Sugar Free Jam Market Size

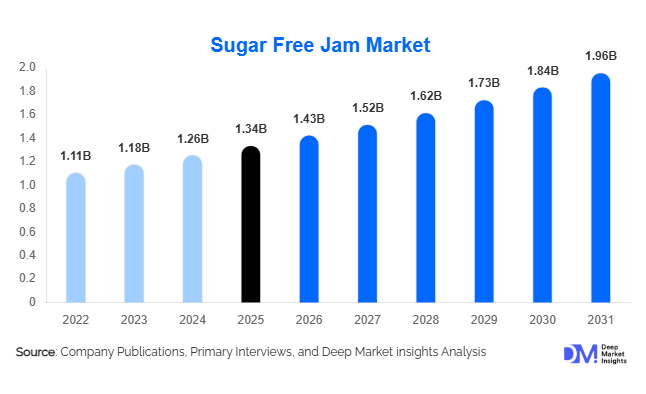

According to Deep Market Insights, the global sugar free jam market size was valued at USD 1.34 billion in 2025 and is projected to grow from USD 1.43 billion in 2026 to reach USD 1.96 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The sugar free jam market growth is primarily driven by rising consumer awareness regarding sugar reduction, increasing prevalence of diabetes and obesity, growing demand for clean-label food products, and continuous innovation in natural sweetener technologies. The market has evolved beyond its traditional diabetic consumer base and is increasingly attracting health-conscious consumers seeking low-calorie breakfast spreads and functional food alternatives. Manufacturers are introducing products formulated with stevia, monk fruit, erythritol, allulose, and other natural sweeteners to address changing dietary preferences while maintaining taste and texture standards comparable to conventional fruit jams.

Key Market Insights

- Fruit-based sugar free jams account for more than 70% of global demand, led by strawberry, mixed berry, blueberry, and raspberry variants.

- Natural sweetener adoption is accelerating globally, with stevia-based products representing the largest share among sugar-free jam formulations.

- North America dominates the global market, supported by high health awareness, established retail infrastructure, and widespread consumer adoption of reduced-sugar foods.

- Asia-Pacific is the fastest-growing regional market, driven by increasing diabetes prevalence, rising disposable incomes, and expanding organized retail channels.

- Premium and organic sugar free jams are gaining significant traction, supported by consumer preference for clean-label and minimally processed food products.

- E-commerce channels are reshaping product accessibility, enabling niche brands and premium manufacturers to reach broader consumer audiences globally.

Sugar Free Jam Market Latest Trends

Natural Sweetener-Based Formulations Becoming Mainstream

The sugar free jam industry is experiencing a major transition from artificial sweeteners toward naturally derived alternatives such as stevia, monk fruit extract, erythritol, and allulose. Consumers increasingly prefer ingredient transparency and products perceived as natural, leading manufacturers to reformulate existing product portfolios. Improvements in sweetener technologies have significantly reduced aftertaste concerns historically associated with sugar substitutes. Leading manufacturers are investing heavily in research and development to create formulations that replicate the taste, mouthfeel, and preservation properties of traditional sugar-based jams. This trend is particularly prominent across North America and Europe, where clean-label purchasing behavior continues to influence food and beverage innovation.

Functional and Wellness-Oriented Jam Products Gaining Popularity

Manufacturers are increasingly positioning sugar free jams as functional nutrition products rather than simple breakfast spreads. New product launches incorporate dietary fiber, antioxidants, probiotics, vitamins, collagen, and plant-based nutrients to appeal to wellness-focused consumers. Keto-friendly, low-carbohydrate, and diabetic-specific formulations are also gaining traction. The convergence of preventive healthcare and personalized nutrition is creating opportunities for premium products that address specific health concerns. As consumers increasingly seek foods that contribute to overall wellness, sugar free jams are evolving into multifunctional products that support weight management, digestive health, and balanced nutrition.

Sugar Free Jam Market Drivers

Rising Global Diabetes and Obesity Rates

The increasing prevalence of diabetes, obesity, and metabolic disorders remains one of the most important drivers of sugar free jam market growth. Consumers diagnosed with diabetes or actively managing sugar intake are seeking healthier alternatives to conventional spreads. Governments, healthcare organizations, and nutrition experts continue to promote sugar reduction strategies, encouraging consumers to adopt lower-sugar food products. As awareness regarding the health impacts of excessive sugar consumption grows, sugar free jams are becoming an attractive substitute across household and foodservice applications.

