Food Packaging Market Size

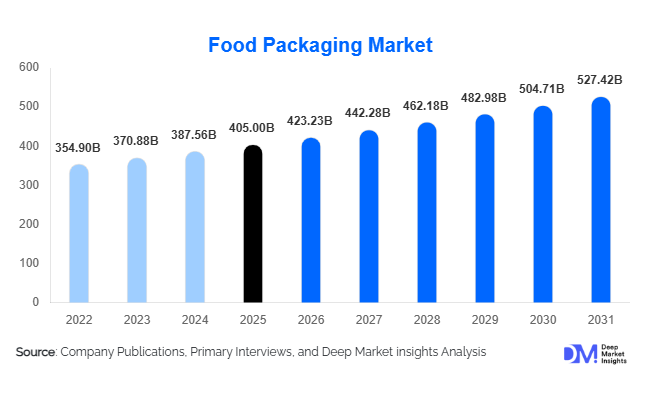

According to Deep Market Insights, the global food packaging market size was valued at USD 405 billion in 2025 and is projected to grow from USD 423.23 billion in 2026 to reach USD 527.42 billion by 2031, expanding at a CAGR of 4.5% during the forecast period (2026–2031). The food packaging market growth is primarily driven by rising consumption of processed and convenience foods, expansion of organized retail and e-commerce grocery platforms, and increasing regulatory emphasis on sustainable and recyclable packaging materials.

Key Market Insights

- Flexible plastic packaging dominates the market, accounting for nearly 43% of total demand due to cost efficiency, lightweight properties, and superior barrier protection.

- Asia-Pacific leads the global market, contributing approximately 38% of total revenue in 2025, supported by strong food processing growth in China and India.

- Plastic materials account for nearly 45% of total packaging consumption, although paper-based and compostable alternatives are gaining share under sustainability mandates.

- Ready-to-eat and processed foods represent the largest application segment, contributing about 22% of global demand.

- Top five companies collectively hold 22–25% market share, reflecting moderate consolidation with strong regional competition.

- Sustainability-driven innovation, including recyclable mono-material films and fiber-based trays, is reshaping product development pipelines.

What are the latest trends in the food packaging market?

Sustainable and Recyclable Packaging Acceleration

Food packaging manufacturers are rapidly transitioning toward recyclable, biodegradable, and compostable materials. Mono-material polyethylene and polypropylene laminates are replacing complex multi-layer films to improve recyclability. Paper-based barrier solutions are expanding in the bakery, dairy, and ready-meal segments. Governments in Europe and North America are enforcing extended producer responsibility (EPR) regulations, compelling manufacturers to redesign packaging formats. Brands are increasingly adopting post-consumer recycled (PCR) resins to meet corporate ESG targets, positioning sustainability as a long-term structural growth driver.

Smart and Active Packaging Integration

Technological innovation is transforming food safety and shelf-life management. Active packaging solutions such as oxygen scavengers, antimicrobial coatings, and modified atmosphere packaging (MAP) are seeing increased adoption in meat, seafood, and dairy products. Smart labels with QR codes and temperature indicators enhance traceability and consumer engagement. Automation and digital printing technologies are also improving customization, reducing turnaround time, and enabling short production runs for private-label brands.

What are the key drivers in the food packaging market?

Growth in Processed and Convenience Foods

Urbanization and busy consumer lifestyles are fueling demand for ready-to-eat meals, frozen foods, and snack products. The global processed food industry, valued at over USD 3 trillion, continues to expand at 5–6% annually, directly increasing packaging consumption. High-barrier flexible films and trays are particularly benefiting from this growth.

Expansion of Organized Retail and E-commerce

Supermarket chains and online grocery platforms require durable, lightweight, and protective packaging formats. Corrugated boxes and protective flexible packaging have witnessed sustained demand growth due to home delivery models. E-commerce grocery is expanding at over 10% CAGR globally, strengthening secondary packaging demand.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in crude oil prices impact polyethylene, polypropylene, and PET resin costs. Similarly, pulp and aluminum price volatility affects paperboard and metal packaging segments. Margin pressures remain a persistent challenge for converters.

Environmental Regulations on Plastics

Stringent bans on single-use plastics in certain regions require capital-intensive material transitions. Companies must invest heavily in R&D and retooling to comply with sustainability standards, potentially slowing short-term profitability.

What are the key opportunities in the food packaging industry?

Emerging Market Manufacturing Expansion

Rapid industrialization in India, Indonesia, Vietnam, and Africa presents opportunities for localized packaging production. Government-backed food parks and manufacturing incentives are reducing entry barriers and attracting foreign direct investment.

Smart & High-Barrier Packaging for Exports

Export-driven meat, seafood, and dairy industries require high-performance packaging to maintain product integrity across long supply chains. Advanced MAP solutions and recyclable high-barrier films offer strong growth potential.

Material Insights

Plastic packaging continues to dominate the global food packaging market, accounting for approximately 45% of total market revenue in 2025. The leadership of plastics is primarily driven by their superior barrier properties against moisture, oxygen, and contaminants, combined with lightweight structure and cost efficiency. Polyethylene (PE), polypropylene (PP), and PET-based materials are widely used in flexible films, pouches, bottles, and trays. The rapid growth of convenience foods, snacks, and frozen products has reinforced demand for multilayer flexible plastics capable of extending shelf life while maintaining product freshness. Additionally, lightweighting trends have reduced resin consumption per unit, improving cost-effectiveness for large-scale food processors.

