Commercial Office Furniture Market Size

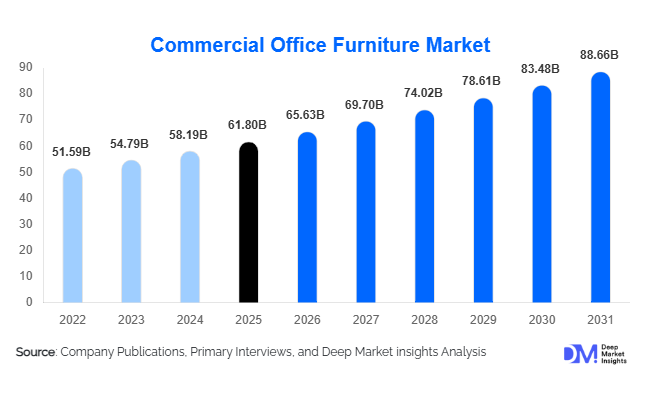

According to Deep Market Insights, the global commercial office furniture market size was valued at USD 61.8 billion in 2025 and is projected to grow from USD 65.63 billion in 2026 to reach USD 88.66 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The commercial office furniture market growth is being driven by rising investments in workplace modernization, increasing adoption of hybrid work models, growing demand for ergonomic office environments, and continued expansion of commercial office infrastructure across developed and emerging economies. Organizations are increasingly viewing workplace design as a strategic tool for enhancing employee productivity, talent retention, collaboration, and corporate sustainability objectives. The shift toward flexible workspaces, collaborative environments, and wellness-oriented office designs has significantly increased demand for advanced furniture solutions, including ergonomic seating, height-adjustable desks, modular workstations, acoustic pods, and technology-integrated furniture systems.

Key Market Insights

- Ergonomic seating remains the largest product category, accounting for nearly 32% of global commercial office furniture revenues in 2025.

- Hybrid workplace transformation is reshaping procurement strategies, driving demand for modular furniture, collaborative workstations, and flexible office layouts.

- Asia-Pacific dominates the global market, representing approximately 41% of total revenues, led by China, India, Japan, and Southeast Asian economies.

- India is emerging as the fastest-growing country market, supported by GCC expansion, technology investments, and commercial real estate development.

- Sustainability-focused procurement is becoming a major purchasing criterion, with enterprises prioritizing recycled materials, low-emission furniture, and circular economy solutions.

- Smart furniture integration, including occupancy sensors, connected desks, workspace analytics, and IoT-enabled office systems, is creating new revenue opportunities for manufacturers.

Commercial Office Furniture Market Trends

Growing Adoption of Hybrid Workplace Furniture Solutions

The transition toward hybrid working models is fundamentally changing office furniture demand globally. Organizations are redesigning traditional office layouts to support collaboration, flexibility, and employee engagement rather than fixed desk occupancy. This has accelerated investments in modular workstations, collaborative seating systems, acoustic furniture, mobile desks, and reconfigurable meeting spaces. Hybrid office environments require furniture that can be easily adapted to changing occupancy levels and team structures. As a result, manufacturers are increasingly introducing flexible product portfolios designed to maximize space utilization while improving workplace functionality. Corporate workplace redesign initiatives across North America and Europe are particularly supporting growth in this segment.

Increasing Demand for Sustainable and Circular Furniture Solutions

Sustainability has become a central purchasing factor within commercial office furniture procurement. Organizations are increasingly prioritizing products manufactured from recycled steel, reclaimed wood, sustainable timber, recyclable plastics, and low-emission materials. Furniture manufacturers are responding by introducing circular economy programs that include refurbishment, product take-back services, recycling initiatives, and extended product lifecycles. Certifications such as FSC, GREENGUARD, BIFMA LEVEL, and LEED compatibility are becoming key differentiators in competitive bidding processes. As ESG reporting requirements become more stringent globally, sustainable office furniture is expected to capture an increasing share of future procurement budgets.

Commercial Office Furniture Market Drivers

Expansion of Commercial Real Estate and Corporate Infrastructure

The growth of commercial office construction remains one of the strongest drivers for the commercial office furniture market. New business parks, technology campuses, financial districts, government buildings, and mixed-use developments continue to generate significant furniture procurement demand. Rapid urbanization and economic diversification initiatives across Asia-Pacific and the Middle East are supporting large-scale investments in commercial infrastructure. Countries such as India, China, Saudi Arabia, and the UAE are witnessing substantial office construction activity, creating long-term opportunities for furniture manufacturers and workplace solution providers.

