Container Homes Market Size

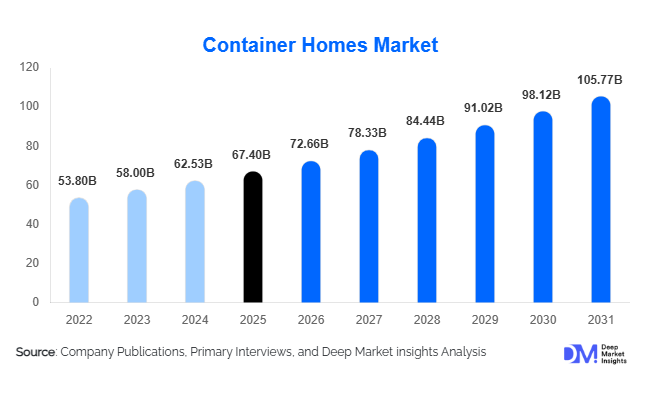

According to Deep Market Insights, the global container homes market size was valued at USD 67.4 billion in 2025 and is projected to grow from USD 72.66 billion in 2026 to reach USD 105.77 billion by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The container homes market growth is primarily driven by increasing demand for affordable housing, rising adoption of sustainable construction materials, and growing preference for modular and prefabricated housing solutions across residential and commercial sectors.

Key Market Insights

- Container homes are increasingly being adopted as sustainable housing alternatives, supported by global carbon reduction goals and circular economy initiatives.

- Affordable housing shortages in urban regions are accelerating demand for modular container-based residential infrastructure.

- North America dominates the global market, led by strong adoption of off-grid homes, tiny homes, and sustainable residential projects in the United States and Canada.

- Asia-Pacific is the fastest-growing region, supported by rapid urbanization, smart-city initiatives, and industrial workforce accommodation demand.

- Luxury container homes and eco-resorts are emerging as high-growth segments, particularly in tourism-driven economies.

- Technological advancements, including smart-home integration, solar-powered systems, and AI-assisted modular design, are transforming market competitiveness.

Container Homes Market Trends

Smart and Sustainable Container Housing Gaining Popularity

The container homes industry is increasingly shifting toward sustainable and energy-efficient modular housing systems. Consumers are prioritizing eco-friendly homes integrated with solar panels, rainwater harvesting systems, energy-efficient insulation, and smart-home automation technologies. Governments and municipalities are also promoting green construction practices to reduce carbon emissions from traditional construction methods. Smart container homes equipped with IoT-enabled energy management systems and remote monitoring capabilities are witnessing particularly strong adoption in North America and Europe. The integration of renewable energy systems and net-zero construction models is expected to become a defining industry trend over the next decade.

Luxury and Designer Container Homes Expanding Globally

Luxury container homes are emerging as a fast-growing segment within the broader modular construction industry. High-end consumers increasingly seek customized container villas, eco-lodges, and designer modular residences that combine sustainability with premium aesthetics. Architects and developers are introducing multi-story luxury structures featuring advanced interior finishes, panoramic glass designs, smart automation, and off-grid capabilities. Tourism operators are also investing heavily in container-based boutique resorts and glamping infrastructure to attract environmentally conscious travelers. This trend is significantly improving consumer perception of container homes as permanent premium housing solutions rather than temporary structures.

Container Homes Market Drivers

Rising Demand for Affordable Housing

Global housing affordability challenges are among the primary growth drivers for the container homes market. Rapid urbanization, rising real estate prices, and increasing construction costs have intensified demand for low-cost alternative housing solutions. Container homes can reduce construction expenses by 20–35% while significantly shortening project timelines compared to conventional buildings. Governments, real estate developers, and municipal authorities are increasingly utilizing modular container housing for affordable residential projects, student accommodation, and workforce housing. This trend is particularly strong in the United States, India, China, and several European countries experiencing urban housing deficits.

Growing Focus on Sustainable Construction

The construction industry is under growing pressure to reduce waste generation and carbon emissions. Container homes support sustainability objectives by repurposing steel shipping containers and minimizing material waste during construction. Rising implementation of green building standards, ESG-focused investments, and circular economy initiatives is accelerating demand for modular construction systems globally. Consumers are also demonstrating higher preference for energy-efficient and environmentally responsible housing solutions. The ability of container homes to integrate renewable energy systems and off-grid infrastructure further strengthens their long-term growth potential.

