Kidney Beans Market Size

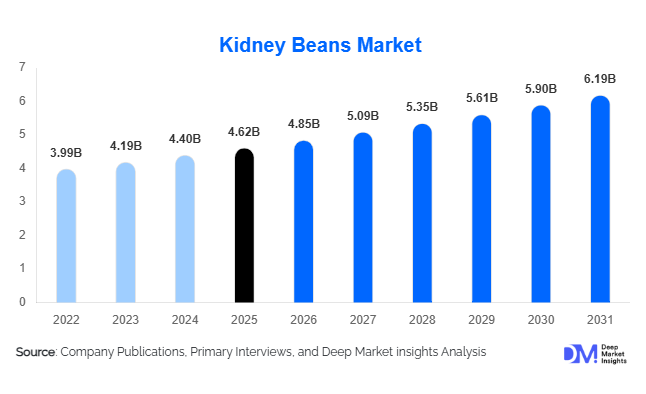

According to Deep Market Insights, the global kidney beans market size was valued at USD 4.62 billion in 2025 and is projected to grow from USD 4.85 billion in 2026 to reach USD 6.19 billion by 2031, expanding at a CAGR of 5.0% during the forecast period (2026–2031). The kidney beans market growth is primarily driven by increasing global consumption of plant-based protein sources, rising awareness regarding nutritional benefits of pulses, growing demand for clean-label food ingredients, and expanding utilization of kidney beans in processed food manufacturing. As consumers increasingly prioritize healthy diets rich in fiber, protein, vitamins, and minerals, kidney beans have emerged as a cost-effective and sustainable protein alternative across developed and emerging economies. Additionally, expanding food security initiatives, institutional nutrition programs, and increasing demand for convenience foods containing legumes continue to support market expansion globally.

Key Market Insights

- Red kidney beans account for more than 55% of global market demand, driven by their widespread use across Asian, Latin American, Middle Eastern, and North American cuisines.

- Dry kidney beans remain the dominant product form, representing nearly 61% of global consumption due to longer shelf life, affordability, and strong international trade volumes.

- Asia-Pacific dominates the global kidney beans market, accounting for approximately 44% of worldwide demand, led by India and China.

- Plant-based protein applications are emerging as the fastest-growing segment, driven by increasing demand for meat alternatives and functional food ingredients.

- Processed food manufacturers account for nearly 40% of market demand, supported by growing production of canned foods, soups, ready meals, and frozen products.

- Technological advancements in precision agriculture, optical sorting, and automated processing are improving yield quality, operational efficiency, and supply chain traceability.

Kidney Beans Market Latest Trends

Growing Adoption of Plant-Based Protein Ingredients

One of the most significant trends shaping the kidney beans market is the increasing use of kidney beans as a raw material for plant-based protein products. Food manufacturers are incorporating kidney bean protein concentrates, flours, and functional ingredients into meat substitutes, protein snacks, nutritional supplements, and healthy ready-to-eat products. As consumers seek sustainable alternatives to animal proteins, kidney beans offer an attractive nutritional profile characterized by high protein content, dietary fiber, low fat levels, and essential micronutrients. The rapid expansion of vegan, vegetarian, and flexitarian diets across North America, Europe, and Asia-Pacific is creating substantial demand for kidney bean-derived ingredients. Product developers are also utilizing kidney bean flour in gluten-free bakery products and functional foods, further diversifying application opportunities.

Expansion of Value-Added and Convenience Food Products

Global food manufacturers are increasingly shifting from bulk dry bean sales toward value-added kidney bean products such as canned beans, ready-to-eat meals, frozen foods, instant soups, and pre-cooked packaged legumes. Urbanization, changing lifestyles, and increasing demand for convenience foods are accelerating this transition. Consumers are seeking nutritious meal solutions that require minimal preparation time while retaining health benefits. Consequently, processors are investing in automated packaging, retort technology, and advanced preservation systems to enhance product shelf life and quality. Premium organic kidney beans, traceable sourcing programs, and sustainable packaging solutions are also gaining momentum, particularly in developed markets where consumers prioritize transparency and environmental responsibility.

Kidney Beans Market Drivers

Rising Global Demand for Plant-Based Nutrition

The growing preference for plant-based diets remains one of the strongest growth drivers for the kidney beans market. Consumers are increasingly reducing meat consumption due to health, environmental, and ethical considerations. Kidney beans provide an affordable and sustainable protein source that supports balanced nutrition while reducing dietary dependence on animal-based proteins. Growing awareness regarding cardiovascular health, diabetes management, and digestive wellness has further increased pulse consumption worldwide.

