Online Travel Agent Market Size

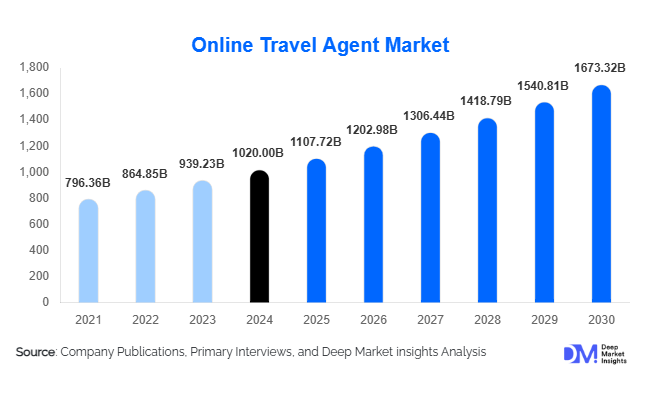

According to Deep Market Insights, the global online travel agent (OTA) market size was valued at approximately USD 1,020 billion in 2025 and is projected to grow from USD 1,107.72 billion in 2026 to reach nearly USD 1,673.32 billion by 2031, expanding at a CAGR of around 8.6% during the forecast period (2026–2031). The OTA market growth is primarily driven by rising global travel demand, increasing smartphone and internet penetration, growing preference for digital booking platforms, and the continued shift from offline to online travel planning across both leisure and corporate segments.

Key Market Insights

- Mobile-based bookings dominate the OTA market, accounting for more than half of global transactions due to app-based loyalty programs and convenience.

- Asia-Pacific represents the largest regional market, driven by rapid growth in domestic and outbound travel from China, India, and Southeast Asia.

- Air ticketing remains the largest booking segment, benefiting from high-frequency travel and strong price-comparison behavior.

- Leisure travel contributes the majority of OTA revenue, supported by experiential tourism and flexible work arrangements.

- Corporate travel bookings are the fastest-growing end-use segment, driven by digital travel management adoption.

- AI-driven personalization and dynamic pricing are reshaping customer engagement and conversion rates.

Online Travel Agent Market Trends

Mobile-First and App-Centric Booking Ecosystems

Mobile applications have become the primary interface for OTA transactions, accounting for an estimated 54% of global bookings in 2025. OTAs are investing heavily in app-only discounts, integrated wallets, real-time alerts, and loyalty programs to increase user retention. Super-app models, particularly in Asia-Pacific, are bundling travel bookings with payments, insurance, and local experiences, enhancing ecosystem stickiness and transaction frequency.

AI-Powered Personalization and Dynamic Packaging

Artificial intelligence is increasingly embedded across OTA platforms to personalize search results, recommend bundled travel packages, and optimize pricing in real time. AI-driven personalization has improved conversion rates and average booking values, particularly for hotels and vacation packages. Dynamic packaging that combines flights, accommodations, ground transport, and experiences is gaining traction, allowing OTAs to differentiate offerings and improve margins.

Online Travel Agent Market Drivers

Rising Global Tourism and Travel Activity

The recovery and expansion of global tourism activity continue to be a major driver for the OTA market. Both international and domestic travel volumes have surpassed pre-pandemic levels in several regions, increasing booking volumes across flights, hotels, and experiences. Emerging markets are contributing significantly to incremental demand, particularly for domestic travel bookings.

Increasing Digital Adoption and Price Transparency

Consumers increasingly prefer OTAs due to price transparency, ease of comparison, and access to a wide range of inventory. Digital payment adoption and improved trust in online transactions have further strengthened OTA penetration, particularly in developing economies where offline booking once dominated.

Online Travel Agent Market Restraints

Margin Pressure from Direct Supplier Channels

Airlines and hotel chains are aggressively promoting direct bookings through exclusive discounts and loyalty benefits, placing pressure on OTA commission margins. Rising customer acquisition costs and reduced commissions pose challenges to long-term profitability for OTA platforms.

Regulatory and Data Privacy Challenges

Cross-border digital taxation, data localization laws, and data privacy regulations increase compliance costs and operational complexity for global OTAs. Regulatory fragmentation across regions remains a persistent restraint for seamless international operations.

Online Travel Agent Market Opportunities

Corporate Travel Digitization

The digital transformation of corporate travel management presents a high-value opportunity for OTAs. Platforms offering integrated expense management, policy compliance, sustainability reporting, and analytics are seeing strong adoption from multinational corporations, supporting higher-margin recurring revenue streams.

