Teff Products Market Size

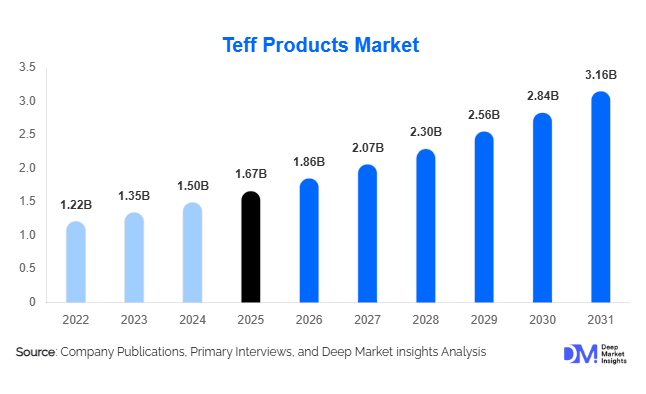

According to Deep Market Insights, the global teff products market size was valued at USD 1.67 billion in 2025 and is projected to grow from USD 1.86 billion in 2026 to reach USD 3.16 billion by 2031, expanding at a CAGR of 11.2% during the forecast period (2026–2031). The teff products market growth is primarily driven by the increasing demand for gluten-free foods, rising consumer preference for ancient grains and functional nutrition, and expanding applications of teff across bakery, breakfast cereal, sports nutrition, and health food categories. As consumers increasingly seek nutrient-dense ingredients with clean-label positioning, teff has emerged as a premium grain alternative to conventional wheat and rice-based products. Growing awareness of digestive health, plant-based nutrition, and sustainable food consumption is further accelerating global adoption of teff-derived products.

Key Market Insights

- Teff flour remains the largest product category, accounting for nearly 38% of global market revenue due to widespread use in gluten-free bakery and food manufacturing applications.

- Gluten-free foods represent the largest application segment, contributing approximately 34% of total market demand globally.

- North America dominates the global teff products market, supported by strong consumer awareness of ancient grains, mature health-food retail channels, and expanding gluten-free product portfolios.

- Asia-Pacific is the fastest-growing regional market, driven by increasing health consciousness, rising disposable incomes, and growing adoption of specialty grains in India, China, and Australia.

- Organic teff products are gaining significant traction, benefiting from consumer demand for certified sustainable and clean-label food products.

- Product innovation across cereals, snack bars, protein blends, and functional beverages is creating new growth opportunities for manufacturers and retailers.

Teff Products Market Latest Trends

Ancient Grains Becoming Mainstream Functional Ingredients

The global food industry is witnessing a significant shift toward ancient grains as consumers increasingly prioritize nutritional quality and ingredient transparency. Teff is benefiting from this trend due to its naturally high fiber, iron, calcium, and protein content. Food manufacturers are incorporating teff into premium breads, cereals, energy bars, granola products, and ready-to-eat snacks to differentiate their offerings from conventional grain-based products. The grain's strong nutritional profile allows brands to position products within premium wellness and functional food categories. Retailers are expanding shelf space dedicated to ancient grains, while foodservice operators are introducing teff-based menu items to address growing consumer demand for healthier alternatives. This trend is expected to continue supporting premium pricing and market expansion over the coming decade.

Expansion of Teff-Based Convenience Foods

Convenience-oriented teff products are rapidly gaining popularity among urban consumers seeking healthy foods with minimal preparation time. Manufacturers are launching teff-based breakfast cereals, snack bars, baking mixes, ready-to-eat meals, and instant porridge products to capture growing demand from busy consumers. Innovation in processing technologies has improved texture, flavor profiles, and shelf stability, making teff products more appealing to mainstream audiences. E-commerce platforms are also enabling niche teff brands to access broader customer bases globally. As convenience and health continue to converge within the food industry, processed teff products are expected to record faster growth than traditional whole-grain offerings.

Teff Products Market Drivers

Rising Demand for Gluten-Free Foods

The increasing prevalence of gluten intolerance, celiac disease, and gluten-sensitive lifestyles is one of the strongest growth drivers for the teff products market. Consumers are actively seeking gluten-free alternatives that provide superior nutrition compared to conventional rice and corn-based products. Teff's naturally gluten-free composition, combined with its high mineral and protein content, makes it particularly attractive to both consumers and food manufacturers. The expansion of gluten-free product ranges by major retailers and food companies is creating substantial demand for teff flour and related ingredients across developed and emerging markets.

Growing Consumer Interest in Functional Nutrition

Health-conscious consumers are increasingly prioritizing foods that deliver measurable nutritional benefits beyond basic caloric intake. Teff's rich content of iron, dietary fiber, resistant starch, and essential amino acids aligns closely with this trend. Functional food manufacturers are incorporating teff into products targeting digestive health, weight management, heart health, and sports performance. Growing interest in plant-based diets is further supporting teff adoption, as consumers seek nutrient-dense grains that can complement vegetarian and vegan eating patterns.