Growing Consumer Preference for Clean-Label Foods

Consumers increasingly demand products with simple ingredient lists, natural sweeteners, and minimal processing. Clean-label trends have expanded beyond premium food categories and are now influencing mainstream purchasing decisions. Sugar free jam manufacturers are responding by eliminating artificial additives and incorporating fruit-forward recipes supported by natural sweetening systems. The ability to market products as naturally sweetened, preservative-free, and organic has become a significant competitive advantage within the category.

Sugar Free Jam Market Restraints

Higher Manufacturing Costs Compared to Conventional Jam

Natural sweeteners such as monk fruit and allulose remain considerably more expensive than conventional sugar. Additionally, sugar performs multiple functions in jam production, including preservation, texture enhancement, and flavor balancing. Replacing these functionalities requires advanced formulation expertise and often increases production costs. Consequently, sugar free jams typically command premium retail pricing, which can limit adoption in price-sensitive markets.

Challenges Related to Taste and Texture Optimization

Despite significant technological advancements, achieving identical taste and texture characteristics to conventional jam remains challenging. Some sweeteners may introduce aftertastes or alter mouthfeel characteristics. Consumer expectations for traditional fruit spread experiences remain high, requiring continuous investment in formulation technologies. Manufacturers that fail to deliver satisfactory sensory performance may experience lower repeat purchase rates and slower category adoption.

Sugar Free Jam Industry Key Opportunities

Expansion Across Emerging Asia-Pacific Markets

Asia-Pacific represents one of the most significant growth opportunities for sugar free jam manufacturers. Countries such as China, India, Indonesia, Vietnam, and Thailand are witnessing rapid growth in diabetes prevalence alongside increasing disposable incomes and urbanization. Expanding modern retail infrastructure and greater exposure to health-oriented food products are creating favorable conditions for market penetration. Localized fruit flavors and region-specific formulations can further accelerate adoption among first-time consumers. Manufacturers that establish early distribution networks in these markets are likely to gain substantial long-term competitive advantages.

Growth of Functional and Personalized Nutrition Products

The rapid expansion of functional foods presents a compelling opportunity for industry participants. Sugar free jams fortified with probiotics, vitamins, antioxidants, fiber, or protein can address growing demand for preventive healthcare solutions. Personalized nutrition trends are encouraging consumers to seek products aligned with specific dietary objectives such as weight management, digestive health, sports nutrition, and diabetic support. Premium functional formulations typically command higher margins and strengthen brand differentiation. The integration of nutritional benefits beyond sugar reduction is expected to become a major growth avenue over the coming decade.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.34 Billion |

| Market Size in 2026 | USD 1.43 Billion |

| Market Size in 2031 | USD 1.96 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fruit-based sugar free jams dominated the global market and accounted for approximately 72% of total revenue in 2025. The segment’s leadership is primarily driven by strong consumer familiarity with fruit preserves, widespread breakfast consumption patterns, and the ability of manufacturers to offer a broad range of flavors that closely replicate traditional jams without added sugar. Strawberry, mixed berry, blueberry, raspberry, and other fruit-based variants continue to maintain strong demand due to their established presence in retail channels and compatibility with health-conscious dietary preferences. The growing consumer focus on reducing sugar intake without compromising taste has further strengthened demand for fruit-derived sugar free spreads. In addition, manufacturers continue to introduce products with enhanced nutritional profiles, including higher fruit content and clean-label formulations, which support sustained segment growth.Specialty and premium sugar free jams represent the fastest-growing product category within the market. Demand for organic, keto-friendly, probiotic-enriched, high-fiber, and functional fruit spreads is accelerating as consumers increasingly seek products that deliver both nutritional benefits and lifestyle alignment. Rising interest in personalized nutrition, digestive health, weight management, and natural ingredients has encouraged manufacturers to develop value-added offerings targeted at wellness-oriented consumers. Premium products also benefit from growing consumer willingness to pay higher prices for products perceived as healthier, more natural, and minimally processed.Vegetable-based sugar free jams remain a relatively niche category but continue to gain attention among health-conscious consumers seeking innovative flavor experiences and differentiated nutritional benefits. Manufacturers are increasingly experimenting with vegetable-fruit blends and functional ingredients to expand product portfolios and appeal to consumers looking for unique alternatives to conventional fruit spreads.

