Curtain Fabric Market Size

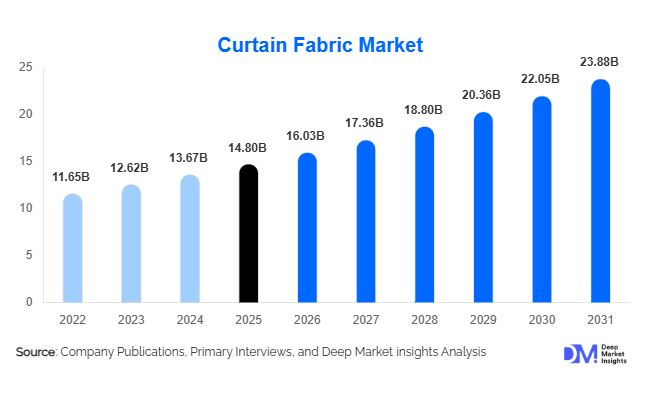

According to Deep Market Insights, the global curtain fabric market size was valued at USD 14.8 billion in 2025 and is projected to grow from USD 16.03 billion in 2026 to reach USD 23.88 billion by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The curtain fabric market growth is primarily driven by increasing residential construction activities, rising consumer expenditure on home décor and interior aesthetics, growing demand for energy-efficient blackout curtains, and rapid expansion of hospitality and commercial infrastructure projects worldwide.

The market has evolved significantly from traditional decorative textile applications into a multifunctional interior furnishing industry focused on sustainability, thermal insulation, acoustic performance, and smart-home compatibility. Consumers increasingly prefer premium curtain fabrics that combine visual appeal with practical benefits such as UV protection, temperature control, and noise reduction. Technological advancements in textile manufacturing, including digital printing, antimicrobial coatings, recycled fibers, and automated weaving systems, are further transforming product innovation across global markets.

Asia-Pacific dominates the global curtain fabric industry due to strong textile manufacturing ecosystems in China and India, rising urbanization, and export-oriented production capabilities. Meanwhile, North America and Europe continue to witness strong demand for sustainable, luxury, and smart-compatible curtain fabrics across residential and commercial applications. Hospitality expansion, real estate modernization, and rising renovation spending continue to create long-term opportunities for manufacturers globally.

Key Market Insights

- Polyester curtain fabrics dominate the market, accounting for the largest share due to affordability, durability, and compatibility with blackout and thermal technologies.

- Blackout and thermal-insulated curtains are witnessing rapid adoption, driven by increasing focus on energy efficiency and indoor comfort across residential and hospitality sectors.

- Asia-Pacific leads the global curtain fabric market, supported by large-scale textile manufacturing, strong exports, and rising urban housing demand in China and India.

- Europe remains a major market for sustainable and premium fabrics, with growing preference for eco-friendly and recycled curtain materials.

- Smart-home integration is reshaping the industry, increasing demand for lightweight and motorized curtain-compatible fabrics.

- Digital textile printing and sustainable production technologies are becoming key competitive differentiators among leading manufacturers globally.

Curtain Fabric Market Trends

Sustainable and Recycled Curtain Fabrics Gaining Momentum

Sustainability has emerged as one of the most influential trends within the global curtain fabric market. Consumers are increasingly seeking environmentally friendly home furnishing products manufactured using recycled polyester, organic cotton, and low-impact dyeing technologies. Governments and environmental agencies across Europe and North America are implementing stricter regulations regarding textile waste, chemical emissions, and water-intensive production processes, pushing manufacturers toward circular textile production systems.

Major curtain fabric producers are investing heavily in recycled fiber technologies and sustainable sourcing certifications to strengthen export competitiveness and brand positioning. Recycled polyester curtains derived from post-consumer plastic waste are gaining popularity among environmentally conscious consumers and hospitality operators aiming to reduce carbon footprints. In addition, natural fabrics such as linen, hemp, and bamboo-based textiles are witnessing rising demand in luxury interior décor applications due to their eco-friendly appeal and premium aesthetics. Sustainable curtain fabrics are increasingly becoming standard procurement criteria for commercial buildings, hotels, and institutional projects.

