Conductive Ink Pen Market Size

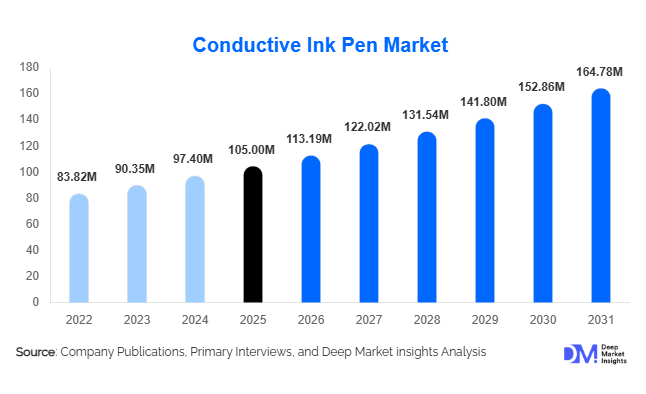

According to Deep Market Insights, the global conductive ink pen market size was valued at USD 105 million in 2025 and is projected to grow from USD 113.19 million in 2026 to reach USD 164.78 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The conductive ink pen market growth is primarily driven by increasing adoption of printed electronics, growing demand for rapid circuit prototyping solutions, rising investments in STEM education programs, and the expansion of flexible and wearable electronic device development globally. Conductive ink pens have become valuable tools across educational institutions, research laboratories, electronics manufacturing facilities, and industrial maintenance operations due to their ability to create conductive traces quickly without complex fabrication equipment.

Key Market Insights

- Silver-based conductive ink pens dominate the market, accounting for approximately 52% of global revenue due to superior conductivity, durability, and compatibility with printed electronics applications.

- Circuit prototyping remains the largest application segment, representing nearly 30% of global demand as startups, R&D centers, and electronics manufacturers increasingly adopt rapid development methodologies.

- Asia-Pacific dominates the global market, holding approximately 41% market share in 2025, supported by strong electronics manufacturing ecosystems in China, Japan, South Korea, Taiwan, and India.

- Flexible and wearable electronics applications are the fastest-growing demand segment, driven by innovations in healthcare monitoring, smart textiles, and flexible sensor technologies.

- E-commerce channels account for more than 42% of global sales, reflecting increasing digital procurement of electronic tools and educational kits.

- Graphene and hybrid conductive materials are emerging as next-generation technologies, helping manufacturers reduce dependence on silver while improving performance characteristics.

Conductive Ink Pen Market Trends

Growing Adoption of Flexible and Printed Electronics

The rapid expansion of flexible electronics, printed sensors, smart packaging, wearable devices, and RFID technologies is significantly increasing demand for conductive ink pens. Research organizations, product developers, and electronics startups are utilizing conductive ink pens for quick validation of flexible circuit designs before transitioning to large-scale production. The increasing use of printed electronic components in healthcare monitoring devices, consumer electronics, automotive interiors, and smart packaging solutions continues to support demand. Conductive ink pens enable engineers and researchers to shorten development cycles and reduce prototyping costs, making them a preferred tool within innovation-driven electronics sectors.

Emergence of Graphene and Hybrid Conductive Ink Technologies

Manufacturers are increasingly investing in graphene, carbon nanotube, and hybrid conductive formulations to address the cost and supply-chain challenges associated with silver-based inks. These advanced materials offer improved flexibility, lower material costs, and enhanced environmental sustainability. Hybrid conductive inks combining metallic and carbon-based materials are gaining popularity in educational, industrial, and wearable electronics applications. As graphene manufacturing scales globally, conductive ink pen manufacturers are expected to launch new product portfolios that provide competitive conductivity performance while reducing exposure to precious metal price volatility.

Conductive Ink Pen Market Drivers

Expansion of Electronics Prototyping and Product Development Activities

The increasing pace of innovation within the electronics industry has significantly increased demand for rapid prototyping solutions. Conductive ink pens allow engineers, product designers, and researchers to develop and test circuit concepts without requiring expensive PCB fabrication processes. Startups and innovation centers are particularly adopting conductive pen technologies to accelerate product development timelines and reduce R&D costs. This trend is especially visible across consumer electronics, IoT devices, wearable technologies, and sensor development applications.

