Stuffed Pasta Market Size

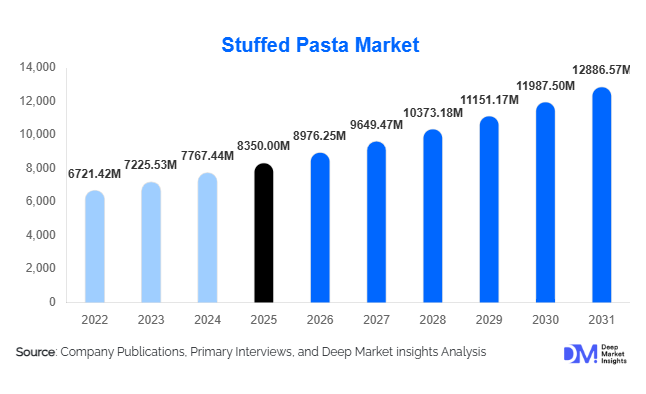

According to Deep Market Insights, the global stuffed pasta market size was valued at USD 8,350 million in 2025 and is projected to grow from USD 8,976.25 million in 2026 to reach USD 12,886.57 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The stuffed pasta market growth is primarily driven by increasing demand for convenience foods, rising consumer inclination toward premium and gourmet meal experiences, and expanding global adoption of Italian cuisine across both developed and emerging economies. Technological advancements in freezing, packaging, and processing have significantly improved product shelf life and quality, further accelerating consumption across retail and foodservice channels.

Key Market Insights

- Frozen stuffed pasta dominates the market, supported by extended shelf life, improved freezing technologies, and rising demand for ready-to-cook meals.

- Retail distribution channels lead globally, particularly supermarkets and hypermarkets, due to wide product availability and strong promotional activities.

- Europe holds the largest market share, driven by traditional consumption patterns and strong production capabilities in Italy, Germany, and France.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable income, and increasing exposure to Western cuisines.

- Cheese-based fillings remain the most popular segment, owing to their universal appeal and compatibility with vegetarian diets.

- Plant-based stuffed pasta is emerging as a high-growth segment, supported by growing vegan and health-conscious consumer trends.

What are the latest trends in the stuffed pasta market?

Rise of Plant-Based and Functional Fillings

The increasing shift toward plant-based diets is significantly influencing product innovation in the stuffed pasta market. Manufacturers are introducing vegan fillings such as lentil-based protein, tofu ricotta, and plant-derived cheese alternatives to cater to health-conscious and environmentally aware consumers. Functional ingredients such as high-protein blends, fiber-rich vegetables, and gluten-free formulations are also gaining traction. This trend is particularly strong in North America and Europe, where consumers actively seek healthier meal alternatives without compromising on taste. The growing popularity of flexitarian diets is further expanding the addressable market for plant-based stuffed pasta products.

Premiumization and Gourmet Offerings

Premium stuffed pasta products are witnessing robust demand as consumers increasingly seek restaurant-quality experiences at home. Gourmet variants featuring truffle, seafood, artisanal cheeses, and region-specific ingredients are becoming mainstream in retail shelves. Companies are investing in high-quality raw materials and innovative recipes to differentiate their offerings. Premium packaging and branding strategies are also being employed to position these products as high-value items. This trend is particularly evident in urban markets, where consumers are willing to pay higher prices for convenience combined with superior taste and authenticity.

What are the key drivers in the stuffed pasta market?

Growing Demand for Convenience Foods

The rise in dual-income households and busy urban lifestyles has significantly increased demand for convenient meal solutions. Stuffed pasta products, particularly frozen and refrigerated variants, offer quick preparation times and minimal cooking effort, making them highly appealing to time-constrained consumers. The expansion of modern retail and online grocery platforms has further enhanced product accessibility, supporting sustained growth in this segment.

Globalization of Culinary Preferences

Increasing exposure to international cuisines through travel, media, and digital platforms has expanded the popularity of Italian food globally. Stuffed pasta varieties such as ravioli and tortellini are now widely consumed across regions beyond Europe. Foodservice operators are incorporating these dishes into menus, while retail brands are localizing flavors to suit regional tastes, further driving market penetration.

What are the restraints for the global market?