Product Innovation Across Food Categories

Continuous innovation is expanding teff applications beyond traditional flour products. Manufacturers are developing teff-based pasta, breakfast cereals, nutritional beverages, snack bars, protein blends, and infant nutrition products. These innovations are increasing consumer exposure to teff while creating new revenue streams across multiple food categories. Investment in processing technologies and product development is enabling companies to improve product functionality, texture, and taste, accelerating adoption among mainstream consumers.

Teff Products Market Restraints

Supply Chain Concentration and Production Volatility

Global teff production remains heavily concentrated in Ethiopia, creating vulnerability to supply disruptions, weather-related production challenges, and export policy fluctuations. Supply instability can result in raw material shortages and price volatility, limiting large-scale adoption among multinational food manufacturers. Expanding cultivation into new agricultural regions remains critical for reducing long-term supply risks.

Limited Consumer Awareness in Emerging Markets

Despite growing popularity in North America and Europe, consumer awareness of teff remains relatively limited across many emerging economies. Compared with quinoa, oats, and other ancient grains, teff often lacks mainstream recognition. Manufacturers must invest in consumer education, marketing campaigns, and product sampling initiatives to build awareness and support wider market penetration.

Teff Products Industry Key Opportunities

Expansion of Sports Nutrition and Performance Foods

The sports nutrition industry presents a significant growth opportunity for teff product manufacturers. Teff's slow-release carbohydrates, balanced amino acid profile, and naturally occurring minerals make it highly suitable for endurance athletes and active consumers. Manufacturers are increasingly exploring applications in protein blends, meal replacement products, recovery beverages, and energy bars. As consumers shift toward natural and clean-label sports nutrition solutions, teff-based formulations can provide differentiation and support premium pricing strategies. The segment is expected to outpace overall market growth through 2031.

Development of Regional Teff Cultivation Programs

The expansion of commercial teff farming beyond Ethiopia represents a major opportunity for industry participants. Countries including the United States, Australia, Canada, India, and South Africa are increasingly evaluating teff cultivation due to its drought tolerance and nutritional value. Regional cultivation can improve supply security, reduce transportation costs, and enable locally sourced product claims. Governments promoting agricultural diversification and climate-resilient crops may further support investments in teff farming, processing infrastructure, and contract agriculture programs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.67 Billion |

| Market Size in 2026 | USD 1.86 Billion |

| Market Size in 2031 | USD 3.16 Billion |

| CAGR | 11.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The teff products market is segmented into teff flour, whole teff grain, ready-to-eat teff products, teff-based beverages, and nutritional blends. Among these, teff flour dominates the global market, accounting for approximately 38% of total revenue in 2025. The segment’s leadership is primarily driven by the growing demand for gluten-free and nutrient-dense ingredients across bakery, snack, cereal, and packaged food applications. Food manufacturers increasingly prefer teff flour due to its versatility, high fiber content, rich mineral profile, and ability to enhance the nutritional value of gluten-free formulations without compromising product quality. The rising prevalence of gluten intolerance, celiac disease, and consumer preference for clean-label ingredients further strengthens demand for teff flour globally.Whole teff grain remains a significant segment, particularly in traditional consumption markets and among consumers seeking minimally processed foods with high nutritional value. Demand for whole grains continues to increase as consumers become more aware of the health benefits associated with fiber-rich diets and natural food ingredients. Ready-to-eat teff products, including breakfast cereals, snack bars, crackers, and convenience foods, represent one of the fastest-growing categories within the market. Growth is supported by changing lifestyles, increasing urbanization, and rising demand for healthy on-the-go meal solutions. Similarly, teff-based beverages and nutritional blends are gaining market traction as manufacturers expand product offerings within functional nutrition, wellness, and sports nutrition categories. Continuous product innovation, wider retail availability, and growing consumer familiarity with ancient grains are expected to further diversify the product landscape and enhance overall market penetration during the forecast period.

