Inert Gases for Food Processing Market Size

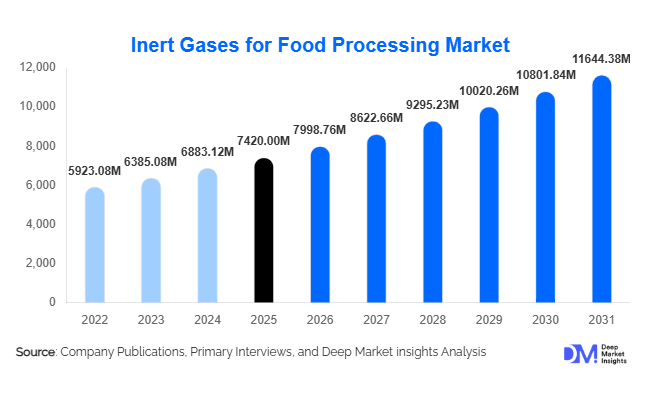

According to Deep Market Insights, the global inert gases for food processing market size was valued at USD 7,420 million in 2025 and is projected to grow from USD 7,998.76 million in 2026 to reach USD 11,644.38 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). Market growth is primarily driven by the increasing demand for extended shelf life, rapid expansion of packaged and convenience foods, and rising investments in cold-chain and modified atmosphere packaging (MAP) technologies. The growing need to reduce food waste, comply with stringent food safety standards, and enhance product freshness across global supply chains continues to position inert gases-particularly nitrogen and carbon dioxide-as critical enablers in modern food processing.

Key Market Insights

- Nitrogen remains the dominant gas type, accounting for nearly 45% of total market share in 2025 due to its extensive use in MAP and food blanketing applications.

- Modified Atmosphere Packaging (MAP) leads by functionality, contributing approximately 38% of overall demand as packaged meat and ready-to-eat meals expand globally.

- North America dominates the market, supported by advanced meat processing and beverage industries.

- Asia-Pacific is the fastest-growing region, driven by expanding retail infrastructure and export-oriented food manufacturing in China and India.

- Bulk liquid supply remains the preferred distribution mode, accounting for over 50% of total revenues among large-scale processors.

- Technological advancements in on-site nitrogen generation and cryogenic freezing are improving cost efficiency and sustainability metrics across food plants.

What are the latest trends in the inert gases for food processing market?

Rising Adoption of On-Site Gas Generation Systems

Food manufacturers are increasingly installing on-site nitrogen generation systems using pressure swing adsorption (PSA) technology. This shift reduces dependency on bulk transportation, lowers operational costs, and improves supply reliability. Sustainability goals are also accelerating adoption, as on-site systems minimize carbon emissions associated with gas delivery logistics. Mid-sized food processors in emerging economies are rapidly integrating compact nitrogen generators, enhancing decentralized gas availability.

Growth in Cryogenic Freezing Applications

Rapid freezing using liquid nitrogen and carbon dioxide is gaining traction, particularly in seafood, meat, and bakery segments. Cryogenic systems ensure faster freezing rates, better texture retention, and minimal microbial growth. With global frozen food demand expanding at over 8% annually, processors are investing in cryogenic tunnels and immersion systems to meet export quality standards and reduce product spoilage.

What are the key drivers in the inert gases for food processing market?

Expansion of Packaged and Convenience Foods

The global processed food industry, valued at over USD 4 trillion, continues to expand due to urbanization and changing dietary patterns. Packaged snacks, ready meals, and frozen foods rely heavily on inert gases for oxidation prevention and shelf-life extension. MAP technology is increasingly integrated into automated packaging lines, boosting nitrogen and CO₂ consumption worldwide.

Stringent Food Safety Regulations

Regulatory authorities such as the FDA and EFSA mandate strict food preservation and contamination control standards. Inert gases reduce microbial activity and oxygen exposure, ensuring compliance with hygiene protocols. Export-focused food processors must adhere to international quality benchmarks, driving sustained demand for high-purity food-grade gases.

What are the restraints for the global market?

