Beverage Packaging Market Size

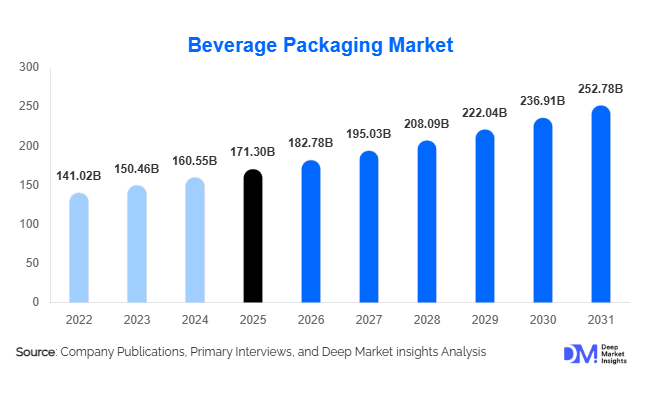

According to Deep Market Insights, the global beverage packaging market size was valued at USD 171.3 billion in 2025 and is projected to grow from USD 182.78 billion in 2026 to reach USD 252.78 billion by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The beverage packaging market growth is primarily driven by increasing consumption of packaged beverages, rising demand for sustainable and recyclable packaging solutions, and rapid technological advancements in lightweight, smart, and aseptic packaging systems. Growing urbanization, changing consumer lifestyles, and expanding ready-to-drink beverage categories are accelerating investments in innovative packaging formats across both developed and emerging economies.

Key Market Insights

- Sustainable and recyclable packaging solutions are becoming central to beverage packaging strategies, with global beverage brands increasingly adopting recycled PET, aluminum cans, and biodegradable materials.

- Ready-to-drink beverages and functional drinks are driving packaging innovation, particularly in lightweight bottles, slim cans, and aseptic cartons.

- Asia-Pacific dominates the global beverage packaging market, supported by rapid beverage consumption growth in China and India.

- Europe remains the leading region for sustainable beverage packaging innovation, driven by strict recycling regulations and circular economy initiatives.

- Smart packaging technologies are gaining momentum, including QR-enabled labels, traceability systems, and interactive packaging for consumer engagement.

- E-commerce beverage delivery is reshaping packaging demand, encouraging the adoption of durable, lightweight, and protective transport packaging solutions.

Beverage Packaging Market Latest Trends

Sustainable Packaging Adoption Accelerating Globally

Sustainability has become one of the most influential trends shaping the global beverage packaging market. Beverage companies are increasingly replacing virgin plastics with recycled PET (rPET), aluminum cans, paper-based cartons, and compostable packaging materials to meet regulatory requirements and consumer expectations. Governments across Europe and North America are implementing strict packaging waste reduction targets and recycled content mandates, accelerating investments in circular economy packaging infrastructure. Lightweight packaging formats are also gaining traction as manufacturers seek to reduce carbon emissions and transportation costs. Major beverage brands are adopting reusable bottle systems and expanding closed-loop recycling initiatives to strengthen sustainability commitments and improve environmental performance.

Smart and Digitally Connected Packaging Expanding

Digitalization is transforming beverage packaging through the integration of smart labels, QR codes, NFC-enabled packaging, and AI-powered traceability systems. Beverage companies are increasingly using connected packaging to enhance customer engagement, provide product authentication, and improve supply chain visibility. Smart packaging solutions are particularly important in premium alcoholic beverages, where anti-counterfeit technologies are becoming essential. QR-enabled beverage packaging also supports personalized marketing campaigns, sustainability education, and consumer interaction. Digital printing technologies are enabling shorter production runs, customized packaging designs, and faster product launches, supporting beverage brands seeking differentiation in highly competitive retail environments.

Beverage Packaging Market Drivers

Rising Consumption of Packaged Beverages

The growing global demand for packaged beverages remains a major driver of the beverage packaging market. Urbanization, increasing disposable incomes, and changing dietary habits are fueling consumption of bottled water, carbonated drinks, energy beverages, ready-to-drink tea and coffee, and functional beverages. Emerging economies such as China, India, Indonesia, and Brazil are witnessing rapid growth in packaged beverage demand due to expanding middle-class populations and improving retail infrastructure. Beverage manufacturers are increasing production capacities, directly supporting higher demand for bottles, cans, cartons, and flexible packaging formats.

