Soy Sauce Packaging Bottles Market Size

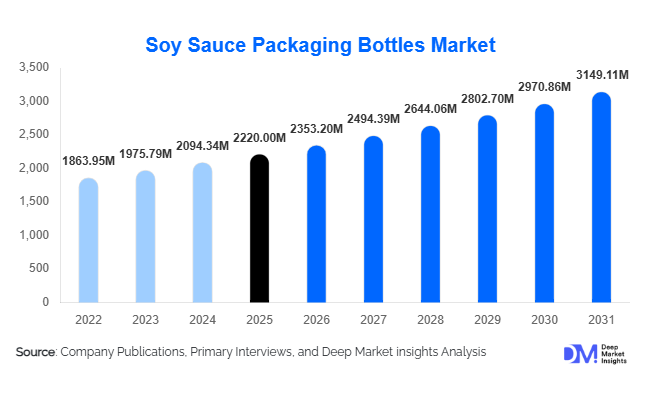

According to Deep Market Insights, the global soy sauce packaging bottles market size was valued at USD 2,220 million in 2025 and is projected to grow from USD 2,353.20 million in 2026 to reach USD 3,149.11 million by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The soy sauce packaging bottles market growth is being driven by rising global consumption of Asian condiments, expanding retail distribution of packaged sauces, increasing demand for premium and sustainable packaging formats, and continued growth in foodservice and export-oriented food manufacturing industries. Packaging plays a critical role in preserving product quality, preventing contamination, extending shelf life, and enhancing consumer convenience. As soy sauce consumption expands beyond traditional Asian markets into North America, Europe, the Middle East, and Latin America, demand for differentiated bottle formats, lightweight materials, and recyclable packaging solutions continues to increase.

Key Market Insights

- Glass bottles remain the dominant packaging format, accounting for approximately 44% of the global market value in 2025 due to premium positioning and superior product preservation.

- Asia-Pacific dominates global demand, representing nearly 58% of market revenue, supported by large-scale soy sauce consumption in China, Japan, South Korea, and Southeast Asia.

- Sustainable packaging adoption is accelerating, with food manufacturers increasingly utilizing recyclable glass, rPET, and lightweight packaging solutions.

- Foodservice and hospitality applications are growing rapidly, driven by increasing restaurant penetration and international popularity of Asian cuisine.

- Premium soy sauce products are boosting demand for decorative and specialty bottles, particularly in Japan, China, Europe, and North America.

- Smart packaging technologies, including QR-enabled labels, anti-counterfeit closures, and traceability solutions, are gradually being integrated into premium packaging formats.

- Export-oriented soy sauce manufacturing continues to create strong demand for durable, tamper-evident, and regulatory-compliant bottle packaging.

Soy Sauce Packaging Bottles Market Latest Trends

Sustainable and Lightweight Packaging Becoming Industry Standard

Environmental regulations and corporate sustainability commitments are significantly reshaping the soy sauce packaging bottles market. Major condiment manufacturers are increasingly adopting lightweight glass containers, recycled PET (rPET), and reusable bottle designs to reduce carbon footprints and transportation costs. Lightweight packaging reduces logistics expenses while improving handling efficiency throughout supply chains. In mature markets such as Europe, Japan, and North America, food companies are implementing circular packaging strategies that prioritize recyclability and recycled-content utilization. Retailers are also encouraging suppliers to adopt eco-friendly packaging to meet sustainability targets. As a result, demand for recyclable glass bottles, refillable containers, and post-consumer recycled plastics continues to grow across both retail and foodservice channels.

Premiumization Driving Advanced Bottle Design Innovation

The premium soy sauce category is expanding globally, creating strong demand for aesthetically differentiated packaging solutions. Manufacturers are introducing decorative glass bottles, customized embossing, ergonomic dispenser designs, and premium closure systems to enhance shelf appeal and brand differentiation. Consumers increasingly associate premium packaging with higher-quality ingredients and authentic production methods. Japanese and Korean premium soy sauce brands are particularly investing in sophisticated bottle designs to strengthen brand positioning in international markets. Premium packaging also supports higher retail pricing and improved margins for both condiment manufacturers and packaging suppliers.

Soy Sauce Packaging Bottles Market Drivers

Growing Global Consumption of Asian Cuisine

The rapid globalization of Asian cuisine remains one of the strongest growth drivers for soy sauce packaging bottles. Restaurants, quick-service chains, and retail consumers across North America, Europe, Latin America, and the Middle East are increasingly incorporating soy sauce into everyday food preparation. The expansion of sushi restaurants, Asian fusion dining, Korean food culture, and home cooking trends has substantially increased soy sauce consumption. This growth directly translates into higher demand for retail-sized and foodservice packaging formats across multiple regions.

