Packaging Gases for Food Market Size

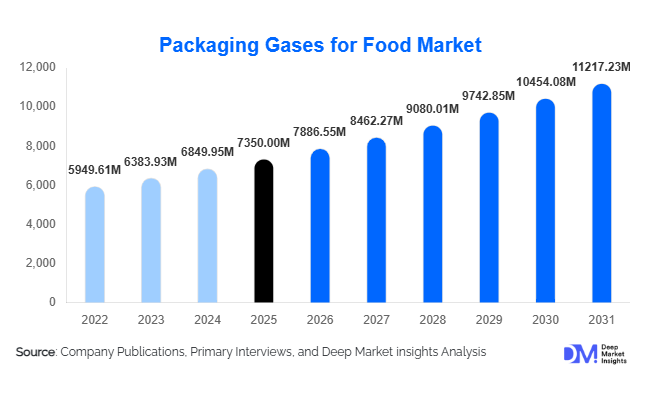

According to Deep Market Insights,the global packaging gases for food market size was valued at USD 7,350 million in 2025 and is projected to grow from USD 7,886.55 million in 2026 to reach USD 11,217.23 million by 2031, expanding at a CAGR of 7.3% during the forecast period (2026–2031). The market growth is primarily driven by the rising global consumption of processed and convenience foods, increasing adoption of modified atmosphere packaging (MAP), and expanding cold chain infrastructure across emerging economies. Packaging gases such as carbon dioxide, nitrogen, and oxygen play a critical role in extending shelf life, preserving freshness, and ensuring regulatory compliance in food safety standards.

Key Market Insights

- Carbon dioxide dominates the market, accounting for nearly 42% of total demand in 2025 due to its antimicrobial properties and extensive use in meat and bakery packaging.

- Modified Atmosphere Packaging (MAP) represents over 55% of application share, making it the most widely adopted technology globally.

- Europe leads the global market with approximately 30% share, supported by stringent food safety regulations and strong processed food exports.

- Asia-Pacific is the fastest-growing region, registering close to 9% CAGR due to rapid retail modernization and cold chain investments.

- Meat, poultry, and seafood account for nearly 34% of total market value, driven by export-oriented processing industries.

- The top five companies control approximately 58% of global market share, reflecting moderate consolidation among industrial gas leaders.

What are the latest trends in the packaging gases for food market?

Shift Toward On-Site Gas Generation Systems

Food processors are increasingly investing in on-site nitrogen generation and CO₂ recovery systems to mitigate supply volatility and reduce long-term procurement costs. This trend is particularly strong in North America and Europe, where recent CO₂ shortages highlighted vulnerabilities in centralized supply chains. On-site generation enhances operational reliability, reduces transportation emissions, and improves cost predictability. Large meat processors and dairy manufacturers are entering long-term contracts with industrial gas suppliers that bundle equipment installation, monitoring systems, and maintenance services.

Integration with Smart and Sustainable Packaging

The integration of packaging gases with intelligent packaging technologies is gaining traction. Oxygen sensors, freshness indicators, and real-time gas monitoring systems are being deployed to enhance product transparency and reduce food waste. Sustainability concerns are also reshaping procurement decisions, with food companies prioritizing low-carbon CO₂ sources recovered from bioethanol or ammonia plants. This aligns with global ESG mandates and corporate carbon reduction targets, strengthening the role of packaging gases in sustainable food supply chains.

What are the key drivers in the packaging gases for food market?

Growth in Processed and Convenience Food Consumption

Rapid urbanization, dual-income households, and expanding supermarket penetration are accelerating demand for ready-to-eat meals, packaged meats, dairy snacks, and fresh-cut produce. Packaging gases extend shelf life by 30–300%, making them indispensable in modern food retail. Asia-Pacific and Latin America are witnessing strong processed food growth, directly boosting MAP adoption rates.

