Hand Warmers Market Size

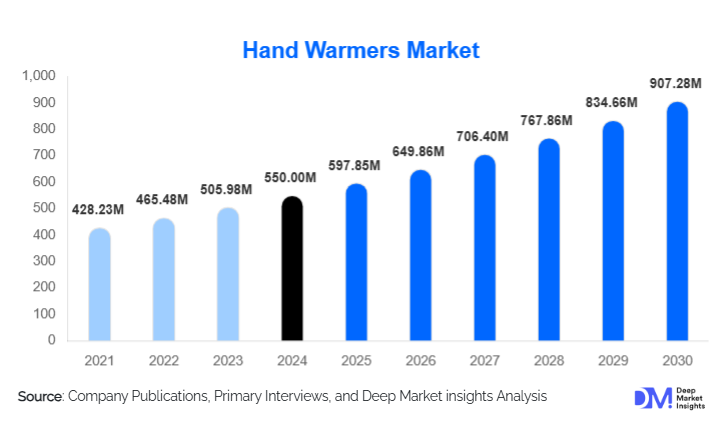

According to Deep Market Insights, the global hand warmers market size was valued at USD 1,450 million in 2024 and is projected to grow from USD 1,597.90 million in 2025 to reach USD 2,596.91 million by 2030, expanding at a CAGR of 10.2% during the forecast period (2025–2030). The market growth is driven by rising winter tourism, increased adoption of portable warming technologies in healthcare and industrial sectors, and growing demand for reusable and eco-friendly warming solutions.

Key Market Insights

- Disposable hand warmers dominate the market, accounting for 46% share in 2024, owing to high usage among daily commuters, outdoor workers, and recreational users.

- North America is the leading regional market, holding a 34% share in 2024, driven by demand from winter sports, military, and healthcare sectors.

- Asia-Pacific is the fastest-growing region, expected to grow at a 13.8% CAGR, led by China, Japan, and South Korea.

- E-commerce accounts for 48% of global sales, benefiting from wide product availability, consumer reviews, and bulk purchase programs.

- Reusable electric and USB-powered hand warmers are gaining traction due to sustainability, long heat duration, and enhanced user safety.

- Outdoor sports and adventure applications hold 31% of the market share, driven by rising participation in skiing, hiking, and mountain expeditions.

What are the latest trends in the hand warmers market?

Eco-Friendly and Reusable Technologies on the Rise

The market is observing a rapid transition from traditional single-use chemical warmers to eco-friendly reusable options, especially in developed markets with strict environmental norms. Manufacturers are introducing biodegradable filling materials, low-toxicity activation compounds, and recyclable aluminum or stainless-steel casings to align with rising sustainability standards and extended producer responsibility policies. Rechargeable lithium-ion and lithium-polymer batteries are being optimized for higher cycle life, allowing hundreds of uses per device and significantly lowering per-use cost compared with disposable packs. Government initiatives to reduce single-use thermal and plastic waste, including landfill restrictions and incentives for green product lines, are further boosting demand for reusable and refillable hand warmers. Large retailers and corporate buyers are also incorporating environmental criteria into procurement, favoring products with eco-labels or carbon-reduced claims. These new-generation warmers offer better heat retention, improved safety features such as short-circuit protection and automatic shut-off, and higher perceived value, making them increasingly popular among urban, industrial, and institutional buyers.

Smart and Wearable Heat-Integrated Warmers

Smart hand warmers equipped with digital temperature control, Bluetooth connectivity, and battery bank capabilities are gaining acceptance among tech-savvy consumers, frequent travelers, and outdoor professionals. Multi-level temperature settings, fast-charging USB-C interfaces, and integrated power indicators are becoming standard in mid- to premium-range devices. Integration of thermal technology into gloves, jackets, insoles, and medical apparel has opened opportunities for cross-category products in outdoor clothing, sportswear, and rehabilitation equipment. Wearable heat patches with IoT-enabled sensors are expected to drive innovation in the medical warming segment, enabling more precise local heating, real-time temperature monitoring, and usage analytics for arthritis and Raynaud’s disease patients. Manufacturers are piloting companion mobile apps for remote control, battery diagnostics, and safety alerts, while B2B collaborations with apparel and PPE brands are creating bundled “heated gear” systems that improve user comfort and expand the average transaction value per customer.

