Edible Packaging Market Size

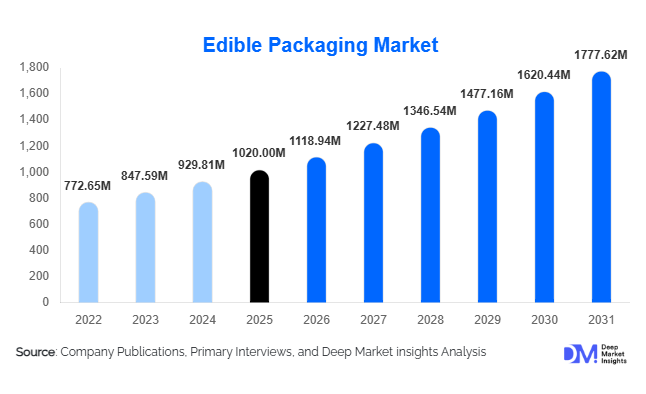

According to Deep Market Insights, the global edible packaging market size was valued at USD 1,020 million in 2025 and is projected to grow from USD 1,118.94 million in 2026 to reach USD 1,777.62 million by 2031, expanding at a CAGR of 9.7% during the forecast period (2026–2031). The edible packaging market growth is primarily driven by increasing regulatory restrictions on single-use plastics, rising consumer demand for sustainable and zero-waste packaging solutions, and growing adoption across the food processing and pharmaceutical industries. As sustainability commitments intensify globally, edible films and coatings derived from polysaccharides, proteins, and lipids are gaining commercial traction as viable alternatives to conventional plastic packaging. Technological improvements in barrier performance, moisture resistance, and antimicrobial functionality are further enhancing adoption across fresh produce, bakery, dairy, and nutraceutical applications.

Key Market Insights

- Polysaccharide-based edible films dominate the market, accounting for nearly 38% of global revenue in 2025 due to cost efficiency and scalability.

- Edible coatings represent the largest product form segment, contributing approximately 42% of total market share in 2025, driven by strong demand in fresh produce exports.

- North America leads the global market, holding around 34% of total revenue share in 2025, supported by strict plastic regulations and ESG adoption.

- Asia-Pacific is the fastest-growing region, expanding at over 11% CAGR, fueled by rising packaged food demand and government sustainability initiatives.

- Food & beverages remain the primary application, accounting for nearly 68% of total demand in 2025.

- The top five companies collectively account for approximately 46% of global market share, indicating moderate consolidation with innovation-driven competition.

What are the latest trends in the edible packaging market?

Shift Toward Functional and Active Edible Films

Manufacturers are increasingly integrating antimicrobial agents, natural antioxidants, probiotics, and oxygen scavengers into edible films and coatings. These functional enhancements extend shelf life by 15–30%, particularly in perishable categories such as fruits, vegetables, dairy, and meat products. Composite films combining polysaccharides and proteins are improving moisture barrier and mechanical strength, expanding commercial viability. The focus is shifting from basic biodegradable films to high-performance, multifunctional edible packaging solutions capable of competing with synthetic plastics.

Rising Adoption in Quick Service Restaurants (QSRs)

Quick service restaurant chains are piloting edible cutlery, dissolvable sachets, and edible condiment packaging as part of broader sustainability commitments. This trend is particularly prominent in North America and Europe, where brand image and ESG compliance are critical. Edible packaging offers a visible sustainability narrative that enhances consumer perception. Several QSR operators are integrating edible formats for sauces, seasonings, and single-serve packaging, accelerating commercialization beyond niche pilot projects.

What are the key drivers in the edible packaging market?

Stringent Global Plastic Regulations

More than 120 countries have introduced partial or full bans on single-use plastics, significantly accelerating demand for biodegradable and edible alternatives. Extended Producer Responsibility (EPR) frameworks in the European Union and North America are pushing food manufacturers to adopt sustainable packaging solutions. Compliance pressures are encouraging investment in edible film R&D and scalable production infrastructure.

Growing Consumer Preference for Sustainable Packaging

Over 60% of consumers globally express a preference for eco-friendly packaging. Millennials and Gen Z demographics, in particular, are influencing purchasing behavior by prioritizing brands aligned with zero-waste initiatives. Edible packaging directly addresses landfill waste reduction and carbon footprint concerns, positioning it as a premium sustainable solution.