Expansion of Processed Food Manufacturing

The rapid growth of the processed food industry is creating significant opportunities for kidney bean suppliers. Kidney beans are extensively used in canned foods, soups, frozen meals, ready-to-eat products, salads, and snack applications. Their versatility, nutritional value, and long shelf life make them highly attractive ingredients for food manufacturers. Rising urbanization and increasing demand for convenience foods are further accelerating industrial consumption.

Government-Led Nutrition and Food Security Programs

Many governments are promoting pulse consumption through public nutrition initiatives, school feeding programs, food assistance schemes, and agricultural support policies. Countries such as India, Brazil, and several African nations actively encourage pulse cultivation and consumption to address nutritional deficiencies while improving food security. These programs create stable demand for kidney beans while supporting domestic production and trade expansion.

Kidney Beans Market Restraints

Agricultural Yield Volatility and Climate Risks

Kidney bean production remains highly vulnerable to climate-related disruptions including droughts, floods, temperature fluctuations, and pest infestations. Such factors can significantly impact crop yields, resulting in supply shortages and price volatility. Climate uncertainty continues to challenge both producers and processors across major producing regions.

Supply Chain and Storage Constraints

The kidney beans market faces logistical challenges associated with storage, transportation, and export infrastructure. In several developing countries, inadequate warehousing facilities and inefficient logistics networks contribute to post-harvest losses and quality degradation. Supply chain disruptions can increase procurement costs and negatively impact profitability across the value chain.

Kidney Beans Market Opportunities

Expansion of Plant-Based Protein Manufacturing

The rapidly growing plant-based food sector presents significant opportunities for kidney bean processors and ingredient manufacturers. Demand for meat alternatives, protein concentrates, and functional ingredients continues to rise globally. Kidney beans possess desirable nutritional characteristics that make them suitable for incorporation into protein-rich formulations, supporting higher-value applications beyond traditional consumption.

Growth of Institutional Nutrition Programs

Public procurement initiatives focused on food security, school nutrition, healthcare facilities, and government-supported meal programs offer attractive growth opportunities for market participants. Kidney beans provide a cost-effective source of protein and essential nutrients, making them ideal candidates for large-scale institutional purchasing contracts. Suppliers capable of ensuring consistent quality and supply can benefit substantially from these long-term demand channels.

Development of Export-Oriented Processing Industries

Many producing countries continue to export kidney beans primarily in raw form, leaving significant value addition opportunities untapped. Investments in canned products, ready-to-eat foods, frozen meals, organic products, and specialty bean ingredients can substantially improve profitability. Export-oriented processors in India, China, Argentina, Brazil, and Canada are increasingly targeting premium international markets where demand for convenient and healthy food products continues to grow.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.62 Billion |

| Market Size in 2026 | USD 4.85 Billion |

| Market Size in 2031 | USD 6.19 Billion |

| CAGR | 5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The red kidney beans segment dominates the global kidney beans market, accounting for approximately 55% of total market value in 2025. The segment’s leadership is primarily driven by its widespread consumption across major food cultures, strong consumer familiarity, high nutritional value, and extensive application in traditional as well as processed food products. Red kidney beans are widely utilized in soups, curries, stews, salads, chili-based dishes, canned foods, and ready-to-eat meals across North America, Latin America, Asia-Pacific, and the Middle East. Their rich protein, fiber, iron, and antioxidant content further strengthens consumer preference as demand for nutrient-dense plant-based foods continues to rise. White kidney beans, including cannellini varieties, constitute the second-largest product category and maintain strong demand across European countries where they are extensively incorporated into Mediterranean cuisine, soups, and premium packaged food products. In addition, specialty and heirloom kidney bean varieties are witnessing growing acceptance among premium consumers seeking differentiated flavor profiles, enhanced nutritional attributes, and traceable sourcing. The increasing popularity of organic farming practices and clean-label food products is further accelerating demand for organic specialty kidney beans, making this category one of the most attractive emerging segments within the global market.

