Unisex Clothing Market Size

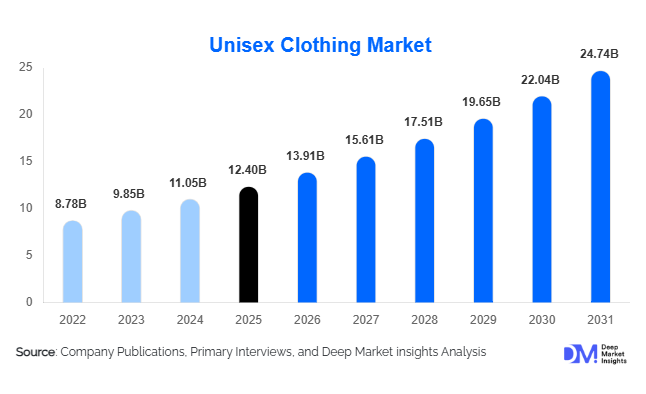

According to Deep Market Insights, the global unisex clothing market size was valued at USD 12.4 billion in 2025 and is projected to grow from USD 13.91 billion in 2026 to reach USD 24.74 billion by 2031, expanding at a CAGR of 12.2% during the forecast period (2026–2031). The growth of the unisex clothing market is primarily driven by changing consumer attitudes toward gender-neutral fashion, increasing acceptance of inclusive apparel, rapid expansion of e-commerce channels, and the growing influence of streetwear and athleisure trends across global fashion markets. The convergence of comfort, functionality, and sustainability has transformed unisex apparel from a niche segment into a mainstream category adopted by both premium and mass-market fashion brands.

Key Market Insights

- Gender-neutral fashion is becoming a mainstream apparel category, driven by growing consumer preference for inclusivity, self-expression, and non-binary fashion identities.

- Streetwear and oversized silhouettes continue to dominate global demand, particularly among Gen Z and Millennial consumers.

- Asia-Pacific dominates the global market, supported by strong manufacturing capabilities, expanding middle-class populations, and rising fashion expenditure.

- India is emerging as one of the fastest-growing country markets, driven by digital commerce growth and increasing acceptance of contemporary fashion trends.

- Sustainable and recycled fabrics are gaining significant traction, with brands increasingly integrating circular fashion principles into product development.

- E-commerce platforms and direct-to-consumer channels are reshaping purchasing behavior through personalized shopping experiences and broader product accessibility.

Unisex Clothing Market Trends

Rise of Inclusive and Gender-Neutral Fashion

One of the most significant trends reshaping the global apparel industry is the increasing adoption of gender-neutral fashion. Consumers are moving away from traditional gender-specific clothing categories and embracing products that prioritize comfort, versatility, and individual expression. Leading apparel brands are introducing dedicated unisex collections that feature neutral color palettes, relaxed fits, and inclusive sizing structures. Retailers are also redesigning store layouts and online merchandising strategies to remove gender barriers and simplify purchasing decisions. This trend is particularly evident among younger consumers, who increasingly view fashion as a medium of self-expression rather than adherence to conventional gender norms.

Sustainability and Circular Fashion Integration

Sustainability is becoming a defining characteristic of the unisex clothing market. Manufacturers are investing in organic cotton, recycled polyester, hemp fibers, and low-impact production processes to meet growing consumer demand for environmentally responsible products. The unisex apparel model naturally supports circular fashion objectives by reducing SKU complexity and extending product lifecycles across broader consumer groups. Many brands are launching resale programs, garment recycling initiatives, and carbon-neutral collections to strengthen their sustainability credentials. As environmental regulations tighten globally, sustainable manufacturing practices are expected to become a key competitive differentiator.

Unisex Clothing Market Drivers

Growing Acceptance of Gender Fluidity and Inclusive Fashion

The increasing social acceptance of gender diversity and non-binary identities is creating substantial demand for unisex apparel. Consumers are seeking clothing that transcends traditional gender categories and offers greater flexibility in styling and personal expression. Fashion brands are responding by expanding inclusive collections and investing in marketing campaigns that emphasize diversity and representation. This cultural transformation is significantly expanding the addressable consumer base for unisex clothing worldwide.