Expansion of Organized Retail and E-Commerce Food Sales

Modern retail channels are increasing the visibility and accessibility of packaged soy sauce products globally. Supermarkets, hypermarkets, convenience stores, and e-commerce platforms require packaging solutions that maximize shelf presentation, transportation efficiency, and consumer convenience. Packaging suppliers are responding by developing bottles with improved durability, leak resistance, tamper-evident features, and optimized dimensions for automated retail distribution systems. The continued expansion of online grocery channels further supports demand for robust packaging capable of protecting products during long-distance transportation.

Rising Demand for Premium Condiments and Specialty Sauces

Consumers are increasingly seeking premium, low-sodium, organic, naturally brewed, and region-specific soy sauce varieties. These products often require higher-end packaging formats that communicate quality and authenticity. Premium soy sauce manufacturers rely heavily on customized glass bottles, dispenser systems, and decorative packaging designs to differentiate products from mass-market alternatives. This premiumization trend has significantly increased average packaging value per unit sold.

Soy Sauce Packaging Bottles Market Restraints

Volatility in Raw Material Prices

Packaging manufacturers remain exposed to fluctuations in glass, resin, aluminum, energy, and transportation costs. Rising energy prices particularly affect glass bottle manufacturing due to the energy-intensive nature of furnace operations. Resin price volatility also impacts PET and HDPE bottle production costs. These cost pressures can reduce manufacturer margins and create pricing challenges throughout the value chain.

Competition from Flexible Packaging Alternatives

Although bottles remain the preferred packaging format for soy sauce, flexible pouches and refill packs are increasingly being adopted in Asia and emerging markets. Flexible packaging offers lower material consumption, reduced logistics costs, and improved sustainability metrics. The growing adoption of refill systems may partially limit growth opportunities for traditional bottle manufacturers over the long term.

Soy Sauce Packaging Bottles Industry Key Opportunities

Growth of Refillable Packaging Ecosystems

Reusable and refillable packaging systems are emerging as a major opportunity across developed markets. Retailers and food manufacturers are exploring refill stations, reusable bottle programs, and concentrated sauce formats to reduce packaging waste. Companies that develop durable refillable bottle solutions can benefit from long-term sustainability-driven demand growth.

Expansion into Emerging Consumer Markets

Soy sauce consumption is growing rapidly in India, Brazil, Mexico, Saudi Arabia, UAE, South Africa, and several Southeast Asian economies. Rising urbanization, increasing disposable incomes, and greater exposure to international cuisines are creating new demand centers for packaged condiments. Packaging suppliers that establish localized production capabilities in these markets are expected to benefit significantly from future growth.

Smart Packaging and Traceability Solutions

Food safety regulations and consumer demand for transparency are driving interest in QR-enabled packaging, anti-counterfeiting systems, and digital traceability technologies. Premium soy sauce brands are increasingly utilizing packaging as a vehicle for consumer engagement, product authentication, and supply chain transparency. This trend creates opportunities for packaging manufacturers offering integrated digital solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2220.00 Million |

| Market Size in 2026 | USD 2353.20 Million |

| Market Size in 2031 | USD 3149.11 Million |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Glass bottles dominate the global soy sauce packaging bottles market, accounting for approximately 44% of total revenue in 2025. The segment maintains its leadership position due to the superior barrier properties of glass, which preserve flavor, aroma, and product quality while preventing chemical interactions with the contents. Glass packaging is widely preferred by premium and traditional soy sauce manufacturers because it enhances brand perception, supports product authenticity, and aligns with growing consumer demand for recyclable and environmentally sustainable packaging solutions. Export-oriented Japanese and Chinese soy sauce producers continue to rely heavily on glass bottles for premium product lines, further reinforcing segment dominance. The growth of the glass segment is primarily driven by increasing consumer preference for premium condiments, expanding demand for sustainable packaging, and rising exports of high-value soy sauce products.Plastic bottles represent nearly 40% of market revenue and remain highly attractive for mass-market applications due to their lightweight nature, lower transportation costs, durability, and cost-efficient manufacturing. Plastic packaging continues to gain popularity among large-volume manufacturers serving supermarkets, convenience stores, and foodservice operators where affordability and logistical efficiency are critical purchasing factors. Advancements in recyclable PET packaging and lightweight bottle designs are further supporting segment expansion. Meanwhile, metal containers and hybrid packaging formats collectively account for the remaining market share and are primarily utilized in industrial, food processing, and specialty premium applications where extended shelf life and enhanced product protection are required.

