Spicy Biscuits Market Size

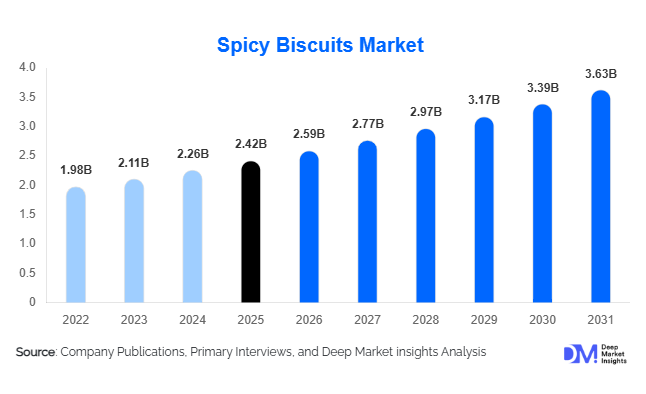

According to Deep Market Insights, the global spicy biscuits market size was valued at USD 2.42 billion in 2025 and is projected to grow from USD 2.59 billion in 2026 to reach USD 3.63 billion by 2031, expanding at a CAGR of 7.0% during the forecast period (2026–2031). The spicy biscuits market growth is being driven by increasing consumer preference for savory snacks, rising demand for ethnic and bold flavor profiles, expanding urban lifestyles, and continuous innovation in packaged snack foods. The market has evolved beyond traditional savory biscuits, with manufacturers introducing premium, health-oriented, and regionally inspired spicy biscuit varieties that cater to changing consumer tastes. Growing penetration of modern retail formats, rising disposable incomes in emerging economies, and the rapid expansion of e-commerce channels are further supporting market growth globally.

Key Market Insights

- Savory spicy biscuits account for nearly 72% of global market demand, significantly outperforming sweet-spicy variants due to wider consumer acceptance and greater product variety.

- Asia-Pacific dominates the global market, accounting for approximately 42% of total demand, led by India, China, Indonesia, Thailand, and Vietnam.

- Health-focused spicy biscuits are gaining traction, with manufacturers introducing wholegrain, high-fiber, protein-enriched, and reduced-sodium formulations.

- Supermarkets and hypermarkets remain the leading distribution channel, contributing nearly 35% of global sales due to extensive product visibility and consumer accessibility.

- E-commerce is emerging as the fastest-growing sales channel, enabling premium, artisanal, and specialty brands to reach broader consumer segments.

- Flavor innovation remains a key competitive strategy, with manufacturers launching products inspired by Indian masala, Korean chili, Mexican jalapeño, Thai chili-lime, and Middle Eastern spice blends.

Spicy Biscuits Market Latest Trends

Premiumization and Health-Focused Product Innovation

The spicy biscuits industry is witnessing a strong shift toward premium and health-oriented products. Consumers increasingly seek snacks that deliver both indulgent flavors and nutritional benefits. In response, manufacturers are launching spicy biscuits made with multigrain flour, whole wheat, millet, oats, seeds, and plant proteins. Reduced-sodium and clean-label formulations are also gaining popularity as health-conscious consumers scrutinize ingredient lists more closely. Premium spicy biscuit offerings featuring gourmet spice blends, artisanal ingredients, and innovative packaging formats are commanding higher retail prices and generating stronger profit margins. This trend is particularly visible in North America, Europe, and urban Asia-Pacific markets where consumers are willing to pay a premium for differentiated snack experiences.

Growing Popularity of Ethnic and Regional Flavors

Globalization of food preferences is accelerating demand for ethnic flavor profiles across the spicy biscuits category. Manufacturers are increasingly introducing products inspired by regional cuisines, including Indian masala, peri-peri, Sichuan pepper, Korean gochujang, Mexican chili, and Middle Eastern spice combinations. Consumers are actively seeking authentic flavor experiences, encouraging brands to diversify product portfolios. Limited-edition launches, seasonal flavors, and region-specific product offerings are becoming important growth strategies. The growing influence of international travel, food content on social media, and multicultural consumer populations is further contributing to demand for globally inspired spicy biscuit products.