Sweetener Type Insights

Stevia-based products accounted for approximately 32% of the global market in 2025, making stevia the leading sweetener category. The segment’s dominance is supported by growing consumer preference for naturally derived ingredients, increasing awareness regarding sugar reduction, and strong regulatory acceptance across major markets. Stevia’s zero-calorie profile, plant-based origin, and compatibility with clean-label product positioning have encouraged widespread adoption among manufacturers seeking to meet evolving consumer expectations. The increasing prevalence of diabetes, obesity, and other lifestyle-related health conditions has further accelerated demand for stevia-sweetened products as consumers seek healthier alternatives to traditional sweeteners.Monk fruit and erythritol-based formulations are experiencing rapid growth due to their favorable taste profiles and ability to complement clean-label product development strategies. Manufacturers increasingly utilize these sweeteners individually or in combination to reduce aftertaste concerns while maintaining sweetness intensity and product functionality. Consumer demand for natural sweeteners that closely mimic the taste of sugar is expected to support continued expansion of these categories.Artificial sweeteners continue to maintain relevance in cost-sensitive product segments and emerging markets where affordability remains a critical purchasing factor. However, their overall market share is gradually declining as consumers increasingly favor naturally sourced alternatives. Hybrid sweetener systems that combine natural and artificial sweeteners are also gaining traction as manufacturers seek to optimize taste, texture, shelf stability, and production costs while meeting diverse consumer preferences.

Packaging Insights

Glass jars remained the dominant packaging format, accounting for approximately 58% of global sales in 2025. The leading position of this segment is driven by strong consumer perceptions regarding product quality, freshness, purity, and premium value. Glass packaging provides excellent product protection while preserving flavor, texture, and shelf life, making it particularly attractive for premium, organic, and clean-label brands. Consumers also increasingly associate glass with sustainability and recyclability, further supporting its continued dominance in developed markets.Plastic tubs and squeeze bottles continue gaining popularity due to their convenience, lightweight nature, lower transportation costs, and reduced breakage risks. These formats are particularly attractive for family-oriented households and consumers seeking ease of use during daily consumption. Manufacturers are increasingly introducing innovative dispensing solutions and recyclable plastic materials to improve functionality while addressing sustainability concerns.Single-serve sachets and portion-controlled packs are emerging as high-growth packaging formats, supported by increasing demand from hospitality establishments, foodservice operators, institutional catering services, and on-the-go consumers. Growing interest in portion management and convenience-oriented consumption patterns is expected to further accelerate adoption. Across all packaging categories, sustainability initiatives are driving investments in recyclable, reusable, and lightweight packaging solutions aimed at reducing environmental impact and improving supply chain efficiency.

Distribution Channel Insights

Hypermarkets and supermarkets remained the largest distribution channel, accounting for approximately 47% of global sales in 2025. The segment’s leadership is supported by extensive product availability, competitive pricing strategies, promotional activities, and the ability of consumers to compare multiple brands within a single shopping destination. Strong retail penetration and established supply chain networks continue to make supermarkets the preferred purchasing channel for sugar free jams across both developed and emerging markets.Health food stores and specialty grocery outlets play a significant role in supporting premium and functional product sales, particularly for organic, keto-friendly, and naturally sweetened formulations. Consumers seeking specialized dietary products often rely on these retail channels due to their curated product assortments and focus on health-oriented offerings.E-commerce represents the fastest-growing distribution channel, driven by increasing online grocery adoption, expanding digital retail ecosystems, and growing consumer preference for convenient purchasing experiences. Online platforms enable niche and emerging brands to directly engage with consumers while providing broader product visibility and accessibility. The rapid expansion of subscription-based food delivery services, direct-to-consumer business models, and quick-commerce platforms is further accelerating market penetration and supporting future growth across urban and suburban markets worldwide.

