Truck Rental Market Size

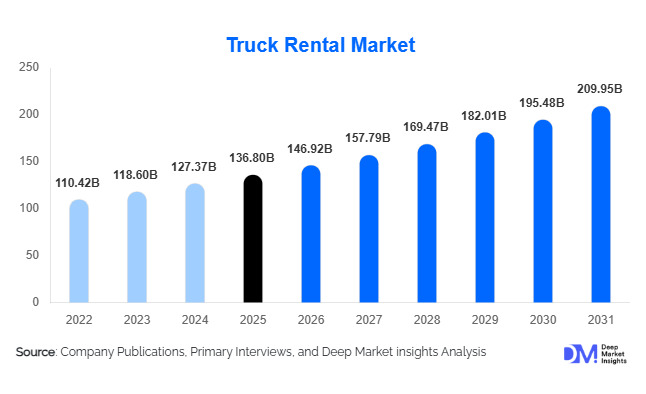

According to Deep Market Insights, the global truck rental market size was valued at USD 136.8 billion in 2025 and is projected to grow from USD 146.92 billion in 2026 to reach USD 210.5 billion by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The truck rental market growth is primarily driven by the increasing adoption of asset-light fleet management strategies, rapid expansion of e-commerce logistics networks, growing infrastructure and construction activities, and rising demand for flexible transportation solutions across industries. Businesses are increasingly shifting from truck ownership to rental and leasing models to reduce capital expenditures, improve fleet utilization, and gain access to modern vehicles equipped with advanced telematics and fleet management technologies.

Key Market Insights

- Short-term truck rentals continue to dominate fleet demand, supported by seasonal freight requirements, e-commerce peaks, and project-based transportation needs.

- Light-duty trucks account for the largest market share globally, driven by urban logistics, parcel delivery, and last-mile transportation applications.

- Asia-Pacific dominates the global truck rental market, led by China, India, Japan, and Southeast Asia's expanding logistics and manufacturing sectors.

- India is emerging as the fastest-growing national market, supported by infrastructure investments, industrial expansion, and increasing logistics outsourcing.

- Electric truck rental fleets are gaining traction, particularly across Europe, China, and North America as fleet operators pursue decarbonization goals.

- Digital fleet management, telematics, and AI-driven route optimization are transforming truck rental operations and improving vehicle utilization rates.

Truck Rental Market Trends

Electrification of Commercial Rental Fleets

Fleet electrification is becoming one of the most significant trends shaping the truck rental industry. Rental providers are increasingly adding battery-electric and hybrid trucks to their fleets as governments introduce stricter emission regulations and sustainability mandates. Large logistics operators are utilizing rental agreements to pilot electric truck deployments without significant upfront capital investment. The trend is particularly prominent across Europe, China, California, and select metropolitan regions where charging infrastructure continues to expand. Rental companies are also partnering with OEMs to accelerate commercial deployment of electric vehicles while reducing fleet transition risks for customers. As battery technology improves and charging networks mature, electric truck rental demand is expected to expand substantially throughout the forecast period.

Digitalization and Fleet-as-a-Service Models

Truck rental providers are increasingly transitioning toward digitally enabled fleet services. Customers now expect online booking capabilities, real-time vehicle tracking, predictive maintenance support, digital contract management, and integrated transportation analytics. Fleet-as-a-Service (FaaS) models are becoming popular among enterprises seeking flexible fleet scaling and operational transparency. AI-powered route optimization, telematics-driven performance monitoring, and predictive maintenance systems are reducing downtime while enhancing customer experience. Subscription-based truck rental models are also emerging as an alternative to traditional leasing structures, particularly among SMEs and regional logistics operators seeking greater operational flexibility.

Truck Rental Market Drivers

Rapid Expansion of E-Commerce Logistics

The global growth of e-commerce has fundamentally transformed freight transportation requirements. Online retailers require scalable transportation capacity to manage fluctuating demand patterns, seasonal sales events, and same-day delivery commitments. Truck rental services provide businesses with flexible fleet capacity without the burden of vehicle ownership. The expansion of fulfillment centers, regional warehouses, and last-mile delivery networks continues to drive substantial demand for rental trucks, particularly in urban and suburban markets.