Spicy Biscuits Market Drivers

Rising Demand for Savory Snacking

Consumer snacking habits have undergone significant transformation over the past decade, with savory snacks increasingly gaining preference over traditional sweet biscuits and confectionery products. Busy lifestyles, urbanization, and increased consumption between meals are driving demand for convenient savory snacks. Spicy biscuits offer a unique combination of flavor, portability, and shelf stability, making them highly attractive to modern consumers. The trend is particularly pronounced among younger consumers seeking flavorful alternatives to conventional snacks.

Expansion of Organized Retail and E-Commerce

The growth of supermarkets, hypermarkets, convenience stores, and digital grocery platforms has significantly enhanced product availability across developed and emerging markets. Organized retail formats provide manufacturers with greater shelf visibility and promotional opportunities. Simultaneously, e-commerce platforms enable specialty and premium brands to access consumers directly, expanding market reach and improving product discovery. Online sales channels are proving particularly valuable for niche spicy biscuit brands introducing innovative flavors and premium formulations.

Continuous Flavor Innovation and Product Diversification

Manufacturers continue investing heavily in research and development to create unique flavor combinations that differentiate products in an increasingly competitive market. New product launches featuring regional spices, fusion flavors, cheese-spice combinations, and health-focused ingredients are attracting consumer attention. Frequent product innovation helps stimulate repeat purchases while allowing brands to address evolving consumer preferences across different demographic groups.

Spicy Biscuits Market Restraints

Health Concerns Related to Sodium and Processed Ingredients

Many conventional spicy biscuits contain relatively high levels of sodium, refined flour, saturated fats, and artificial flavor enhancers. Growing consumer awareness regarding cardiovascular health, obesity, and dietary quality may limit consumption among health-conscious demographics. Manufacturers must continue reformulating products to balance taste with nutritional value while maintaining affordability.

Volatility in Raw Material Prices

The industry remains highly sensitive to fluctuations in the prices of wheat flour, edible oils, dairy ingredients, spices, and packaging materials. Supply chain disruptions, adverse weather conditions, and agricultural commodity inflation can significantly impact production costs and profit margins. Sustained cost pressures may force manufacturers to implement retail price increases, potentially affecting demand in price-sensitive markets.

Spicy Biscuits Industry Key Opportunities

Expansion of Functional and Better-for-You Spicy Biscuits

The growing global healthy-snacking market presents substantial opportunities for manufacturers to introduce functional spicy biscuits incorporating ingredients such as protein isolates, dietary fiber, probiotics, whole grains, and ancient cereals. Products positioned around digestive health, weight management, and clean-label nutrition are expected to generate premium pricing opportunities. Companies successfully combining strong flavor profiles with health benefits are likely to capture significant market share during the forecast period.

Emerging Market Expansion and Export Growth

Rapid urbanization, rising incomes, and increasing packaged food consumption across Asia, Africa, Latin America, and the Middle East create attractive growth opportunities. Countries including India, Indonesia, Vietnam, Saudi Arabia, Nigeria, and Mexico are witnessing strong demand for savory snack products. Export-oriented manufacturers can leverage regional flavor expertise to expand internationally, particularly within diaspora communities and multicultural consumer segments. Investments in local manufacturing facilities and distribution networks are expected to accelerate market penetration in high-growth regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.42 Billion |

