E-Commerce Household Appliances Market Size

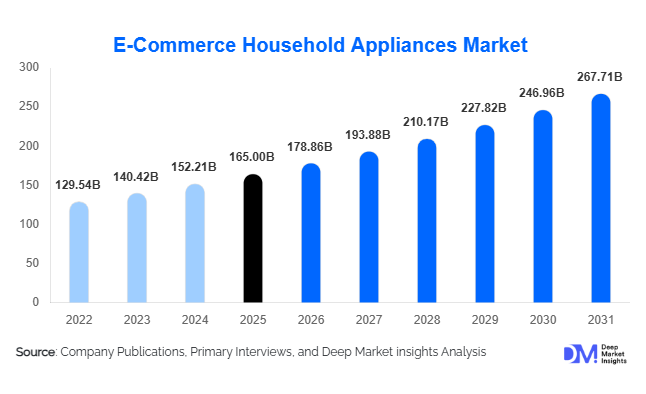

According to Deep Market Insights, the global e-commerce household appliances market size was valued at USD 165.0 billion in 2025 and is projected to grow from USD 178.86 billion in 2026 to reach USD 267.71 billion by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The market growth is primarily driven by the increasing penetration of online retail platforms, rising adoption of smart home appliances, expanding smartphone usage, and growing consumer preference for convenient doorstep delivery and digital financing solutions. The rapid expansion of omnichannel retail infrastructure and AI-enabled product personalization is also accelerating online appliance sales globally.

Key Market Insights

- Smart connected appliances are rapidly gaining popularity, driven by increasing adoption of IoT-enabled home ecosystems and voice-assisted technologies.

- Marketplace-based e-commerce platforms dominate global online appliance sales, supported by competitive pricing, financing schemes, and extensive product assortments.

- Asia-Pacific dominates the global market, led by China and India due to strong digital commerce growth and rising urbanization.

- North America remains a premium appliance demand hub, with strong adoption of AI-enabled and energy-efficient appliances.

- Energy-efficient appliances are becoming a major consumer preference, supported by regulatory initiatives and rising electricity cost awareness.

- Fintech-enabled purchasing models, including EMI financing and buy-now-pay-later solutions, are transforming appliance affordability in emerging economies.

E-Commerce Household Appliances Market Trends

Smart Appliance Adoption Accelerating Globally

The growing penetration of smart homes is significantly transforming the e-commerce household appliances market. Consumers are increasingly purchasing AI-enabled refrigerators, connected washing machines, robotic vacuum cleaners, and voice-controlled kitchen appliances through online platforms. Smart appliances integrated with IoT ecosystems allow remote monitoring, predictive maintenance, and energy optimization, making them highly attractive among urban consumers. Major appliance manufacturers are investing heavily in app-based controls, cloud connectivity, and interoperability with voice assistants to strengthen premium product positioning. Online platforms are also enhancing smart appliance discovery through AI-driven recommendations, virtual product demonstrations, and consumer reviews, helping accelerate adoption across both developed and emerging economies.

Omnichannel and Direct-to-Consumer Expansion

Manufacturers are increasingly strengthening direct-to-consumer (D2C) sales strategies to reduce dependence on third-party marketplaces and improve profitability. Leading appliance companies are investing in dedicated e-commerce websites, digital showrooms, and omnichannel fulfillment networks to enhance customer engagement. Consumers now expect seamless transitions between online research and offline product experience before final purchase. Retailers are integrating same-day delivery, installation scheduling, and digital after-sales support into online channels. The growing importance of mobile commerce and social commerce platforms is also reshaping customer acquisition strategies, particularly among younger demographics who rely heavily on digital shopping ecosystems.

E-Commerce Household Appliances Market Drivers

Rising Internet and Smartphone Penetration

The rapid expansion of internet access and smartphone adoption continues to serve as one of the strongest growth drivers for the e-commerce household appliances market. Consumers increasingly prefer online channels for comparing prices, reviewing product specifications, accessing discounts, and arranging home delivery. Mobile commerce has become especially important in Asia-Pacific markets such as China and India, where smartphone-based shopping dominates digital retail activity. E-commerce companies are enhancing user experience through AI-powered search, multilingual interfaces, and localized payment solutions, enabling broader customer participation across urban and semi-urban markets.

Growing Demand for Energy-Efficient Appliances

Rising electricity prices and increasing environmental awareness are driving global demand for energy-efficient appliances. Governments across North America, Europe, China, and India are implementing stricter energy labeling regulations and incentive programs to encourage adoption of low-power appliances. Online platforms have become important channels for educating consumers regarding inverter technologies, sustainability certifications, and long-term energy savings. Premium smart appliances with energy optimization capabilities are therefore experiencing strong online demand growth, particularly among environmentally conscious households and higher-income consumers.

