Outdoor Privacy Screen Market Size

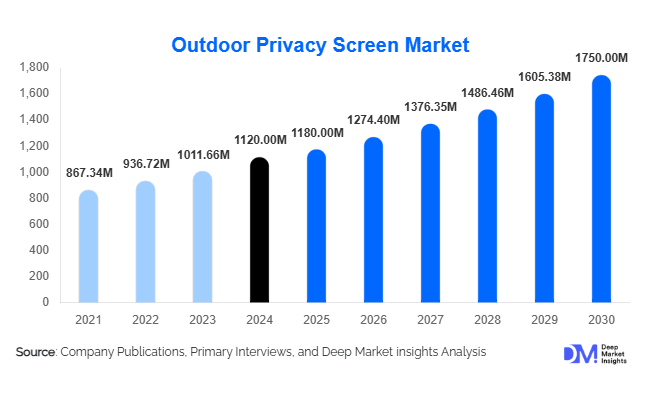

According to Deep Market Insights, the global outdoor privacy screen market size was valued at USD 1,120 million in 2024 and is projected to grow from USD 1,180 million in 2025 to reach USD 1,750 million by 2030, expanding at a CAGR of 8.0% during the forecast period (2025–2030). The market growth is primarily driven by increasing urbanization, rising demand for aesthetic and functional outdoor living solutions, and growing adoption in residential, hospitality, and public spaces worldwide.

Key Market Insights

- Residential demand dominates the market, driven by homeowners investing in balconies, terraces, and gardens to enhance privacy and outdoor aesthetics.

- Commercial adoption is increasing, particularly in hotels, resorts, and restaurants, where privacy screens improve guest comfort and outdoor design.

- Technological integration and modular designs are reshaping the market, including retractable panels, weather-resistant composites, and smart IoT-enabled solutions.

- North America holds the largest share, led by the USA, due to urbanization, high disposable income, and outdoor lifestyle trends.

- Europe is the second-largest market, with Germany and the UK leading the adoption of eco-friendly and premium outdoor screens.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising middle-class income, and increasing e-commerce penetration.

What are the latest trends in the outdoor privacy screen market?

Sustainable and Eco-Friendly Materials

Manufacturers are increasingly adopting sustainable materials such as bamboo, recycled composites, and natural wood. These eco-conscious designs cater to growing consumer preference for environmentally responsible products. Sustainability certifications, recyclable raw materials, and green manufacturing practices are becoming differentiators in the global market. Premium buyers, particularly in North America and Europe, are prioritizing screens that combine aesthetics with sustainability, driving R&D and innovation in material selection.

Modular and Smart Design Integration

Technological innovations such as retractable, modular, and IoT-enabled outdoor privacy screens are gaining traction. Smart screens that offer adjustable shading, solar integration, or automated control appeal to premium segments and commercial applications. Modular designs allow for flexible configuration in residential and commercial spaces, enhancing utility and user experience. Integration of advanced weather-resistant composites also ensures durability while offering aesthetic customization.

What are the key drivers in the outdoor privacy screen market?

Urbanization and Outdoor Living Trends

Urban expansion and limited outdoor space in high-density residential areas drive the need for privacy solutions. Consumers seek functional and visually appealing outdoor screens for balconies, patios, and rooftops. In commercial segments, hospitality and real estate developers are installing screens to enhance customer experience and comply with urban design standards. This trend is particularly strong in North America, Europe, and the Asia-Pacific.

Increasing Demand for Aesthetic and Functional Outdoor Spaces

The rise of outdoor lifestyle culture is boosting demand for privacy screens that combine aesthetics with functionality. Homeowners and commercial establishments use screens to create comfortable, private zones for recreation, dining, and leisure. Decorative panels, modular setups, and multifunctional designs contribute to higher adoption across residential and hospitality applications.

What are the restraints for the global market?

High Initial Costs

Premium materials and technologically advanced screens come at a higher price point, limiting adoption among cost-sensitive consumers. Residential buyers in emerging economies may find these products expensive, restricting market penetration. Manufacturers must balance quality with affordability to expand market reach.

Environmental Degradation and Maintenance

Outdoor screens are exposed to sun, wind, and rain, which can reduce durability over time. Maintenance requirements and material degradation can deter customers, especially in regions with extreme weather conditions, limiting long-term adoption.

What are the key opportunities in the outdoor privacy screen market?

Residential and Urban Infrastructure Growth

Rapid urbanization and increasing apartment and condominium developments present opportunities for outdoor privacy screen adoption. Developers are incorporating privacy solutions into balconies, gardens, and terraces. Government initiatives promoting affordable housing and urban development further boost market potential for manufacturers and new entrants.

Expansion in Commercial and Hospitality Segments

Hotels, resorts, cafés, and restaurants are increasingly adopting privacy screens to enhance guest comfort and outdoor aesthetics. Tourism recovery and infrastructure investments in public spaces provide sustained growth opportunities. Companies offering large-scale, durable installations can capture significant commercial demand globally.