High Production and Cold Chain Costs

Stuffed pasta production requires specialized machinery, quality ingredients, and advanced preservation techniques, particularly for fresh and frozen products. Additionally, maintaining cold chain logistics increases operational costs, which can impact profitability, especially for smaller manufacturers. These factors may limit market expansion in price-sensitive regions.

Health Perception Challenges

Pasta is often perceived as a high-carbohydrate food, which may deter health-conscious consumers. Although manufacturers are introducing whole-grain, gluten-free, and low-carb variants, widespread consumer perception remains a challenge. Addressing these concerns through product innovation and marketing will be critical for sustained growth.

What are the key opportunities in the stuffed pasta industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific and Latin America present significant growth opportunities due to rising disposable incomes, urbanization, and increasing adoption of Western dietary habits. Localizing flavors and expanding distribution networks in countries such as India, China, and Brazil can help companies capture untapped demand. Improved cold chain infrastructure in these regions is also facilitating the distribution of frozen and refrigerated products.

E-commerce and Direct-to-Consumer Growth

The rapid expansion of online grocery platforms and direct-to-consumer channels is opening new avenues for market players. Brands can leverage digital platforms to offer customized products, subscription meal kits, and premium stuffed pasta options. This not only enhances consumer engagement but also improves margins by reducing dependency on intermediaries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8350.00 Million |

| Market Size in 2026 | USD 8976.25 Million |

| Market Size in 2031 | USD 12886.57 Million |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global stuffed pasta market demonstrates a clear dominance of ravioli as the leading product type, accounting for approximately 32% of the global market share in 2025. This leadership position is primarily driven by ravioli’s unmatched versatility, which allows manufacturers and foodservice providers to experiment with a wide range of fillings including cheese, meat, vegetables, and increasingly plant-based alternatives. The product’s strong cultural association with traditional Italian cuisine, combined with its adaptability to modern culinary trends, has significantly enhanced its global appeal. Ravioli is widely available across frozen, fresh, and dried formats, making it accessible to a broad consumer base ranging from budget-conscious households to premium gourmet buyers. The leading driver for this segment is its cross-category adaptability, enabling it to cater to diverse taste preferences and consumption occasions, from quick meals to fine dining experiences.Tortellini represents another important segment within the stuffed pasta category, particularly in premium and artisanal product lines. Its ring-shaped structure and rich filling combinations make it a preferred choice among consumers seeking authentic and indulgent meal options. The demand for tortellini is further supported by the growing trend of premiumization in the global food industry, where consumers are willing to pay higher prices for high-quality, authentic, and aesthetically appealing products. Meanwhile, cannelloni and manicotti maintain strong demand in the foodservice sector due to their suitability for baked dishes and large-portion servings, making them ideal for restaurants, catering services, and institutional kitchens. These products benefit from their ability to be prepared in bulk while maintaining consistent taste and texture.In addition, specialty stuffed pasta types such as agnolotti and cappelletti are gaining traction, particularly in niche and gourmet segments. These products are often associated with regional Italian culinary traditions and are increasingly being introduced in international markets through specialty stores and high-end restaurants. The growing consumer inclination toward authentic and region-specific cuisines is a major factor contributing to the expansion of this segment. Furthermore, innovations in product development, including gluten-free and organic variants, are enhancing the appeal of specialty stuffed pasta, enabling manufacturers to tap into health-conscious and dietary-specific consumer groups. Overall, the product type landscape is characterized by a balance between mass-market staples and premium offerings, with innovation and authenticity acting as key growth enablers.