| Market Size in 2026 | USD 2.59 Billion |

| Market Size in 2031 | USD 3.63 Billion |

| CAGR | 7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The savory spicy biscuits segment dominates the global spicy biscuits market, accounting for approximately 72% of total revenue in 2025 and maintaining its position as the leading product category throughout the forecast period. The segment’s leadership is driven by strong consumer familiarity, frequent consumption occasions, broad flavor versatility, and deep integration into everyday snacking habits across both developed and emerging markets. Popular product varieties include masala biscuits, chili biscuits, pepper biscuits, curry-flavored biscuits, herb-and-spice blends, and cheese-spice combinations that appeal to consumers seeking flavorful savory alternatives to traditional sweet biscuits. The widespread availability of these products across retail channels, combined with continuous flavor innovation and regional customization, has further strengthened segment growth. In Asia-Pacific, where spicy flavors are deeply rooted in local food cultures, manufacturers continue to introduce innovative formulations that cater to evolving consumer preferences, supporting sustained demand expansion.Sweet-spicy biscuits represent a smaller but increasingly attractive category within the market. Products such as ginger-spice biscuits, cinnamon-spice biscuits, chili-chocolate variants, and fusion-flavored offerings are gaining traction among younger consumers and premium snack buyers seeking differentiated taste experiences. Rising consumer interest in flavor experimentation, international cuisines, and indulgent snacking is encouraging manufacturers to expand their sweet-spicy portfolios. While the segment currently accounts for a smaller share of overall revenue, its growth potential remains significant due to increasing product innovation, premium positioning strategies, and growing acceptance of unconventional flavor combinations across global markets.

Ingredient Positioning Insights

Conventional spicy biscuits accounted for approximately 67% of global market demand in 2025, making them the largest ingredient-positioning segment. The segment’s dominance is primarily attributed to its affordability, extensive product availability, established consumer trust, and strong penetration across both organized and traditional retail channels. Conventional formulations continue to appeal to mass-market consumers due to competitive pricing and widespread accessibility, particularly in emerging economies where value-oriented purchasing behavior remains a key market characteristic. Large-scale manufacturing efficiencies and broad distribution networks further support the segment’s leadership position.However, health-oriented spicy biscuits are emerging as the fastest-growing category within the market. Organic, gluten-free, wholegrain, multigrain, protein-enriched, high-fiber, reduced-sodium, and clean-label variants are witnessing accelerated adoption as consumers increasingly prioritize wellness without sacrificing flavor. Growing awareness regarding nutrition, digestive health, ingredient transparency, and balanced snacking habits is encouraging demand for products that combine functional benefits with indulgent taste profiles. Manufacturers are investing heavily in natural seasonings, plant-based ingredients, minimally processed formulations, and premium raw materials to capture evolving consumer preferences. As a result, the health-focused segment is expected to outperform conventional products in terms of growth throughout the forecast period, supported by premiumization trends and increasing demand for better-for-you snack alternatives.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channel in the global spicy biscuits market, accounting for approximately 35% of total sales in 2025. The segment’s dominance is driven by extensive product visibility, wide assortment availability, attractive promotional campaigns, and consumers’ preference for one-stop shopping experiences. These retail formats enable manufacturers to showcase diverse flavor variants, premium product lines, and new launches while benefiting from high foot traffic and strong brand exposure. The continued expansion of modern retail infrastructure across emerging economies further supports channel growth.Traditional grocery stores and neighborhood retail outlets continue to hold substantial importance, particularly across Asia-Pacific, Africa, and parts of Latin America, where localized purchasing patterns and convenience-driven shopping behavior remain prevalent. These outlets play a critical role in ensuring product accessibility across semi-urban and rural markets, supporting broad consumer reach.E-commerce represents the fastest-growing distribution channel, driven by rising internet penetration, increasing smartphone adoption, expanding digital payment ecosystems, and growing consumer preference for convenient online purchasing. Direct-to-consumer business models, subscription-based snack offerings, and digital marketing initiatives are further accelerating online sales growth. Specialty food retailers are also gaining prominence as consumers increasingly seek premium, organic, artisanal, and health-focused spicy biscuit products. Meanwhile, foodservice, institutional, and convenience-store channels continue to expand their contribution to overall market demand by increasing product availability across multiple consumption occasions.