Technology-Integrated Smart Curtain Solutions

The integration of smart-home technologies is significantly transforming the curtain fabric industry. Automated curtain systems linked with IoT-enabled home devices and voice assistants are becoming increasingly popular in premium residential and commercial spaces. This trend is creating demand for lightweight, durable, and automation-compatible curtain fabrics capable of supporting motorized curtain rails and smart operating systems.

Manufacturers are also developing advanced performance-oriented curtain fabrics featuring thermal insulation, UV resistance, sound absorption, antimicrobial coatings, and energy-saving reflective technologies. Digitally printed fabrics are enabling customized interior décor solutions with shorter production cycles and improved design flexibility. AI-based textile design systems and automated weaving technologies are helping manufacturers improve production efficiency, reduce material waste, and accelerate product development timelines. These innovations are particularly attractive to younger consumers and smart-building developers seeking technologically advanced interior furnishing solutions.

Curtain Fabric Market Drivers

Growing Residential Construction and Home Renovation Activities

Rapid urbanization and rising residential construction activities across Asia-Pacific, the Middle East, and Latin America continue to drive significant demand for curtain fabrics globally. Expanding middle-class populations and increasing disposable incomes are encouraging consumers to invest more heavily in home décor products that enhance aesthetics, comfort, and privacy. Curtains are increasingly viewed as essential design components rather than simple utility products.

Home renovation and remodeling trends are also contributing substantially to market expansion, particularly in North America and Europe. Consumers are upgrading living spaces with premium and customized interior solutions, boosting demand for designer curtain fabrics, blackout curtains, and energy-efficient thermal textiles. Increasing penetration of modular homes and smart apartments further supports the growth of technologically compatible curtain fabrics.

Expansion of Hospitality and Commercial Infrastructure

The rapid growth of hospitality, healthcare, retail, and corporate office infrastructure is significantly accelerating demand for commercial-grade curtain fabrics. Hotels, resorts, conference centers, educational institutions, and healthcare facilities increasingly require specialized textiles featuring flame-retardant, antimicrobial, acoustic, and blackout properties.

The recovery of global tourism and rising investments in luxury hospitality projects across the Middle East, Southeast Asia, and North America are driving procurement of premium curtain solutions. Commercial buildings are increasingly prioritizing energy-efficient interiors, further strengthening demand for insulated and UV-resistant curtain fabrics that contribute to reduced HVAC energy consumption and improved indoor comfort.

Curtain Fabric Market Restraints

Raw Material Price Volatility

Fluctuating prices of polyester, cotton, dyes, and textile chemicals remain a major challenge for curtain fabric manufacturers globally. Polyester prices are highly dependent on crude oil market fluctuations, while natural fibers such as cotton are vulnerable to weather disruptions, agricultural supply shortages, and climate-related uncertainties. These pricing instabilities directly impact production costs, profit margins, and long-term procurement planning.

Rising transportation and energy costs further increase manufacturing expenses, particularly for export-oriented producers. Small and medium-sized manufacturers often struggle to absorb raw material cost increases, resulting in pricing pressures across highly competitive market segments.

Competition from Alternative Window Covering Solutions

The increasing adoption of blinds, shutters, shades, and motorized window systems presents a significant challenge to curtain fabric demand in certain commercial and urban residential markets. Modern minimalist architectural trends increasingly favor sleek and low-maintenance window treatment solutions over traditional curtains.

Commercial office buildings and contemporary apartments often prefer automated shades and blinds due to their compact designs and ease of maintenance. To remain competitive, curtain fabric manufacturers must continuously innovate through sustainable materials, multifunctional performance features, premium textures, and smart-home integration capabilities.

Curtain Fabric Market Opportunities

Growth of Smart Homes and Automated Interiors

The global expansion of smart-home ecosystems presents significant growth opportunities for curtain fabric manufacturers. Increasing adoption of voice-controlled automation systems, motorized curtain rails, and AI-enabled interior management technologies is driving demand for specialized curtain fabrics compatible with automated systems.