Consumer Category Insights

General health-conscious consumers represented the largest customer segment, contributing approximately 41% of total market demand in 2025. The segment’s leadership is primarily driven by growing awareness regarding the adverse health effects of excessive sugar consumption and increasing consumer interest in preventive nutrition. Consumers are increasingly incorporating reduced-sugar food products into their daily diets as part of broader wellness and healthy lifestyle initiatives. The expanding availability of sugar free jams across mainstream retail channels has also contributed to wider consumer adoption beyond traditional niche markets.Although diabetic consumers remain a core target audience, the market has evolved significantly as mainstream consumers increasingly seek healthier alternatives to conventional sugar-rich spreads. Rising prevalence of diabetes and prediabetes globally continues to support demand within this consumer group.Weight management consumers, keto followers, fitness enthusiasts, and individuals pursuing low-carbohydrate dietary regimens are increasingly adopting sugar free jams due to their lower calorie content and compatibility with specialized nutrition programs. The diversification of the consumer base has transformed sugar free jams from a medically driven dietary product into a broader lifestyle-oriented category with mass-market appeal.

Application Insights

Household retail consumption accounted for approximately 52% of global demand in 2025, making it the leading application segment. Growth is primarily driven by the widespread use of sugar free jams during breakfast, snacking occasions, and home meal preparation. Increasing consumer preference for healthier food choices, combined with rising awareness regarding sugar reduction, continues to strengthen demand within the household segment. The growing popularity of home-based wellness routines and healthier eating habits has further reinforced segment leadership.Bakery applications represent one of the fastest-growing industrial use categories. Bakery manufacturers are increasingly incorporating sugar free fruit fillings into pastries, cakes, cookies, muffins, and other baked goods to address consumer demand for healthier indulgence products. Rising demand for reduced-sugar bakery products and clean-label formulations is expected to support sustained segment expansion.Dairy manufacturers continue expanding the utilization of sugar free jams in yogurt products, dairy desserts, flavored milk beverages, and functional dairy applications. Functional foods, frozen desserts, nutritional snacks, and ready-to-eat products are emerging application areas that are expected to contribute significantly to future market growth. Foodservice operators, including hotels, restaurants, cafés, and catering establishments, are also expanding sugar free menu offerings to accommodate evolving consumer dietary preferences and health-conscious consumption patterns.

End-Use Industry Insights

Household consumption remained the largest end-use segment, accounting for approximately 49% of global market revenue in 2025. The segment’s dominance is supported by growing consumer demand for healthier pantry staples, rising awareness regarding sugar reduction, and increasing incorporation of sugar free products into everyday diets. Strong retail availability, product affordability, and expanding flavor portfolios have further contributed to widespread household adoption.The bakery industry is emerging as the fastest-growing end-use sector, driven by increasing demand for healthier baked goods, reduced-sugar formulations, and clean-label ingredients. Food manufacturers are actively reformulating products to align with evolving consumer preferences while complying with stricter nutritional standards in several markets.The dairy industry continues to generate substantial demand through yogurt, dessert, and flavored dairy applications, while the functional food industry is becoming an increasingly important consumer of sugar free fruit spreads due to growing interest in health-enhancing ingredients. Rising global trade in processed food products, continuous product innovation, and increasing demand for healthier ingredient solutions are expected to support sustained growth across industrial end-use sectors over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Sugar Free Jam Market Segmentations