Expansion of E-Commerce and Direct-to-Consumer Retail

The rapid growth of digital commerce has accelerated market expansion by enabling brands to reach consumers directly and efficiently. Online platforms provide access to broader product assortments, personalized recommendations, virtual fitting technologies, and transparent pricing. Digital-native apparel companies have been particularly successful in promoting gender-neutral fashion through social media marketing and influencer partnerships. The scalability of e-commerce continues to reduce barriers for emerging brands entering the market.

Unisex Clothing Market Restraints

Challenges Associated with Standardized Sizing

Developing universal sizing systems remains one of the most significant challenges for the industry. Differences in body proportions across genders and regions make it difficult for manufacturers to establish standardized fits that satisfy a diverse consumer base. Inconsistent sizing can increase return rates, inventory management complexities, and customer dissatisfaction, creating operational challenges for brands seeking to scale globally.

Cultural and Regional Adoption Barriers

While acceptance of gender-neutral fashion is increasing worldwide, certain markets continue to exhibit strong preferences for traditional gender-specific apparel. Cultural norms, religious influences, and established purchasing habits can slow adoption rates in some regions. Companies operating globally must therefore tailor their marketing strategies and product offerings to align with local consumer expectations while gradually introducing inclusive fashion concepts.

Unisex Clothing Market Opportunities

Expansion into Emerging Asia-Pacific Markets

Asia-Pacific represents one of the largest growth opportunities for the unisex clothing market. Rising disposable incomes, rapid urbanization, expanding digital commerce penetration, and growing exposure to global fashion trends are supporting demand across China, India, Indonesia, Vietnam, and South Korea. Local brands and international fashion companies are increasingly investing in the region to capitalize on evolving consumer preferences and strong demographic growth.

Sustainable Apparel and Circular Fashion Business Models

The growing consumer preference for sustainable fashion presents substantial opportunities for both established players and new entrants. Companies that invest in recycled materials, biodegradable fabrics, ethical sourcing practices, and resale ecosystems can differentiate themselves in an increasingly competitive market. Regulatory support for sustainable textile manufacturing in Europe and North America is further accelerating investment in circular apparel business models.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.4 Billion |

| Market Size in 2026 | USD 13.91 Billion |

| Market Size in 2031 | USD 24.74 Billion |

| CAGR | 12.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Tops represent the largest product segment within the unisex clothing market, accounting for approximately 34% of global revenue in 2025. T-shirts, hoodies, sweatshirts, and polos remain the most widely adopted categories due to their versatility, comfort, and broad consumer appeal. Streetwear culture has further strengthened demand for oversized tops that naturally align with gender-neutral fashion trends. Bottoms, including joggers, jeans, and relaxed-fit trousers, represent the second-largest segment, supported by growing demand for casual and athleisure-inspired apparel. Outerwear categories such as jackets and windbreakers are also experiencing strong growth as brands introduce seasonally adaptable unisex collections.

Material Type Insights

Cotton remains the dominant material segment, representing approximately 38% of global market revenue. Consumers continue to favor cotton due to its comfort, breathability, affordability, and sustainability profile. Blended fabrics and polyester-based materials maintain strong market positions due to durability and performance benefits, particularly within activewear categories. Recycled fibers and organic cotton are among the fastest-growing material segments as brands increasingly prioritize sustainable sourcing and environmentally responsible production methods.

Distribution Channel Insights

Online retail channels account for approximately 44% of global unisex clothing sales and continue to lead market growth. Brand-owned websites, direct-to-consumer platforms, and third-party e-commerce marketplaces provide consumers with extensive product variety and personalized shopping experiences. Specialty fashion retailers remain important distribution partners, particularly for premium and niche brands. Department stores and hypermarkets continue to serve mainstream consumer segments, while factory outlets support value-oriented purchasing behavior. Social commerce and influencer-driven sales channels are increasingly influencing consumer purchasing decisions, particularly among younger demographics.

