Food Packaging Technology & Equipment Market Size

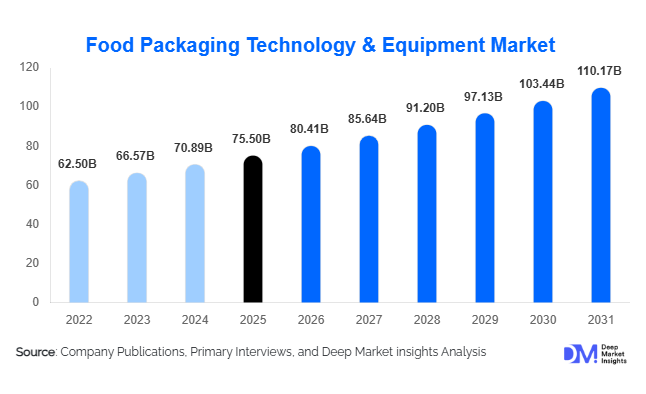

According to Deep Market Insights, the global food packaging technology & equipment market size was valued at USD 75.5 billion in 2025 and is projected to grow from USD 80.41 billionin 2026 to reach USD 110.17 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The market growth is primarily driven by rising packaged food consumption, increasing automation in food processing, and the adoption of smart and sustainable packaging solutions by manufacturers worldwide.

Key Market Insights

- Flexible packaging dominates globally, due to its cost-efficiency, lightweight design, and versatility across beverages, snacks, and frozen foods, capturing a 32% share of the 2025 market.

- Form-Fill-Seal machines lead technology adoption, with 28% market share, enabling manufacturers to improve production speed, hygiene, and precision across multiple food types.

- North America accounts for a significant share, led by the U.S. and Canada, where stringent safety regulations and high automation adoption drive equipment demand.

- Asia-Pacific is the fastest-growing region, fueled by rising urbanization, export-oriented food manufacturing, and investments in modern packaging lines in China, India, and Japan.

- Sustainable packaging adoption, including biodegradable and recyclable materials, is reshaping industry priorities, particularly in Europe and North America.

- Technological integration, such as IoT-enabled equipment, smart packaging, and automated quality inspection, is transforming operational efficiency and traceability in food supply chains.

What are the latest trends in the food packaging technology & equipment market?

Smart and IoT-Enabled Packaging Solutions

Manufacturers are increasingly investing in IoT-enabled packaging systems that offer real-time monitoring of product freshness, temperature control, and supply chain traceability. Smart packaging with QR codes, sensors, and RFID tags is gaining adoption in beverages, dairy, and ready-to-eat foods. These innovations not only enhance consumer engagement but also support compliance with food safety regulations and reduce spoilage during transportation. Companies integrating smart technology can differentiate their offerings and capture high-margin contracts from large-scale food manufacturers and exporters.

Sustainability and Biodegradable Packaging

Eco-friendly and recyclable materials are becoming central to food packaging strategies. Biodegradable films, compostable trays, and recyclable plastics are increasingly preferred due to regulatory pressures and consumer environmental awareness. Advanced equipment capable of handling these new materials is in high demand, creating opportunities for equipment suppliers to provide innovative machinery for sustainable packaging. Europe leads adoption, while North America and Asia-Pacific follow closely, driven by both policy mandates and market preference for green packaging.

What are the key drivers in the food packaging technology & equipment market?

Rising Packaged Food Consumption

The growing demand for convenience foods, ready-to-eat meals, beverages, and snacks is directly driving the need for advanced packaging equipment. Urban lifestyles and e-commerce expansion are boosting the consumption of packaged foods across both developed and emerging markets. This surge necessitates machinery capable of high-speed production, automated filling, sealing, and labeling to meet quality and safety standards efficiently.

Regulatory Compliance and Food Safety

Stringent food safety regulations from bodies like the FDA in the U.S., EFSA in Europe, and ISO food safety standards worldwide are prompting manufacturers to invest in advanced packaging equipment. Automated and hygienic solutions reduce contamination risks, ensure traceability, and comply with regulatory mandates, which in turn supports overall market growth.

Technological Advancements

Innovations in form-fill-seal machines, automated labeling, vacuum and modified-atmosphere packaging, and integrated quality inspection are boosting efficiency and product shelf life. The adoption of robotics, AI, and vision-based inspection systems is also enhancing operational productivity while minimizing labor dependency, offering a strong impetus to market expansion.

What are the restraints for the global market?

High Capital Investment

Advanced packaging machinery and automation systems require significant upfront investment, which can be a barrier for small- and medium-sized manufacturers. The costs of installation, training, and maintenance can limit adoption, particularly in emerging economies.

