Warehouse Clubs Market Size

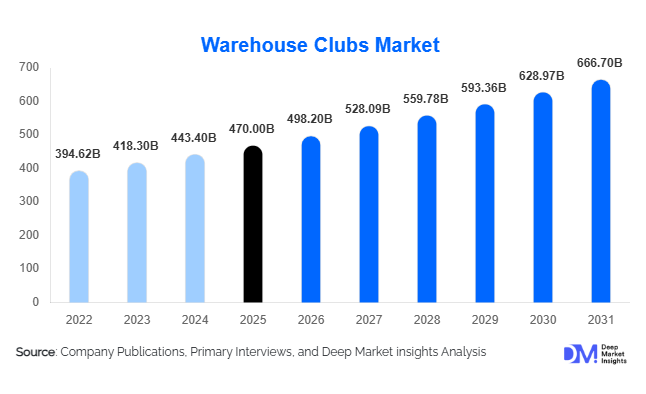

According to Deep Market Insights, the global warehouse clubs market size was valued at USD 470.0 billion in 2025 and is projected to grow from USD 498.20 billion in 2026 to reach USD 666.70 billion by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The warehouse clubs market growth is primarily driven by rising consumer demand for value-based retailing, increasing adoption of membership-based shopping models, growing bulk purchasing behavior among households and businesses, and the rapid expansion of omnichannel retail platforms. Warehouse clubs have established themselves as a resilient retail format due to their ability to offer lower per-unit prices through high-volume purchasing and streamlined operations. The sector continues to benefit from inflationary pressures across food and household categories, encouraging consumers to consolidate purchases and seek cost savings. Furthermore, the expansion of private-label offerings, integrated fuel services, pharmacy programs, and digital memberships is strengthening customer loyalty and enhancing profitability. Technological advancements in inventory optimization, automated checkout systems, and last-mile delivery solutions are further transforming warehouse club operations globally. As organized retail penetration increases across emerging economies and established players continue expanding internationally, warehouse clubs are expected to gain market share from supermarkets, hypermarkets, and traditional wholesale channels throughout the forecast period.

Key Market Insights

- Membership-based retailing continues to gain popularity globally, supported by strong renewal rates, recurring revenue streams, and increasing consumer preference for value-oriented shopping.

- Private-label products are becoming a major growth engine, with warehouse clubs expanding exclusive product portfolios to improve margins and strengthen customer loyalty.

- North America dominates the global warehouse clubs market, accounting for nearly 78% of total market revenue, led by the United States.

- Asia-Pacific is the fastest-growing regional market, driven by rising middle-class populations, retail modernization, and growing acceptance of membership-based retail formats.

- Digital commerce integration is accelerating, with warehouse clubs investing heavily in mobile applications, same-day delivery, and click-and-collect capabilities.

- Artificial intelligence and automation technologies are increasingly being deployed to improve inventory management, operational efficiency, and customer engagement.

Warehouse Clubs Market Trends

Rapid Expansion of Private-Label Merchandise

Private-label products are becoming increasingly important within warehouse club business models. Consumers are demonstrating greater willingness to purchase club-exclusive brands that offer quality comparable to national brands at significantly lower prices. Leading warehouse club operators continue expanding private-label offerings across grocery, household products, health and wellness, apparel, and consumer electronics categories. This trend is improving gross margins while strengthening membership retention. Premium private-label product lines are also gaining traction among higher-income consumers who seek quality and value simultaneously. The continued investment in exclusive product development is expected to remain a key competitive differentiator across the global warehouse clubs market.

Omnichannel Retail Transformation

Warehouse clubs are rapidly evolving from purely physical retail destinations into omnichannel shopping ecosystems. Consumers increasingly expect seamless experiences across in-store, mobile, and online channels. Operators are investing heavily in same-day delivery, curbside pickup, digital memberships, mobile shopping applications, and automated fulfillment centers. Buy Online Pick Up In Store (BOPIS) services are experiencing strong adoption, particularly among urban consumers seeking convenience without sacrificing value. The integration of artificial intelligence, predictive demand forecasting, and personalized promotions is further enhancing customer engagement and improving operational efficiency across warehouse club networks worldwide.

Warehouse Clubs Market Drivers

Growing Consumer Demand for Value-Based Retailing

Persistent inflation across food, household essentials, and consumer goods categories has significantly increased demand for value-focused retail formats. Warehouse clubs provide consumers with access to lower unit pricing through bulk purchasing, making them attractive during periods of economic uncertainty. Households are increasingly consolidating purchases into fewer shopping trips while prioritizing savings on frequently consumed products. This trend has expanded warehouse club appeal beyond traditional high-volume shoppers and contributed to continued membership growth across developed and emerging markets.