Technological and Modular Innovation

Smart and modular designs, such as retractable or IoT-enabled screens, allow differentiation in premium segments. Integration of solar energy, automated shading, and multifunctional panels offers potential for higher margins and increased consumer engagement, particularly in high-income regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2024 | USD 1120 Million |

| Market Size in 2025 | USD 1180 Million |

| Market Size in 2030 | USD 1750 Million |

| CAGR | 8.0% (2025-2030) |

| Base Year for Estimation | 2024 |

| Historical Data | 2021-2023 |

| Forecast Period | 2025-2030 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Folding screens dominate the product segment, accounting for approximately 28% of the global market in 2024. Their portability, flexibility, and ease of installation make them ideal for both residential and commercial applications. Fixed panels and freestanding modular panels are also gaining traction due to durability and customizable designs for large outdoor spaces.

Application Insights

Residential applications lead globally with 55% market share in 2024. Homeowners are investing in privacy solutions for balconies, terraces, gardens, and rooftop areas. Commercial applications, including hotels and restaurants, follow closely, driven by aesthetics and guest comfort. Public spaces such as parks and community areas are emerging as niche but growing applications, particularly in urban planning projects across APAC and Europe.

Distribution Channel Insights

Offline retail channels dominate with a 60% market share in 2024, as consumers prefer evaluating materials and design in person. Online platforms are growing at a CAGR of 12%, offering convenience and broader reach, especially for modular and premium solutions. B2B channels cater to large-scale commercial and municipal projects.

End-Use Insights

Homeowners represent the largest end-use segment with 50% of global demand in 2024. The hospitality and commercial sector is growing faster, projected to expand at a CAGR of 9% due to tourism and public infrastructure projects. Emerging end-use segments include rooftop gardens, co-living communities, and office outdoor spaces, creating new market opportunities and boosting export demand from manufacturing hubs in China and India.

Explore more data points, trends and opportunities Download Free Sample Report

Outdoor Privacy Screen Market Segmentations

By Material Type

- Wood

- Metal (Aluminum, Steel, Iron)

- Fabric/Textile (Polyester, Canvas)

- Synthetic/Composite (PVC, Polycarbonate, Fiberglass)

- Bamboo/Wicker

By Product Type

- Folding Screens

- Fixed Panels

- Retractable Screens

- Freestanding Panels

- Modular Panels

By Application

- Residential (Balcony, Garden, Patio, Terrace)

- Commercial (Hotels, Resorts, Restaurants, Cafés)

- Public Spaces (Parks, Community Areas)

By End-Use Industry

- Homeowners / Residential Property Developers

- Hospitality & Tourism

- Real Estate & Construction

- Government & Public Infrastructure

By Distribution Channel

- Offline Retail (Home Improvement & Specialty Stores)

- Online Retail (E-Commerce & Brand Websites)

- B2B Channels (Contractors, Bulk Suppliers)

Regional Insights

North America

North America holds the largest regional share at 32% in 2024, led by the USA and Canada. High disposable income, urban living trends, and outdoor lifestyle preferences drive market adoption. The USA alone accounts for 28% of global demand, with strong growth in modular and retractable screens for residential and commercial applications.

Europe

Europe holds a 28% market share in 2024, led by Germany and the UK. Demand is driven by eco-friendly materials, premium designs, and urban outdoor aesthetics. Sustainability-conscious consumers in Germany, France, and Italy prefer wood and composite screens for residential and hospitality applications.

Asia-Pacific

APAC is the fastest-growing region with a 10% CAGR, driven by China, India, Japan, and Australia. Rising middle-class income, urbanization, and e-commerce penetration are accelerating market adoption. China represents 12% of global demand, fueled by residential development and commercial infrastructure growth.

Latin America

Brazil, Mexico, and Argentina are driving moderate growth, with increasing adoption of residential and hospitality privacy solutions. Brazil accounts for 5% of global demand, and niche customized installations are gaining traction.

Middle East & Africa

MEA growth is steady, led by the UAE, Saudi Arabia, and South Africa. Luxury residential projects and hospitality investments drive demand for high-quality outdoor screens. Africa’s iconic landscapes and urban development projects also support the commercial adoption of privacy screens.

Key Players in the Outdoor Privacy Screen Market

- ScreenFlex

- Decowood Industries

- Viking Screen Solutions

- Tanex Outdoor Systems

- GreenScape Screens

- EcoWood Panels

- SunScreen Innovations

- PatioGuard

- Horizon Outdoor Solutions

- Timberline Screens

- ShadeMaster

- OutdoorLux

- GardenView Screens

- ModuScreen

- AluPrivacy

Recent Developments

- In March 2025, ScreenFlex launched modular outdoor screens with solar-powered retractable panels for premium residential applications in North America.

- In February 2025, Decowood Industries introduced eco-friendly bamboo composite screens for commercial landscaping projects across Europe.

- In January 2025, Viking Screen Solutions expanded its APAC manufacturing facility to cater to rising demand from China and India for residential and hospitality applications.