E-Commerce Household Appliances Market Restraints

High Logistics and Reverse Supply Chain Costs

Household appliances involve substantial transportation, warehousing, and installation expenses due to their bulky and fragile nature. Large products such as refrigerators, washing machines, and air conditioners require specialized handling and last-mile delivery infrastructure, increasing operational costs for online retailers. Reverse logistics associated with returns, damages, and replacement services further add to profitability challenges. Rural deliveries in developing economies remain particularly difficult because of limited warehousing and transportation infrastructure.

Intense Price Competition and Margin Pressure

The e-commerce household appliances market is characterized by aggressive pricing competition among online marketplaces, manufacturers, and regional brands. Frequent discounting campaigns, festive promotions, and bundled financing offers place significant pressure on operating margins. Smaller brands often struggle to sustain high digital advertising costs and customer acquisition expenses required to compete with dominant multinational manufacturers and established e-commerce platforms. This intense pricing environment continues to challenge long-term profitability across several appliance categories.

E-Commerce Household Appliances Market Opportunities

Expansion Across Emerging Digital Economies

Emerging economies such as India, Indonesia, Vietnam, Brazil, and parts of Africa represent significant growth opportunities for the e-commerce household appliances market. Increasing internet penetration, expanding middle-class populations, and rising digital payment adoption are enabling millions of first-time online appliance buyers. Governments are also investing in digital infrastructure, logistics modernization, and fintech ecosystems to accelerate e-commerce participation. Manufacturers and retailers that localize product offerings, financing schemes, and regional supply chains are expected to gain substantial long-term advantages in these high-growth markets.

Fintech-Integrated Appliance Purchasing Models

The integration of buy-now-pay-later services, digital consumer credit, and EMI financing into e-commerce platforms is creating major opportunities for appliance sales expansion. Consumers in price-sensitive economies increasingly rely on flexible financing models to purchase premium household appliances online. Subscription-based appliance ownership and rental commerce models are also emerging among urban millennials and temporary residents. These financing innovations are increasing average transaction values while improving customer retention and repeat purchases for both manufacturers and online retailers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 165.0 Billion |

| Market Size in 2026 | USD 178.86 Billion |

| Market Size in 2031 | USD 267.71 Billion |

| CAGR | 8.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Category Insights

Major household appliances dominate the e-commerce household appliances market, accounting for more than 60% of total revenue in 2025. Refrigerators, washing machines, and air conditioners represent the largest online sales categories due to strong replacement demand and urban housing expansion. Smart refrigerators and inverter-based washing machines are gaining traction in premium segments because of their energy efficiency and connectivity features. Small household appliances such as air fryers, coffee makers, robotic vacuum cleaners, and personal care devices are witnessing faster unit growth due to affordability and increasing online impulse purchasing behavior. Kitchen-focused appliances continue to experience strong demand growth driven by changing lifestyles, home cooking trends, and modular kitchen adoption.

Technology Insights

Smart connected appliances represent one of the fastest-growing technology segments within the market, accounting for nearly 29% of global revenue in 2025. Consumers increasingly prefer appliances integrated with Wi-Fi connectivity, AI-enabled automation, remote diagnostics, and voice assistant compatibility. Conventional appliances continue to dominate volume sales in developing markets due to affordability advantages, although energy-efficient and inverter-based technologies are rapidly gaining market share globally. Appliance manufacturers are increasingly embedding predictive maintenance, mobile app integration, and energy consumption analytics into product ecosystems to strengthen customer engagement and brand loyalty.

Distribution Channel Insights

Marketplace e-commerce platforms dominate the global market with approximately 58% revenue share in 2025. Consumers prefer these platforms because of extensive product choices, price comparison tools, customer reviews, and financing availability. Brand-owned direct-to-consumer platforms are expanding rapidly as manufacturers seek higher profit margins and stronger customer relationships. Omnichannel retailing is becoming increasingly important, with retailers integrating digital storefronts, physical experience centers, and installation support into unified purchasing ecosystems. Quick commerce and social commerce models are also emerging in urban markets, particularly for small appliances and personal care devices.

Consumer Type Insights

Residential consumers account for more than 78% of total market demand globally, supported by rising urbanization, increasing disposable incomes, and growing smart home adoption. Urban households remain the primary drivers of premium appliance demand due to stronger purchasing power and digital literacy. Commercial buyers such as hotels, restaurants, hospitals, and educational institutions are increasingly adopting online procurement platforms for bulk appliance purchases. The hospitality sector represents one of the fastest-growing commercial segments as hotels and cloud kitchens increasingly invest in modern cooking, refrigeration, and cleaning appliances.