Strong Membership Retention and Recurring Revenue Models

The membership-driven nature of warehouse clubs creates highly predictable revenue streams and strengthens customer loyalty. Industry-leading operators consistently report membership renewal rates exceeding 85%, providing stable cash flow and enabling aggressive pricing strategies. Membership fees also help offset operating costs, allowing warehouse clubs to maintain lower merchandise margins than traditional retailers. As consumers increasingly recognize the value proposition associated with memberships, premium and executive membership tiers are experiencing strong adoption, further enhancing profitability.

Warehouse Clubs Market Restraints

High Capital Requirements for Expansion

Warehouse club operations require substantial upfront investments in real estate, distribution infrastructure, inventory procurement, and technology systems. The large-format nature of warehouse stores necessitates significant land acquisition and construction expenditures, creating high barriers to entry. Additionally, operators must maintain robust logistics networks to support high-volume inventory turnover and ensure consistent product availability. These capital-intensive requirements limit new market entrants and can slow international expansion efforts.

Dependence on Consumer Spending Cycles

Although warehouse clubs typically perform well during inflationary periods, prolonged economic slowdowns can impact discretionary purchases and premium product sales. Membership upgrades, non-essential merchandise categories, and large-ticket purchases may experience reduced demand during periods of weak consumer confidence. Additionally, changing shopping habits and increasing competition from discount retailers and e-commerce platforms may create pricing pressures that affect long-term profitability.

Warehouse Clubs Market Opportunities

Expansion Across Emerging Economies

Emerging economies present significant opportunities for warehouse club operators due to rising urbanization, expanding middle-class populations, and increasing organized retail penetration. Markets such as India, Indonesia, Vietnam, Saudi Arabia, and the United Arab Emirates remain underpenetrated compared to North America. Growing consumer awareness of value-oriented shopping and increasing household purchasing power are creating favorable conditions for membership-based retail models. Companies that establish early market positions and adapt offerings to local consumer preferences are expected to benefit significantly from long-term growth opportunities.

Digital Membership Ecosystems and Data Monetization

The growing adoption of digital memberships presents opportunities to deepen customer engagement while generating new revenue streams. Warehouse clubs can leverage customer purchasing data to develop personalized promotions, targeted marketing campaigns, and subscription-based services. Artificial intelligence-powered recommendation engines and loyalty programs can improve customer retention and increase average transaction values. As consumers become increasingly comfortable with digital retail experiences, warehouse clubs have substantial opportunities to expand beyond traditional brick-and-mortar operations and create integrated retail ecosystems.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 470.0 Billion |

| Market Size in 2026 | USD 498.20 Billion |

| Market Size in 2031 | USD 666.70 Billion |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Membership Model Insights

Individual consumer memberships account for approximately 72% of the global warehouse clubs market and remain the dominant membership category. Strong household participation, recurring annual renewals, and widespread adoption of bulk purchasing behavior continue supporting segment leadership. Premium and executive membership tiers are experiencing particularly strong growth due to benefits such as cashback rewards, exclusive discounts, fuel savings, and enhanced service offerings. Business memberships also represent an important growth area as small businesses, restaurants, and institutional buyers increasingly leverage warehouse clubs for procurement efficiencies and cost reduction strategies.

Merchandise Category Insights

Grocery and fresh food products represent the largest merchandise category, accounting for nearly 48% of total market revenue. Frequent purchasing cycles, inflation-driven consumer behavior, and demand for bulk food purchases continue supporting category dominance. Fresh produce, meat, seafood, dairy products, frozen foods, and packaged goods drive consistent customer traffic throughout the year. Household essentials, health and wellness products, and consumer electronics represent additional high-growth categories. Private-label merchandise is gaining significant traction across all product categories as consumers increasingly prioritize value without compromising quality.

Sales Channel Insights

Physical warehouse clubs continue to dominate the market, contributing approximately 78% of total revenues in 2025. Large-format stores remain central to the warehouse club value proposition due to their ability to showcase extensive merchandise assortments and encourage bulk purchases. However, e-commerce channels are expanding rapidly as consumers increasingly seek convenience and flexible fulfillment options. Mobile commerce, online ordering, and click-and-collect services are becoming integral components of warehouse club retail strategies. Omnichannel integration is expected to play a critical role in future competitive differentiation.