Filling Type Insights

Filling type plays a critical role in shaping consumer preferences in the stuffed pasta market, with cheese-based fillings emerging as the dominant segment, accounting for approximately 38% of the total market share. The leading driver for this segment is its universal appeal, as cheese-based fillings are widely accepted across different cultures, age groups, and dietary preferences. These fillings are particularly popular among vegetarian consumers, making them a staple option in both developed and emerging markets. The availability of diverse cheese varieties such as ricotta, mozzarella, parmesan, and blended cheeses further enhances product differentiation and consumer engagement. Additionally, cheese-based fillings align well with comfort food trends, which continue to drive demand globally.Vegetable-based fillings are witnessing robust growth, driven by increasing health awareness and the rising popularity of balanced diets. Consumers are increasingly seeking nutrient-rich and low-calorie food options, which has led to the incorporation of ingredients such as spinach, mushrooms, pumpkin, and mixed vegetables in stuffed pasta products. This segment benefits from its alignment with clean-label trends, as many vegetable-based fillings are perceived as natural and minimally processed.Plant-based fillings are emerging as a high-growth segment, supported by the global shift toward vegan and sustainable diets. The increasing adoption of plant-based lifestyles, particularly among younger consumers, is driving innovation in this category. Manufacturers are investing in the development of plant-based protein alternatives that replicate the taste and texture of traditional meat fillings, thereby expanding the appeal of stuffed pasta to a broader audience. The growing availability of these products in mainstream retail channels is further accelerating their adoption. Overall, the filling type segment is evolving rapidly, with health, sustainability, and innovation serving as key growth drivers.

Processing Type Insights

Processing type is a crucial determinant of product accessibility and consumer convenience in the stuffed pasta market. Frozen stuffed pasta dominates this segment, accounting for nearly 41% of the global market share. The leading driver for this segment is the increasing demand for convenience foods, as frozen products offer extended shelf life, easy storage, and quick preparation. Technological advancements in freezing methods, such as individually quick frozen (IQF) techniques, have significantly improved product quality by preserving taste, texture, and nutritional value. This has enhanced consumer confidence in frozen stuffed pasta, making it a preferred choice for busy households and working professionals.Fresh and refrigerated stuffed pasta products occupy a strong position in the premium segment, where consumers prioritize quality, authenticity, and freshness. These products are often perceived as superior in taste and texture compared to their frozen and dried counterparts. The growth of this segment is driven by the increasing availability of fresh pasta in supermarkets, specialty stores, and online platforms, as well as the rising popularity of home cooking. Additionally, the expansion of cold chain logistics has enabled manufacturers to distribute fresh products more efficiently across regions.Dried stuffed pasta, while representing a smaller share of the market, continues to play an important role in price-sensitive regions. These products offer the advantage of long shelf life without the need for refrigeration, making them suitable for markets with limited cold storage infrastructure. The affordability and ease of transportation associated with dried stuffed pasta contribute to its sustained demand, particularly in emerging economies. Furthermore, ongoing product innovations aimed at improving the quality and variety of dried stuffed pasta are expected to support its growth in the coming years. Overall, the processing type segment reflects a balance between convenience, quality, and affordability, with each category catering to specific consumer needs.

Distribution Channel Insights

Distribution channels play a pivotal role in determining market reach and consumer accessibility in the stuffed pasta market. Retail channels dominate the market, accounting for approximately 55% of total sales. The leading driver for this segment is the widespread availability of stuffed pasta products across supermarkets and hypermarkets, which offer consumers a wide range of options in terms of product type, brand, and price. These retail formats benefit from strong supply chain networks and strategic product placements, which enhance visibility and drive impulse purchases. In addition, private label offerings by major retail chains are contributing to market growth by providing cost-effective alternatives to branded products.Online retail is emerging as a rapidly growing distribution channel, driven by the increasing penetration of e-commerce platforms and changing consumer shopping behaviors. The convenience of online shopping, coupled with the availability of detailed product information and home delivery services, has made this channel particularly attractive to urban consumers. The COVID-19 pandemic further accelerated the adoption of online grocery shopping, a trend that continues to influence purchasing patterns. Manufacturers are increasingly partnering with e-commerce platforms to expand their digital presence and reach a wider audience.Foodservice channels, including restaurants, hotels, and catering services, also play a significant role in the stuffed pasta market. These channels are particularly important for premium and bulk purchases, as they cater to consumers seeking high-quality dining experiences. The growth of the global hospitality industry, along with the increasing popularity of Italian cuisine, is driving demand in this segment. Additionally, the introduction of innovative menu offerings and the use of stuffed pasta in fusion cuisines are further enhancing its appeal in the foodservice sector. Overall, the distribution landscape is evolving with the integration of traditional and digital channels, creating new growth opportunities for market players.

