Duty Drawback Service Market Size

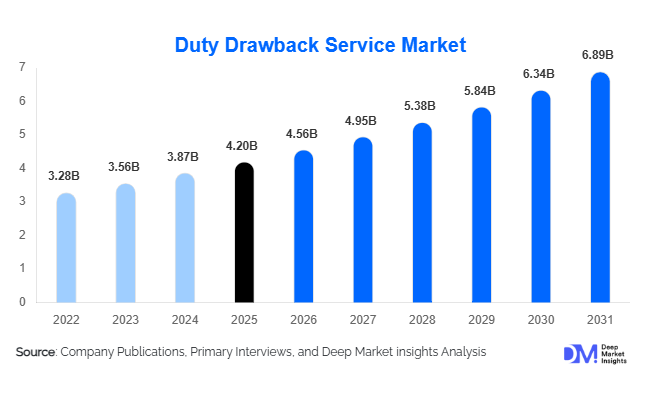

According to Deep Market Insights, the global duty drawback service market size was valued at USD 4.20 billion in 2025 and is projected to grow from USD 4.56 billion in 2025 to reach USD 6.89 billion by 2031, expanding at a CAGR of 8.6% during the forecast period (2025–2031). The duty drawback service market growth is primarily driven by increasing international trade volumes, rising complexity of customs regulations, growing adoption of trade compliance technologies, and greater awareness among exporters regarding recoverable duties and taxes. Companies operating across global supply chains are increasingly leveraging duty drawback services to improve profitability, enhance cash flow, and maintain regulatory compliance. The expansion of export-oriented manufacturing sectors across Asia-Pacific, North America, and Europe is further creating favorable conditions for duty recovery service providers.

Key Market Insights

- Duty recovery is increasingly becoming a strategic cost optimization tool, with manufacturers and exporters integrating drawback programs into broader supply chain management initiatives.

- Digital customs transformation is accelerating globally, creating strong demand for automated drawback filing, compliance monitoring, and AI-driven duty recovery platforms.

- North America dominates the global market, supported by mature customs frameworks, high trade volumes, and strong awareness of duty recovery opportunities.

- Asia-Pacific is the fastest-growing regional market, driven by export-led manufacturing growth in China, India, Vietnam, and Southeast Asia.

- Large multinational manufacturers account for the majority of drawback claims, particularly across automotive, electronics, industrial machinery, and pharmaceutical industries.

- Cloud-based customs management platforms and workflow automation solutions are significantly reducing claim processing times while improving compliance and recovery rates.

Duty Drawback Service Market Trends

Digitalization of Customs Recovery Processes

One of the most significant trends reshaping the duty drawback service market is the rapid digitization of customs and trade compliance functions. Organizations are increasingly replacing manual claim preparation processes with cloud-based customs management systems capable of automatically identifying eligible transactions, validating documentation, and preparing drawback submissions. Artificial intelligence and machine learning technologies are improving claim accuracy while reducing processing times and administrative costs. Service providers are investing heavily in automated compliance platforms that integrate directly with enterprise resource planning systems, customs databases, and trade management software. As governments continue modernizing customs infrastructure, digital duty recovery solutions are expected to become standard practice across global trade operations.

Expansion of Export-Oriented Manufacturing Supply Chains

Global supply chain diversification is creating new opportunities for duty drawback service providers. Manufacturing investments are increasingly shifting toward emerging production hubs such as India, Vietnam, Mexico, Indonesia, and Eastern Europe. As companies establish export-oriented production facilities in these regions, the volume of imported raw materials, components, and intermediate goods eligible for drawback programs continues to increase. Manufacturers are actively seeking specialized service providers to maximize duty recovery while ensuring compliance with evolving customs regulations. This trend is particularly evident in automotive, electronics, pharmaceuticals, and industrial equipment manufacturing sectors where import-export activity remains highly integrated.

Duty Drawback Service Market Drivers

Increasing Complexity of Global Trade Regulations

Customs regulations, tariff schedules, free trade agreements, and export control requirements have become increasingly complex across major trading economies. Businesses often struggle to identify eligible drawback opportunities and maintain compliance with evolving regulations. Duty drawback service providers offer specialized expertise that helps organizations recover duties while minimizing regulatory risk. As trade compliance requirements continue expanding globally, demand for professional drawback management services is expected to increase substantially.

