Temporary Floor Protection Market Size

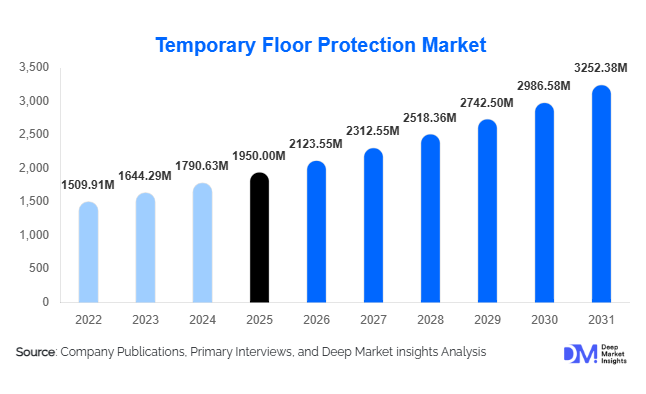

According to Deep Market Insights, the global temporary floor protection market size was valued at USD 1,950 million in 2025 and is projected to grow from USD 2,123.55 million in 2026 to reach USD 3,252.38 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The temporary floor protection market growth is primarily driven by rising construction and renovation activities worldwide, increasing awareness regarding floor damage prevention during project execution, and growing adoption of sustainable protective materials across commercial, residential, industrial, and infrastructure applications. As flooring installations become increasingly premium and expensive, contractors and facility owners are prioritizing protective solutions that reduce repair costs, minimize project delays, and improve overall asset preservation.

Key Market Insights

- Construction and renovation activities account for the majority of temporary floor protection demand, with new commercial and infrastructure projects generating substantial consumption of protection boards, films, and heavy-duty coverings.

- Sustainable and recyclable floor protection products are gaining market share, driven by green building certifications and increasing environmental regulations across developed markets.

- North America dominates the global market, supported by strong commercial remodeling activity, institutional construction spending, and widespread adoption of premium floor protection solutions.

- Asia-Pacific is the fastest-growing region, fueled by rapid urbanization, industrial expansion, and large-scale infrastructure investments across China, India, and Southeast Asia.

- Heavy-duty protection systems are witnessing accelerated adoption, particularly in industrial facilities, logistics centers, semiconductor fabs, and transportation infrastructure projects.

- Product innovation is shifting toward reusable, moisture-resistant, and high-load-capacity solutions, helping contractors improve project efficiency while reducing material waste.

Temporary Floor Protection Market Trends

Sustainable Protection Materials Becoming Industry Standard

The market is witnessing a significant transition toward environmentally responsible floor protection products. Contractors, developers, and government agencies are increasingly specifying recyclable paper boards, reusable composite sheets, and low-impact protective systems in construction tenders. Green building certifications such as LEED and BREEAM are encouraging the adoption of sustainable products that contribute to waste reduction and lower environmental footprints. Manufacturers are responding by introducing recycled fiber-based boards and reusable protection solutions capable of multiple project cycles. Sustainability has evolved from a product differentiator into a purchasing requirement for many large-scale commercial and institutional projects.

Growing Adoption of Heavy-Duty and Multi-Surface Protection Systems

Temporary floor protection products are evolving beyond basic surface coverings into engineered systems capable of handling heavy equipment, machinery movement, and prolonged project durations. Contractors increasingly prefer multi-surface protection products that can be applied across hardwood, tile, concrete, laminate, and epoxy flooring. Heavy-duty protection boards with enhanced load-bearing capacity are gaining popularity in industrial construction, logistics facilities, airports, and semiconductor manufacturing projects. Manufacturers are also integrating moisture resistance, fire-retardant properties, and anti-slip functionality to improve jobsite safety and performance.

Temporary Floor Protection Market Drivers

Expansion of Global Construction and Infrastructure Spending

The growth of residential, commercial, industrial, and public infrastructure projects worldwide continues to be the primary driver of temporary floor protection demand. Governments are investing heavily in transportation networks, healthcare facilities, educational institutions, and smart city developments. These projects require extensive protection of finished flooring during multiple construction phases, creating consistent demand for protective boards, films, and coverings. The increasing complexity and scale of infrastructure projects are further supporting long-term market expansion.