What are the key drivers in the hand warmers market?

Growth in Winter Tourism and Outdoor Sports

Rising participation in skiing, hiking, mountaineering, winter trekking, and endurance events is significantly driving demand for portable heating solutions. Leading countries like Canada, Switzerland, Japan, the U.S., and Nordic nations are promoting winter adventure sports through tourism campaigns, event hosting, and infrastructure upgrades, which in turn lifts sales of complementary products such as hand warmers, heated gloves, and thermal apparel. The adventure sports and winter tourism segment is growing at nearly 15% CAGR, with a higher share of spending occurring in cold months, supporting overall industry growth for hand warmers and related safety gear. Increasing participation from first-time and occasional travelers, who tend to over-index on safety accessories, further boosts unit volumes in tourist-heavy destinations and airport retail channels.

Industrial and Occupational Demand in Cold Workplaces

Construction, mining, logistics, warehousing, and oil & gas workers in low-temperature environments rely on hand warmers for safety, dexterity, and compliance with occupational comfort guidelines. Extended exposure to sub-zero temperatures can reduce productivity and increase injury risk, prompting employers to adopt portable warming solutions alongside insulated clothing. Occupational safety regulations and recommendations in the U.S. and Europe emphasize thermal protection in extreme cold, increasing corporate bulk purchases of rechargeable and high-duration hand warmers for field staff. The industrial application segment is expected to show strong and relatively stable growth because these purchases are budgeted into annual safety and PPE spending, creating repeat demand across cold-weather zones such as Canada, Scandinavia, Russia, and high-altitude work sites globally.

E-Commerce Growth and Direct Consumer Access

Digital retailing now accounts for nearly half of industry revenue, making hand warmers accessible to consumers in both mature and emerging markets. Marketplaces such as Amazon, Alibaba, Walmart.com, and specialist sporting goods platforms support seasonal sales peaks, rapid product comparisons, and visibility for niche brands that previously lacked physical shelf space. Online channels enable long-tail assortment, including specialized medical, industrial, and smart warmers, as well as personalization options such as branded casings and custom packs for corporate gifting. Subscription services, pre-winter promotional campaigns, and targeted digital advertising help smooth demand volatility and drive repeat purchases, particularly in regions with well-established winter seasons.

What are the restraints for the global market?

Environmental Concerns Over Disposable Warmers

Single-use hand warmers typically contain non-biodegradable plastics, iron powder, salts, and activated carbon, contributing to growing environmental concerns and scrutiny from regulators and environmental groups. In markets with strict waste management regulations, municipalities and retailers are increasingly discouraging or limiting single-use products, putting pressure on manufacturers that depend heavily on disposable formats for volume sales. Companies face rising costs linked to material substitution, product redesign, and potential take-back or recycling schemes, all of which affect profit margins and pricing strategies. Failure to adapt to greener formulations also carries reputational risk, particularly among younger, sustainability-conscious consumers who are shifting purchases toward reusable devices.

Seasonal Sales Dependency and Limited Use in Tropical Regions

Due to climate dependency, demand remains structurally low in tropical and equatorial regions like Southeast Asia, much of Africa, and parts of Latin America, where average winter temperatures do not justify widespread use of hand warmers. In core markets, seasonal fluctuations produce concentrated sales peaks in late autumn and winter, followed by sharp volume declines in warmer months. These patterns complicate production planning, capacity utilization, and inventory management, as manufacturers must balance sufficient pre-season stock with the risk of unsold inventory and discounting. This cyclicality poses challenges for global scalability, long-term forecasting, and investment in new production lines, particularly for smaller players without diversified product portfolios.