Form Insights

The dry kidney beans segment accounted for nearly 61% of global demand in 2025, making it the largest form category in the market. The segment’s dominance is largely attributed to its cost-effectiveness, extended shelf life, ease of transportation, and strong presence in international commodity trade. Dry kidney beans remain a staple food ingredient in developing economies where affordability and long-term storage capabilities are critical purchasing considerations. The canned kidney beans segment is emerging as the fastest-growing category due to increasing consumer preference for convenience foods, time-saving meal solutions, and ready-to-use ingredients. Rising urbanization, busy lifestyles, and expanding retail penetration continue to support growth in canned products across developed and emerging economies. Frozen kidney beans and ready-to-eat bean-based products are also gaining momentum, particularly in North America and Europe, where consumers increasingly prioritize convenience without compromising nutritional value. Furthermore, kidney bean flour, starches, protein concentrates, and functional ingredients are creating new growth opportunities within the market. The expansion of gluten-free foods, plant-based nutrition products, sports nutrition formulations, and functional food applications is driving increasing utilization of kidney bean-derived ingredients across the global food manufacturing sector.

Application Insights

Processed food manufacturing represents the largest application segment, contributing approximately 40% of global kidney bean demand in 2025. The segment’s leadership is supported by the growing consumption of convenience foods, increasing demand for nutritious ready meals, and expanding use of legumes in value-added food formulations. Kidney beans are widely incorporated into canned foods, soups, frozen meals, salads, meal kits, snacks, and prepared food products due to their nutritional benefits and versatility. Household consumption continues to represent a substantial share of global demand, particularly across Asia-Pacific, Latin America, and parts of Africa where pulses remain essential dietary staples and affordable protein sources. Foodservice establishments, including restaurants, hotels, catering companies, and institutional kitchens, are increasingly integrating kidney beans into menu offerings to address rising consumer demand for healthier and plant-based meal options. Additionally, the ingredient manufacturing segment is experiencing robust growth as food producers increasingly utilize kidney bean flours, protein concentrates, starches, and functional ingredients in bakery products, meat alternatives, nutritional supplements, and advanced food formulations designed to meet evolving consumer preferences.

Distribution Channel Insights

Traditional grocery stores continue to account for the largest share of global kidney bean distribution, representing approximately 42% of total sales in 2025. The segment’s dominance is driven by extensive accessibility, established consumer purchasing habits, strong penetration in rural and semi-urban regions, and the continued importance of informal retail networks across developing economies. Small neighborhood stores and local food retailers remain critical distribution points, particularly in Asia-Pacific, Latin America, and Africa. Supermarkets and hypermarkets are steadily expanding their market presence as urbanization accelerates and organized retail infrastructure develops across emerging economies. These retail formats offer consumers greater product variety, improved packaging options, and wider availability of premium and branded kidney bean products. E-commerce platforms are rapidly emerging as a significant growth channel, supported by increasing internet penetration, digital payment adoption, and growing consumer interest in specialty, organic, and premium bean varieties. Institutional procurement channels, including schools, hospitals, military organizations, government nutrition programs, and food assistance agencies, also represent an increasingly important source of stable demand as public and private organizations continue to prioritize affordable, protein-rich food products.

End-Use Industry Insights

The food processing industry remains the largest end-use sector in the global kidney beans market, accounting for approximately 38% of overall demand in 2025. The segment’s leading position is primarily driven by the rapid expansion of convenience foods, increasing demand for nutritious packaged products, and growing utilization of legumes in processed food manufacturing. Food processors continue to expand production of canned foods, soups, frozen meals, ready-to-eat products, snacks, and plant-based food offerings containing kidney beans. Household retail consumption remains a foundational market segment, supported by increasing health awareness, dietary diversification, and growing recognition of pulses as affordable sources of protein and dietary fiber. The plant-based protein industry represents the fastest-growing end-use category as manufacturers increasingly incorporate kidney bean proteins into meat alternatives, protein blends, vegan food products, and nutritional supplements. Furthermore, nutraceutical and functional food manufacturers are expanding the use of kidney bean extracts, starches, and protein ingredients in wellness-oriented products targeting weight management, digestive health, blood sugar management, and overall nutritional enhancement.