Rising Investments in STEM Education and Electronics Training

Governments and educational institutions worldwide are expanding STEM education programs to address future workforce requirements in electronics, robotics, and engineering sectors. Conductive ink pens provide a practical and cost-effective teaching tool for introducing circuit design concepts. Universities, technical institutes, maker spaces, and K-12 educational programs increasingly incorporate conductive ink kits into laboratory exercises and innovation programs. The growing focus on experiential learning continues to create substantial recurring demand within the education segment.

Conductive Ink Pen Market Restraints

Volatility in Silver Prices and Raw Material Costs

Silver remains the most widely used conductive material due to its excellent electrical properties. However, fluctuations in silver prices directly impact manufacturing costs and product pricing. Market participants face ongoing challenges in maintaining profitability while remaining competitive in price-sensitive segments such as education and consumer hobbyist applications. Raw material price volatility continues to influence procurement strategies and long-term product planning.

Performance Limitations Compared to Traditional PCB Manufacturing

Although conductive ink pens provide exceptional flexibility for prototyping and repair applications, they cannot fully match the conductivity, reliability, and miniaturization capabilities offered by conventional PCB manufacturing technologies. Certain high-performance electronics applications continue to require traditional fabrication methods, limiting conductive ink pen adoption in large-scale commercial production environments. Manufacturers must continue improving conductivity, adhesion, and durability characteristics to expand application opportunities.

Conductive Ink Pen Market Opportunities

Growth of Wearable Electronics and Smart Textile Development

The rapid expansion of wearable healthcare devices, smart clothing, fitness trackers, and flexible sensors presents significant opportunities for conductive ink pen manufacturers. Product developers increasingly rely on conductive ink pens during the early stages of wearable circuit design and testing. The growing adoption of connected healthcare devices and personalized electronics is expected to create substantial long-term demand for advanced conductive prototyping tools.

Industrial Maintenance and PCB Repair Applications

Electronics manufacturers and maintenance service providers are increasingly utilizing conductive ink pens for PCB trace restoration, component rework, and rapid repair applications. These tools reduce equipment downtime and provide a cost-effective alternative to complete board replacement. Industrial-grade conductive ink formulations designed for aerospace, automotive, and defense electronics applications are expected to create attractive growth opportunities for manufacturers serving high-value end-user industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 105 Million |

| Market Size in 2026 | USD 113.19 Million |

| Market Size in 2031 | USD 164.78 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Silver conductive ink pens dominated the global conductive ink pen market, accounting for approximately 52% of total revenue in 2025. The segment continues to lead due to its unmatched electrical conductivity, superior oxidation resistance, excellent adhesion properties, and long operational lifespan compared to alternative conductive materials. Silver-based formulations are extensively used in advanced electronics prototyping, PCB repair, sensor development, RFID antenna fabrication, and printed electronics research, where conductivity performance is critical. The growing adoption of flexible electronics, wearable devices, and next-generation printed sensors has further reinforced demand for silver conductive inks, particularly in North America, Europe, Japan, South Korea, and China, where innovation activity remains concentrated.

The segment's leadership is also supported by increasing investments in semiconductor research, electronics miniaturization, and advanced manufacturing technologies. Educational institutions and research laboratories continue to favor silver conductive pens due to their reliability and ease of use in experimental applications. While silver remains the premium material category, manufacturers are actively developing cost-optimized formulations to address raw material price volatility.

Carbon-based conductive pens, including graphene and carbon nanotube (CNT) formulations, are emerging as the fastest-growing material category due to lower production costs, enhanced sustainability, and improving conductivity performance. These products are increasingly being adopted in educational projects, smart packaging, and flexible electronics applications. Copper-based conductive pens continue gaining traction in cost-sensitive industrial applications, while conductive polymer-based formulations are creating opportunities within wearable electronics and biomedical device development. Hybrid conductive ink systems combining metallic and carbon-based materials are increasingly being commercialized to balance conductivity performance, flexibility, and affordability.

Application Insights

Circuit prototyping remained the largest application segment, accounting for nearly 30% of global market demand in 2025. The segment's dominance is primarily driven by the accelerating pace of electronics innovation across consumer electronics, IoT devices, wearable technologies, industrial automation systems, and smart sensors. Conductive ink pens allow engineers, product developers, startups, and researchers to rapidly validate circuit concepts without incurring the cost and time associated with conventional PCB fabrication processes. As product development cycles continue to shorten globally, rapid prototyping solutions have become increasingly important across both commercial and academic environments.

The segment also benefits from growing investments in electronics incubation centers, startup ecosystems, university research programs, and maker spaces. Conductive ink pens significantly reduce prototyping costs while enabling quick design modifications, making them highly attractive for early-stage product development activities. In addition, the rise of open-source hardware platforms and DIY electronics communities continues to create substantial demand for circuit prototyping tools.