Capacity Insights

The 251–500 ml segment leads the global market with approximately 37% share of total revenue in 2025. This capacity range has emerged as the preferred retail packaging format across developed and emerging markets due to its ideal balance between affordability, convenience, storage efficiency, and household consumption requirements. The segment is widely distributed through supermarkets, hypermarkets, convenience stores, and online retail channels, making it the most accessible and frequently purchased package size among consumers. The leading growth driver for this segment is the increasing preference for mid-sized packaging formats that provide adequate product volume for regular household usage without requiring frequent repurchases.The 501–1,000 ml category continues to experience strong demand from foodservice establishments, restaurants, institutional kitchens, and commercial users seeking greater cost efficiency through bulk purchasing. Rising restaurant activity and growing consumption of soy sauce in food preparation applications are supporting expansion within this segment. At the same time, packaging formats below 250 ml are witnessing accelerated growth, particularly in premium, artisanal, organic, and specialty soy sauce categories where consumers increasingly seek product trial sizes, gourmet offerings, and convenience-oriented packaging solutions.

Closure Type Insights

Screw-cap closures account for nearly 52% of total market revenue, making them the dominant closure format globally. Their widespread adoption is supported by low manufacturing costs, ease of integration into automated filling operations, excellent leak-prevention performance, and compatibility with both glass and plastic bottle formats. Manufacturers continue to favor screw-cap systems because they provide reliable product sealing while maintaining production efficiency and cost competitiveness. The primary growth driver for the segment is the increasing demand for cost-effective and highly reliable closure solutions that ensure product safety throughout transportation, storage, and consumer use.Dispensing spout closures represent the fastest-growing category within the market as consumers increasingly prioritize convenience, controlled pouring, reduced product wastage, and enhanced user experience. Premium soy sauce brands are actively incorporating dispensing technologies to differentiate products and improve functionality. Flip-top caps and specialty closure systems also continue to gain traction in selected premium and foodservice applications where ease of use and packaging innovation play an important role in purchasing decisions.

Bottle Design Insights

Standard cylindrical bottles account for approximately 48% of global demand and remain the most widely utilized bottle design. The segment benefits from superior manufacturing efficiency, optimized material utilization, ease of transportation, and seamless compatibility with high-speed automated filling and labeling systems. Large-scale soy sauce producers continue to favor cylindrical designs because they offer lower production costs while maximizing operational efficiency across supply chains. The leading growth driver for this segment is the increasing need for cost-efficient packaging formats that support large-volume production and distribution activities.Despite the dominance of conventional designs, decorative, ergonomic, and premium-shaped bottles are expanding at a faster pace as manufacturers increasingly focus on product differentiation and brand positioning. Premium packaging designs help companies strengthen shelf visibility, enhance consumer engagement, and support higher product pricing strategies. The growing premiumization trend across condiment categories is expected to accelerate demand for innovative bottle aesthetics throughout the forecast period.

End-Use Insights

Household consumption remains the largest end-use segment, accounting for approximately 46% of total market revenue in 2025. The segment continues to benefit from widespread retail availability, stable consumer demand for cooking condiments, and increasing incorporation of soy sauce into everyday meal preparation across both Asian and non-Asian households. The primary growth driver for the household segment is the expanding adoption of soy sauce in home cooking, supported by rising consumer interest in international cuisines and growing retail penetration across emerging economies.Foodservice and hospitality represent approximately 28% of global demand and constitute the fastest-growing end-use category. Expansion of restaurant chains, quick-service restaurants, cloud kitchens, hotels, and catering services has significantly increased commercial consumption of soy sauce products worldwide. Growing popularity of Asian cuisine across North America, Europe, and emerging markets continues to create substantial packaging demand from foodservice operators. Food processing applications account for approximately 18% of market demand and are supported by increasing use of soy sauce as a flavoring ingredient in packaged foods, ready meals, marinades, sauces, snacks, and processed meat products.