Growing Demand for Sustainable and Lightweight Packaging

Consumers and regulators are placing increasing pressure on beverage companies to reduce packaging waste and improve sustainability performance. This has accelerated the adoption of recyclable aluminum cans, paper-based beverage cartons, lightweight PET bottles, and biodegradable packaging solutions. Lightweight packaging technologies reduce transportation costs and improve supply chain efficiency while lowering carbon emissions. Beverage manufacturers are also investing heavily in recycled materials and mono-material packaging systems to comply with evolving sustainability regulations and improve recyclability.

Global Market Restraints

Raw Material Price Volatility

Fluctuations in raw material prices continue to challenge beverage packaging manufacturers globally. Prices of aluminum, PET resin, glass manufacturing energy inputs, and paper pulp are highly sensitive to geopolitical disruptions, energy costs, and global supply chain instability. Sudden price increases directly affect packaging production costs and reduce operating margins for manufacturers. Smaller packaging companies are particularly vulnerable to raw material price swings due to limited procurement scale and lower bargaining power.

Increasing Regulatory Pressure on Plastic Packaging

Governments worldwide are implementing stringent regulations aimed at reducing plastic waste and improving recycling rates. Plastic taxes, mandatory recycled content requirements, and extended producer responsibility regulations are increasing compliance costs for beverage packaging companies. Manufacturers must invest heavily in recycling infrastructure, sustainable materials research, and packaging redesign initiatives to meet evolving environmental standards. These regulatory pressures are especially significant in Europe and North America, where sustainability compliance requirements are becoming increasingly complex.

Beverage Packaging Industry Key Opportunities

Expansion of Functional and Ready-to-Drink Beverages

The rapid growth of functional beverages, energy drinks, protein beverages, and ready-to-drink coffee and tea products presents substantial opportunities for beverage packaging manufacturers. These premium beverage categories require advanced packaging formats with strong barrier protection, portability, resealability, and premium shelf appeal. Slim aluminum cans, aseptic cartons, stand-up pouches, and lightweight PET bottles are benefiting significantly from this trend. Beverage packaging companies investing in premium and convenience-oriented packaging technologies are expected to capture strong long-term growth opportunities.

Growth in Circular Economy Packaging Infrastructure

Investments in recycling systems, reusable packaging networks, and circular economy infrastructure are creating major opportunities across the global beverage packaging market. Governments and beverage producers are increasingly supporting closed-loop recycling initiatives and deposit-return systems to improve collection and recycling rates. Companies specializing in recycled PET processing, aluminum recycling, and sustainable material innovation are expected to benefit significantly from these initiatives. Growing consumer awareness regarding sustainable packaging is also encouraging beverage brands to prioritize environmentally responsible packaging solutions.

Packaging Material Insights

Plastic packaging remains the dominant material segment in the beverage packaging market, accounting for nearly 41% of global market demand in 2025. PET bottles continue to lead due to their lightweight structure, low production cost, durability, and compatibility with high-speed beverage filling systems. Plastic packaging is particularly dominant in bottled water, carbonated soft drinks, and juice applications because of transportation efficiency and convenience. However, sustainability concerns are gradually shifting industry focus toward recycled PET and bio-based plastics. Aluminum packaging is experiencing strong growth due to its high recyclability and increasing adoption in energy drinks and ready-to-drink alcoholic beverages. Glass packaging continues to maintain a strong presence in premium alcoholic beverages, particularly wine and spirits, where brand image and product preservation remain critical.

Packaging Type Insights

Bottles represent the leading packaging type globally, contributing approximately 38% of total beverage packaging market share in 2025. Plastic bottles dominate mass-market beverage categories such as bottled water and carbonated drinks, while glass bottles remain preferred for premium beverages and alcoholic products. Aluminum cans are rapidly gaining popularity due to sustainability benefits, portability, and strong demand from energy drink and ready-to-drink beverage manufacturers. Carton packaging, especially aseptic cartons, is witnessing rising demand in dairy beverages, plant-based drinks, and juices due to extended shelf life and lower refrigeration requirements. Flexible pouches and bag-in-box systems are also expanding in niche beverage applications because of cost efficiency and reduced packaging waste.