What are the restraints for the global market?

High Production Costs

Edible packaging materials remain 20–40% more expensive than traditional plastic films due to limited economies of scale and specialized processing requirements. Scaling production facilities and reducing raw material processing costs remain critical to achieving broader market penetration.

Consumer Hygiene and Perception Concerns

Despite sustainability advantages, some consumers remain hesitant to consume packaging directly due to hygiene concerns. Clear labeling, regulatory approvals, and awareness campaigns are necessary to strengthen market acceptance.

What are the key opportunities in the edible packaging industry?

Expansion in the Asia-Pacific Food Processing Sector

Asia-Pacific represents the fastest-growing opportunity, driven by urbanization and the expansion of packaged food industries in China and India. Rising exports of fresh produce and processed foods are increasing demand for shelf-life-enhancing edible coatings. Localized production facilities can significantly reduce costs and enhance regional competitiveness.

Integration with Nutraceutical and Pharmaceutical Applications

The nutraceutical and pharmaceutical sectors present high-margin growth avenues, particularly for dissolvable films and capsule coatings. Oral thin films for vitamins and supplements are gaining traction, expanding edible packaging beyond traditional food applications.

Material Type Insights

Polysaccharide-based edible packaging leads the global market with approximately 38% share in 2025, driven by starch and cellulose availability and lower production costs. Protein-based films, including gelatin and whey protein formats, account for nearly 30% of total demand, benefiting from superior oxygen barrier properties. Composite films combining polysaccharides and proteins are gaining share due to enhanced mechanical strength and moisture resistance. Lipid-based coatings remain niche but are widely used in fruit coatings to prevent moisture loss.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1020 Million |

| Market Size in 2026 | USD 1118.94 Million |

| Market Size in 2031 | USD 1777.62 Million |

| CAGR | 9.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Edible coatings remain the leading product form, accounting for approximately 42% of global revenue in 2025. The primary driver behind this dominance is their seamless integration into existing food processing lines without requiring major packaging redesign. Coatings are widely adopted in fresh fruits, vegetables, meat, and dairy products because they extend shelf life by reducing moisture loss and oxidation while remaining invisible to consumers. Export-oriented agricultural economies such as India, Mexico, Spain, and Chile are major adopters, as edible coatings enhance cross-border shipment viability and reduce post-harvest losses by up to 20–30%.

Edible films represent nearly 35% of total market revenue, driven largely by demand in bakery, confectionery, and ready-to-eat food applications. These films provide oxygen barrier protection and portion control while reducing secondary plastic wrapping. Growth in premium packaged snacks and single-serve food formats is accelerating film adoption. Edible sachets and pouches are emerging strongly within quick service restaurants (QSRs) and instant beverage segments. Their adoption is driven by sustainability branding and regulatory compliance. Meanwhile, edible cutlery and containers remain in pilot phases but are gaining attention in event catering, airline catering, and institutional food services, supported by plastic bans and ESG commitments.

Application Insights

The food & beverages segment dominates with approximately 68% of total demand in 2025, valued at nearly USD 694 million. The primary growth driver is regulatory pressure to reduce plastic waste in food packaging, combined with food waste reduction initiatives. Fresh produce, bakery, dairy, and meat applications account for the largest share within this segment. Increasing global trade in perishable goods is significantly boosting demand for edible coatings that improve export durability.

Pharmaceutical applications contribute approximately 18% of global revenue in 2025, driven by oral dissolvable films and capsule coatings. Growth in nutraceutical consumption and patient-friendly drug delivery formats is strengthening this segment. Edible thin films are increasingly used for pediatric and geriatric medicines due to ease of consumption. Nutraceuticals and limited personal care applications represent smaller but rapidly expanding segments. Rising global demand for functional supplements, especially in North America and Asia-Pacific, is increasing demand for dissolvable vitamin films and edible delivery strips.

Distribution Channel Insights

Direct B2B sales dominate the market with 61% share in 2025, primarily because edible packaging solutions require customized formulations, technical validation, and regulatory documentation. Large food processors and pharmaceutical companies prefer direct procurement agreements to ensure compliance with FDA and EFSA standards and to maintain product consistency.