Consumer Age Group Insights

Young adults aged 20–34 years represent the largest consumer segment, accounting for approximately 41% of global market demand. This demographic exhibits strong preferences for fashion innovation, digital shopping experiences, and inclusive brand values. Teenagers and younger consumers continue to drive emerging fashion trends through social media engagement and influencer-led purchasing behavior. Adults aged 35–54 years represent a significant contributor to market revenues due to higher disposable incomes and increasing adoption of comfort-focused apparel. The senior population remains a smaller but steadily expanding consumer segment, particularly for casual and functional clothing categories.

End-Use Insights

Individual consumers account for approximately 82% of total market demand and remain the primary end-use segment. Growing interest in personal style expression, comfort-driven fashion, and inclusive apparel continues to support consumer purchases globally. Corporate and institutional demand is also increasing as businesses adopt gender-neutral workplace uniforms and inclusive dress code policies. Educational institutions, hospitality operators, and sports organizations are emerging as important commercial buyers of unisex apparel, contributing to broader market diversification and long-term demand stability.

Explore more data points, trends and opportunities Download Free Sample Report

Unisex Clothing Market Segmentations

By Product Type

- Tops

- Bottoms

- Outerwear

- Activewear & Sportswear

- Loungewear & Sleepwear

- Ethnic & Cultural Wear

- Formal & Workwear

- Intimate & Base Layer Apparel

By Material Type

- Cotton

- Polyester

- Blended Fabrics

- Organic Cotton

- Recycled Fibers

- Wool

- Linen

- Hemp

- Nylon

- Others

By Distribution Channel

- Brand-Owned Online Stores

- Third-Party E-Commerce Platforms

- Specialty Fashion Stores

- Department Stores

- Hypermarkets & Supermarkets

- Factory Outlets

- Direct-to-Consumer (DTC) Stores

By Consumer Age Group

- Children (0–12 Years)

- Teenagers (13–19 Years)

- Young Adults (20–34 Years)

- Adults (35–54 Years)

- Seniors (55+ Years)

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 38% of global market revenue and represents the largest regional market. China leads regional demand due to its large consumer base, sophisticated manufacturing ecosystem, and growing fashion expenditure. India is among the fastest-growing markets globally, supported by rising disposable incomes, expanding urban populations, and increasing digital retail penetration. Japan and South Korea continue to influence global fashion trends through streetwear, minimalist design aesthetics, and youth-oriented fashion culture. Southeast Asian countries are also emerging as important growth centers due to improving economic conditions and rising apparel consumption.

North America

North America represents approximately 29% of global demand, with the United States accounting for nearly 24% of worldwide market revenues. The region benefits from high consumer awareness of inclusive fashion, advanced e-commerce infrastructure, and strong purchasing power. Growing demand for sustainable apparel and diversity-focused brand messaging continues to support market growth. Canada also contributes significantly through premium apparel consumption and increasing adoption of gender-neutral fashion collections.

Europe

Europe accounts for approximately 25% of global market revenue. Germany, the United Kingdom, France, Italy, and the Netherlands are among the leading markets within the region. Strong sustainability regulations, consumer awareness regarding ethical fashion, and widespread support for diversity initiatives continue to drive demand. European consumers demonstrate strong interest in premium-quality products manufactured using environmentally responsible materials and production methods.

Latin America

Latin America represents approximately 5% of global market demand, led by Brazil and Mexico. Rising urbanization, increasing social media influence, and growing adoption of international fashion trends are supporting regional market expansion. Although economic volatility remains a challenge, demand for affordable and mid-range unisex apparel continues to increase.

Middle East & Africa

The Middle East and Africa account for approximately 3% of global revenue. The United Arab Emirates and Saudi Arabia are driving regional growth through premium fashion consumption and increasing adoption of global fashion trends. South Africa remains the largest market within Africa, supported by a developed retail sector and growing interest in contemporary apparel. Younger consumer demographics are increasingly embracing gender-neutral fashion concepts, creating future growth opportunities across the region.

Key Players in the Unisex Clothing Market

- Inditex

- H&M Group

- Uniqlo

- Nike Inc.

- Adidas AG

- Gap Inc.

- Levi Strauss & Co.

- PVH Corp.

- American Eagle Outfitters

- ASOS plc

- Mango

- Lululemon Athletica

- Telfar

- TomboyX

- The Phluid Project