Rising Focus on Employee Wellness and Workplace Productivity

Organizations increasingly recognize the relationship between workplace design, employee well-being, and productivity. As a result, ergonomic furniture solutions such as task chairs, sit-stand desks, adjustable workstations, and wellness-oriented office layouts are becoming standard workplace investments. Companies are allocating larger budgets toward workplace enhancements designed to improve employee comfort, reduce musculoskeletal disorders, and support talent retention initiatives. This trend is particularly prominent among technology firms, financial institutions, consulting organizations, and multinational corporations.

Commercial Office Furniture Market Restraints

Volatility in Raw Material Prices

The commercial office furniture industry remains highly exposed to fluctuations in steel, aluminum, engineered wood, foam, plastic, and logistics costs. Significant variations in commodity prices can impact production economics and compress manufacturer profit margins. Rising transportation expenses and supply chain disruptions further increase operational complexity, particularly for companies operating global manufacturing networks. These cost pressures often lead to higher product prices, which can delay procurement decisions among cost-sensitive customers.

Intense Price Competition Across Commodity Segments

The market remains highly competitive, particularly in standard seating, storage, and workstation categories. Regional manufacturers and low-cost imports continue to exert pricing pressure, especially within developing economies. Product commoditization can reduce profitability and limit differentiation opportunities for manufacturers operating in the economy and mid-range segments. Maintaining product innovation, sustainability credentials, and service quality has therefore become increasingly important for sustaining competitive advantages.

Commercial Office Furniture Market Opportunities

Expansion of Smart and Connected Office Furniture

The integration of smart technologies into office furniture presents significant growth opportunities for manufacturers. IoT-enabled desks, occupancy monitoring systems, workspace analytics platforms, wireless charging solutions, and sensor-integrated workstations are gaining traction among large enterprises seeking data-driven workplace optimization. Smart office furniture not only enhances employee experience but also enables organizations to improve space utilization and operational efficiency. As digital workplace transformation accelerates globally, connected furniture solutions are expected to become a major premium product category.

Emerging Market Commercial Infrastructure Development

Rapid commercial development across India, Southeast Asia, the Middle East, and Africa presents substantial opportunities for industry participants. Government initiatives focused on smart cities, technology parks, financial districts, and industrial corridors are creating strong demand for office furniture solutions. Multinational corporations establishing regional headquarters in emerging markets further contribute to demand growth. Manufacturers that establish local production capabilities and region-specific product portfolios can benefit from lower costs, faster delivery times, and stronger customer relationships.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 61.8 Billion |

| Market Size in 2026 | USD 65.63 Billion |

| Market Size in 2031 | USD 88.66 Billion |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Seating furniture remains the largest product category within the commercial office furniture market, accounting for approximately 32% of total revenues in 2025. Demand is driven by ongoing investments in ergonomic office environments and workplace wellness initiatives. Task chairs continue to dominate procurement volumes due to their widespread application across corporate offices, government institutions, and educational facilities. Workstations and desks represent the second-largest segment, supported by demand for modular and height-adjustable solutions that accommodate hybrid working models. Office systems and partitions are experiencing robust growth as organizations increasingly prioritize flexible workspace configurations and acoustic privacy solutions. Storage furniture remains essential for traditional office environments, while reception and common-area furniture are benefiting from increased investments in employee experience and workplace aesthetics.

Material Insights

Wood-based furniture remains the dominant material segment, representing approximately 44% of global market revenues. Engineered wood products are particularly popular due to their affordability, versatility, and sustainability improvements. Metal furniture continues to gain market share owing to its durability, strength, and suitability for modular office systems. Recycled and sustainable materials are emerging as one of the fastest-growing material categories as enterprises seek environmentally responsible procurement solutions. Composite materials combining wood, metal, and polymer components are increasingly used in premium office furniture designs that balance aesthetics, functionality, and durability.

Distribution Channel Insights

Direct enterprise procurement remains the leading distribution channel, accounting for approximately 65% of global market revenues. Large organizations typically purchase furniture through direct manufacturer contracts, allowing for customization, project management support, and large-scale deployment. Office furniture dealers and contract furniture specialists continue to play an important role in serving mid-sized enterprises and regional markets. E-commerce channels are experiencing rapid growth, particularly among small and medium-sized businesses seeking streamlined procurement processes and transparent pricing. Digital configuration tools, virtual showrooms, and online product customization capabilities are further supporting online sales growth.

End-Use Industry Insights

Corporate offices remain the largest end-use segment, contributing approximately 42% of global commercial office furniture demand. Technology companies continue to be among the most significant buyers due to ongoing campus expansion and workplace transformation projects. The BFSI sector represents another major demand source, driven by branch modernization initiatives and corporate office investments. Government and public administration organizations maintain stable demand through workplace modernization programs and public infrastructure projects. Co-working operators are among the fastest-growing end users, reflecting the increasing popularity of flexible workspace models across major urban centers worldwide.

Enterprise Size Insights

Large enterprises account for the largest share of commercial office furniture demand, representing approximately 52% of market revenues. These organizations typically undertake large-scale procurement projects, workplace redesign initiatives, and recurring furniture replacement programs. Medium-sized enterprises continue to generate significant demand through office expansion and modernization activities. Small businesses increasingly contribute to market growth through flexible workspace adoption and digital procurement channels that simplify purchasing processes. The growing startup ecosystem across Asia-Pacific and North America is further supporting furniture demand among smaller organizations.

Explore more data points, trends and opportunities Download Free Sample Report

Commercial Office Furniture Market Segmentations

By Product Type

- Seating Furniture

- Workstations & Desks

- Tables

- Storage Furniture

- Office Systems & Partitions

- Reception & Common Area Furniture

- Accessories & Ancillary Furniture

By Material

- Wood

- Metal

- Plastic & Polymer

- Glass

- Composite & Hybrid Materials

- Sustainable/Recycled Materials

By Distribution Channel

- Direct Sales

- Office Furniture Dealers

- Contract Furniture Specialists

- E-commerce Platforms

- Retail Showrooms

By Workspace Configuration

- Traditional Office Layouts

- Open-Plan Offices

- Hybrid Workspaces

- Co-working Spaces

- Activity-Based Working Environments

By End-Use Industry

- Corporate Offices

- Information Technology & ITES

- Banking, Financial Services & Insurance (BFSI)

- Government & Public Administration

- Education

- Healthcare Administration

- Legal & Consulting Firms

- Manufacturing Administrative Offices

- Co-working Operators

- Real Estate & Business Services

- Telecommunications

- Others

Regional Insights

Asia-Pacific

Asia-Pacific dominates the commercial office furniture market with approximately 41% of global revenues. China remains the largest individual market due to its extensive commercial construction sector, strong manufacturing base, and large corporate workforce. India is the fastest-growing country market, supported by technology sector expansion, Global Capability Center (GCC) growth, and increasing foreign direct investment. Japan and South Korea continue to generate demand through office modernization initiatives, while Southeast Asian countries such as Vietnam, Indonesia, and Thailand are benefiting from increasing commercial real estate development and multinational corporate investments.

North America

North America accounts for approximately 28% of global market revenues, with the United States representing nearly 24% of worldwide demand. Hybrid workplace transformation, ergonomic furniture adoption, and premium office design trends continue to drive market growth. Large technology firms, financial institutions, and professional services organizations remain key purchasers. Canada contributes additional demand through government modernization programs and growing technology-sector investments.

Europe

Europe represents approximately 23% of global market demand. Germany remains the region's largest market, supported by its strong industrial base and corporate sector. The United Kingdom, France, Italy, and the Netherlands continue to invest heavily in sustainable office environments. European organizations are particularly focused on ESG compliance, circular procurement practices, and low-carbon workplace solutions, creating strong demand for environmentally certified furniture products.

Latin America

Brazil leads the Latin American market, followed by Mexico, Chile, and Colombia. Demand is supported by commercial property investments, multinational corporate expansion, and modernization of business infrastructure. While regional growth remains moderate compared to Asia-Pacific, increasing urbanization and service-sector development continue to create opportunities for office furniture suppliers.

Middle East & Africa

The Middle East and Africa region is experiencing strong growth driven by large-scale commercial development projects. Saudi Arabia and the UAE are leading demand through economic diversification initiatives, financial center development, and government infrastructure programs. South Africa remains the largest market in Africa, while increasing investments in commercial real estate across Nigeria, Kenya, and Egypt are supporting additional growth opportunities.

Key Players in the Commercial Office Furniture Market

- Steelcase

- MillerKnoll

- Haworth

- HNI Corporation

- Okamura Corporation

- Kokuyo

- Kinnarps

- Global Furniture Group

- Fursys

- ITOKI Corporation

- Kimball International

- UE Furniture

- Aurora Corporation

- AIS Inc.

- Teknion