PCB repair and rework applications remain an important revenue contributor, particularly within electronics manufacturing facilities seeking cost-effective maintenance solutions. Meanwhile, flexible electronics development, wearable device prototyping, RFID and NFC antenna creation, printed sensor fabrication, and smart packaging applications represent the fastest-growing opportunities. Growing adoption of Industry 4.0 technologies, connected devices, and printed electronic components is expected to further expand the application scope of conductive ink pens during the forecast period.

Distribution Channel Insights

E-commerce platforms accounted for approximately 42% of global conductive ink pen sales in 2025, making them the largest distribution channel. The leadership of online sales channels is driven by increasing digital procurement practices, wider product availability, transparent pricing structures, and easy access to technical specifications and customer reviews. E-commerce platforms enable manufacturers to reach a global customer base while providing educational institutions, hobbyists, researchers, and industrial users with convenient purchasing options.

The growth of online electronics marketplaces and direct-to-consumer sales models has significantly improved market accessibility, particularly in developing regions where specialized electronics retailers may have limited presence. Educational kits, prototyping tools, and DIY electronics products are increasingly purchased through online platforms due to broader product selection and faster product comparison capabilities.

Direct sales channels continue to play a critical role for industrial customers, government laboratories, and large educational institutions requiring technical support, customized formulations, and volume-based procurement agreements. Specialty electronics retailers remain relevant among professional engineers and maker communities, while educational supply distributors maintain strong penetration within academic markets. Continued digitalization of industrial procurement systems and expansion of B2B e-commerce ecosystems are expected to further strengthen online channel dominance over the coming years.

End-User Insights

Electronics manufacturers represented the largest end-user segment, accounting for approximately 28% of global market demand in 2025. The segment's leadership is directly linked to the rapid expansion of electronics manufacturing activities worldwide, particularly across Asia-Pacific, North America, and Europe. Conductive ink pens are widely utilized for PCB trace repair, circuit testing, rapid prototyping, product validation, and production support functions. As electronics manufacturers seek faster and more cost-efficient development processes, conductive ink technologies are increasingly integrated into engineering and maintenance workflows.

The continued growth of semiconductor manufacturing, consumer electronics production, industrial automation systems, electric vehicles, and connected devices is further supporting demand from this segment. Electronics manufacturers benefit from reduced prototyping lead times and lower maintenance costs through the adoption of conductive ink pen solutions.

Educational institutions and research laboratories constitute the second-largest consumer category, driven by increasing investments in STEM education, engineering programs, electronics training, and innovation-focused research initiatives. Automotive OEMs and aerospace organizations are increasingly utilizing conductive ink technologies for electronics testing and prototype development. Meanwhile, the healthcare sector is emerging as one of the fastest-growing end-user segments, supported by rising development of wearable medical devices, biosensors, smart diagnostic platforms, and flexible healthcare electronics.

Explore more data points, trends and opportunities Download Free Sample Report

Conductive Ink Pen Market Segmentations

By Material Type

- Silver Conductive Ink Pens

- Copper Conductive Ink Pens

- Carbon-Based Conductive Ink Pens

- Nickel Conductive Ink Pens

- Conductive Polymer Ink Pens

- Hybrid Conductive Ink Pens

By Application

- Circuit Prototyping

- PCB Repair and Rework

- Flexible Electronics Development

- Wearable Electronics

- RFID and NFC Antenna Drawing

- Sensor Fabrication

- Educational STEM Projects

- Research Laboratory Applications

- DIY Electronics and Maker Projects

- Smart Packaging Development

By Distribution Channel

- Direct Sales

- Industrial Distributors

- E-Commerce Platforms

- Educational Supply Distributors

- Specialty Electronics Retailers

By End User

- Electronics Manufacturers

- Educational Institutions

- Research Institutes & Universities

- Industrial Maintenance Providers

- Automotive OEMs & Tier Suppliers

- Aerospace & Defense Organizations

- Healthcare Device Developers

- Consumer Hobbyists & Makers

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 41% of the global conductive ink pen market in 2025, making it the largest regional market. The region's leadership is primarily driven by its dominant position in global electronics manufacturing, semiconductor production, printed electronics development, and consumer electronics exports. China alone accounts for nearly 18% of global demand due to its extensive electronics supply chain, strong government support for advanced manufacturing, and growing investments in flexible electronics technologies. The country's expanding printed electronics ecosystem and increasing adoption of smart manufacturing technologies continue to generate substantial demand for conductive prototyping tools.