Explore more data points, trends and opportunities Download Free Sample Report

Soy Sauce Packaging Bottles Market Segmentations

By Material Type

- Glass Bottles

- Plastic Bottles

- Metal Bottles

- Hybrid/Composite Bottles

By Capacity

- Up to 100 ml

- 101–250 ml

- 251–500 ml

- 501–1,000 ml

- Above 1,000 ml

By Closure Type

- Screw Cap Bottles

- Flip-Top Bottles

- Dispensing Spout Bottles

- Pump Dispensing Bottles

- Tamper-Evident Closure Bottles

By Bottle Design

- Standard Cylindrical Bottles

- Ergonomic Grip Bottles

- Tabletop Dispenser Bottles

- Premium/Decorative Bottles

- Refillable Bottles

By Transparency

- Transparent Bottles

- Colored/Opaque Bottles

By End Use

- Household Consumption

- Foodservice & Hospitality

- Food Processing Industry

- Retail & Private Label Packaging

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global soy sauce packaging bottles market, accounting for approximately 58% of total revenue in 2025. The region serves as both the largest production hub and the largest consumption center for soy sauce globally. China alone contributes nearly 29% of worldwide demand owing to its extensive manufacturing base, large population, and deeply rooted consumption culture. Japan accounts for approximately 12% of global demand and continues to lead the industry in premium packaging innovation, product differentiation, and sustainable packaging development. South Korea, Indonesia, Thailand, Vietnam, and Taiwan collectively contribute substantial demand due to the integral role of soy-based condiments in regional cuisines. India is emerging as one of the fastest-growing markets, supported by rapid urbanization, expanding organized retail, increasing exposure to international food trends, and rising popularity of Asian cuisine among younger consumers.The region's growth is primarily driven by strong domestic soy sauce consumption, expanding middle-class populations, rising disposable incomes, continuous growth of the foodservice industry, increasing exports of packaged soy sauce products, and ongoing investments in modern packaging technologies. The presence of major soy sauce manufacturers and established supply chains further strengthens Asia-Pacific's leadership position within the global market.

North America

North America accounts for approximately 14% of global market demand. The United States represents nearly 11% of worldwide consumption and remains the primary contributor to regional revenue. Demand growth is being supported by increasing consumption of Asian cuisine, expanding restaurant and quick-service chains, growing multicultural populations, and rising consumer preference for premium condiments and authentic international food products. Retail distribution channels, including supermarkets, warehouse clubs, specialty food stores, and e-commerce platforms, continue to facilitate broad product accessibility.Regional growth is driven by the rapid adoption of Asian-inspired cooking at home, increasing demand for premium and low-sodium soy sauce variants, expansion of foodservice establishments featuring Asian menus, and growing consumer awareness regarding sustainable packaging solutions. Innovation in convenience packaging and premium product positioning is also contributing to higher packaging value across the region.

Europe

Europe contributes approximately 16% of global market revenue and represents one of the fastest-growing regional markets. Germany, the United Kingdom, France, Italy, and the Netherlands are among the largest consumers of soy sauce products across the region. Demand is increasingly supported by changing dietary preferences, growing popularity of Asian restaurants, and rising incorporation of international flavors into everyday cooking habits. Import demand for premium soy sauce products continues to expand, creating opportunities for advanced and high-value packaging solutions.The primary drivers of regional growth include increasing consumption of Asian cuisine, strong demand for premium imported food products, expansion of organized retail networks, and stringent sustainability regulations encouraging the adoption of recyclable and environmentally friendly packaging materials. Consumer preference for premium packaging aesthetics and eco-conscious purchasing behavior is further supporting market expansion throughout Europe.

Latin America

Latin America accounts for approximately 6% of global market demand. Brazil and Mexico remain the leading markets within the region, supported by growing urban populations, expanding middle-income consumer groups, and increasing availability of international food products. Rising exposure to global culinary trends is encouraging greater adoption of soy sauce across both household and foodservice channels.Regional market growth is being driven by accelerating urbanization, modernization of retail infrastructure, expansion of supermarket and hypermarket networks, increasing penetration of international restaurant chains, and growing consumer willingness to experiment with global cuisines. Improvements in distribution systems and broader product availability are expected to further strengthen demand for soy sauce packaging bottles across Latin America.

Middle East & Africa

The Middle East & Africa region contributes approximately 6% of global market value. Saudi Arabia, the United Arab Emirates, South Africa, and Egypt represent the major demand centers within the region. Consumption continues to increase as international food products become more accessible and consumers show greater interest in diverse culinary experiences. The UAE remains one of the fastest-growing markets due to its large expatriate population and highly developed hospitality sector.Growth across the region is driven by expanding tourism activity, rapid development of the hospitality and foodservice sectors, increasing urbanization, rising disposable incomes, growth in international retail chains, and growing popularity of Asian cuisine among both local and expatriate populations. Continued investments in modern retail infrastructure and foodservice expansion are expected to create significant opportunities for soy sauce packaging manufacturers throughout the forecast period.

Key Players in the Soy Sauce Packaging Bottles Market

- Ardagh Group

- O-I Glass, Inc.

- Verallia

- Vidrala S.A.

- Vetropack Holding AG

- Amcor plc

- Berry Global Group

- Silgan Holdings Inc.

- ALPLA Group

- Gerresheimer AG

- Piramal Glass

- Orora Limited

- Toyo Glass Co., Ltd.

- Nihon Yamamura Glass Co., Ltd.

- HEINZ-GLAS Group