Rising Renovation and Remodeling Activities

Renovation spending has increased significantly across North America and Europe as aging commercial buildings, hotels, healthcare facilities, and residential properties undergo modernization. Existing flooring often represents a substantial investment, encouraging contractors to utilize temporary floor protection solutions throughout refurbishment activities. The trend toward premium flooring installations, including hardwood, luxury vinyl, and stone surfaces, is further accelerating demand for high-performance protection products that prevent costly repairs and replacements.

Temporary Floor Protection Market Restraints

Volatility in Raw Material Prices

Manufacturers remain exposed to fluctuations in the prices of polyethylene, polypropylene, recycled paper fiber, rubber, and other raw materials used in floor protection products. Changes in energy costs, transportation expenses, and supply chain disruptions can impact production economics and profit margins. Smaller manufacturers often face challenges in passing increased costs to customers due to competitive pricing pressures within the market.

Market Fragmentation and Price Competition

The temporary floor protection market remains fragmented, with numerous regional suppliers competing alongside global manufacturers. Product commoditization in standard film and sheet categories creates pricing pressure and limits differentiation opportunities. While premium engineered products command higher margins, many buyers continue to prioritize cost over performance, creating challenges for suppliers seeking to expand value-added product portfolios.

Temporary Floor Protection Market Opportunities

Growth of Sustainable Construction Practices

The increasing emphasis on sustainable construction provides substantial opportunities for manufacturers offering recyclable and reusable floor protection solutions. Green building initiatives are encouraging project owners to specify environmentally responsible materials throughout construction processes. Suppliers that develop certified sustainable products can access premium market segments while strengthening relationships with environmentally conscious contractors and developers. This trend is particularly strong across North America and Europe, where sustainability requirements continue to expand.

Infrastructure and Industrial Megaproject Development

Large-scale infrastructure developments and industrial investments are creating significant growth opportunities. Airports, railway systems, semiconductor fabrication plants, battery manufacturing facilities, logistics hubs, and healthcare infrastructure projects require extensive floor protection throughout construction and commissioning phases. Countries such as India, China, Saudi Arabia, Vietnam, and the United States are experiencing elevated construction spending levels, generating substantial demand for heavy-duty floor protection systems designed for long-duration projects and high-load environments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1950 Million |

| Market Size in 2026 | USD 2123.55 Million |

| Market Size in 2031 | USD 3252.38 Million |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Floor protection boards represent the largest product segment, accounting for approximately 34% of the global market in 2025. Their dominance is attributed to superior durability, load-bearing capability, and suitability for protecting high-value surfaces during extended construction activities. Protective films maintain strong demand across residential and commercial applications due to ease of installation and cost-effectiveness. Protective sheets continue to gain adoption in moisture-sensitive environments, while rubber mats and specialized heavy-duty coverings are expanding rapidly in industrial and infrastructure projects. Manufacturers are increasingly introducing composite protection boards that combine strength, reusability, and sustainability, helping to meet evolving contractor requirements.

Material Insights

Polyethylene-based products account for the largest material share of the market at approximately 29% in 2025 due to their affordability, moisture resistance, flexibility, and broad applicability across multiple floor surfaces. Paper and recycled fiber materials are experiencing strong growth as sustainability initiatives gain momentum globally. Polypropylene products remain widely used in heavy-duty applications requiring enhanced strength and durability. Composite materials are emerging as a premium segment, offering reusable solutions with superior protection characteristics for high-value commercial and industrial projects. Rubber and foam materials continue to serve specialized applications where cushioning, impact resistance, and anti-slip performance are critical.

Application Insights

New construction projects account for approximately 44% of global temporary floor protection demand, making them the largest application segment. Commercial buildings, healthcare facilities, educational institutions, and mixed-use developments represent key sources of consumption. Renovation and remodeling activities constitute the second-largest application category as aging building infrastructure undergoes modernization. Industrial maintenance shutdowns are generating increasing demand for specialized protection systems capable of withstanding heavy equipment movement and prolonged exposure. Events, exhibitions, and relocation projects continue to provide niche growth opportunities, particularly for reusable and rapid-installation floor protection products.

