytics