Ceramic Tableware Market Size

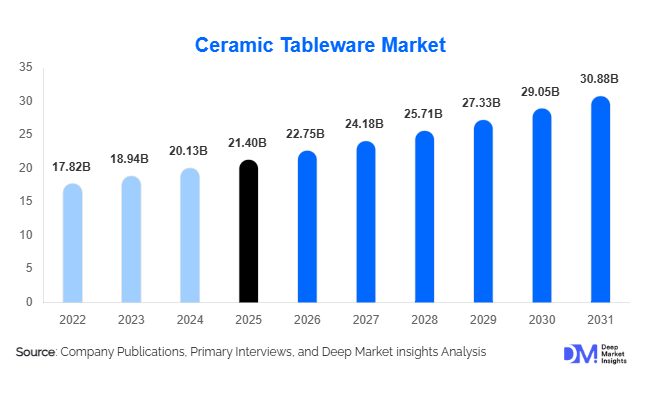

According to Deep Market Insights, the global ceramic tableware market size was valued at USD 21.4 billion in 2025 and is projected to grow from USD 22.75 billion in 2026 to reach USD 30.88 billion by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The ceramic tableware market growth is primarily driven by rising consumer spending on premium dining experiences, increasing demand from the hospitality sector, growing preference for sustainable reusable tableware, and the expansion of organized retail and e-commerce channels globally. Ceramic tableware continues to gain popularity due to its durability, aesthetic appeal, food safety characteristics, and ability to complement evolving interior décor trends. Manufacturers are increasingly investing in innovative glazing technologies, customized designs, and eco-friendly production methods to address changing consumer preferences. In addition, the expansion of hotels, restaurants, cafés, and catering services across emerging economies is creating sustained demand for commercial-grade ceramic tableware products.

Key Market Insights

- Porcelain remains the dominant material category, accounting for more than 58% of global ceramic tableware demand due to its durability, premium appearance, and stain resistance.

- Residential households represent the largest end-user segment, contributing nearly 65% of global market revenues in 2025.

- Asia-Pacific dominates the global ceramic tableware market, supported by strong manufacturing capabilities, rising urbanization, and growing consumer spending.

- The hospitality industry represents the fastest-growing demand segment, driven by expanding tourism, hotel construction, and restaurant development globally.

- E-commerce is transforming purchasing behavior, enabling direct-to-consumer sales and expanding access to premium and artisanal ceramic brands.

- Sustainability initiatives and restrictions on single-use products are accelerating demand for reusable ceramic dining and serving solutions.

Ceramic Tableware Market Trends

Premium and Designer Tableware Driving Market Expansion

Consumers are increasingly viewing tableware as an extension of lifestyle and interior décor preferences. Premium ceramic collections featuring handcrafted finishes, artistic patterns, luxury collaborations, and minimalist designs are gaining widespread popularity across developed and emerging markets. Manufacturers are launching designer collections targeted toward affluent consumers and hospitality operators seeking differentiated dining experiences. Social media platforms and home décor trends have further accelerated demand for aesthetically appealing ceramic tableware, particularly among younger urban consumers. Premiumization is allowing manufacturers to achieve higher margins while creating opportunities for customization and limited-edition collections.

Sustainable Manufacturing and Eco-Friendly Ceramics Gaining Momentum

Environmental awareness is becoming a major purchasing consideration in the ceramic tableware market. Manufacturers are investing in lead-free glazing technologies, energy-efficient kilns, recycled packaging materials, and low-emission production processes to meet sustainability objectives. Consumers are increasingly replacing disposable and plastic-based dining products with durable ceramic alternatives. Hospitality operators are also prioritizing reusable serving solutions to align with sustainability commitments and regulatory requirements. These trends are encouraging innovation across the ceramic value chain and creating long-term growth opportunities for environmentally responsible producers.

Ceramic Tableware Market Drivers

Expansion of the Global Hospitality Industry

The continued growth of hotels, restaurants, cafés, resorts, and catering services is generating substantial demand for ceramic tableware products. Commercial dining establishments regularly replace plates, bowls, serving platters, and beverageware to maintain hygiene standards and aesthetic consistency. Increasing tourism activity and rising investments in hospitality infrastructure across Asia-Pacific, the Middle East, and Europe are supporting long-term demand growth. Premium dining concepts are further driving purchases of customized ceramic tableware that enhances brand identity and customer experience.