Customer Type Insights

Individual households account for nearly 69% of warehouse club purchases globally, making them the largest customer segment. Rising living costs and increased focus on household budgeting continue driving demand for bulk purchasing opportunities. Small and medium-sized enterprises represent the fastest-growing customer category, utilizing warehouse clubs for cost-effective procurement of food products, office supplies, cleaning products, and operational necessities. Restaurants, hotels, healthcare facilities, educational institutions, and government organizations are also increasing warehouse club purchases to optimize procurement expenditures and improve supply chain efficiency.

Store Format Insights

Large-format warehouse clubs exceeding 120,000 square feet account for approximately 74% of total market revenue. These facilities offer the broadest product selection, highest inventory turnover, and strongest economies of scale. Their ability to support integrated services such as fuel stations, pharmacies, optical centers, and food courts enhances customer traffic and increases average spending. Mid-sized and compact urban warehouse formats are gaining traction in densely populated metropolitan markets where real estate constraints limit large-scale developments. These alternative formats are expected to support future market expansion in urban centers globally.

Explore more data points, trends and opportunities Download Free Sample Report

Warehouse Clubs Market Segmentations

By Membership Model

- Individual Consumer Membership

- Business Membership

- Hybrid Membership Programs

By Merchandise Category

- Grocery & Fresh Food

- Household Essentials

- Consumer Electronics

- Home & Furniture

- Apparel & Footwear

- Health & Wellness Products

- Automotive Products

- Office Supplies

- Seasonal Merchandise

- Jewelry & Luxury Goods

- Private Label Products

By Sales Channel

- Physical Warehouse Clubs

- E-commerce Platforms

- Omnichannel Retail

By Customer Type

- Individual Households

- Small & Medium Enterprises (SMEs)

- Restaurants & Foodservice Operators

- Hotels & Hospitality Companies

- Educational Institutions

- Government & Public Organizations

- Healthcare Facilities

- Non-Profit Organizations

By Store Format

- Large Format Warehouse Clubs

- Mid-Size Warehouse Clubs

- Urban Compact Warehouse Clubs

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 78% of global warehouse club revenues in 2025. The United States alone contributes nearly 68% of global demand, supported by mature membership adoption, strong consumer purchasing power, and extensive store networks operated by leading players. Canada maintains a well-established warehouse club ecosystem driven by high household participation rates, while Mexico continues benefiting from increasing organized retail penetration and rising middle-class consumption. Strong logistics infrastructure and high membership renewal rates support the region's continued dominance.

Europe

Europe represents approximately 7% of global market revenue, with the United Kingdom, Germany, France, Spain, and Italy serving as key markets. Economic uncertainty and inflationary pressures have increased consumer interest in value-based retail formats, supporting warehouse club expansion across the region. Business-focused membership models are particularly popular among small enterprises and independent retailers seeking procurement efficiencies. Growth opportunities remain substantial as warehouse club penetration levels remain below those observed in North America.

Asia-Pacific

Asia-Pacific accounts for nearly 10% of global warehouse club revenues and represents the fastest-growing regional market. China leads regional demand due to rapid urbanization, expanding middle-class populations, and increasing acceptance of membership-based retailing. Japan, South Korea, and Australia maintain established warehouse club operations with stable growth prospects. India is expected to emerge as one of the most attractive long-term opportunities, supported by retail modernization initiatives, rising disposable incomes, and growing consumer awareness of value-oriented shopping models.

Latin America

Latin America contributes approximately 3% of global market revenue, with Mexico, Brazil, Chile, Colombia, and Costa Rica serving as key demand centers. Rising urban populations and growing middle-class purchasing power continue supporting warehouse club adoption. International operators are increasingly exploring expansion opportunities across the region to capitalize on favorable demographic and economic trends.

Middle East & Africa

The Middle East and Africa account for approximately 2% of global warehouse club revenues. Saudi Arabia, the United Arab Emirates, South Africa, and Egypt are emerging as important markets due to retail sector modernization and increasing consumer spending. Government economic diversification initiatives and rising foreign direct investment are expected to support long-term market development across the region.

Key Players in the Warehouse Clubs Market

- Costco Wholesale Corporation

- Sam's Club

- BJ's Wholesale Club Holdings Inc.

- PriceSmart Inc.

- Makro Group

- Metro AG

- Booker Group

- Selgros Cash & Carry

- Atacadão

- Restaurant Depot

- Smart & Final

- WinCo Foods

- E-Mart Traders

- LOTTE VIC Market

- Lulu Wholesale