Container Homes Market Restraints

Regulatory and Zoning Challenges

One of the major restraints in the container homes market is the lack of standardized regulations across countries and municipalities. Building codes, zoning approvals, insulation standards, and safety certifications vary significantly by region, creating project delays and compliance complexities. In some regions, container homes continue to face restrictions related to permanent residential occupancy and land-use policies. These regulatory barriers increase development costs and limit market penetration, particularly for smaller manufacturers and new entrants.

Volatility in Raw Material and Logistics Costs

Fluctuating steel prices, shipping container availability, and transportation costs remain critical challenges for manufacturers and developers. Global supply chain disruptions have periodically increased container procurement costs, negatively affecting project profitability. Additional expenses associated with insulation upgrades, corrosion resistance, ventilation systems, and interior customization can further elevate total construction costs. These factors may reduce price competitiveness in certain regional markets and slow wider adoption among middle-income consumers.

Container Homes Market Opportunities

Disaster Relief and Emergency Housing Applications

The increasing frequency of natural disasters and humanitarian crises is creating significant opportunities for container-based emergency housing systems. Governments, NGOs, and international humanitarian agencies are increasingly adopting modular container structures for temporary shelters, mobile clinics, and emergency accommodation facilities. Container homes offer rapid deployment, structural durability, portability, and scalability, making them highly suitable for disaster-prone regions. Rising investments in resilient infrastructure and emergency preparedness programs are expected to strengthen long-term demand for container housing solutions globally.

Growth of Eco-Tourism and Off-Grid Living

The expansion of eco-tourism and sustainable lifestyle movements is opening new growth avenues for luxury container resorts, glamping sites, and off-grid residential projects. Travelers increasingly seek eco-conscious accommodations integrated with renewable energy systems and immersive natural experiences. Container homes provide flexible and aesthetically appealing solutions for remote tourism infrastructure. Simultaneously, growing consumer interest in minimalist living, digital nomad lifestyles, and off-grid housing is accelerating adoption of compact modular container residences across North America, Australia, and Europe.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 67.4 Billion |

| Market Size in 2026 | USD 72.66 Billion |

| Market Size in 2031 | USD 105.77 Billion |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Container Type Insights

Used and repurposed shipping containers dominate the market, accounting for nearly 58% of global revenue in 2025. Their leadership is driven by lower procurement costs, sustainability benefits, and increasing adoption of recycled construction materials. High-cube containers are gaining popularity due to improved interior height and design flexibility, particularly in premium residential projects. Refrigerated containers are also witnessing niche adoption in specialized healthcare, laboratory, and climate-controlled applications. Multi-container hybrid structures are increasingly preferred for luxury villas, commercial offices, and modular apartment complexes due to their scalability and architectural versatility.

Application Insights

Residential housing remains the largest application segment, contributing approximately 46% of global market demand in 2025. Rising urban housing shortages and increasing acceptance of modular living are driving widespread residential adoption. Hospitality applications are among the fastest-growing segments, supported by increasing investments in eco-resorts, boutique hotels, and glamping infrastructure. Workforce accommodation demand from mining, energy, and infrastructure sectors is also expanding rapidly due to the portability and cost-efficiency of container structures. Educational and healthcare infrastructure applications are emerging steadily as governments seek modular solutions for classrooms, clinics, and remote healthcare facilities.

Construction Model Insights

Factory-built modular units dominate the market with nearly 61% share due to superior quality control, faster installation timelines, and reduced labor dependency. Manufacturers increasingly utilize automated fabrication technologies and robotic welding systems to improve scalability and consistency. Plug-and-play modular systems are witnessing rapid adoption for emergency housing and commercial infrastructure applications due to their portability and ease of deployment. Flat-pack modular systems are also expanding in popularity because they reduce transportation costs and simplify international shipping logistics.