Shift Toward Asset-Light Transportation Models

Organizations across logistics, retail, manufacturing, and construction industries are increasingly adopting asset-light operating strategies. Rather than investing capital in vehicle ownership, businesses are leveraging rental fleets to improve cash flow, reduce maintenance liabilities, and enhance operational agility. Truck rental providers offer customers access to modern fleets, maintenance services, insurance coverage, and fleet management support, making rental solutions economically attractive compared with outright vehicle ownership.

Truck Rental Market Restraints

Rising Vehicle Acquisition and Financing Costs

Commercial vehicle prices have increased significantly due to inflationary pressures, supply chain disruptions, advanced technology integration, and stricter emissions compliance requirements. These factors increase fleet replacement costs for rental companies and can impact profitability. Elevated financing costs and higher interest rates further constrain fleet expansion initiatives, particularly for smaller rental providers operating in highly competitive markets.

Infrastructure Limitations for Alternative Fuel Trucks

Although electric and alternative fuel trucks represent major growth opportunities, infrastructure limitations continue to hinder widespread adoption. Charging station availability remains insufficient across many freight corridors, while hydrogen refueling infrastructure is still in the early stages of deployment. These limitations reduce operational flexibility and may slow the pace of fleet electrification, particularly for long-haul transportation applications.

Truck Rental Market Opportunities

Growth of Electric Truck Rental Services

The transition toward low-emission transportation creates significant opportunities for truck rental providers. Many businesses prefer renting electric trucks before committing to large-scale fleet purchases. Rental providers can capture demand from companies seeking compliance with environmental regulations, ESG commitments, and carbon reduction targets. Government incentives and expanding charging infrastructure further strengthen the business case for electric truck rental services globally.

Infrastructure and Construction Boom in Emerging Markets

Large-scale infrastructure development across India, Southeast Asia, the Middle East, and Africa is generating substantial transportation requirements. Construction projects, industrial corridors, mining developments, and logistics hubs often require temporary truck fleets for limited project durations. Rental providers can capitalize on this demand by offering specialized vehicle categories and project-based fleet solutions tailored to infrastructure contractors and industrial operators.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 136.8 Billion |

| Market Size in 2026 | USD 146.92 Billion |

| Market Size in 2031 | USD 209.95 Billion |

| CAGR | 7.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Truck Type Insights

Light-duty trucks represent the largest segment of the truck rental market, accounting for approximately 68.5% of global revenue in 2025. Their dominance is attributed to strong demand from e-commerce delivery services, urban logistics providers, and retail distribution networks. Medium-duty trucks maintain a significant presence in regional freight transportation and industrial logistics operations, while heavy-duty trucks support long-haul transportation, mining, energy, and large-scale construction activities. The increasing adoption of urban delivery networks and same-day fulfillment models continues to reinforce the leadership of light-duty rental trucks globally.

Rental Duration Insights

Short-term rentals account for approximately 54% of global market revenue and remain the preferred rental model among logistics providers, retailers, and construction companies. Businesses increasingly utilize short-term contracts to address seasonal demand fluctuations, temporary projects, and fleet replacement requirements. Medium-term rentals are gaining popularity among SMEs seeking operational flexibility, while long-term rentals continue to attract large enterprises looking for predictable transportation costs and comprehensive fleet management support.

Propulsion Type Insights

Internal combustion engine trucks account for approximately 92% of the market, reflecting the extensive availability of fueling infrastructure and established maintenance ecosystems. Diesel-powered fleets continue to dominate long-haul freight transportation globally. However, battery-electric trucks represent the fastest-growing propulsion segment as fleet operators pursue sustainability objectives and governments introduce stricter emissions regulations. Hybrid and alternative fuel trucks are gradually gaining market acceptance in specific regional markets and urban delivery applications.

Application Insights

Freight transportation remains the largest application segment, accounting for nearly 38% of global truck rental demand. The segment benefits from rising domestic freight volumes, international trade activity, and expanding supply chain networks. Last-mile delivery applications are experiencing the fastest growth due to e-commerce expansion and urbanization trends. Construction logistics, manufacturing transportation, mining operations, and retail distribution continue to generate substantial rental demand, particularly in emerging economies undergoing industrialization and infrastructure development.