Paper & paperboard represent the second-largest material segment, supported by sustainability mandates, plastic reduction policies, and rising demand for corrugated shipping boxes in e-commerce grocery. Fiber-based packaging is witnessing accelerated adoption in Europe and North America due to recyclability and consumer preference for environmentally responsible packaging. Metal packaging, particularly aluminum and tinplate cans, maintains strong demand in processed foods, canned vegetables, and ready meals due to durability and long shelf-life preservation. Glass packaging, while holding a smaller share, remains important in premium food categories such as sauces, baby food, and specialty beverages, where product visibility and chemical inertness are valued.

Packaging Type Insights

Flexible packaging leads the market with approximately 43% share in 2025, primarily driven by the rising consumption of ready-to-eat meals, snacks, dairy products, and frozen foods. Stand-up pouches, retort pouches, and laminated films offer cost efficiency, reduced transportation weight, and enhanced shelf appeal. The key driver behind flexible packaging growth is its ability to combine performance and sustainability, especially with the shift toward recyclable mono-material films.

Rigid packaging remains strong in dairy containers, beverage bottles, and glass jars, particularly where structural integrity and resealability are essential. Meanwhile, semi-rigid packaging such as thermoformed trays and clamshells is expanding rapidly in ready-meal and fresh produce segments. Growth in meal kits and chilled food categories continues to boost demand for high-clarity trays with modified atmosphere packaging (MAP) capabilities.

Application Insights

Ready-to-eat (RTE) and processed foods account for nearly 22% of total packaging demand, making it the leading application segment globally. The primary growth driver for this segment is urbanization, increasing dual-income households, and rising demand for convenience-oriented food consumption. High-barrier flexible films and microwaveable trays are particularly benefiting from this trend.

Dairy and meat applications follow closely, requiring advanced packaging technologies such as MAP and vacuum sealing to ensure safety and shelf life. Frozen foods and snack products are experiencing above-average growth due to retail expansion and online grocery penetration. Bakery and confectionery packaging remains stable but is increasingly transitioning toward recyclable paper-based materials to comply with sustainability standards.

End-Use Industry Insights

Food processing companies represent approximately 55% of total packaging procurement, forming the backbone of market demand. Large multinational food manufacturers and regional processors require a consistent high-volume supply of flexible films, cartons, and rigid containers. The key growth driver for this segment is global processed food industry expansion, particularly in emerging economies.

Quick-service restaurants (QSRs) and foodservice chains are among the fastest-growing end-use segments due to rapid urban expansion and delivery platform proliferation. E-commerce grocery is the fastest-growing distribution channel, expanding at over 10% CAGR, significantly increasing demand for corrugated secondary packaging and protective materials. Retail supermarkets maintain steady procurement volumes, while export-oriented food industries in the U.S., Brazil, China, and Germany drive demand for durable, temperature-resistant, and high-barrier packaging formats.

| By Material Type | By Packaging Type | By Application | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global food packaging market with approximately 38% market share in 2025 and is also the fastest-growing region, expanding at nearly 5.8–6% CAGR. China dominates regional demand due to its massive food manufacturing base and strong export activity in processed foods and seafood. Rapid urbanization, growth in modern retail, and rising disposable incomes are key growth drivers. India is the fastest-growing major market within the region, expanding at a 6–7% CAGR, supported by government-backed food processing initiatives and the “Make in India” manufacturing push. Japan and South Korea contribute stable, high-value demand, particularly in premium and technologically advanced packaging solutions, including smart and active packaging formats.

North America

North America accounts for approximately 25% of global market revenue, with the United States contributing the majority share. The region’s growth is driven by high per capita consumption of processed and frozen foods, advanced retail infrastructure, and strong adoption of sustainable packaging innovations. Stringent recycling mandates and ESG commitments are accelerating investments in recyclable plastics and fiber-based packaging. Canada demonstrates stable demand in dairy and frozen food packaging, while Mexico benefits from food export activities and manufacturing expansion.

Europe

Europe represents around 22% of global demand, led by Germany, France, the U.K., and Italy. Regional growth is strongly influenced by regulatory drivers, including EU directives targeting plastic waste reduction and circular economy goals. These policies are accelerating the adoption of paper-based packaging, compostable materials, and recycled content plastics. Advanced automation and technological integration in packaging facilities also support efficiency improvements across Western Europe.

Latin America

Latin America is an emerging growth region, led by Brazil and Mexico. Brazil’s strong meat and poultry export industry drives demand for high-barrier vacuum and MAP packaging. Expansion of organized retail and rising middle-class consumption in Mexico further stimulates flexible packaging demand. Economic stabilization and trade agreements are supporting gradual investment in domestic food processing capacity.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, driven by rising food imports, urbanization, and increasing investment in domestic food processing. Saudi Arabia and the UAE are investing in food security initiatives and local manufacturing, boosting packaging consumption. South Africa remains the leading Sub-Saharan market, supported by retail expansion and export-driven agricultural industries. Infrastructure development and population growth across the region continue to provide long-term demand support for packaged food products.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Food Packaging Market

- Amcor

- Berry Global

- Sealed Air

- Mondi Group

- Sonoco Products Company

- Smurfit Westrock

- Huhtamaki

- Tetra Pak

- Ball Corporation

- Crown Holdings

- DS Smith

- Silgan Holdings

- Constantia Flexibles

- Winpak

- Coveris