Application Insights

Based on application, the market is categorized into gluten-free foods, functional foods, bakery products, sports nutrition, dietary supplements, infant nutrition, and animal feed. Gluten-free foods represent the largest application segment, accounting for approximately 34% of global market demand in 2025. The segment's dominance is primarily driven by the increasing prevalence of gluten sensitivity and celiac disease, coupled with growing consumer adoption of gluten-free diets as part of broader health and wellness lifestyles. Teff has emerged as a preferred ingredient among food manufacturers due to its naturally gluten-free composition, superior nutritional profile, and ability to improve product differentiation in an increasingly competitive market.Functional foods constitute another major application area, benefiting from rising consumer demand for nutrient-rich products that support digestive health, immunity, energy management, and overall well-being. Bakery applications continue to generate substantial demand as manufacturers increasingly incorporate teff flour into breads, cookies, cakes, muffins, and specialty baked products to enhance nutritional content while meeting gluten-free requirements. Sports nutrition and dietary supplement applications are witnessing strong growth due to increasing recognition of teff's protein, iron, calcium, and essential amino acid content, which support active lifestyles and athletic performance. Infant nutrition is also emerging as a promising application segment, supported by growing interest in nutrient-dense ingredients for early childhood development. Although animal feed currently accounts for a relatively small share of the market, demand is gradually increasing in selected agricultural markets where alternative nutrient-rich feed ingredients are gaining acceptance.

Distribution Channel Insights

The market is distributed through supermarkets and hypermarkets, specialty health food stores, online retail platforms, direct-to-consumer channels, and foodservice networks. Supermarkets and hypermarkets account for approximately 45% of global teff product sales, making them the leading distribution channel. The segment's dominance is driven by extensive product visibility, broad consumer reach, and the ability of major retail chains to position teff products alongside health foods, organic products, and specialty grains. Growing shelf space allocation for functional and gluten-free foods within large retail formats continues to support segment expansion.Specialty health food stores remain an important channel, particularly for premium, organic, and niche teff products targeting wellness-focused consumers. These outlets play a critical role in educating consumers about the nutritional benefits of ancient grains and supporting premium product positioning. Online retail and direct-to-consumer channels are experiencing rapid growth as e-commerce platforms improve product accessibility, enable subscription-based purchasing models, and allow emerging brands to reach geographically diverse consumer bases. Increasing digitalization, convenience-driven shopping behaviors, and the availability of detailed product information are further accelerating online sales. Foodservice distribution is also expanding steadily, supported by the growing incorporation of teff ingredients into restaurant menus, artisan bakeries, cafés, and hospitality establishments focused on healthy and innovative food offerings.

End-User Insights

Based on end users, the market includes food and beverage manufacturers, bakery and confectionery producers, household consumers, nutraceutical companies, sports nutrition manufacturers, infant nutrition producers, and foodservice operators. Food and beverage manufacturers represent the largest end-user segment, accounting for approximately 31% of total market demand. The segment's leadership is primarily attributed to increasing incorporation of teff ingredients into packaged foods, cereals, snacks, bakery products, meal replacements, and functional food formulations. Rising consumer demand for healthier food alternatives continues to encourage manufacturers to integrate nutrient-rich ancient grains into mainstream product portfolios.Bakery and confectionery manufacturers also account for a significant share of consumption due to growing demand for gluten-free and specialty baked products. Household consumers remain a key source of retail demand, particularly across North America and Europe, where health-conscious purchasing patterns and interest in alternative grains continue to strengthen. Nutraceutical producers, sports nutrition brands, and infant nutrition manufacturers are emerging as high-growth end-user categories as consumers increasingly seek products offering enhanced nutritional benefits and functional health attributes. Demand from foodservice and hospitality operators is also rising steadily as restaurants, cafés, and premium dining establishments incorporate ancient grains into innovative menu offerings to meet evolving consumer preferences.

Nature Insights

The market is segmented into conventional and organic teff products. Conventional teff products dominate the global market, accounting for approximately 82% of total revenue in 2025. The segment's leadership is largely driven by greater production volumes, lower product costs, wider distribution networks, and consistent supply availability. Food manufacturers continue to favor conventional teff due to its competitive pricing and suitability for large-scale commercial food production. The ability to maintain stable sourcing and meet growing industrial demand further strengthens the segment's position across global markets.Organic teff products, while representing a smaller share of overall revenue, are expected to witness faster growth throughout the forecast period. Increasing consumer preference for sustainable agriculture, clean-label ingredients, chemical-free cultivation practices, and certified organic food products is driving demand within the segment. Premium pricing opportunities associated with organic certification are attracting investments from producers, processors, and retailers seeking to capitalize on higher-margin market opportunities. As environmental sustainability and health-conscious purchasing behaviors continue to influence food consumption patterns, organic teff products are expected to gain increasing market share over the coming years.