End-User Insights

Real estate developers represent the largest end-user segment globally, accounting for nearly 29% of market demand in 2025. Developers are increasingly integrating container-based housing into affordable residential communities, co-living spaces, and mixed-use developments. Individual homeowners are driving strong demand for tiny homes and off-grid living solutions, particularly in North America and Europe. Hospitality operators are rapidly expanding investments in container-based eco-resorts and experiential tourism accommodation. Government agencies and humanitarian organizations are also significant contributors due to growing deployment of modular structures for disaster relief, temporary housing, and public infrastructure expansion.

Price Category Insights

Mid-range container homes currently account for the largest market share, balancing affordability with modern amenities and customization options. Economy container homes remain highly popular in developing economies and workforce accommodation applications due to their low construction costs. Premium and luxury container homes are the fastest-growing category globally, supported by rising consumer interest in sustainable luxury living, architectural innovation, and smart-home integration. Developers increasingly focus on high-end finishes, advanced insulation technologies, and customized interior layouts to differentiate premium offerings.

Explore more data points, trends and opportunities Download Free Sample Report

Container Homes Market Segmentations

By Container Type

- New/One-Trip Shipping Containers

- Used/Repurposed Shipping Containers

- High Cube Containers

- Refrigerated (Reefer) Containers

- Hybrid Modular Containers

By Application

- Residential Housing

- Hospitality & Eco-Resorts

- Workforce Accommodation

- Commercial & Office Infrastructure

- Healthcare Facilities

- Educational Infrastructure

- Emergency & Disaster Relief Housing

By Construction Model

- Factory-Built Modular Units

- On-Site Fabricated Units

- Pre-Assembled Plug-and-Play Units

- Flat-Pack Modular Systems

By End User

- Individual Homeowners

- Real Estate Developers

- Hospitality Operators

- Government & Municipal Authorities

- NGOs & Humanitarian Agencies

- Industrial & Mining Companies

By Price Category

- Economy Container Homes

- Mid-Range Container Homes

- Premium/Luxury Container Homes

Regional Insights

North America

North America accounted for nearly 38% of the global container homes market in 2025, making it the largest regional market. The United States dominates regional demand due to increasing adoption of sustainable construction methods, rising housing costs, and growing popularity of off-grid living. California, Texas, Colorado, and Florida represent key demand centers for tiny homes and modular residential developments. Canada is also experiencing strong growth supported by affordable housing initiatives and demand for remote workforce accommodation solutions.

Europe

Europe represents approximately 24% of global market demand, supported by strong sustainability regulations and widespread adoption of modular construction technologies. Germany, the United Kingdom, the Netherlands, and Nordic countries are major demand centers due to high environmental awareness and government support for green housing initiatives. Luxury eco-resorts and smart modular homes are particularly popular across Western Europe. Rising energy-efficiency standards are further encouraging adoption of insulated container housing systems.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, projected to expand at a CAGR exceeding 9% through 2031. China serves as both a major manufacturing hub and a growing domestic market for modular housing systems. India is witnessing strong demand driven by affordable housing programs, smart-city investments, and urban population growth. Australia represents a mature market for luxury container homes and mining workforce accommodation. Southeast Asian countries are also increasing investments in modular infrastructure to support tourism and industrial expansion.

Latin America

Latin America is gradually expanding its adoption of modular housing solutions, led by Brazil, Mexico, and Chile. Urban housing deficits and rising tourism investments are supporting demand for affordable container-based residential and hospitality infrastructure. Mining operations in Chile and Peru are increasingly utilizing portable workforce accommodation systems. Governments are also exploring modular housing projects to address low-income housing shortages in major urban centers.

Middle East & Africa

The Middle East and Africa region is witnessing growing adoption of container homes for workforce accommodation, tourism infrastructure, and refugee housing applications. The UAE and Saudi Arabia are investing significantly in smart-city and tourism development projects utilizing modular construction technologies. South Africa remains a key African market for container-based residential and commercial infrastructure. Humanitarian housing demand across several African regions also contributes to market growth, particularly through NGO-supported modular shelter projects.

Key Players in the Container Homes Market

- SG Blocks

- HONOMOBO

- Tempohousing

- Giant Containers

- Royal Wolf

- BMarko Structures

- Anderco

- Speed House Group

- IQ Container Homes

- Mods International

- CIMC Modular Building Systems

- Algeco

- Mobile Mini Solutions

- Shanghai Haicheng Special Steel Container

- Supertech Industries