Tennis Balls Market Size

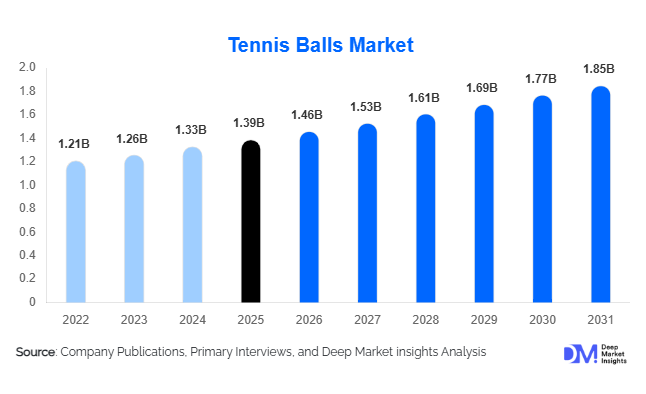

According to Deep Market Insights, the global tennis balls market size was valued at USD 1.39 billion in 2025 and is projected to grow from USD 1.46 billion in 2026 to reach USD 1.85 billion by 2031, expanding at a CAGR of 4.9% during the forecast period (2026–2031). The tennis balls market growth is primarily driven by increasing global participation in tennis, rising investments in sports infrastructure, expanding tennis academy networks, and the recurring replacement nature of tennis balls across professional, recreational, and training applications. Unlike other sporting equipment categories, tennis balls generate continuous demand due to pressure loss, wear and tear, and tournament regulations requiring frequent replacement. Growing adoption of tennis among youth populations, increasing government-backed sports development programs, and the emergence of organized coaching ecosystems are creating a stable long-term demand outlook. Furthermore, sustainability initiatives, premium product innovations, and the rapid expansion of e-commerce channels are reshaping the competitive landscape and creating new growth opportunities for manufacturers worldwide.

Key Market Insights

- Pressurized tennis balls account for nearly 74% of global demand, supported by their widespread adoption in professional tournaments and club-level competitions.

- Tennis academies and coaching centers represent one of the fastest-growing end-use segments, driven by increasing youth participation and professional training programs.

- North America dominates the global market, accounting for approximately 36% of total revenue in 2025, led by strong participation rates in the United States.

- Asia-Pacific is the fastest-growing regional market, supported by expanding tennis infrastructure in China, India, Japan, and Southeast Asia.

- Sustainable tennis ball development is emerging as a major industry focus, with manufacturers investing in recyclable packaging, eco-friendly felt materials, and lower-carbon production methods.

- Online retail channels are rapidly gaining market share, enabling direct-to-consumer sales and subscription-based replenishment models.

Tennis Balls Market Trends

Sustainability and Circular Economy Initiatives Accelerating

The tennis balls industry is increasingly embracing sustainability as environmental concerns surrounding ball disposal continue to gain attention. Millions of tennis balls are discarded annually worldwide, creating significant waste management challenges. Manufacturers are responding through the development of recyclable packaging materials, environmentally friendly felt compositions, and collection programs designed to repurpose used tennis balls for playground surfaces, athletic facilities, and construction materials. Major tennis tournaments and clubs are also implementing recycling partnerships to reduce landfill contributions. Sustainability initiatives are increasingly becoming an important purchasing criterion for institutions and tournament organizers, encouraging manufacturers to invest in greener production technologies and lower-emission manufacturing processes.

Premiumization of Tennis Ball Offerings

Consumer preferences are increasingly shifting toward premium tennis balls that offer superior durability, pressure retention, and consistent bounce performance. Professional players, academies, and serious recreational users are willing to pay higher prices for products that maintain performance over longer playing periods. Manufacturers are investing in advanced felt technologies, enhanced rubber core formulations, and improved pressure retention systems to differentiate their products. Premium product segments are experiencing stronger growth than standard offerings, particularly in North America, Europe, Japan, and Australia. Tournament partnerships and professional endorsements continue to reinforce the perception of premium brands, enabling manufacturers to improve margins while strengthening customer loyalty.