Explore more data points, trends and opportunities Download Free Sample Report

Teff Products Market Segmentations

By Product Type

-

Whole Teff Grain

- White Teff Grain

- Brown Teff Grain

- Mixed/Colored Teff Grain

-

Teff Flour

- Conventional Teff Flour

- Organic Teff Flour

-

Ready-to-Eat (RTE) Teff Foods

- Breakfast Cereals

- Granola & Muesli

- Snack Bars

- Puffed Snacks

-

Teff Bakery Products

- Bread

- Flatbreads & Injera

- Biscuits & Cookies

- Cakes & Muffins

- Teff-Based Pasta & Noodles

- Teff-Based Beverage Products

- Teff Ingredients & Blends

By Nature

- Conventional Teff Products

- Organic Teff Products

By Application

- Gluten-Free Foods

- Functional & Health Foods

- Bakery Applications

- Breakfast Foods & Cereals

- Sports Nutrition

- Infant Nutrition

- Dietary Supplements

- Animal Feed

By End User

- Household Consumers

- Food & Beverage Manufacturers

- Bakery & Confectionery Manufacturers

- Foodservice & Hospitality

- Nutraceutical & Functional Food Producers

- Infant Nutrition Manufacturers

- Animal Feed Manufacturers

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Health Food Stores

- Convenience Stores

- Online Retail & E-Commerce

- Direct-to-Consumer (DTC)

- Foodservice Distribution

Regional Insights

North America

North America accounted for approximately 34% of global teff products market revenue in 2025, making it the largest regional market. The United States contributes nearly 27% of global demand and remains the primary growth engine within the region. Market expansion is supported by strong consumer demand for gluten-free foods, increasing adoption of functional nutrition products, and growing interest in ancient grains as part of healthy dietary patterns. The region benefits from a highly developed retail ecosystem, extensive availability of specialty food products, strong consumer purchasing power, and widespread awareness regarding the nutritional benefits of teff. Rising product innovation by food manufacturers, growing demand for plant-based ingredients, and increasing incorporation of teff into bakery, snack, and wellness products continue to support long-term market growth. Canada is also experiencing rising adoption of teff products across health food stores, natural grocery retailers, and premium bakery categories.

Europe

Europe represents approximately 29% of the global market and remains one of the most important regions for teff consumption outside Ethiopia. Germany, the United Kingdom, France, Italy, Spain, and the Netherlands serve as major demand centers across the region. Growth is driven by increasing consumer preference for organic foods, clean-label ingredients, sustainable nutrition, and gluten-free dietary products. Europe’s well-established health and wellness industry, coupled with stringent food quality standards and growing demand for plant-based nutrition, continues to create favorable conditions for market expansion. Germany remains the largest market within the region, accounting for roughly 7% of global demand. The rapid development of gluten-free bakery products, functional foods, and premium health food categories is expected to sustain long-term growth, while increasing investments in sustainable food systems further support adoption of ancient grains such as teff.

Asia-Pacific

Asia-Pacific accounted for approximately 18% of global revenue in 2025 and is projected to register the fastest growth rate through 2031. India, China, Australia, Japan, and South Korea are emerging as important demand centers due to increasing health awareness, rising disposable incomes, and expanding middle-class populations. The region's growth is being driven by growing consumer interest in nutrient-dense foods, rapid urbanization, increasing demand for plant-based nutrition, and expanding availability of imported specialty food products. Australia is developing into a notable cultivation and processing hub, helping strengthen regional supply capabilities. India is expected to be the fastest-growing country globally, supported by expanding health-food retail networks, rising demand for gluten-free products, growing fitness-conscious populations, and increasing awareness of ancient grains as nutritional alternatives to conventional cereals.

Latin America

Latin America represents approximately 5% of global market demand, with Brazil, Mexico, Argentina, and Chile leading regional consumption. Although the market remains relatively nascent, growth prospects continue to improve as awareness of healthy eating habits and gluten-free nutrition expands across urban populations. Increasing consumer interest in functional foods, rising incidence of lifestyle-related health concerns, and gradual expansion of premium grocery retail channels are supporting demand growth. Specialty food retailers and health-focused supermarkets are increasingly introducing teff products to consumers seeking nutrient-rich alternatives to traditional grains. Continued improvements in product availability, distribution infrastructure, and consumer education are expected to contribute to steady market expansion across the region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 14% of global demand and remains strategically important due to Ethiopia's dominant role in global teff production and consumption. Ethiopia continues to serve as the largest producer and domestic consumer of teff products worldwide, providing a strong foundation for regional market development. Growth across the broader region is supported by expanding export activities, increasing investment in agricultural modernization, and growing international demand for teff-based products. In the Middle East, countries such as the UAE and Saudi Arabia are witnessing rising demand driven by growing expatriate populations, increasing health-food consumption, higher disposable incomes, and expanding availability of premium imported food products. The region's importance within the global value chain is expected to strengthen further as production capacities, processing capabilities, and export networks continue to develop, enhancing the availability of teff products across international markets.

Key Players in the Teff Products Market

- The Teff Company

- Bob's Red Mill

- Maskal Teff

- Ancient Harvest

- King Arthur Baking Company

- Shiloh Farms

- Arrowhead Mills

- Amandin Organic

- Tobia Teff

- Nu-World Foods

- Nature's Path Foods

- Woodland Foods

- Shipton Mill

- Teff Tribe

- Pure Living Organic