Expansion in Emerging Travel Markets

Rapid growth in outbound and domestic travel from India, Southeast Asia, Latin America, and the Middle East offers significant untapped potential. Localized platforms, vernacular language support, and integration with regional transport providers can accelerate OTA adoption in these markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1020 Billion |

| Market Size in 2026 | USD 1107.72 Billion |

| Market Size in 2031 | USD 1673.32 Billion |

| CAGR | 8.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Booking Type Insights

Air ticketing dominates the OTA market, accounting for approximately 38% of total revenue in 2025, driven by high transaction frequency and fare comparison behavior. Hotel and accommodation bookings represent the second-largest segment, benefiting from bundled offerings and dynamic pricing. Vacation packages are growing rapidly as travelers seek convenience and cost savings through bundled flight-and-hotel deals. Car rentals, rail and bus ticketing, cruises, and travel experiences collectively contribute a growing share as OTAs expand into ancillary services.

Platform Type Insights

Mobile applications lead the platform segment with over half of global OTA transactions, followed by mobile web platforms. Desktop-based bookings remain relevant for complex itineraries and corporate travel planning, but continue to lose share as mobile UX improves. App-based platforms are driving higher engagement and repeat usage through personalized notifications and loyalty rewards.

Traveler Type Insights

Leisure travelers account for nearly 62% of OTA demand, supported by experiential travel trends and flexible work models. Business travelers represent a smaller but faster-growing segment, driven by digital corporate travel management solutions. Group and solo travelers are increasingly using OTAs for customized itineraries and budget optimization.

End-Use Insights

Individual consumers dominate OTA usage, contributing around 68% of total bookings. Corporate clients represent the fastest-growing end-use segment, expanding at nearly 9.5% CAGR, driven by enterprise adoption of digital travel tools. Government and institutional bookings are emerging as niche applications, particularly for centralized travel procurement.

Explore more data points, trends and opportunities Download Free Sample Report

Online Travel Agent Market Segmentations

By Booking Type

- Air Ticketing

- Hotel & Accommodation Booking

- Vacation Packages (Flight + Hotel + Add-ons)

- Car Rental Services

- Rail & Bus Ticketing

- Cruises & Ferry Booking

- Travel Experiences & Activities

By Platform Type

- Desktop-Based Platforms

- Mobile Web Platforms

- Mobile Application-Based Platforms

By Traveler Type

- Leisure Travelers

- Business Travelers

- Group Travelers

- Solo Travelers

By Pricing Model

- Agency (Commission-Based) Model

- Merchant (Net Rate / Mark-up) Model

- Advertising & Meta-search Model

- Subscription & Loyalty-Based Model

By End User

- Individual Consumers

- Corporate Clients

- Travel Management Companies

- Government & Institutional Users

Regional Insights

Asia-Pacific

Asia-Pacific is the largest OTA market, accounting for roughly 41% of global revenue in 2025. China, India, Japan, and Southeast Asia drive demand through mobile-first adoption, strong domestic tourism, and expanding middle-class populations. India is the fastest-growing national market, with double-digit growth supported by low-cost carriers and digital payments.

North America

North America represents approximately 23% of the global OTA market, led by the United States. High booking values, strong corporate travel demand, and mature digital infrastructure support steady growth. Innovation in AI-driven personalization remains a key differentiator in this region.

Europe

Europe accounts for about 21% of global OTA revenue, driven by cross-border travel within the EU. The U.K., Germany, France, and Spain are major contributors, with sustainability-focused travel gaining importance.

Latin America

Latin America holds around 6% of the market, led by Brazil and Mexico. Growth is driven by domestic travel and increasing mobile adoption, though pricing sensitivity remains high.

Middle East & Africa

The Middle East & Africa region contributes approximately 9% of global OTA revenue. The UAE and Saudi Arabia lead demand, supported by tourism investments and high outbound travel spending.

Key Players in the Online Travel Agent Market

- Booking Holdings

- Expedia Group

- Trip.com Group

- Airbnb

- MakeMyTrip

- eDreams ODIGEO

- Despegar

- Webjet Limited

- TripAdvisor

- Traveloka

- OYO

- TUI Group

- Hopper

- Cleartrip

- Ctrip International