End-Use Insights

Commercial construction remains the largest end-use segment, representing approximately 31% of global market demand in 2025. Office developments, retail facilities, hospitality projects, healthcare infrastructure, and institutional buildings drive substantial consumption of floor protection materials. Industrial facilities are emerging as the fastest-growing end-use segment, supported by investments in semiconductor manufacturing, battery production, logistics infrastructure, and pharmaceutical facilities. Infrastructure projects such as airports, rail stations, and public transportation systems are also contributing significantly to market expansion. Residential construction continues to generate stable demand, particularly in regions experiencing strong housing development activity.

Distribution Channel Insights

Building material distributors dominate the market, accounting for approximately 41% of global sales. Their established relationships with contractors, project managers, and construction firms enable efficient product distribution across multiple project categories. Direct sales channels remain important for large infrastructure and industrial projects requiring customized solutions and technical support. Industrial supply dealers play a key role in servicing maintenance and manufacturing applications, while e-commerce platforms are experiencing rapid growth due to increasing digital procurement practices. Rental service providers are also emerging as an attractive channel for reusable protection systems deployed in short-term projects.

Explore more data points, trends and opportunities Download Free Sample Report

Temporary Floor Protection Market Segmentations

By Product Type

- Floor Protection Boards

- Protective Films

- Protective Sheets

- Mats & Runners

- Specialty Protection Solutions

By Material

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Paper & Recycled Fiber

- Rubber

- Foam

- Composite Materials

By Application

- New Construction Projects

- Renovation & Remodeling

- Industrial Maintenance Shutdowns

- Commercial Fit-Out Projects

- Events & Exhibitions

- Moving & Relocation Activities

By End User

- Residential Construction

- Commercial Construction

- Industrial Facilities

- Institutional Buildings

- Infrastructure Projects

- Events & Entertainment Venues

By Distribution Channel

- Direct Sales

- Building Material Distributors

- Industrial Supply Dealers

- E-commerce Platforms

- Rental Service Providers

Regional Insights

North America

North America accounted for approximately 35% of the global temporary floor protection market revenue in 2025, making it the largest regional market worldwide. The United States alone represented nearly 28% of global demand, supported by strong commercial renovation spending, healthcare infrastructure modernization, warehouse and logistics facility construction, and large-scale institutional development projects. The region continues to witness significant investments in data centers, semiconductor manufacturing facilities, educational institutions, and mixed-use commercial developments, all of which require extensive floor protection throughout construction and commissioning phases.

A major growth driver in North America is the increasing preference for premium flooring materials such as hardwood, luxury vinyl tile (LVT), engineered wood, and natural stone, which require effective protection against damage during construction and renovation activities. Additionally, stringent construction quality standards, workplace safety regulations, and growing awareness among contractors regarding lifecycle cost reduction have increased the adoption of advanced floor protection products. Canada continues to contribute steadily to regional growth through public infrastructure investments, healthcare expansion projects, transportation upgrades, and commercial real estate development. The growing trend toward sustainable construction practices and LEED-certified projects is also driving demand for recyclable and reusable temporary floor protection solutions across the region.

Europe

Europe represented approximately 24% of the global temporary floor protection market demand in 2025, with Germany, the United Kingdom, France, Italy, Spain, and the Netherlands serving as the region's primary markets. The European market is largely driven by renovation and refurbishment activity, as a substantial proportion of commercial, residential, and institutional buildings across the region are several decades old and require modernization. Renovation projects frequently involve the installation of high-value flooring systems, creating strong demand for protective coverings that prevent damage during construction activities.