Stringent Food Safety Regulations

Regulatory authorities across the U.S., Europe, China, and India are enforcing strict microbial safety and traceability requirements. Packaging gases reduce oxidation and inhibit bacterial growth, ensuring compliance with HACCP and ISO 22000 standards. This regulatory push continues to drive adoption among both multinational and regional food processors.

What are the restraints for the global market?

CO₂ Supply Volatility

The market remains vulnerable to fluctuations in carbon dioxide supply, often linked to fertilizer and bioethanol plant operations. Periodic shortages have caused price spikes of 12–18%, impacting profit margins and operational stability for food processors.

High Initial CapEx for MAP Equipment

Small and medium-sized food manufacturers face barriers due to the capital-intensive nature of MAP machinery and gas blending systems. Limited technical expertise and infrastructure gaps in developing regions further constrain adoption.

What are the key opportunities in the packaging gases for food industry?

Expansion of Cold Chain Infrastructure in Emerging Markets

Governments in India, China, Brazil, and Gulf countries are investing heavily in refrigerated logistics and food processing zones. As cold chain penetration increases, demand for advanced packaging technologies and gas solutions is expected to rise significantly, creating strong entry opportunities for industrial gas providers.

E-Commerce Grocery and Export-Driven Demand

The growth of online grocery retail and cross-border trade in perishable goods is driving demand for extended shelf-life packaging solutions. Meat exports from Brazil, seafood exports from Vietnam and Norway, and dairy exports from Europe rely heavily on MAP systems, creating sustained demand for packaging gases globally.

Gas Type Insights

Carbon dioxide dominates the global packaging gases market, accounting for approximately 42% of total revenue share in 2025. Its leadership position is primarily driven by its strong antimicrobial properties, ability to inhibit bacterial and fungal growth, and effectiveness in extending the shelf life of perishable food products. Carbon dioxide is extensively used in meat, poultry, seafood, and bakery packaging, where microbial control is critical to maintaining product safety and freshness. The growing global demand for protein-rich diets and export-oriented meat processing industries further strengthens its market dominance. Nitrogen represents the second-largest segment, widely utilized for oxygen displacement to prevent oxidation, rancidity, and moisture degradation in snack foods, dairy products, coffee, and ready-to-eat meals. Its inert nature makes it ideal for maintaining product texture and flavor integrity. Oxygen is selectively applied in red meat packaging to preserve the bright red color that consumers associate with freshness, while argon and customized specialty gas mixtures serve premium and niche applications, including high-value fresh produce and gourmet food products. Increasing demand for tailored gas blends designed for specific food categories is expanding value-added service opportunities and strengthening long-term supplier partnerships across the food processing industry.

Application Technology Insights

Modified Atmosphere Packaging (MAP) remains the leading application technology, accounting for nearly 55% of total market value in 2025. Its dominance is driven by its ability to significantly extend shelf life, reduce food waste, and maintain product quality without the need for chemical preservatives. The rising global consumption of packaged and convenience foods, coupled with stringent food safety regulations, continues to accelerate MAP adoption across both developed and emerging markets. Controlled Atmosphere Packaging (CAP) plays a critical role in bulk storage and long-distance transportation of fresh fruits and vegetables, particularly in export-driven agricultural economies. Vacuum packaging combined with gas flushing is gaining traction among mid-sized food processors seeking cost-effective yet efficient preservation methods. Meanwhile, active packaging systems are emerging in premium and technologically advanced segments where real-time monitoring, freshness indicators, and enhanced oxygen control are essential. Continuous technological advancements in automation, smart sensors, and gas mixing systems are further strengthening the adoption of advanced packaging solutions worldwide.