Japan and South Korea remain key innovation hubs for flexible displays, wearable electronics, advanced sensors, and conductive material technologies. Both countries benefit from strong R&D investments and high concentrations of electronics manufacturers. India is emerging as one of the fastest-growing markets in the region due to initiatives such as electronics manufacturing expansion, semiconductor investments, startup ecosystem growth, and increasing STEM education funding. Taiwan's leadership in semiconductor fabrication and electronics design services further supports regional market growth. The combination of manufacturing scale, export-oriented production, and rising research expenditures continues to position Asia-Pacific as the primary growth engine for the conductive ink pen market.

North America

North America accounted for approximately 28% of global market revenue in 2025, with the United States representing nearly 22% of worldwide demand. Regional growth is driven by strong investments in electronics research and development, advanced manufacturing technologies, aerospace and defense programs, and innovation-driven startup ecosystems. The United States hosts a significant concentration of semiconductor companies, technology startups, engineering institutions, and maker communities that actively utilize conductive ink technologies for rapid prototyping and product development.

Government support for domestic semiconductor production, growing investments in flexible electronics research, and increasing commercialization of wearable devices continue to stimulate market demand. Universities and national research laboratories remain major consumers of conductive ink products due to extensive research activities in printed electronics and advanced materials. Canada contributes through growing adoption across industrial automation, technical education, and electronics maintenance applications. Strong innovation infrastructure and high R&D expenditure remain the primary growth drivers across the region.

Europe

Europe accounted for approximately 22% of the global conductive ink pen market in 2025. The region's demand is largely driven by advanced automotive electronics, industrial automation systems, sustainable manufacturing initiatives, and growing investments in printed electronics technologies. Germany remains the largest market within Europe due to its strong automotive engineering base, industrial electronics sector, and leadership in Industry 4.0 implementation. The country's focus on smart manufacturing and connected industrial systems continues to support demand for rapid electronics prototyping tools.

The United Kingdom, France, Italy, and the Netherlands are significant consumers of conductive ink pens within universities, research laboratories, and technology development organizations. Growing investments in flexible electronics, smart packaging, wearable healthcare technologies, and sustainable conductive materials are further expanding market opportunities. Additionally, stringent environmental regulations are encouraging innovation in low-toxicity and environmentally friendly conductive formulations, supporting long-term market growth throughout the region.

Latin America

Latin America represented approximately 5% of global market demand in 2025, led by Brazil and Mexico. Regional growth is supported by increasing investments in electronics assembly operations, industrial automation projects, technical education programs, and manufacturing modernization initiatives. Mexico benefits significantly from its integration into North American electronics and automotive supply chains, creating growing demand for electronics testing, maintenance, and prototyping solutions.

Brazil remains the largest market in South America due to expanding industrial manufacturing activities and increasing adoption of engineering education programs. The region is also witnessing growing participation in STEM-focused educational initiatives, which is creating additional demand for conductive ink pens in academic environments. Although market penetration remains lower than in developed regions, improving industrial infrastructure and increasing electronics production activities are expected to support steady future growth.

Middle East & Africa

The Middle East & Africa accounted for approximately 4% of global market revenue in 2025. While still at an emerging stage, the region is experiencing increasing demand driven by economic diversification strategies, technology-focused investments, and industrial development initiatives. The United Arab Emirates and Saudi Arabia are leading markets due to substantial investments in advanced manufacturing, smart city projects, technical education, and innovation ecosystems. Government programs aimed at reducing dependence on oil revenues are encouraging the development of technology-intensive industries, creating new opportunities for conductive ink technologies.

South Africa remains an important market due to demand from educational institutions, electronics maintenance services, and industrial sectors. Across the region, increasing investments in engineering education, vocational training programs, and digital transformation initiatives are supporting gradual market expansion. The emergence of regional technology hubs and innovation centers is expected to further strengthen demand for conductive prototyping and electronics development tools over the forecast period.

Key Players in the Conductive Ink Pen Market

- Chemtronics

- Circuit Scribe

- MG Chemicals

- Bare Conductive

- Electroninks

- Heraeus

- Henkel

- DuPont

- Creative Materials

- NovaCentrix

- Sun Chemical

- Vorbeck Materials

- Applied Ink Solutions

- Intrinsiq Materials

- Advanced Nano Products