End-Use Insights

Household retail consumption remains the dominant end-use segment, accounting for approximately 74% of global demand in 2025. The segment benefits from the widespread popularity of spicy biscuits as a daily snack consumed during tea-time, work breaks, travel, and other on-the-go occasions. Rising urbanization, busy lifestyles, and growing demand for convenient packaged snacks continue to support household consumption across both developed and developing markets. The affordability, portability, and long shelf life of spicy biscuits further contribute to their strong household penetration.Foodservice establishments represent the fastest-growing end-use segment within the market. Cafés, restaurants, hotels, quick-service restaurants, airline catering providers, and hospitality operators are increasingly incorporating packaged savory snacks into their offerings to enhance customer convenience and diversify snack menus. The growth of café culture, expanding tourism activity, and rising demand for ready-to-serve snack products are creating significant opportunities within this segment.Institutional consumption across offices, educational institutions, healthcare facilities, government organizations, and transportation catering services is also expanding steadily. In addition, export-oriented demand continues to strengthen, particularly in countries such as India, Indonesia, Malaysia, and Turkey, where manufacturers are increasingly supplying mainstream retail channels as well as ethnic food markets across North America, Europe, the Middle East, and Africa.

Consumer Group Insights

Adult consumers constitute the largest consumer group in the global spicy biscuits market, accounting for approximately 41% of total consumption in 2025. The segment’s leadership is driven by established snacking habits, higher purchasing power, growing preference for savory flavors, and frequent consumption across home, workplace, and travel settings. Adults often view spicy biscuits as convenient and satisfying snack options that complement busy lifestyles, making them the primary driver of overall market demand.Young adults represent one of the fastest-growing consumer segments due to their willingness to experiment with international cuisines, bold flavor profiles, and premium snack products. Increasing exposure to global food trends through digital platforms and social media is encouraging greater adoption of innovative spicy biscuit varieties among this demographic. Teenagers also contribute significantly to market growth, particularly through demand for trendy flavors, limited-edition products, and attractive packaging formats.Senior consumers are increasingly seeking healthier snack alternatives that offer reduced sodium content, wholegrain ingredients, higher fiber levels, and improved nutritional value. This trend is creating opportunities for manufacturers to develop age-specific product offerings while expanding the appeal of spicy biscuits across a broader consumer base. Customized packaging formats, portion-controlled products, and varying levels of flavor intensity are further helping manufacturers address the diverse preferences of different demographic groups.

Explore more data points, trends and opportunities Download Free Sample Report

Spicy Biscuits Market Segmentations

By Product Type

- Savory Spicy Biscuits

- Sweet-Spicy Biscuits

By Ingredient Positioning

- Conventional Spicy Biscuits

- Organic Spicy Biscuits

- Gluten-Free Spicy Biscuits

- High-Fiber Spicy Biscuits

- Wholegrain/Multigrain Spicy Biscuits

- Protein-Enriched Spicy Biscuits

- Reduced-Sodium Spicy Biscuits

By Packaging Format

- Single-Serve Packs (<50g)

- Regular Packs (50–150g)

- Family Packs (>150g)

- Multipack Formats

- Institutional/Bulk Packs

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Traditional Grocery Stores

- Specialty Food Stores

- Online Retail/E-Commerce

- Foodservice & Institutional Sales

By Price Tier

- Economy

- Mid-Priced

- Premium

- Super-Premium/Artisanal

Regional Insights

Asia-Pacific

Asia-Pacific remains the largest and fastest-growing regional market, accounting for approximately 42% of global demand in 2025. India represents the largest individual market globally, contributing nearly 18% of worldwide consumption due to its strong cultural preference for spicy snacks, extensive biscuit manufacturing base, and widespread consumption across both urban and rural populations. China follows with approximately 9% of global market share, supported by rapid urbanization, rising disposable incomes, increasing premium snack adoption, and expanding modern retail networks. Indonesia, Thailand, Vietnam, Malaysia, and the Philippines continue to record robust growth as expanding middle-class populations increase spending on packaged foods and convenience snacks.Regional growth is primarily driven by strong consumer affinity for spicy flavors, rapid urbanization, rising disposable incomes, growing working populations, expanding modern retail infrastructure, increasing penetration of organized food retail, rising e-commerce adoption, and continuous product innovation tailored to local taste preferences. The region also benefits from a large youth population, growing demand for convenient on-the-go snacks, and strong domestic manufacturing capabilities, positioning Asia-Pacific as the key engine of global market expansion throughout the forecast period.