End-Use Industry Insights

The meat, poultry, and seafood segment represents the largest end-use industry, contributing approximately 34% of the total market size in 2025. The segment’s leadership is driven by increasing global protein consumption, strict hygiene regulations, and growing international trade of frozen and chilled meat products. Export-oriented processing facilities rely heavily on packaging gases to maintain product freshness and comply with international safety standards, making this segment the primary demand driver for the market. Dairy products and ready-to-eat meals are among the fastest-growing categories, supported by rapid urbanization, rising disposable incomes, and shifting consumer preferences toward convenience foods. Fresh produce packaging is expanding significantly, particularly in Asia-Pacific, where supermarket penetration, organized retail growth, and improved cold chain logistics are transforming traditional distribution channels. The global processed food industry, valued at over USD 4 trillion, continues to generate sustained demand for advanced packaging technologies, reinforcing the long-term growth trajectory of the packaging gases market.

| By Gas Type | By Application Technology | By Food Category (End-Use Industry) | By Distribution Channel | By Region |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 28% of the global market share in 2025, with the United States contributing nearly three-quarters of regional demand. Regional growth is driven by strong meat and poultry exports, well-established cold chain infrastructure, and high penetration of Modified Atmosphere Packaging technologies across retail and foodservice sectors. The presence of major food processing companies and advanced automation in packaging facilities further accelerates adoption. Increasing consumer preference for packaged fresh foods and extended shelf-life products supports consistent demand. Canada contributes significantly through its seafood and dairy processing industries, while Mexico is witnessing steady growth supported by expanding food manufacturing capabilities and cross-border trade activities.

Europe

Europe leads the global market with nearly 30% share in 2025, supported by stringent food safety regulations, sustainability mandates, and strong emphasis on reducing food waste. Countries such as Germany, France, the U.K., Italy, and the Netherlands are major contributors to regional demand. Germany alone accounts for nearly 20% of European consumption, driven by its advanced food processing industry and strong export orientation. The European Union’s regulatory framework encourages adoption of high-performance packaging technologies that enhance shelf life while maintaining environmental compliance. Growing demand for organic and premium packaged foods further supports the use of specialized gas blends and innovative MAP solutions across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at a CAGR of close to 9% during the forecast period. China contributes nearly 40% of regional demand, followed by Japan and India. Rapid urbanization, rising disposable incomes, and significant expansion of organized retail and e-commerce grocery platforms are key growth drivers. Increasing exports of seafood, processed foods, and ready-to-eat meals further stimulate demand for advanced packaging solutions. Investments in cold chain logistics infrastructure and government initiatives aimed at reducing food wastage are accelerating the adoption of MAP and other preservation technologies. India’s expanding dairy and meat processing sectors are also contributing substantially to regional growth.

Latin America

Latin America is experiencing steady growth, led by Brazil and Mexico. Brazil’s strong meat export industry serves as the primary growth engine, supported by large-scale poultry and beef production facilities that rely on packaging gases to maintain product quality during international shipments. Mexico benefits from expanding food manufacturing and increasing supermarket penetration, which drives the adoption of MAP technologies. Rising middle-class consumption and improving distribution networks across the region are further enhancing market expansion.

Middle East & Africa

The Middle East & Africa region is gradually emerging as a significant growth market. The UAE and Saudi Arabia are key demand centers due to heavy reliance on food imports and rapid modernization of retail infrastructure, including hypermarkets and large supermarket chains. The need to maintain freshness of imported meat, dairy, and fresh produce products drives demand for packaging gases. South Africa remains a regional hub with relatively advanced food processing capabilities and growing export activities. Increasing investments in cold storage facilities and government initiatives to enhance food security are expected to further support market growth across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Packaging Gases for Food Market

- Linde plc

- Air Liquide

- Air Products and Chemicals Inc.

- Messer Group

- Nippon Sanso Holdings Corporation

- Taiyo Nippon Sanso

- SOL Group

- Gulf Cryo

- Yingde Gases

- Matheson Tri-Gas

- Universal Industrial Gases

- Strandmøllen

- Ellenbarrie Industrial Gases

- INOX Air Products

- Bhuruka Gases