Rising Consumer Expenditure on Home Décor and Dining Experiences

Modern consumers increasingly prioritize home aesthetics and dining presentation, driving demand for premium ceramic tableware collections. Growing disposable incomes, urbanization, and changing lifestyle preferences are encouraging consumers to invest in coordinated dining sets and decorative serving products. The influence of social media, food photography, and home entertaining trends is further stimulating purchases of premium and visually distinctive ceramic products. Manufacturers continue to introduce innovative designs to cater to this evolving consumer demand.

Ceramic Tableware Market Restraints

High Energy and Manufacturing Costs

Ceramic tableware production requires energy-intensive firing processes, making manufacturers vulnerable to fluctuations in electricity and fuel prices. Rising energy costs have increased production expenses across major manufacturing regions, placing pressure on operating margins and product pricing. Smaller manufacturers often face challenges in adopting advanced kiln technologies due to high capital investment requirements. These cost pressures can impact competitiveness, particularly in price-sensitive markets.

Competition from Alternative Materials

The ceramic tableware market faces growing competition from glassware, melamine products, stainless steel dining solutions, bamboo-based alternatives, and other lightweight materials. Cost-conscious consumers and commercial buyers often select lower-cost alternatives, particularly for high-volume applications. While ceramics offer superior aesthetics and durability, competition from substitute materials remains a challenge, especially in emerging markets where affordability strongly influences purchasing decisions.

Ceramic Tableware Market Opportunities

Growth of Hospitality Infrastructure in Emerging Economies

Rapid expansion of hotels, resorts, restaurants, and tourism facilities across India, Southeast Asia, the Middle East, and Africa presents significant opportunities for ceramic tableware manufacturers. Government-led tourism initiatives and increasing foreign direct investments in hospitality infrastructure are creating large-scale procurement opportunities. Commercial establishments increasingly seek durable, customized, and aesthetically appealing ceramic products to enhance guest experiences and brand differentiation.

Sustainable Product Innovation and Circular Manufacturing

Growing consumer preference for environmentally responsible products is encouraging manufacturers to develop sustainable ceramic solutions. Opportunities exist in lead-free glazes, recycled raw materials, renewable energy-powered manufacturing, and eco-certified product lines. Companies investing in sustainable production methods are likely to benefit from stronger consumer acceptance, enhanced brand reputation, and improved access to environmentally conscious institutional buyers. Sustainability certifications are also becoming an important differentiator within premium market segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 21.4 Billion |

| Market Size in 2026 | USD 22.75 Billion |

| Market Size in 2031 | USD 30.88 Billion |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dinnerware remains the largest product category within the ceramic tableware market, accounting for approximately 41.5% of global revenues in 2025. Plates, bowls, serving dishes, and coordinated dining sets continue to represent the highest-volume products due to their widespread use across households and commercial establishments. Beverageware products, including mugs, cups, and tea sets, constitute a significant secondary segment supported by rising coffee and tea consumption globally. Serveware products such as platters, trays, and serving bowls are witnessing increased demand from hospitality operators seeking elevated dining presentation. Specialty ceramic products, including oven-to-table cookware and decorative collections, are gaining traction among premium consumers looking for multifunctional and aesthetically appealing dining solutions.

Material Type Insights

Porcelain dominates the ceramic tableware market with an estimated 58.5% share of global revenues in 2025. Its superior durability, elegant appearance, and resistance to staining make it the preferred material across residential and hospitality applications. Bone china remains a prominent premium segment, particularly among luxury consumers and fine-dining establishments seeking lightweight yet durable products. Stoneware is experiencing strong demand due to its rustic aesthetics and affordability, making it popular among modern households. Earthenware products continue to maintain relevance in regional and artisanal markets, while vitreous china and specialty ceramic materials serve niche premium applications requiring enhanced durability and visual appeal.

Distribution Channel Insights

Hypermarkets and supermarkets account for the largest distribution channel share, contributing approximately 33.6% of global sales. These outlets offer consumers extensive product selections and competitive pricing, making them a preferred purchasing destination. Specialty homeware retailers continue to play a critical role in premium product sales, particularly within developed markets. E-commerce platforms represent the fastest-growing distribution channel as consumers increasingly seek convenience, broader product variety, and direct access to global brands. Direct-to-business sales remain essential for hospitality and institutional customers, enabling manufacturers to secure large-volume contracts and customized product orders. Brand-owned stores are also expanding to strengthen customer engagement and showcase premium collections.