What are the key opportunities in the hand warmers industry?

Healthcare and Medical Therapeutic Applications

Hand warmers designed for medical and therapeutic use in managing Raynaud’s disease, arthritis, carpal tunnel syndrome, and poor peripheral circulation are gaining steady popularity. These products are increasingly prescribed or recommended as part of non-invasive pain management and circulation-improvement protocols, especially among elderly patients in Europe, Japan, and North America. Medical-grade warmers with controlled temperature ranges, skin-safe materials, and clinically validated performance can secure premium pricing, insurance reimbursements in some markets, and distribution through pharmacies, orthopedic clinics, and rehabilitation centers. As healthcare systems emphasize home-based care and self-management of chronic conditions, demand for compact, reusable therapeutic warmers is expected to rise, opening a differentiated, higher-margin subsegment within the broader market.

Smart, Rechargeable, and Wearable Thermal Solutions

Smart USB-powered warmers with adjustable temperature controls, LED indicators, and integrated power bank functions are expanding market possibilities beyond basic heating. These devices appeal to multi-purpose buyers who value both warmth and device charging in outdoor, travel, or emergency contexts. Integration with wearable gear, outdoor clothing, heated gloves, and liners is driving strong interest among consumers seeking seamless, hands-free warming products. Partnerships between electronics brands, outdoor apparel manufacturers, and PPE suppliers enable co-branded offerings that bundle hand warmers with jackets, gloves, or industrial safety kits. This segment also supports ongoing innovation in battery efficiency, miniaturization, and ergonomic design, allowing companies to differentiate and defend higher price points while capturing repeat purchases as technology upgrades.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2024 | USD 1450 Million |

| Market Size in 2025 | USD 1597.90 Million |

| Market Size in 2030 | USD 2596.91 Million |

| CAGR | 10.2% (2025-2030) |

| Base Year for Estimation | 2024 |

| Historical Data | 2021-2023 |

| Forecast Period | 2025-2030 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Disposable hand warmers led the market with a 46% share in 2024 due to their low unit price, ease of distribution, and strong presence in mass retail, convenience stores, pharmacies, and travel outlets. They are widely used for commuting, hiking, stadium events, seasonal retail promotions, and emergency preparedness kits, particularly in North America and Europe. However, growth rates for disposable products are moderating as regulatory and consumer pressures shift attention to more sustainable formats. Reusable and rechargeable hand warmers are expected to grow at over 12% CAGR, gaining share as battery costs decline and product lifespans improve. This growth is particularly notable in Europe and Asia-Pacific, where sustainability regulations and awareness are accelerating the transition from single-use to durable warming solutions.

Application Insights

Outdoor sports and adventure applications hold 31% of the market, driven by rising participation in winter camping, skiing, snowboarding, mountaineering, trekking, and marathon events in cold climates. These users typically require extended-duration warmth and often purchase multiple units per trip or per family, increasing overall volume. Military and defense applications remain lucrative, especially in the U.S., Russia, China, and India, where substantial budgets are allocated for cold-weather gear procurement for troops stationed in high-altitude and extreme-climate regions. Additional applications in construction, mining, and logistics contribute a stable baseline demand, as employers integrate hand warmers into personal protective equipment kits to maintain worker performance in low-temperature conditions.

Distribution Channel Insights

Online channels dominate with a 48% share in 2024, owing to ease of access, detailed product information, user reviews, and the ability to compare prices and functions across brands. Seasonal promotions, flash sales, and bundled offers on major e-commerce platforms significantly influence consumer purchase timing and brand choice.