Growing Export Activity Across Emerging Markets

The expansion of export-oriented manufacturing in Asia-Pacific and Latin America is creating significant demand for duty recovery solutions. Governments are actively promoting exports through industrial development initiatives, production-linked incentives, and trade facilitation programs. As export volumes continue increasing, companies are recognizing the financial benefits of recovering customs duties paid on imported goods and components used in exported products. This trend is particularly strong among automotive manufacturers, electronics producers, pharmaceutical exporters, and industrial machinery companies.

Duty Drawback Service Market Restraints

Documentation and Record-Keeping Challenges

Duty drawback claims require extensive documentation, including import declarations, export records, bills of materials, customs filings, and inventory tracking information. Many organizations struggle to maintain the level of documentation required to support successful claims. Incomplete records, inconsistent data management practices, and inadequate audit trails frequently result in delayed or rejected claims, limiting market adoption among smaller exporters and manufacturers.

Regulatory Variations Across Jurisdictions

Duty drawback programs differ significantly between countries, creating operational challenges for multinational organizations. Regulatory requirements, filing procedures, eligibility criteria, and audit standards vary across customs jurisdictions. Service providers must continuously monitor regulatory developments and maintain country-specific expertise, increasing operational costs and limiting scalability. Frequent policy revisions and trade agreement updates further contribute to market complexity.

Duty Drawback Service Market Opportunities

AI-Powered Trade Compliance and Duty Recovery Solutions

The growing adoption of artificial intelligence presents significant opportunities for duty drawback service providers. AI-powered systems can analyze trade transactions, identify recovery opportunities, automate document validation, and predict potential compliance risks. Organizations increasingly seek technology-enabled solutions capable of reducing administrative burdens while maximizing recoverable duties. Providers that successfully integrate advanced analytics, automation, and predictive compliance capabilities are expected to gain competitive advantages and expand market share.

Growth of Manufacturing Hubs in Emerging Economies

Countries such as India, Vietnam, Mexico, and Indonesia are attracting substantial manufacturing investments as global companies diversify production networks. Export-oriented industries operating in these regions are becoming major consumers of duty drawback services. Government-led initiatives supporting industrial growth, foreign direct investment, and export competitiveness are expected to create long-term opportunities for customs consulting firms, drawback specialists, and compliance technology providers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.20 Billion |

| Market Size in 2026 | USD 4.56 Billion |

| Market Size in 2031 | USD 6.89 Billion |

| CAGR | 8.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Service Type Insights

Documentation and filing services represent the largest segment of the duty drawback service market, accounting for approximately 32% of global revenue in 2025. Organizations frequently outsource claim preparation and submission activities due to the complexity of customs documentation requirements and the need for specialized expertise. Trade compliance advisory services are also witnessing strong growth as companies seek support in navigating increasingly complex customs regulations. Managed drawback programs continue gaining popularity among multinational enterprises seeking end-to-end duty recovery solutions. Technology-enabled filing platforms are emerging as one of the fastest-growing service categories as organizations prioritize efficiency, automation, and regulatory accuracy.

Drawback Program Insights

Manufacturing drawback programs account for the largest share of market demand, representing nearly 38% of global revenues. This dominance reflects the extensive use of imported components and raw materials in export-oriented manufacturing industries. Unused merchandise drawback programs remain particularly important for distributors and trading companies that re-export imported products without substantial modification. Substitution drawback and direct identification programs continue gaining adoption among large enterprises seeking to maximize recovery opportunities across complex global supply chains.

Enterprise Size Insights

Large enterprises account for approximately 58% of the duty drawback service market, driven by high trade volumes, extensive import-export activities, and greater awareness of duty recovery opportunities. Multinational manufacturers, automotive companies, electronics producers, and pharmaceutical firms represent the primary customer base. Mid-sized enterprises are increasingly adopting outsourced drawback solutions as service providers introduce more affordable technology-enabled platforms. Small enterprises remain an underpenetrated segment but represent a significant long-term growth opportunity as digital customs solutions become more accessible.

Industry Vertical Insights

Automotive manufacturers represent the largest industry segment, accounting for nearly 14% of global duty drawback service demand. The industry's highly globalized supply chains and extensive use of imported components create substantial duty recovery opportunities. Electronics and semiconductor manufacturers are among the fastest-growing verticals due to increasing cross-border trade in components and finished products. Pharmaceutical, industrial machinery, chemical, and aerospace sectors also contribute significantly to market growth, supported by high-value trade flows and complex customs requirements.