Beverage Type Insights

Non-alcoholic beverages dominate the global beverage packaging market, accounting for nearly 67% of total market demand in 2025. Bottled water remains the largest contributor due to rising health awareness and increasing concerns regarding water quality in emerging markets. Functional beverages, energy drinks, ready-to-drink coffee, and plant-based beverages are among the fastest-growing beverage categories globally, driving demand for innovative and sustainable packaging formats. Alcoholic beverages continue to generate strong demand for premium glass bottles and aluminum cans, particularly in beer, wine, spirits, and ready-to-drink cocktail segments. The growing popularity of hard seltzers and low-alcohol beverages is further supporting innovation in lightweight and recyclable packaging solutions.

Technology Insights

Aseptic packaging is emerging as one of the fastest-growing technology segments in the beverage packaging market, accounting for nearly 19% of total market demand in 2025. Aseptic packaging technologies enable extended shelf life without refrigeration or preservatives, making them highly suitable for dairy beverages, juices, plant-based drinks, and functional beverages. Smart packaging technologies are also gaining traction, particularly in premium beverage categories where QR-enabled labels, freshness indicators, and traceability systems enhance customer engagement and supply chain transparency. Lightweight packaging technology continues to play a critical role in reducing logistics costs and improving sustainability performance across beverage supply chains.

Sustainability Insights

Recyclable packaging accounted for approximately 46% of the global beverage packaging market in 2025, reflecting the industry's increasing emphasis on sustainability and circular economy initiatives. Beverage brands are prioritizing recyclable aluminum cans, recycled PET bottles, and paper-based cartons to meet regulatory requirements and environmental goals. Reusable packaging systems are also gaining traction in developed markets, particularly in Europe, where refillable bottle networks and deposit-return schemes are expanding rapidly. Compostable and biodegradable beverage packaging materials are emerging as niche but rapidly growing segments driven by sustainability-focused consumers and regulatory support.

| By Packaging Material | By Packaging Type | By Beverage Type | By Packaging Technology | By Sustainability Type |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for nearly 24% of the global beverage packaging market in 2025, driven primarily by strong beverage consumption in the United States and Canada. The region is witnessing increasing demand for sustainable packaging solutions, particularly aluminum cans, recyclable PET bottles, and paper-based cartons. Functional beverages, ready-to-drink coffee, and premium alcoholic beverages are major growth drivers supporting packaging innovation. Beverage companies in North America are heavily investing in recycling infrastructure, lightweight packaging technologies, and smart packaging solutions to meet sustainability targets and consumer expectations.

Europe

Europe remains a leading market for sustainable beverage packaging innovation, accounting for approximately 27% of global market share in 2025. Germany, France, the United Kingdom, and Italy are major contributors to regional demand due to strong beverage industries and strict environmental regulations. Europe is leading the adoption of recycled packaging materials, deposit-return systems, and circular economy initiatives. Premium alcoholic beverages, bottled water, and dairy beverages continue to support strong demand for glass bottles, aluminum cans, and aseptic cartons across the region.

Asia-Pacific

Asia-Pacific dominates the global beverage packaging market with nearly 39% market share in 2025 and remains the fastest-growing regional market globally. China leads regional demand due to its large beverage manufacturing industry and rapidly expanding packaged beverage consumption. India is witnessing exceptionally strong growth driven by urbanization, rising disposable incomes, and increasing demand for bottled water, dairy beverages, and energy drinks. Japan and South Korea are major adopters of smart and sustainable beverage packaging technologies. Expanding retail infrastructure and growing e-commerce beverage sales are further supporting market growth across Southeast Asia.

Latin America

Latin America is experiencing steady growth in beverage packaging demand, led by Brazil and Mexico. Brazil’s strong beer and soft drink industries continue to support high demand for aluminum cans and PET bottles. Mexico remains a major exporter of alcoholic beverages and packaged drinks, increasing demand for premium glass and metal packaging solutions. Rising consumption of bottled water and energy drinks is also supporting packaging investments across the region.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth market for beverage packaging, supported by rising urbanization, tourism growth, and increasing bottled water consumption. Saudi Arabia, UAE, and South Africa are major regional contributors. Growing investments in foodservice, hospitality, and retail infrastructure are accelerating demand for sustainable and lightweight beverage packaging solutions. Africa is also witnessing increasing adoption of affordable flexible packaging formats due to expanding middle-class populations and improving beverage distribution networks.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Beverage Packaging Market

- Amcor

- Ball Corporation

- Crown Holdings

- Tetra Pak

- Ardagh Group

- O-I Glass

- Berry Global

- Silgan Holdings

- Smurfit Westrock

- SIG Group

- CANPACK

- Alpla Group

- Sonoco Products Company

- Nampak

- Krones AG