Explore more data points, trends and opportunities Download Free Sample Report

Hand Warmers Market Segmentations

By Product Type

- Disposable Air-Activated Warmers

- Rechargeable Electric/Battery Warmers

- Fuel-Based Catalytic Warmers

- Phase Change Material Warmers

- Gel-Based Reusable Warmers

By Heat Source Technology

- Air-Activated (Oxidation-Based)

- Electric/Battery-Operated

- Catalytic Fuel-Based

- Infrared and Wearable Heating

- Phase Change Thermal Packs

By Distribution Channel

- Online Retail (E-commerce Marketplaces, Brand Websites)

- Sporting Goods & Outdoor Stores

- Pharmacy & Medical Supply Stores

- Supermarkets & Hypermarkets

- Industrial & Safety Equipment Distributors

Regional Insights

North America

North America leads the market with a 34% share in 2024, supported by strong usage in winter sports, outdoor recreation, military procurement, and medical applications. The U.S. accounts for 21% of global demand, driven by high disposable income, mature retail and e-commerce infrastructure, and a large base of winter travelers and outdoor enthusiasts. Canada contributes significantly through extended winter seasons, strong skiing and snowboarding culture, and reliance on hand warmers among industrial and resource-sector workers operating in sub-zero environments. Regional buyers show increasing interest in rechargeable and smart warmers, accelerating the shift away from purely disposable products.

Europe

Europe holds 27% of the market, driven by demand from Germany, the U.K., Sweden, Norway, Switzerland, and other Alpine and Nordic countries. High urban adoption, well-developed winter sports infrastructure, and strong integration of thermal aids into healthcare and eldercare support steady demand. Governments and employers in Europe emphasize worker safety in cold environments, contributing to industrial and municipal procurement of hand warmers for outdoor staff, emergency services, and public events. Environmental regulations and consumer expectations are also pushing faster adoption of reusable and eco-certified devices across the region.

Asia-Pacific

APAC is the fastest-growing region, expected to register a 13.8% CAGR, led by China, Japan, and South Korea. China is the global manufacturing hub for both disposable and rechargeable warmers, benefiting from scale, export capabilities, and growing domestic consumption in colder northern provinces. Japan leads in technological innovation, with brands focusing on compact, high-efficiency warmers, often integrated with apparel. South Korea shows strong uptake among young consumers engaged in winter sports and urban commuting. Expanding e-commerce penetration across the region is further accelerating product availability and category awareness.

Latin America

Latin America accounts for 6% of global demand, led by Chile, Argentina, and Peru, mainly for mountaineering, high-altitude tourism, and mining and industrial applications in the Andes. While overall climate conditions limit broad consumer adoption, specific cold regions and industries generate targeted demand for both disposable and rechargeable devices. Growth is supported by greater participation in adventure tourism, the expansion of local outdoor retail, and increased safety focus in high-altitude mining operations, where maintaining hand dexterity and comfort is critical.

Middle East & Africa

MEA holds around 4% of market share, with adoption growing in high-altitude regions, desert areas with cold nights, and military and security operations. South Africa and Kenya are emerging markets due to tourism activities in cooler regions and elevated terrains, where hand warmers are used alongside other thermal gear. The UAE and other Gulf countries serve as key import and re-export hubs, supplying travelers, expedition groups, and specialized industrial operations. While the region is not a core volume driver, niche demand in defense, tourism, and industrial safety is gradually increasing the penetration of higher-value rechargeable products.

Key Players in the Hand Warmers Market

- Zippo Manufacturing Company

- HotHands

- The North Face

- Kobayashi Pharmaceutical Co., Ltd.

- OCOOPA

- Heat Factory

- Energizer Holdings, Inc.

Recent Developments

- In October 2024, OCOOPA launched a dual-purpose rechargeable hand warmer with smartphone charging capabilities and extended battery life.

- In September 2024, Zippo announced a reusable catalytic hand warmer with eco-friendly refillable fuel canisters designed for long-duration outdoor events.

- In July 2024, Kobayashi introduced biodegradable single-use warmers made from plant-based, compostable materials to reduce plastic waste.