North America

North America accounts for approximately 23% of global market demand, with the United States serving as the region’s dominant market. Growing multicultural populations, rising acceptance of ethnic and international flavors, and increasing consumer interest in premium savory snacks continue to support market expansion. Consumers are increasingly attracted to globally inspired products that offer distinctive taste experiences while aligning with evolving snacking preferences. Canada is also experiencing steady growth, particularly in urban centers characterized by diverse demographics and strong retail penetration.Regional growth is being driven by increasing demand for premium and gourmet snack products, rising consumer interest in international cuisines, expanding ethnic food consumption, strong innovation in flavor development, growing preference for healthier snack alternatives, and rapid growth of e-commerce-based food retailing. The popularity of convenient packaged snacks among busy consumers and continued investments in product premiumization further contribute to market development across the region.

Europe

Europe contributes approximately 22% of global market revenue, with the United Kingdom, Germany, France, Italy, and Spain representing the region’s largest markets. Demand for spicy biscuits continues to increase as consumers seek flavorful alternatives to traditional sweet biscuits and conventional snack products. Premium, artisanal, and health-focused offerings are gaining popularity, particularly among consumers seeking products with natural ingredients, clean-label formulations, and enhanced nutritional profiles.Regional growth is supported by strong retail infrastructure, increasing consumer interest in international cuisines, rising multicultural food influences, growing demand for premium snacking experiences, and expanding adoption of healthier food products. Premiumization trends remain particularly strong across Western Europe, while Eastern European markets are benefiting from rising disposable incomes and increasing availability of packaged snack products through modern retail channels.

Latin America

Latin America accounts for approximately 6% of global demand, with Mexico representing the region’s largest market due to its long-standing cultural affinity for spicy foods and well-established snack consumption habits. Brazil, Colombia, Chile, Peru, and Argentina are also witnessing growing demand for packaged savory snacks as consumer lifestyles become increasingly urbanized and convenience-oriented.Regional growth is being driven by expanding urban populations, improving economic conditions, rising disposable incomes, increasing penetration of modern retail formats, growing demand for convenient packaged foods, and strong consumer acceptance of spicy flavor profiles. The gradual expansion of international food manufacturers alongside local product innovation is further enhancing product availability and supporting long-term market development across the region.

Middle East & Africa

The Middle East & Africa region represents approximately 7% of global market value and is among the fastest-growing regional markets. Saudi Arabia, the United Arab Emirates, South Africa, Nigeria, Egypt, and Kenya are emerging as key growth markets supported by expanding retail infrastructure and increasing demand for convenient savory snack products. Consumer preference for flavorful snacks, combined with evolving dietary habits and rising packaged food consumption, continues to strengthen market opportunities across the region.Regional growth is primarily driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, increasing modern retail penetration, growing youth demographics, strong demand for convenience foods, and significant investments in food distribution infrastructure. The Gulf Cooperation Council countries are experiencing particularly strong growth due to premium food consumption trends, high purchasing power, and expanding international food product availability, while African markets are benefiting from increasing packaged food adoption and improving retail accessibility.

Key Players in the Spicy Biscuits Market

- Britannia Industries

- Parle Products

- ITC Limited

- Mondelez International

- Pladis

- Nestlé

- Kellanova

- Danone

- Anmol Industries

- Bisk Farm

- Yildiz Holding

- Ülker

- Mayora Indah

- Orion Corporation

- Julie's Manufacturing