Ingredient suppliers and converters account for approximately 28% of market share, particularly in regions where localized blending and formulation are required. These intermediaries play a crucial role in scaling edible film production for mid-sized food manufacturers. Online B2B platforms are emerging as procurement channels for small and medium enterprises. Although currently accounting for less than 10% of total revenue, digital sourcing is expected to grow as standardized edible film formats become more widely available.

End-Use Industry Insights

Food processing companies account for approximately 55% of total demand in 2025, valued at nearly USD 560 million. The key driver for this segment is large-scale compliance with plastic reduction mandates and ESG targets. Major multinational food brands are integrating edible coatings and films to meet sustainability pledges while improving shelf stability. Quick service restaurant (QSR) chains represent the fastest-growing end-use segment, expanding at over 11% CAGR. Growth is fueled by public sustainability commitments and consumer-facing eco-branding strategies. Edible condiment sachets and cutlery are being piloted in urban markets across North America and Europe. Pharmaceutical manufacturers contribute around USD 180 million in 2025, supported by expanding oral thin film technologies. Nutraceutical companies are also experiencing double-digit growth due to increasing global demand for functional supplements and personalized nutrition products.

Explore more data points, trends and opportunities Download Free Sample Report

Edible Packaging Market Segmentations

By Material Type

- Polysaccharide-Based Edible Packaging

- Protein-Based Edible Packaging

- Lipid-Based Edible Packaging

- Composite Edible Films & Coatings

By Product Form

- Edible Films

- Edible Coatings

- Edible Sachets & Pouches

- Edible Cutlery & Containers

By Application

- Food & Beverages

- Pharmaceuticals

- Nutraceuticals

- Personal Care

By Distribution Channel

- Direct B2B Sales

- Ingredient Suppliers & Converters

- Online B2B Platforms

By End-Use Industry

- Food Processing Companies

- Quick Service Restaurants (QSRs)

- Pharmaceutical Manufacturers

- Nutraceutical Companies

- Retail & E-commerce Food Brands

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, making it the leading regional market. The United States accounts for nearly 78% of regional demand, driven by stringent state-level plastic bans, strong ESG disclosure requirements, and rapid adoption among QSR chains. High consumer awareness regarding sustainability and willingness to pay premium prices for eco-friendly packaging further support market expansion. Canada contributes significantly through fresh produce exports and packaged food manufacturing. The presence of leading innovators and R&D investments in biodegradable materials also strengthens regional competitiveness.

Europe

Europe represents around 29% of global revenue in 2025, driven primarily by regulatory enforcement under the EU Single-Use Plastics Directive and Circular Economy Action Plan. Germany accounts for roughly 22% of European demand, followed by France, the UK, Italy, and Spain. Strong government incentives for biodegradable material research and high consumer preference for sustainable packaging are major growth drivers. Additionally, Europe’s strong fresh produce export market supports demand for edible coatings to reduce spoilage during cross-border shipments.

Asia-Pacific

Asia-Pacific holds approximately 27% of the global share and is the fastest-growing region at over 11.5% CAGR. China and India are primary growth engines due to the rapid expansion of food processing industries, increasing urbanization, and rising packaged food consumption. Government initiatives promoting biodegradable materials and domestic manufacturing, such as sustainability-linked industrial policies, are accelerating investment in bio-based packaging production facilities. Japan and South Korea contribute through technological innovation in high-performance composite films.

Latin America

Latin America accounts for approximately 6% of global demand, with Brazil and Mexico leading adoption. The primary regional driver is export-oriented agriculture, particularly fruits and vegetables shipped to North America and Europe. Edible coatings reduce post-harvest losses and improve export margins, making them commercially attractive. Growing environmental regulations in Brazil are further supporting local adoption.

Middle East & Africa

The Middle East & Africa region represents nearly 4% of global revenue. The UAE and Saudi Arabia are driving premium food packaging demand due to strong QSR expansion and high-income consumer bases. In Africa, South Africa leads regional adoption through food processing and export-driven agriculture. Sustainability initiatives in Gulf countries and increasing foreign investment in food manufacturing are expected to gradually strengthen market penetration.