Tennis Balls Market Drivers

Growing Global Participation in Tennis

Tennis participation has expanded significantly across both developed and emerging economies. Increased awareness of health and fitness, combined with the popularity of international tournaments such as Wimbledon, the US Open, the Australian Open, and Roland Garros, has encouraged participation among players of all age groups. Grassroots development programs, school-based tennis initiatives, and government-supported sports participation campaigns continue to increase the global player base. As tennis balls require regular replacement, growth in participation directly translates into recurring demand, making player expansion one of the most important growth drivers for the market.

Expansion of Tennis Academies and Professional Training Infrastructure

The rapid growth of tennis academies and coaching facilities worldwide is generating substantial demand for training and practice balls. Professional training centers consume large volumes of tennis balls due to intensive daily usage, creating stable institutional purchasing patterns. Countries such as China, India, Spain, France, and the United States have witnessed increased investment in player development infrastructure. The growing number of junior development programs and elite coaching centers is expected to sustain long-term demand growth across both premium and training ball categories.

Tennis Balls Market Restraints

Raw Material Price Volatility

The production of tennis balls relies heavily on natural rubber, synthetic rubber compounds, wool felt, and packaging materials. Fluctuations in raw material prices can significantly impact manufacturing costs and profit margins. Manufacturers often face challenges in passing increased costs directly to consumers, particularly in highly competitive markets. Volatility in energy prices and transportation costs further contributes to pricing pressures throughout the value chain.

Competition from Alternative Racquet Sports

The growing popularity of sports such as pickleball, padel, badminton, and squash presents a competitive challenge to tennis participation growth. In particular, pickleball has experienced rapid adoption in North America, while padel is expanding quickly across Europe, Latin America, and the Middle East. These sports often require lower infrastructure investment and shorter learning curves, potentially diverting participation and consumer spending away from traditional tennis activities.

Tennis Balls Market Opportunities

Expansion into Emerging Tennis Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East present significant opportunities for tennis ball manufacturers. Countries including India, China, Saudi Arabia, UAE, Brazil, and Mexico are investing heavily in sports infrastructure and youth development programs. Rising disposable incomes and increasing exposure to international sporting events are encouraging greater participation in tennis. Manufacturers that establish localized production facilities, distribution partnerships, and region-specific product portfolios are expected to benefit from substantial long-term demand growth.

Sustainable Tennis Ball Innovation

Environmental sustainability presents a major opportunity for product differentiation and premium positioning. Manufacturers investing in recyclable materials, biodegradable components, and carbon-efficient production technologies can address growing environmental concerns among consumers and institutions. Sustainable products are increasingly favored by tennis clubs, educational institutions, and tournament organizers seeking to meet environmental objectives. As sustainability becomes a key purchasing criterion, companies capable of delivering performance and environmental benefits simultaneously are likely to gain competitive advantages.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.39 Billion |

| Market Size in 2026 | USD 1.46 Billion |

| Market Size in 2031 | USD 1.85 Billion |

| CAGR | 4.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Ball Construction Type Insights

Pressurized tennis balls dominate the market, accounting for approximately 74% of global revenue in 2025. Their leadership position is supported by widespread usage across professional tournaments, club competitions, and advanced recreational play. These balls provide superior bounce consistency and playing characteristics, making them the preferred choice for competitive applications. Pressureless tennis balls maintain a significant niche within training environments, ball machine operations, and institutional coaching programs due to their extended lifespan and lower replacement frequency. Growing demand from tennis academies and practice facilities continues to support expansion of the pressureless segment, particularly in developing markets where cost efficiency remains an important purchasing factor.

Court Surface Compatibility Insights

Hard court tennis balls represent the largest segment, accounting for approximately 52% of global market demand. Their dominance reflects the extensive global installation base of hard court facilities, particularly across North America and Asia-Pacific. Hard court balls feature enhanced felt durability to withstand abrasive surfaces and maintain performance over extended playing sessions. Clay court balls continue to hold strong demand in European markets, particularly in France, Spain, and Italy, while grass court balls remain a specialized segment primarily linked to professional tournaments and select club facilities. Multi-surface balls are increasingly gaining popularity among recreational consumers seeking versatility across different playing environments.

Application Insights

Tennis training and coaching applications account for approximately 39% of global market revenue, making them the largest application segment. Tennis academies, coaching institutions, and player development programs require high-volume purchases throughout the year, creating predictable recurring demand. Professional competition remains an important premium segment driven by tournament regulations and sponsorship agreements. Recreational play contributes substantial volume consumption due to the large global base of amateur players, while tennis ball machine applications are experiencing steady growth as automated training technologies become more widely adopted across clubs and academies.