Energy-Intensive Production Processes

The production of nitrogen and carbon dioxide is energy-intensive, making the industry vulnerable to electricity and natural gas price volatility. Fluctuating input costs directly affect supplier margins and pricing strategies.

High Infrastructure Investment Requirements

Cryogenic storage tanks, transport systems, and MAP integration require significant capital investment. Small and medium-scale food processors may face financial constraints, limiting rapid adoption in certain developing regions.

What are the key opportunities in the inert gases for food processing industry?

Export-Driven Meat and Seafood Processing Growth

Major exporting countries such as Brazil, India, Thailand, and the United States are expanding meat and seafood production capacities. Export compliance requirements necessitate advanced preservation techniques, creating strong opportunities for cryogenic gas suppliers and MAP solution providers near export hubs.

Sustainable Packaging and Waste Reduction Initiatives

Governments and food manufacturers are focusing on reducing food waste across supply chains. Inert gas applications significantly extend shelf life, aligning with sustainability mandates. Companies offering integrated gas management solutions and digital monitoring systems can capitalize on ESG-driven procurement strategies.

Gas Type Insights

Nitrogen dominates the global market, accounting for approximately 45% share in 2025, primarily due to its inert characteristics, abundant availability, and cost efficiency in oxygen displacement applications. Its widespread use in Modified Atmosphere Packaging (MAP), snack packaging, dairy preservation, and edible oil storage significantly supports segment leadership. The gas effectively prevents oxidation, maintains product texture, and extends shelf life without altering flavor profiles, making it highly preferred across large-scale food processing facilities. Carbon dioxide represents nearly 35% of total demand, driven by its dual functionality in carbonation and antimicrobial preservation. Its strong adoption within beverage manufacturing, particularly carbonated soft drinks, beer, and sparkling water, reinforces steady consumption, while its bacteriostatic properties enhance shelf life in meat and bakery packaging applications. Argon and blended gases collectively account for approximately 20% of the market, largely utilized in premium preservation environments, high-value seafood storage, specialty dairy applications, and controlled atmosphere storage systems. Growing demand for high-quality exports and extended distribution cycles continues to support the adoption of blended gas formulations.

Functionality Insights

Modified Atmosphere Packaging leads the market with approximately 38% share in 2025, supported by the rising global consumption of fresh-cut produce, processed meat, ready-to-eat meals, and convenience food products. The leading driver for this segment is the increasing need to extend product shelf life while maintaining freshness, color stability, and safety standards across organized retail chains and export markets. The rapid expansion of supermarkets, e-commerce grocery platforms, and cold chain infrastructure further strengthens MAP adoption. Cryogenic freezing represents the second-largest functional segment and is expanding at over 8% CAGR, driven by stringent export quality requirements and growing frozen food consumption worldwide. The ability of cryogenic gases to preserve cellular structure, texture, and nutritional value makes them critical in seafood, meat, and processed food exports. Carbonation applications continue to generate substantial demand, particularly in North America and Europe, where beverage manufacturing remains highly developed and per capita consumption of carbonated beverages is strong.

Distribution Mode Insights

Bulk liquid supply accounts for approximately 52% of total revenues in 2025, making it the leading distribution mode. The primary driver for this segment is cost efficiency and uninterrupted supply for large-scale food processors and beverage manufacturers operating continuous production lines. Bulk delivery reduces logistical costs per unit and ensures operational reliability in high-volume facilities. Cylinder-based distribution remains essential for small and medium-sized enterprises, specialty processors, and decentralized food production units where flexibility and lower upfront infrastructure investment are critical. On-site gas generation is emerging as the fastest-growing distribution segment, supported by sustainability initiatives, long-term cost optimization, reduced transportation emissions, and supply chain resilience strategies adopted by large food processing companies. Increasing energy efficiency technologies and advancements in nitrogen generation systems further accelerate adoption.