Price Segment Insights

The mid-range segment dominates the market with approximately 46% share globally, benefiting from strong demand among middle-income households seeking advanced features at affordable pricing. Economy appliances continue to witness significant demand growth across emerging markets due to first-time appliance adoption. Premium and luxury smart appliances are expanding rapidly in developed economies and affluent urban regions, supported by growing smart home penetration and consumer preference for technologically advanced products. Consumers are increasingly willing to pay higher prices for connected appliances offering automation, sustainability, and enhanced user convenience.

Explore more data points, trends and opportunities Download Free Sample Report

E-Commerce Household Appliances Market Segmentations

By Product Category

- Major Household Appliances

- Small Household Appliances

- Smart Connected Appliances

- Energy-Efficient Appliances

By Technology Type

- Conventional Appliances

- Wi-Fi Enabled Appliances

- AI-Powered Appliances

- IoT-Integrated Appliances

By Distribution Channel

- Marketplace E-commerce Platforms

- Brand-Owned Direct-to-Consumer Platforms

- Quick Commerce Platforms

- Social Commerce Platforms

- Subscription and Rental Commerce Platforms

By Consumer Type

- Residential Consumers

- Hotels and Hospitality

- Corporate Offices

- Healthcare Facilities

- Educational Institutions

By Price Segment

- Economy Segment

- Mid-Range Segment

- Premium Segment

- Luxury Smart Appliance Segment

Regional Insights

North America

North America accounts for nearly 24% of the global e-commerce household appliances market in 2025, led primarily by the United States. The region benefits from strong consumer purchasing power, advanced logistics infrastructure, and widespread smart home adoption. U.S. consumers increasingly prefer premium connected appliances and energy-efficient products, driving strong online demand for AI-enabled refrigerators, robotic vacuum cleaners, and smart climate-control systems. Canada also demonstrates robust growth in omnichannel appliance retailing due to high internet penetration and expanding digital payment ecosystems.

Europe

Europe contributes approximately 22% of global market demand, supported by strong consumer preference for sustainable and energy-efficient appliances. Germany, the United Kingdom, France, and Italy represent major regional markets. European consumers prioritize premium appliance quality, low-energy consumption, and environmentally sustainable technologies. Online channels are becoming increasingly important for appliance comparison and financing. Germany remains a leading manufacturing and consumption hub, while the United Kingdom continues witnessing rapid growth in direct-to-consumer appliance retailing and omnichannel purchasing behavior.

Asia-Pacific

Asia-Pacific dominates the global market with approximately 43% revenue share in 2025 and remains the fastest-growing region globally. China represents the largest single-country market due to its highly developed digital commerce ecosystem and strong domestic appliance manufacturing base. India is experiencing rapid market expansion driven by rising middle-class incomes, increasing smartphone penetration, and government-led digitalization initiatives. Southeast Asian economies including Indonesia, Vietnam, Thailand, and the Philippines are also witnessing accelerated appliance e-commerce adoption due to improving logistics networks and mobile commerce growth.

Latin America

Latin America is steadily emerging as an important growth market led by Brazil and Mexico. Rising fintech adoption, improving internet connectivity, and expanding urban populations are strengthening online appliance purchases across the region. Consumers increasingly prefer mid-range and installment-based appliance purchasing models due to affordability considerations. Although economic volatility and logistics challenges remain barriers in some countries, regional e-commerce infrastructure continues to improve steadily.

Middle East & Africa

The Middle East & Africa region is witnessing rising demand for premium household appliances, particularly in the UAE and Saudi Arabia. Smart city projects, increasing residential construction, and growing expatriate populations are supporting strong appliance demand across urban centers. The UAE remains a regional e-commerce hub for imported premium appliances, while Saudi Arabia’s digital transformation initiatives are accelerating online retail participation. South Africa also represents an important regional market due to expanding digital commerce penetration and rising middle-income household demand.

Key Players in the E-Commerce Household Appliances Market

- Samsung Electronics

- LG Electronics

- Whirlpool Corporation

- Haier Smart Home

- Electrolux AB

- Panasonic Corporation

- Bosch Home Appliances

- Midea Group

- Hisense Group

- Arcelik A.S.

- Sharp Corporation

- Toshiba Lifestyle Products

- Hitachi Appliances

- GE Appliances

- Philips Domestic Appliance