Distribution Channel Insights

Sporting goods retail stores account for approximately 34% of global sales and remain the leading distribution channel. These stores provide consumers with access to a broad range of brands, product specifications, and price points. Specialty tennis retailers continue to serve advanced players and institutional buyers seeking expert product guidance. Online retail channels are rapidly gaining market share as consumers increasingly value convenience, product reviews, and competitive pricing. Direct-to-club and academy sales represent a strategically important channel for manufacturers, enabling long-term supply agreements and recurring institutional revenue streams.

End-User Insights

Recreational consumers account for approximately 38% of global demand and remain the largest end-user segment. Growth is supported by increasing participation among adults seeking fitness-oriented recreational activities. Tennis clubs and academies collectively represent a significant share of market consumption due to frequent ball replacement requirements. Educational institutions are emerging as an attractive growth segment as schools and universities increasingly incorporate tennis into sports development programs. Sports infrastructure operators and professional organizations continue to generate demand for premium-grade products designed to meet competition standards.

Explore more data points, trends and opportunities Download Free Sample Report

Tennis Balls Market Segmentations

By Ball Construction Type

- Pressurized Tennis Balls

- Pressureless Tennis Balls

By Court Surface Compatibility

- Hard Court Balls (Extra Duty Felt)

- Clay Court Balls (Regular Duty Felt)

- Grass Court Balls

- Multi-Surface Tennis Balls

By Player Category

- Professional Competition Balls

- Advanced Amateur Balls

- Recreational Adult Balls

- Junior Development Balls

By Stage Ball Type

- Stage 3 Red Balls

- Stage 2 Orange Balls

- Stage 1 Green Balls

- Standard Yellow Balls

By Application

- Professional Competition

- Tennis Training & Coaching

- Recreational Play

- Tennis Ball Machines

- School & Institutional Programs

Regional Insights

North America

North America accounted for approximately 36% of global tennis ball revenue in 2025, making it the largest regional market. The United States alone contributes nearly 31% of global demand, supported by high participation rates, extensive tennis infrastructure, strong club networks, and the presence of major tournaments such as the US Open. Canada continues to experience steady growth driven by increasing recreational participation and investments in community sports facilities. Premium tennis ball products enjoy strong adoption across the region, supported by consumer willingness to invest in performance-enhancing sporting equipment.

Europe

Europe represents approximately 29% of global market revenue, supported by well-established tennis traditions and extensive club-based participation. France, Germany, Spain, Italy, and the United Kingdom are among the largest consumers within the region. France benefits from strong tennis culture associated with Roland Garros, while Spain's internationally recognized academy ecosystem generates significant training ball demand. European consumers increasingly favor sustainable products, encouraging manufacturers to introduce environmentally responsible product lines.

Asia-Pacific

Asia-Pacific accounted for approximately 24% of global market revenue in 2025 and represents the fastest-growing regional market, with forecast growth exceeding 6.5% annually. China remains the largest market within the region, driven by expanding urban sports infrastructure and rising participation rates. India is emerging as one of the fastest-growing countries globally, supported by increasing middle-class incomes, government sports initiatives, and rapid expansion of tennis academies. Japan and Australia continue to provide stable demand through mature tennis ecosystems and strong consumer spending on premium sporting goods.

Latin America

Latin America accounted for approximately 7% of global demand, led by Brazil, Mexico, and Argentina. Growing investments in sports development programs and increasing interest in organized tennis activities are supporting market expansion. Rising participation among younger demographics and growing availability of coaching facilities are expected to contribute to future demand growth across the region.

Middle East & Africa

The Middle East & Africa region accounted for approximately 4% of global revenue in 2025. UAE, Saudi Arabia, South Africa, and Egypt are among the most significant markets. Government-backed sports development initiatives, investments in international tournaments, and growing private sector participation are creating favorable growth conditions. Saudi Arabia's increasing investments in sports infrastructure and international sporting events are expected to support future demand expansion.

Key Players in the Tennis Balls Market

- Wilson Sporting Goods

- HEAD (Penn)

- Dunlop Sports

- Slazenger

- Yonex

- Babolat

- Tecnifibre

- Gamma Sports

- Prince Sports

- Double Fish

- DHS

- Teloon

- Artengo

- Volkl

- ProKennex