Luxury residential developments, premium hotels, and smart commercial buildings are increasingly integrating automated blackout and thermal curtains to improve energy efficiency and user convenience. Manufacturers capable of developing lightweight, durable, and technologically compatible fabrics are expected to gain competitive advantages in this evolving segment. Smart curtain integration is also supporting premium pricing opportunities and higher-margin product categories.

Expansion of Specialized Commercial Applications

Specialized commercial and institutional applications are creating new growth avenues for the curtain fabric market. Hospitals and healthcare facilities are increasingly adopting antimicrobial curtain fabrics to improve hygiene standards and infection control measures. Educational institutions, cinemas, auditoriums, and corporate offices are generating rising demand for acoustic and sound-absorbing curtain materials.

Government regulations concerning fire safety and indoor environmental standards are also accelerating demand for flame-retardant and energy-efficient curtain fabrics across commercial buildings. These high-performance applications offer manufacturers opportunities to diversify beyond conventional residential demand while improving profitability through long-term institutional procurement contracts.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.8 Billion |

| Market Size in 2026 | USD 16.03 Billion |

| Market Size in 2031 | USD 23.88 Billion |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Fabric Material Insights

Polyester curtain fabrics dominate the global market, accounting for nearly 38% of total revenue share in 2025 due to their affordability, wrinkle resistance, durability, and low maintenance requirements. Polyester fabrics are widely preferred across residential and commercial applications because they support blackout coatings, thermal insulation technologies, and digital printing customization. Cotton and linen curtain fabrics continue to gain traction in premium residential interiors and luxury hospitality applications owing to their natural aesthetics and eco-friendly appeal. Blended fabrics such as cotton-polyester and linen-polyester combinations are also witnessing strong demand as consumers seek balance between durability, affordability, and premium texture. Sustainable recycled fabrics are emerging rapidly as a high-growth category, particularly across Europe and North America where environmental regulations and eco-conscious purchasing behavior continue to strengthen.

Functionality Insights

Blackout curtain fabrics remain the leading functionality segment, representing approximately 29% of global demand in 2025. Rising awareness regarding energy efficiency, thermal insulation, and sleep quality is accelerating adoption across hotels, hospitals, residential bedrooms, and corporate environments. Thermal-insulated curtains are gaining popularity in regions with extreme weather conditions due to their ability to reduce indoor temperature fluctuations and lower HVAC energy consumption. Sheer curtain fabrics continue to maintain steady demand in decorative residential applications where natural lighting and aesthetics are prioritized. Fire-retardant and antimicrobial curtain fabrics are increasingly being adopted in healthcare, hospitality, and institutional buildings due to stringent safety and hygiene regulations. Acoustic curtain fabrics are also emerging as a fast-growing niche segment in offices, educational institutions, and entertainment venues.

Application Insights

Residential applications account for nearly 61% of global curtain fabric demand, supported by rising housing construction, home renovation trends, and increasing consumer spending on interior décor products. Living rooms and bedrooms remain the primary consumption categories, particularly for blackout and decorative curtain fabrics. Commercial applications are witnessing strong growth due to expanding hospitality, retail, and corporate infrastructure investments worldwide. Hotels and resorts continue to procure premium blackout and luxury decorative fabrics to enhance guest comfort and energy efficiency. Healthcare facilities are increasingly adopting antimicrobial curtain fabrics, while educational institutions and office spaces are driving demand for acoustic and flame-retardant textiles. Industrial and institutional applications, including auditoriums, government buildings, and transportation interiors, are also generating demand for specialized performance-oriented curtain materials.

Distribution Channel Insights

Offline distribution channels continue to dominate the curtain fabric market, accounting for nearly 68% of total sales globally. Consumers prefer physical retail outlets, home décor stores, and textile showrooms because they allow direct evaluation of fabric texture, color, transparency, and quality before purchase. Interior designers and contract furnishing suppliers also play a significant role in large-scale commercial procurement projects.

Online sales channels are growing rapidly due to increasing digitalization of home furnishing retail. E-commerce platforms and brand-owned websites are expanding product accessibility through virtual visualization tools, customized ordering solutions, and direct-to-consumer marketing strategies. Younger consumers increasingly prefer online channels for comparing designs, prices, and product reviews before purchasing curtain fabrics.