Explore more data points, trends and opportunities Download Free Sample Report

Stuffed Pasta Market Segmentations

By Product Type

- Ravioli

- Tortellini

- Cannelloni

- Agnolotti

- Cappelletti

- Manicotti

- Others

By Filling Type

- Cheese-Based Fillings

- Meat-Based Fillings

- Vegetable-Based Fillings

- Seafood-Based Fillings

- Plant-Based/Vegan Fillings

By Processing Type

- Fresh Stuffed Pasta

- Frozen Stuffed Pasta

- Dried Stuffed Pasta

- Refrigerated Ready-to-Cook Stuffed Pasta

By Distribution Channel

- Retail

- Foodservice

By Price Range

- Economy Segment

- Mid-Range Segment

- Premium/Gourmet Segment

Regional Insights

Europe

Europe remains the largest regional market for stuffed pasta, accounting for approximately 38% of the global market share in 2025. The region’s dominance is rooted in its deep cultural connection to pasta, particularly in countries such as Italy, which serves as both a major producer and exporter. The leading driver for regional growth is the strong tradition of pasta consumption combined with continuous product innovation. Italy’s well-established manufacturing base and global reputation for high-quality pasta products contribute significantly to market expansion. In addition, countries such as Germany and France are witnessing strong demand due to their advanced retail infrastructure and high levels of consumer awareness. The presence of premium and artisanal product offerings further supports market growth, as consumers increasingly seek authentic and high-quality food experiences. Furthermore, the growing trend of organic and clean-label products is influencing purchasing decisions across the region.

North America

North America accounts for approximately 28% of the global stuffed pasta market, with the United States leading regional growth. The primary driver in this region is the high demand for convenience foods, supported by busy lifestyles and a strong preference for ready-to-cook meal solutions. The well-developed retail infrastructure, including supermarkets, hypermarkets, and online platforms, ensures widespread product availability. In addition, the increasing popularity of premium and gourmet food products is driving demand for high-quality stuffed pasta variants. Canada also contributes to regional growth, particularly in the frozen segment, where consumers value convenience and long shelf life. The influence of multicultural cuisines and the growing interest in international flavors are further expanding the market in North America.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for stuffed pasta, with a projected CAGR exceeding 9%. The leading driver for growth in this region is rapid urbanization, which is accompanied by rising disposable incomes and changing dietary habits. Countries such as China, India, and Japan are witnessing increasing adoption of Western cuisines, including pasta, driven by globalization and the expansion of international food chains. The growth of modern retail formats and e-commerce platforms is significantly enhancing product accessibility, particularly in urban areas. Additionally, the younger population’s openness to experimenting with new cuisines is creating a favorable environment for market expansion. Manufacturers are also introducing localized flavors and product variations to cater to regional tastes, further supporting growth in the Asia-Pacific market.

Latin America

Latin America is experiencing steady growth in the stuffed pasta market, led by countries such as Brazil and Argentina. The primary driver for regional growth is the strong cultural affinity for pasta, which is deeply ingrained in local cuisines. The increasing availability of packaged and processed food products is further supporting market expansion, as consumers seek convenient meal options. Urbanization and the growth of the middle-class population are contributing to higher disposable incomes, enabling consumers to spend more on premium and value-added food products. In addition, the expansion of retail and foodservice sectors is enhancing product accessibility and visibility across the region.

Middle East & Africa

The Middle East & Africa region is witnessing gradual growth in the stuffed pasta market, with key contributions from countries such as the United Arab Emirates and Saudi Arabia. The leading driver for growth in this region is the increasing influence of international cuisines, supported by a large expatriate population and a thriving tourism industry. The expansion of modern retail chains and foodservice outlets is improving product availability and accessibility. Additionally, rising urbanization and changing lifestyles are driving demand for convenient and ready-to-cook food products. While the market is still in a developing stage, ongoing investments in retail infrastructure and the growing popularity of global food trends are expected to create significant growth opportunities in the coming years.

Key Players in the Stuffed Pasta Market

- Barilla Group

- Nestlé S.A.

- Giovanni Rana

- Ebro Foods S.A.

- General Mills, Inc.

- Conagra Brands, Inc.

- TreeHouse Foods, Inc.

- Buitoni Food Company

- Pasta Zara S.p.A.

- La Molisana S.p.A.

- Premier Foods plc

- Amy’s Kitchen, Inc.

- Kraft Heinz Company

- Armanino Foods of Distinction

- Cucina Fresca Gourmet Foods