Customer Type Insights

Small and medium-sized enterprises account for approximately 44% of global truck rental revenue, making them the largest customer category. SMEs frequently prefer rental solutions because they provide access to transportation assets without substantial capital investments. Large enterprises continue to utilize long-term rental agreements for fleet optimization, while government organizations and public sector agencies increasingly rely on rental fleets for infrastructure projects, disaster response operations, and municipal services. Independent contractors and owner-operators also represent an important customer segment, particularly within regional freight transportation markets.

End-Use Industry Insights

Transportation and logistics represent the largest end-use industry, contributing approximately 35% of global truck rental demand. The rapid growth of e-commerce, third-party logistics providers, and cross-border trade continues to support segment expansion. Construction remains one of the fastest-growing end-use sectors, driven by public infrastructure investments and industrial development projects worldwide. Manufacturing, retail, agriculture, mining, and energy industries also contribute significantly to truck rental demand, reflecting the essential role of transportation services across industrial value chains.

Explore more data points, trends and opportunities Download Free Sample Report

Truck Rental Market Segmentations

By Truck Type

- Light-Duty Trucks

- Medium-Duty Trucks

- Heavy-Duty Trucks

By Rental Duration

- Short-Term Rental

- Medium-Term Rental

- Long-Term Rental

By Propulsion Type

- Internal Combustion Engine Trucks

- Battery Electric Trucks

- Hybrid Trucks

- Alternative Fuel Trucks (CNG, LNG & Hydrogen)

By Application

- Freight Transportation

- Last-Mile Delivery

- Construction & Infrastructure Logistics

- Industrial & Manufacturing Logistics

- Retail Distribution

- Agriculture & Food Supply Chain Logistics

- Mining & Energy Logistics

- Event & Temporary Project Logistics

- Household Relocation & Moving Services

By Customer Type

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- Owner Operators & Independent Contractors

- Government & Public Sector Organizations

- Individual Consumers

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 41.5% of global truck rental market revenue in 2025, making it the largest regional market. China leads demand due to its extensive manufacturing base, freight transportation activity, and rapidly growing e-commerce sector. India represents the fastest-growing country globally, supported by infrastructure development, logistics modernization initiatives, and increasing industrial output. Japan, South Korea, and Australia contribute substantial demand through mature logistics industries and advanced fleet management practices. Southeast Asian countries including Indonesia, Vietnam, and Thailand are also emerging as attractive growth markets due to industrial expansion and rising freight volumes.

North America

North America accounted for approximately 26% of global market revenue in 2025. The United States remains the region's dominant market, representing nearly 22% of global demand. High trucking penetration, sophisticated logistics networks, and widespread adoption of fleet leasing models support market growth. Canada contributes through mining, energy, and cross-border transportation activities. Electrification initiatives and advanced telematics adoption continue to drive innovation across the regional market.

Europe

Europe represents approximately 22% of global truck rental revenue. Germany leads demand due to its manufacturing exports and logistics infrastructure, followed by the United Kingdom, France, Italy, Spain, and the Netherlands. Fleet electrification policies, sustainability regulations, and strong cross-border transportation activity continue to support regional growth. Europe is also one of the leading regions for electric commercial vehicle adoption.

Latin America

Latin America accounts for approximately 4.5% of the global market, led by Brazil and Mexico. Brazil's agriculture, mining, and domestic freight transportation sectors generate substantial rental demand. Mexico benefits from nearshoring investments and manufacturing integration with North American supply chains. Improving logistics infrastructure across the region is expected to create additional growth opportunities.

Middle East & Africa

The Middle East and Africa account for approximately 6% of global market revenue. Saudi Arabia and the UAE are driving growth through large-scale infrastructure projects, logistics corridor development, and industrial diversification initiatives. South Africa remains the region's largest transportation market, while increasing mining investments across Africa continue to support demand for heavy-duty rental vehicles.

Key Players in the Truck Rental Market

- Penske Truck Leasing

- Ryder System

- Enterprise Truck Rental

- Daimler Truck Financial Services

- PACCAR Leasing

- Volvo Financial Services

- TRATON Financial Services

- NationaLease

- Idealease

- TIP Group

- Fraikin Group

- Petit Forestier

- Hino Leasing

- United Rentals

- Avis Budget Group