Cookware Market Size

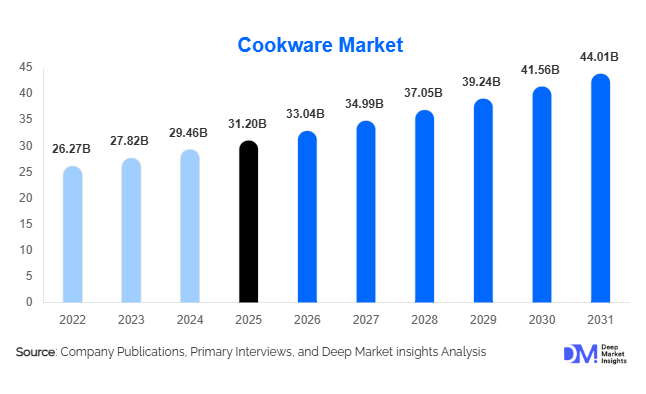

According to Deep Market Insights, the global cookware market size was valued at USD 31.2 billion in 2025 and is projected to grow from USD 33.04 billion in 2026 to reach USD 43.9 billion by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). Market growth is primarily driven by rising consumer interest in home cooking, increasing adoption of premium and health-conscious cookware products, rapid urbanization in emerging economies, and expanding demand from commercial foodservice establishments. The industry is also benefiting from the transition toward induction-compatible cookware, PFAS-free coatings, and technologically advanced cookware solutions that align with changing consumer preferences for convenience, sustainability, and durability.

Key Market Insights

- Stainless steel remains the dominant cookware material segment, accounting for approximately 34% of global market revenue due to durability, food safety, and induction compatibility.

- Non-stick cookware continues to lead product demand, representing over 50% of global cookware sales as consumers prioritize convenience and ease of cleaning.

- Asia-Pacific dominates the global cookware market, supported by strong manufacturing capabilities, growing household formation, and rising middle-class consumption in China and India.

- India is emerging as the fastest-growing major cookware market, driven by urbanization, premiumization, and increasing penetration of organized retail channels.

- E-commerce and direct-to-consumer sales channels are reshaping distribution models, enabling brands to reach consumers directly while improving margins.

- Health-conscious cookware innovations, including ceramic coatings, PFAS-free products, and smart cookware technologies, are becoming major competitive differentiators.

Cookware Market Trends

Premiumization Driving Consumer Purchasing Behavior

Consumers worldwide are increasingly upgrading from basic cookware products to premium cookware solutions that offer superior performance, durability, aesthetics, and safety. Stainless steel cookware, multi-ply clad cookware, enameled cast iron products, and ceramic-coated cookware are witnessing significant demand growth. Premium cookware manufacturers are positioning their products as long-term investments, emphasizing durability, energy efficiency, and healthier cooking outcomes. The trend is particularly strong in North America, Europe, Japan, South Korea, and urban centers across emerging economies. Rising disposable incomes and kitchen renovation activities are further supporting premium cookware adoption.

Growing Adoption of PFAS-Free and Sustainable Cookware

Health and environmental concerns are significantly influencing cookware purchasing decisions. Consumers are increasingly seeking alternatives to traditional non-stick coatings, leading to growing demand for ceramic-coated cookware, stainless steel cookware, and other PFAS-free solutions. Manufacturers are investing in environmentally responsible production methods, recyclable materials, and sustainable packaging to align with evolving regulatory standards and consumer expectations. The growing emphasis on sustainability is expected to reshape product development strategies throughout the forecast period, while eco-friendly cookware continues to gain traction among younger demographics and environmentally conscious households.

Cookware Market Drivers

Expansion of Home Cooking Culture

The increasing popularity of home cooking remains one of the strongest drivers of cookware demand globally. Consumers are spending more time preparing meals at home due to health awareness, cost savings, culinary experimentation, and the influence of digital cooking content. Social media platforms, cooking influencers, recipe-sharing communities, and online culinary education have encouraged consumers to invest in specialized cookware products. This trend has accelerated demand for frying pans, sauté pans, Dutch ovens, pressure cookers, and premium cookware sets across developed and emerging markets.