End-Use Industry Insights

Meat, poultry, and seafood processing remains the largest end-use segment, contributing approximately 34% of overall demand in 2025. The leading growth driver for this segment is the necessity to extend shelf life, maintain color stability, and prevent microbial growth during storage and transportation, particularly for export-oriented processing facilities. Rising global protein consumption and expanding quick-service restaurant networks further stimulate demand. The beverage industry follows as a major contributor, supported by sustained carbonation requirements across carbonated soft drinks, beer, sparkling beverages, and functional drinks. Increasing product diversification and premium beverage launches strengthen gas consumption volumes. Dairy, bakery, and ready-to-eat meal segments are emerging as high-growth categories due to expanding organized retail penetration, growing urbanization, increasing disposable income levels, and rising demand for convenience-based food products. Frozen bakery and ready-to-cook meals are particularly benefiting from advancements in cryogenic freezing and MAP technologies.

| By Gas Type | By Functionality | By Distribution Mode | By End-Use Industry | By Process Stage |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 32% of the global market share in 2025, led by the United States, which accounts for nearly 78% of regional consumption. Regional growth is driven by highly advanced meat processing infrastructure, strong penetration of packaged and convenience foods, and sustained demand for beverage carbonation. The presence of large multinational food processors, strict food safety regulations, and continuous investment in cold chain logistics further strengthen market expansion. Technological advancements in MAP and cryogenic systems, along with increasing adoption of on-site gas generation for operational efficiency, contribute to steady growth. Canada supports regional expansion through its strong frozen seafood exports, dairy processing modernization, and rising demand for sustainable packaging technologies.

Europe

Europe represents approximately 27% of global demand, supported by key economies such as Germany, France, the United Kingdom, Italy, and Spain. Regional growth is primarily driven by stringent food safety regulations, well-established cold chain networks, and sustainability-focused packaging initiatives aligned with environmental policies. The European Union’s emphasis on reducing food waste significantly accelerates adoption of Modified Atmosphere Packaging solutions. Mature retail infrastructure, strong private-label penetration, and premium product positioning further sustain steady demand. Additionally, high consumption of processed meat products and carbonated beverages supports consistent gas utilization across the region.

Asia-Pacific

Asia-Pacific accounts for approximately 29% market share in 2025 and is the fastest-growing region, expanding at over 9% CAGR. Rapid urbanization, increasing disposable incomes, and shifting dietary patterns toward processed and packaged foods serve as primary growth drivers. China leads regional consumption due to its large-scale food manufacturing base, expanding export capabilities, and strong domestic demand for frozen and ready-to-eat products. India represents the fastest-growing national market within the region, supported by expanding organized retail chains, government-backed food processing incentives under industrial development programs, and rapid growth of cold storage infrastructure. Southeast Asian countries are also contributing significantly due to rising seafood exports and expanding beverage manufacturing facilities.

Latin America

Latin America demonstrates steady market growth, led by Brazil, which dominates regional demand due to its strong meat and poultry export industry. Increasing compliance with international food safety standards and export-oriented packaging requirements drive sustained adoption of preservation gases. Mexico supports regional expansion through its well-established beverage manufacturing sector, growing snack production facilities, and expanding convenience food consumption. Rising foreign direct investments in food processing infrastructure further strengthen regional market prospects.

Middle East & Africa

The Middle East & Africa region is witnessing gradual expansion, supported primarily by increasing adoption of Modified Atmosphere Packaging in GCC countries due to heavy reliance on food imports and the need to extend product shelf life during transportation. Growing investments in food processing and cold storage infrastructure across Saudi Arabia and the UAE contribute to market growth. South Africa leads regional production capacity, particularly in processed meats, beverages, and dairy applications. Expanding retail modernization, urban population growth, and rising consumer demand for packaged food products continue to drive long-term market development across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Inert Gases for Food Processing Market

- Linde plc

- Air Liquide

- Air Products and Chemicals, Inc.

- Messer Group GmbH

- Taiyo Nippon Sanso Corporation

- Air Water Inc.

- SOL Group

- Matheson Tri-Gas, Inc.

- Gulf Cryo

- Yingde Gases

- Ellenbarrie Industrial Gases

- Universal Industrial Gases

- Strandmøllen A/S

- SIAD Group

- Nexair LLC