Price Range Insights

Mid-range curtain fabrics currently represent the largest market segment due to balanced pricing, wide product availability, and broad consumer affordability across residential applications. Economy curtain fabrics continue to witness stable demand in developing regions where price sensitivity remains high. However, premium and luxury curtain fabrics are emerging as the fastest-growing category, driven by increasing demand for designer interiors, sustainable textiles, and customized decorative solutions.

Luxury hotels, premium apartments, and high-end residential projects increasingly prefer natural fabrics such as linen, silk blends, and textured jacquard materials. Premium curtain fabrics also offer higher profit margins for manufacturers through customization, performance coatings, and exclusive design collections.

Explore more data points, trends and opportunities Download Free Sample Report

Curtain Fabric Market Segmentations

By Fabric Material

- Natural Fabrics

- Synthetic Fabrics

- Blended Fabrics

By Functionality

- Blackout Curtain Fabrics

- Thermal-Insulated Curtain Fabrics

- Sheer Curtain Fabrics

- Fire-Retardant Curtain Fabrics

- Acoustic Curtain Fabrics

- UV-Resistant Curtain Fabrics

- Antimicrobial Curtain Fabrics

By Application

- Residential

- Commercial

- Industrial & Institutional

By Distribution Channel

- Offline Retail Stores

- Home Décor Specialty Stores

- Interior Design Studios

- E-commerce Platforms

- Brand-Owned Websites

By Price Range

- Economy Curtain Fabrics

- Mid-Range Curtain Fabrics

- Premium/Luxury Curtain Fabrics

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global curtain fabric market, accounting for approximately 41% of total market share in 2025. China remains the largest producer and exporter due to its integrated textile manufacturing ecosystem, cost-efficient production capabilities, and strong global trade infrastructure. India is among the fastest-growing markets, supported by expanding urban housing demand, rising middle-class incomes, and government-backed textile manufacturing initiatives such as “Make in India.” Southeast Asian countries including Vietnam and Indonesia are also emerging as major textile manufacturing hubs due to lower labor costs and increasing foreign investments.

North America

North America represents nearly 24% of global market demand, led primarily by the United States. Strong home renovation spending, rising smart-home adoption, and increasing preference for energy-efficient interiors continue to support market expansion. Demand for blackout, thermal-insulated, and sustainable curtain fabrics remains particularly strong in residential and hospitality sectors. Canada is also witnessing increasing adoption of eco-friendly and energy-saving curtain solutions driven by sustainability-focused building regulations.

Europe

Europe accounts for roughly 22% of the global curtain fabric market, with Germany, the United Kingdom, France, and Italy serving as key demand centers. European consumers increasingly prioritize sustainable textiles, recycled materials, and premium interior décor products. Strict environmental regulations concerning textile processing and chemical usage are accelerating adoption of certified eco-friendly curtain fabrics. Luxury residential renovation projects and commercial infrastructure modernization continue to support stable regional demand.

Latin America

Latin America is gradually emerging as a promising market for curtain fabrics, led by Brazil and Mexico. Rising urbanization, growing residential construction activity, and increasing investment in retail and hospitality infrastructure are supporting market growth. Demand remains concentrated in mid-range and decorative curtain fabric categories due to rising middle-class consumption and expanding home furnishing retail networks.

Middle East & Africa

The Middle East & Africa region is witnessing rapid growth due to luxury hospitality expansion, smart-city developments, and premium real estate investments. Saudi Arabia and the UAE are major growth markets driven by large-scale tourism and infrastructure projects. Hotels and commercial developments increasingly demand premium blackout, fire-retardant, and energy-efficient curtain fabrics. South Africa also represents a significant regional market due to expanding commercial infrastructure and residential renovation activities.

Key Players in the Curtain Fabric Market

- Hunter Douglas

- Dedar Milano

- Vescom

- Glen Raven

- Sanderson Design Group

- Kobayashi Textile

- Nien Made Enterprise

- Springs Window Fashions

- Welspun Living

- Trident Group

- Luthai Textile

- Fuanna

- Romo Group

- Sunbrella

- Nitori Holdings