By Product Type

- Fruit-Based Sugar Free Jam

- Vegetable-Based Sugar Free Jam

- Specialty & Premium Sugar Free Jam

By Sweetener Type

- Natural Sweeteners

- Artificial Sweeteners

- Hybrid Sweetener Formulations

By Packaging Format

- Glass Jars

- Plastic Jars/Tubs

- Squeeze Bottles

- Sachets/Portion Packs

- Flexible Pouches

By Distribution Channel

- Hypermarkets & Supermarkets

- Convenience Stores

- Health Food Stores

- Specialty Grocery Stores

- Pharmacy & Drug Stores

- Brand-Owned E-commerce

- Third-Party E-commerce Marketplaces

- Quick Commerce Platforms

- Subscription-Based Food Delivery

- Institutional Distribution

By Consumer Category

- Diabetic Consumers

- Weight Management Consumers

- Keto & Low-Carb Consumers

- Fitness & Wellness Consumers

- General Health-Conscious Consumers

- Pediatric/Family Consumers

Regional Insights

North America

North America accounted for approximately 34% of the global sugar free jam market in 2025, making it the largest regional market. The United States alone represents nearly 27% of global demand, supported by strong health awareness, high prevalence of diabetes and obesity, premium food consumption trends, and extensive retail penetration. Consumers across the region increasingly prioritize low-sugar, clean-label, and functional food products, creating favorable conditions for market expansion. The growing popularity of ketogenic, low-carbohydrate, and weight-management diets continues to stimulate demand for sugar free fruit spreads. In addition, ongoing innovation in natural sweeteners, organic food products, and wellness-focused nutrition solutions supports sustained market growth. Canada is also experiencing increasing demand for naturally sweetened and organic products, further contributing to regional development.

Europe

Europe represented approximately 31% of global revenue in 2025, making it the second-largest regional market. Germany, the United Kingdom, France, Italy, Spain, and the Netherlands remain major demand centers. The region benefits from a mature health and wellness food industry, strong consumer preference for reduced-sugar products, and widespread acceptance of organic and clean-label foods. One of the primary growth drivers is the implementation of government-led sugar reduction initiatives and nutritional labeling regulations aimed at improving public health outcomes. Growing awareness of lifestyle-related diseases and increasing consumer focus on preventive healthcare continue to encourage the adoption of sugar free alternatives. Germany remains the largest European market due to its established breakfast culture, high fruit spread consumption, and strong retail infrastructure supporting premium food products.

Asia-Pacific

Asia-Pacific accounted for approximately 22% of global demand in 2025 and is expected to register the highest growth rate through 2031. China, India, Japan, South Korea, and Australia are leading regional markets. Rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing health consciousness are significantly influencing purchasing behavior across the region. The growing prevalence of diabetes and obesity has accelerated consumer demand for reduced-sugar food products, while increasing exposure to Western-style breakfast habits continues to expand jam consumption. The rapid growth of modern retail formats, e-commerce platforms, and premium packaged food categories further supports market development. India is expected to emerge as the fastest-growing national market, driven by expanding organized retail networks, growing wellness awareness, rising demand for premium packaged foods, and increasing adoption of healthier dietary choices among younger consumers.

Latin America

Latin America accounted for approximately 7% of global market revenue in 2025. Brazil and Mexico dominate regional demand due to growing middle-class populations, improving purchasing power, and increasing exposure to healthier packaged food products. Rising awareness regarding diabetes management and healthy eating habits is encouraging consumers to seek reduced-sugar alternatives across various food categories. Retail modernization, expansion of supermarket chains, and growing penetration of international food brands are improving product accessibility throughout the region. In addition, local manufacturers are increasingly introducing sugar free product lines to capitalize on evolving consumer preferences and rising demand for wellness-oriented foods.

Middle East & Africa

The Middle East and Africa region accounted for approximately 6% of global demand in 2025. The United Arab Emirates, Saudi Arabia, South Africa, and Egypt are among the key markets driving regional growth. Rising awareness regarding diabetes prevention and management, increasing healthcare expenditure, and growing adoption of healthier lifestyles are encouraging consumers to reduce sugar consumption. The region is also benefiting from increasing imports of premium food products, expanding modern retail infrastructure, and rising urbanization rates. Growing expatriate populations, changing dietary patterns, and increasing demand for premium and functional food products are creating additional growth opportunities. Although the market remains relatively nascent compared to developed regions, improving consumer awareness and continued investments in retail and food distribution networks are expected to support long-term market expansion.

Key Players in the Sugar Free Jam Market

- Hero Group

- The J.M. Smucker Company

- Andros Group

- Zuegg Group

- AGRANA Beteiligungs AG

- Frulact

- Zentis GmbH

- Valio

- Puratos

- Döhler Group

- Tree Top Inc.

- Fourayes

- Fresh Food Industries

- BINA

- Ingredion Incorporated