Growing Adoption of Induction Cooking Systems

The global transition toward energy-efficient cooking appliances has accelerated the adoption of induction cooktops. As governments and consumers seek cleaner and more energy-efficient kitchen solutions, demand for induction-compatible cookware continues to rise. Stainless steel, carbon steel, and multi-ply cookware manufacturers are benefiting from this transition, particularly across Europe, China, Japan, and urban regions of North America. The expansion of induction cooking infrastructure is expected to remain a major catalyst for cookware replacement demand throughout the forecast period.

Cookware Market Restraints

Volatility in Raw Material Prices

Cookware manufacturers remain highly exposed to fluctuations in the prices of stainless steel, aluminum, copper, iron, and energy inputs. Changes in commodity markets directly impact manufacturing costs and profit margins. Frequent price adjustments can create challenges for both manufacturers and retailers, particularly in highly competitive markets where passing costs to consumers is difficult. Raw material inflation continues to influence pricing strategies and investment decisions across the industry.

Highly Fragmented Competitive Landscape

The cookware market remains fragmented across regional and global players, creating significant pricing pressure. The presence of numerous private-label brands, local manufacturers, and low-cost imports limits pricing power for established companies. Market participants must continuously invest in product innovation, branding, and distribution expansion to maintain market share. This competitive intensity often compresses margins and increases customer acquisition costs.

Cookware Market Opportunities

Smart and Connected Cookware Solutions

The integration of IoT, sensors, and digital technologies into cookware products presents a significant growth opportunity. Smart cookware solutions featuring temperature monitoring, mobile application connectivity, guided cooking functions, and automated cooking assistance are gaining traction among technology-oriented consumers. As smart kitchens become more prevalent, connected cookware products are expected to generate premium revenue opportunities and strengthen customer engagement.

Expansion Across Emerging Economies

Rapid urbanization, growing middle-class populations, and rising disposable incomes across India, Indonesia, Vietnam, the Philippines, Brazil, and several African nations are creating substantial demand for cookware products. Consumers in these markets are increasingly transitioning from unorganized cookware purchases to branded products offering improved quality and durability. Manufacturers establishing localized production facilities and distribution networks are well-positioned to capitalize on long-term growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 31.2 Billion |

| Market Size in 2026 | USD 33.04 Billion |

| Market Size in 2031 | USD 44.01 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pans represent the largest product segment, accounting for approximately 27% of the global cookware market revenue in 2025. Frying pans and sauté pans remain the most frequently purchased cookware products due to their versatility and daily usage across households and commercial kitchens. Cookware sets are gaining popularity among first-time homeowners and urban consumers seeking complete kitchen solutions. Pressure cookers continue to exhibit strong demand across Asia-Pacific markets, particularly in India, where they remain an essential household cooking appliance. Speciality cookware products such as Dutch ovens, woks, and grill pans are witnessing increased adoption as consumers experiment with diverse cuisines and advanced cooking techniques.

Material Insights

Stainless steel dominates the global cookware market with an estimated 34% market share. The material's durability, corrosion resistance, food safety characteristics, and compatibility with induction cooking systems make it the preferred choice among consumers and professional chefs. Aluminium cookware remains highly popular due to its affordability and superior heat conductivity, particularly in emerging economies. Cast iron cookware continues to gain momentum in premium segments because of its heat retention properties and suitability for healthy cooking. Ceramic cookware is emerging as one of the fastest-growing categories due to rising demand for non-toxic and environmentally friendly cooking solutions.

Coating Type Insights

Non-stick coatings account for approximately 54% of global cookware demand. Consumers continue to favour non-stick cookware because of ease of cleaning, convenience, and reduced oil requirements during cooking. Ceramic-coated cookware represents the fastest-growing coating category, supported by increasing awareness regarding PFAS-free cooking surfaces. Hard-anodised coatings are also gaining popularity due to enhanced durability, scratch resistance, and premium positioning. Manufacturers are increasingly investing in next-generation coating technologies that improve longevity while meeting evolving regulatory requirements.