One of the most important regional growth drivers is the increasing focus on sustainability and circular construction practices. Environmental regulations and green building standards are encouraging contractors and developers to adopt recyclable paper-based boards, reusable protection systems, and environmentally friendly materials. Germany remains the largest market within Europe due to strong industrial construction and commercial redevelopment activity, while the United Kingdom benefits from extensive healthcare, transportation, and educational infrastructure projects. France and Italy continue to generate demand through urban regeneration programs and commercial real estate modernization initiatives. The growing emphasis on reducing construction waste and improving project efficiency is expected to further strengthen demand for advanced floor protection products throughout Europe.

Asia-Pacific

Asia-Pacific accounted for approximately 31% of the global temporary floor protection market revenue in 2025 and is projected to remain the fastest-growing regional market through 2031, supported by a forecast CAGR exceeding 10%. China represents the largest market within the region due to ongoing urban development, transportation infrastructure expansion, industrial facility construction, and large-scale public infrastructure investments. The country's extensive construction sector continues to generate significant demand for floor protection materials across residential, commercial, and industrial applications.

India is emerging as the fastest-growing country globally, driven by rapid urbanization, smart city initiatives, industrial corridor developments, manufacturing expansion, and increasing investments under infrastructure modernization programs. Government initiatives promoting domestic manufacturing and industrial development are accelerating the construction of factories, logistics centers, warehouses, and commercial facilities that require temporary floor protection throughout project execution. Japan and South Korea contribute significantly through advanced manufacturing investments, healthcare infrastructure upgrades, and commercial redevelopment projects. Southeast Asian economies, including Vietnam, Indonesia, Thailand, and Malaysia, are experiencing growing demand due to rising foreign direct investment (FDI), industrial relocation activities, and increasing residential construction. The region's expanding middle-class population, rising construction spending, and growing adoption of modern building practices are expected to sustain long-term market growth.

Latin America

Latin America represented approximately 4% of the global temporary floor protection market in 2025, with Brazil and Mexico accounting for the majority of regional demand. The market is benefiting from increasing investments in industrial facilities, logistics infrastructure, commercial real estate, and residential construction projects. Brazil remains the largest market in the region due to ongoing infrastructure development and urban construction activity, while Mexico continues to benefit from nearshoring-related manufacturing investments and warehouse development associated with North American supply chain expansion.

The primary growth drivers across Latin America include rising awareness regarding construction quality standards, increasing adoption of premium flooring materials, and growing efforts by contractors to reduce project rework costs. Industrial parks, distribution centers, and manufacturing facilities are generating increasing demand for heavy-duty protection systems capable of withstanding equipment movement and high foot traffic. Although market penetration remains lower compared to developed regions, improving construction practices and growing investment in commercial infrastructure are expected to create substantial opportunities for floor protection manufacturers over the forecast period.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6% othe f global temporary floor protection market demand in 2025. Saudi Arabia and the United Arab Emirates are the largest consumers within the region, driven by ambitious infrastructure programs, tourism developments, smart city projects, airports, hospitality complexes, and large-scale commercial construction activities. Mega-projects associated with Saudi Vision 2031, including NEOM, The Red Sea Project, and major transportation infrastructure investments, are generating significant demand for temporary floor protection products throughout project lifecycles.

A key regional growth driver is the substantial government spending directed toward economic diversification and non-oil sector development. The UAE continues to witness strong demand from luxury hospitality, commercial real estate, and mixed-use developments, where high-end flooring installations require advanced protection systems. In Africa, South Africa remains the largest market, supported by commercial construction, industrial facility upgrades, healthcare infrastructure expansion, and institutional development projects. Other countries, including Egypt, Nigeria, Kenya, and Morocco,o are gradually increasing their adoption of floor protection solutions as construction activity expands and awareness regarding asset protection improves. Rising foreign investment, urbanization, and infrastructure modernization initiatives are expected to support long-term market growth across the region.

Key Players in the Temporary Floor Protection Market

- 3M

- Trimaco

- Surface Shields

- Ram Board

- Packexe

- Pro Tect Associates

- Armor Surface Protection

- Easydek

- Floortex

- Norkan

- Presto Tape

- Protecta Screen

- DuraBoard

- Coverguard

- Builder Board Systems