End User Insights

Residential households account for approximately 64.6% of global ceramic tableware demand, supported by rising home improvement spending, urbanization, and lifestyle-driven purchasing behavior. Consumers increasingly invest in premium dining sets and decorative tableware to complement modern interiors and enhance home dining experiences. The hospitality sector represents the fastest-growing end-user segment, driven by expanding tourism infrastructure and increasing demand for customized dining solutions. Hotels, restaurants, cafés, and catering companies are significant purchasers of ceramic tableware due to its durability and premium presentation characteristics. Institutional users, including healthcare facilities, educational institutions, and corporate cafeterias, continue to generate steady demand for durable and reusable dining products.

Design Category Insights

Contemporary minimalist designs represent the leading design category, accounting for approximately 28% of global demand. Consumers increasingly favor clean aesthetics, neutral color palettes, and versatile tableware that complements modern interior styles. Decorative and printed ceramics remain popular among traditional households and regional markets where cultural patterns and artistic designs influence purchasing decisions. Handmade and artisan ceramic collections are gaining popularity among premium consumers seeking authenticity and uniqueness. Ethnic-inspired and heritage-themed collections also continue to attract niche consumer segments, particularly within tourism-driven and luxury retail channels.

Explore more data points, trends and opportunities Download Free Sample Report

Ceramic Tableware Market Segmentations

By Product Type

- Dinnerware

- Beverageware

- Serveware

- Specialty Tableware

- Gift & Premium Collections

By Material Type

- Porcelain

- Bone China

- Stoneware

- Earthenware

- Vitreous China

- Fine Ceramics & Artisan Ceramics

By End User

- Residential Households

- Hospitality (Hotels, Restaurants & Cafés)

- Institutional Users

- Catering & Event Services

By Distribution Channel

- Hypermarkets & Supermarkets

- Specialty Homeware Stores

- Department Stores

- Brand-Owned Stores

- E-Commerce Platforms

- Direct-to-Business Sales

By Design Category

- Plain / Solid Color

- Printed / Decorative

- Handmade Artistic

- Contemporary Minimalist

- Ethnic & Traditional Designs

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 34.5% of the global ceramic tableware market and remains both the largest and fastest-growing regional market. China dominates regional demand and production due to its extensive ceramic manufacturing infrastructure and strong export capabilities. India is emerging as a major growth market supported by urbanization, rising disposable incomes, and expansion of hospitality and foodservice industries. Japan and South Korea contribute significantly through premium ceramic consumption and advanced manufacturing capabilities. Increasing household spending and tourism investments continue to strengthen regional demand.

Europe

Europe represents approximately 28% of global market revenues and remains a key market for premium ceramic tableware products. Germany, the United Kingdom, France, and Italy drive regional demand through strong hospitality sectors and high consumer spending on home décor products. European consumers increasingly prioritize sustainable and high-quality tableware, encouraging demand for premium porcelain and designer collections. Established ceramic manufacturing traditions across the region continue to support innovation and product differentiation.

North America

North America accounts for approximately 24% of global market demand, led primarily by the United States. Strong consumer spending, growing interest in home dining experiences, and high e-commerce penetration continue to support market growth. Premium ceramic products and customized tableware solutions are particularly popular among affluent households and upscale hospitality establishments. Canada contributes additional demand through steady residential consumption and expanding foodservice activity.

Latin America

Latin America represents approximately 5.5% of global demand, with Brazil and Mexico serving as the primary consumption markets. Urbanization, rising middle-class incomes, and growth in organized retail channels are supporting market expansion. Hospitality and tourism investments are creating additional demand opportunities for commercial ceramic tableware products across the region.

Middle East & Africa

The Middle East and Africa account for approximately 8% of global market revenues. Saudi Arabia and the United Arab Emirates are driving regional growth through significant investments in hospitality infrastructure, tourism development, and luxury dining establishments. Increasing international visitor arrivals and government-led tourism diversification programs continue to create favorable conditions for ceramic tableware demand. South Africa remains an important regional market supported by a well-established hospitality sector.

Key Players in the Ceramic Tableware Market

- Villeroy & Boch

- Portmeirion Group

- Steelite International

- Churchill China

- Noritake Co., Limited

- Rosenthal GmbH

- Lenox Corporation

- Denby Pottery Company Ltd.

- Fiskars Group

- Kahla Porzellan GmbH

- Libbey Inc.

- Bernardaud

- BHS Tabletop AG

- RAK Porcelain

- Wedgwood