Distribution Channel Insights

Offline retail channels continue to dominate the cookware market, representing approximately 79% of global sales. Speciality kitchen stores, department stores, hypermarkets, and brand-owned retail outlets remain important purchasing destinations due to consumers' preference for physically evaluating cookware before purchase. However, online retail is expanding rapidly as digital platforms offer broader product selections, competitive pricing, and direct-to-consumer engagement opportunities. E-commerce marketplaces and manufacturer-operated websites are becoming increasingly important channels for premium cookware brands seeking to enhance profitability and customer loyalty.

End-Use Insights

Residential households account for approximately 82% of global cookware consumption, generating demand worth more than USD 25 billion annually. Rising home ownership, kitchen remodelling projects, and increasing interest in cooking continue to support household demand. Commercial foodservice represents the fastest-growing end-use segment, driven by expansion in restaurants, hotels, catering services, cloud kitchens, and institutional food operations. Growthin then tourism and hospitality industries is creating additional demand for professional-grade cookware products designed for intensive commercial use.

Explore more data points, trends and opportunities Download Free Sample Report

Cookware Market Segmentations

By Product Type

- Pots

- Pans

- Pressure Cookers

- Specialty Cookware

- Bakeware-Cookware Hybrids

- Cookware Sets

By Material

- Stainless Steel

- Aluminum

- Cast Iron

- Copper

- Carbon Steel

- Ceramic

- Glass

- Titanium

- Multi-Ply/Clad Metal Composites

By Coating Type

- Non-Stick PTFE Coated

- Ceramic Coated

- Hard-Anodized Coated

- Enameled Coated

- Uncoated Cookware

By Distribution Channel

- Hypermarkets & Supermarkets

- Department Stores

- Specialty Kitchen Stores

- Brand-Owned Stores

- E-commerce Marketplaces

- Direct-to-Consumer Websites

By End User

- Residential Households

- Restaurants

- Hotels

- Cafés

- Catering Services

- Institutional Kitchens

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 40% of the global cookware market, making it the largest regional market worldwide. China dominates regional demand due to its large consumer base, strong manufacturing ecosystem, and growing middle-class population. India is emerging as the fastest-growing major market, supported by rising urbanization, increasing disposable incomes, and expanding organized retail networks. Japan and South Korea continue to drive premium cookware demand through innovation and consumer preference for high-quality kitchen products.

North America

North America represents approximately 24% of global cookware revenue. The United States remains the largest market within the region, accounting for nearly 85% of regional demand. Growth is supported by premium cookware adoption, kitchen renovation spending, and increasing demand for healthy cooking solutions. Consumers are increasingly investing in stainless steel, ceramic-coated, and induction-compatible cookware products.

Europe

Europe accounts for nearly 23% of global market demand. Germany, France, the United Kingdom, Italy, and Spain remain key contributors to regional growth. The widespread adoption of induction cooking systems and strong consumer preference for sustainable products continue to support demand for premium cookware solutions. European consumers demonstrate a strong willingness to invest in long-lasting, environmentally responsible cookware products.

Latin America

Latin America represents approximately 6% of global cookware demand. Brazil remains the largest regional market, followed by Mexico and Argentina. Rising household consumption, expanding middle-class populations, and growing penetration of organized retail channels are contributing to steady market growth. Manufacturers are increasingly targeting affordable premium cookware products to address changing consumer preferences.

Middle East & Africa

The Middle East & Africa account for approximately 7% of global market revenue. Saudi Arabia and the UAE are driving premium cookware demand, supported by rising disposable incomes and growth in the hospitality sector. South Africa remains the largest cookware market in Sub-Saharan Africa. Investments in tourism infrastructure and commercial foodservice establishments continue to generate additional demand for cookware products throughout the region.

Key Players in the Cookware Market

- Groupe SEB

- Meyer Corporation

- Newell Brands

- TTK Prestige

- Hawkins Cookers

- Tramontina

- Fissler

- Le Creuset

- SCANPAN

- The Vollrath Company

- Cristel

- de Buyer

- Nordic Ware

- Wilh. Werhahn KG

- Middleby Corporation