Technology Adoption Insights

Workflow automation platforms dominate technology adoption within the market, accounting for approximately 36% of total technology-related spending. Organizations increasingly seek solutions capable of automating claim identification, document verification, audit preparation, and compliance monitoring. Cloud-based duty recovery platforms are gaining momentum due to scalability, integration capabilities, and lower implementation costs. Artificial intelligence and advanced analytics are emerging as important differentiators, helping organizations improve recovery rates while reducing compliance risks.

Explore more data points, trends and opportunities Download Free Sample Report

Duty Drawback Service Market Segmentations

By Service Type

- Duty Drawback Claim Identification & Eligibility Assessment

- Documentation & Filing Services

- Customs Refund Processing Services

- Trade Compliance & Regulatory Advisory

- Audit Support & Risk Management Services

- Duty Recovery Program Management

- Post-Claim Monitoring & Appeals Management

- Duty Optimization & Tariff Engineering Services

- Managed Outsourcing Services

- Technology-Enabled Drawback Processing Platforms

By Industry Vertical

- Automotive

- Aerospace & Defense

- Industrial Machinery

- Electronics & Semiconductors

- Pharmaceuticals & Medical Devices

- Chemicals & Petrochemicals

- Consumer Goods

- Retail & E-Commerce

- Food & Beverage

- Textile & Apparel

- Metals & Mining

- Agriculture & Agribusiness

By Enterprise Size

- Large Enterprises

- Mid-Sized Enterprises

- Small Enterprises

By Delivery Model

- Consulting-Based Services

- Customs Brokerage-Based Services

- Software-as-a-Service (SaaS) Platforms

- Hybrid Managed Service Platforms

By End User

- Exporters

- Importers

- Manufacturers

- Third-Party Logistics Providers (3PLs)

- Freight Forwarders

- Customs Brokers

- Trading Companies

Regional Insights

North America

North America accounted for approximately 37% of global duty drawback service market revenue in 2025, making it the largest regional market. The United States alone contributes nearly 31% of global demand due to its sophisticated customs framework, extensive import-export activity, and widespread awareness of drawback programs. Canada and Mexico also represent important markets, supported by integrated supply chains and strong cross-border trade activity under regional trade agreements. High levels of customs compliance maturity and advanced technology adoption continue supporting regional market growth.

Europe

Europe remains a major market for duty drawback services, accounting for approximately 22% of global revenue. Germany leads regional demand due to its export-oriented manufacturing sector and strong automotive industry presence. The United Kingdom, France, Italy, Netherlands, and Poland are also significant contributors. Regulatory complexity following Brexit has increased demand for customs advisory and drawback management services across the region. European manufacturers increasingly utilize duty recovery strategies to improve competitiveness in global export markets.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market and accounted for approximately 31% of global revenue in 2025. China remains the largest market within the region, supported by its dominant position in global manufacturing and exports. India is emerging as the fastest-growing national market, driven by manufacturing expansion, export promotion initiatives, and increased foreign investment. Vietnam, South Korea, Japan, Thailand, and Indonesia are also witnessing strong growth as companies expand export-oriented production activities throughout the region.

Latin America

Latin America accounted for approximately 5% of global market revenue in 2025. Brazil and Mexico lead regional demand due to their manufacturing sectors and increasing participation in global supply chains. Export diversification efforts and industrial development initiatives are creating new opportunities for duty recovery service providers across the region.

Middle East & Africa

The Middle East and Africa accounted for approximately 5% of global revenue in 2025. The United Arab Emirates serves as a major regional trade hub, generating significant demand for customs advisory and duty recovery services. Saudi Arabia is witnessing increased adoption as industrial diversification programs stimulate manufacturing and export activity. South Africa remains the largest market in Sub-Saharan Africa, supported by its industrial base and international trade activities.

Key Players in the Duty Drawback Service Market

- Livingston International

- CH Powell Company

- Mohawk Global

- International Tariff Management (ITM)

- Rogers & Brown Customs Brokers

- Comstock & Theakston

- Joseph Smith Company

- Soo Hoo Customs Broker

- KPMG Trade & Customs

- Deloitte Global Trade Advisory

- PwC Customs & International Trade

- Ernst & Young Global Trade

- BDO Trade Advisory

- Crowe Global Trade Services

- Global Training Center