Explore more data points, trends and opportunities Download Free Sample Report

Kidney Beans Market Segmentations

By Product Type

-

Red Kidney Beans

- Dark Red Kidney Beans

- Light Red Kidney Beans

-

White Kidney Beans

- Cannellini Beans

- Small White Kidney Beans

- Speckled Kidney Beans

- Other Specialty Kidney Beans

By Form

- Dry Kidney Beans

- Canned Kidney Beans

- Frozen Kidney Beans

- Ready-to-Eat Kidney Beans

- Kidney Bean Flour/Powder

- Kidney Bean Protein Ingredients

By Nature

- Conventional

- Organic

By Application

- Direct Household Consumption

- Processed Food Manufacturing

- Foodservice Industry

- Ingredient Industry

- Animal Feed Applications

By Distribution Channel

- Modern Retail

- Traditional Grocery Stores

- Online Retail / E-Commerce

- Cash & Carry / Wholesale Clubs

- Institutional Procurement

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global kidney beans market, accounting for approximately 44% of total market value in 2025. India remains the largest consumer globally, representing nearly 18% of worldwide demand due to strong pulse consumption traditions, favorable government nutrition initiatives, and the widespread role of legumes in daily diets. China is another major market, supported by increasing health awareness, rising disposable incomes, and rapid expansion of the processed food industry. Demand across Southeast Asian countries including Indonesia, Vietnam, Thailand, and the Philippines continues to increase as urbanization, dietary diversification, and growing middle-class populations drive consumption of protein-rich food products. Regional market growth is further supported by population expansion, increasing focus on food security, rising adoption of plant-based diets, growing investments in food processing infrastructure, and favorable government programs promoting pulse production and consumption. As a result, Asia-Pacific is expected to remain both the largest and fastest-growing regional market through 2031.

North America

North America accounts for approximately 18% of global kidney bean demand, led by the United States and Canada. The region's growth is primarily driven by increasing adoption of plant-based and flexitarian diets, rising consumer awareness regarding protein-rich foods, and growing demand for clean-label and functional food products. The popularity of Latin American, Mexican, and Mediterranean cuisines has further expanded kidney bean consumption across foodservice and household applications. The United States remains a major importer, processor, and consumer of kidney beans, while Canada continues to play a significant role as both a producer and exporter. Additional growth drivers include increasing demand for organic products, expansion of meat alternative industries, strong retail distribution networks, and continued innovation in convenient packaged food products featuring legumes and plant-based ingredients.

Europe

Europe represents approximately 14% of global market demand, with Germany, the United Kingdom, France, Italy, and Spain serving as major consumption centers. The regional market is benefiting from increasing adoption of vegetarian and vegan lifestyles, growing consumer emphasis on sustainability, and stronger demand for environmentally responsible food choices. Kidney beans are increasingly incorporated into ready meals, canned foods, soups, salads, and alternative protein formulations. Rising awareness regarding the health benefits of legumes, coupled with supportive regulatory initiatives encouraging sustainable food systems, continues to strengthen market growth. Furthermore, expanding investments in plant-based food innovation, increasing demand for organic products, and growing retail availability of premium bean varieties are supporting sustained expansion across the European market.

Latin America

Latin America accounts for approximately 16% of global market value and remains one of the most established kidney bean consumption regions worldwide. The market is strongly supported by the deep cultural integration of beans into daily diets across countries such as Brazil, Mexico, Argentina, Colombia, and Chile. Kidney beans serve as a staple source of affordable nutrition and protein throughout the region. Growth is being driven by rising urbanization, increasing disposable incomes, expanding food processing activities, and growing demand for packaged and convenience food products. The region also benefits from favorable agricultural conditions, extensive pulse cultivation capabilities, and strong export activity, enabling Latin America to maintain its position as both a major consumer and an important supplier within the global kidney beans market.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of global kidney bean demand and presents significant long-term growth opportunities. Major importing countries include Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Nigeria, where growing populations and increasing food consumption requirements continue to drive market expansion. Rising awareness of affordable plant-based protein sources, expanding retail infrastructure, and increasing urbanization are supporting stronger consumption across both household and foodservice sectors. Government-led food security initiatives, strategic investments in food supply chains, and efforts to improve nutritional outcomes are further contributing to demand growth. In addition, the region's continued dependence on imported pulses creates substantial opportunities for international exporters, processors, and suppliers seeking to capitalize on expanding consumption and improving distribution networks.

Key Players in the Kidney Beans Market

- Goya Foods

- Bush Brothers & Company

- Bonduelle

- Conagra Brands

- B&G Foods

- Faribault Foods

- AGT Food and Ingredients

- The Scoular Company

- Archer Daniels Midland (ADM)

- Olam Food Ingredients

- SunOpta

- Diefenbaker Spice & Pulse

- BroadGrain Commodities

- Groupe Gelpass

- MTR Foods