Raw Material Price Volatility

Fluctuating prices of plastics, aluminum, paper, and eco-friendly materials impact overall production costs. This volatility can affect profit margins and may slow down investment in new packaging technologies, especially for high-volume manufacturers.

What are the key opportunities in the food packaging technology & equipment industry?

Expansion in Emerging Economies

Rising urbanization, increasing disposable income, and growing food processing industries in countries like India, Brazil, and Nigeria are creating significant demand for packaging machinery. Export-driven manufacturing hubs are also pushing the adoption of automated and high-efficiency equipment, offering opportunities for both local and global equipment suppliers.

Integration of Smart Technologies

IoT, sensors, and digital monitoring systems are enabling real-time quality control and supply chain visibility. Manufacturers investing in smart packaging equipment can gain competitive advantages, reduce product spoilage, and enhance traceability for global exports.

Sustainability-Focused Equipment Upgrades

Environmental regulations and consumer preference for green packaging are driving demand for machinery that handles biodegradable, recyclable, and compostable materials. Companies offering advanced machinery for eco-friendly packaging are positioned to capture premium market segments while aligning with global sustainability initiatives.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 75.5 Billion |

| Market Size in 2026 | USD 80.41 Billion |

| Market Size in 2031 | USD 110.17 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Flexible packaging remains the dominant product type in the food packaging technology & equipment market, accounting for approximately 32% of the global market in 2025. Its leadership is primarily driven by cost efficiency, lightweight properties, extended shelf-life capabilities, and superior barrier performance against moisture and oxygen. The rapid growth of snack foods, frozen products, and single-serve beverages has further accelerated demand for pouching, bagging, and film-based solutions. Additionally, flexible packaging reduces logistics costs due to lower material usage and improved pallet optimization, making it particularly attractive for export-driven food manufacturers.

From a technology standpoint, form-fill-seal (FFS) machines lead with nearly 28% share of the global equipment market. Their dominance is attributed to high production speeds, automation compatibility, hygienic design, and the ability to integrate filling, sealing, and labeling in a single continuous process. Food manufacturers increasingly prefer FFS systems because they reduce contamination risk, minimize material wastage, and lower labor dependency. The growing demand for high-volume packaged foods in emerging economies has further strengthened FFS adoption.

Application Insights

The market serves a broad range of applications, including beverages, dairy, frozen foods, bakery & confectionery, meat & poultry, fruits & vegetables, and ready-to-eat (RTE) products. Among these, beverages remain the most equipment-intensive application, due to complex liquid filling, capping, sealing, labeling, and sterilization requirements. High throughput requirements in carbonated and non-carbonated drink production lines significantly increase machinery demand. Dairy and frozen foods follow closely, driven by stringent hygiene standards, cold chain integration, and modified atmosphere packaging (MAP) requirements to extend shelf life. Growth in urban convenience food consumption is pushing RTE and frozen food packaging demand at a strong pace globally.

Emerging applications such as nutraceuticals, functional foods, and plant-based ready meals are creating incremental opportunities. These segments require precision dosing, traceability coding, tamper-evident sealing, and export-grade quality inspection systems. In export-oriented markets, automated inspection technologies such as metal detection, X-ray scanning, and checkweighers are becoming mandatory to comply with international standards, further boosting demand for integrated packaging lines.

Distribution Channel Insights

Direct sales remain the dominant distribution channel, particularly for large-scale food processors and multinational beverage manufacturers. Equipment suppliers typically offer turnkey packaging solutions, installation, training, and long-term service contracts, which enhance customer retention and recurring revenue streams. Customized machinery and integrated production lines are commonly procured through direct manufacturer engagement. Industrial distributors play a significant role in serving small and medium-sized enterprises (SMEs), particularly in emerging markets where localized support and financing flexibility are critical. These distributors often provide mid-range machinery and retrofit solutions to upgrade existing production lines.

Online B2B platforms are gradually emerging as supplementary sales channels, especially for modular and mid-sized equipment. Digital platforms enable easier comparison of technical specifications, pricing transparency, and global supplier access. Furthermore, bundled maintenance, predictive servicing, and spare parts supply agreements are becoming central to competitive differentiation, as operational uptime is critical in food manufacturing environments.

End-Use Industry Insights

Food & beverage manufacturers dominate the market with approximately 55% share, driven by mass production requirements, regulatory compliance needs, and expanding export volumes. Large beverage bottlers, dairy processors, and ready-to-eat meal producers are investing heavily in automated filling, sealing, labeling, and inspection systems to enhance efficiency and reduce contamination risks.

Retail chains and private-label food brands are also influencing packaging investments, as supermarkets increasingly demand customized packaging formats and traceability compliance. The HoReCa segment is witnessing moderate but steady growth, particularly in urban centers where packaged food distribution to hospitality chains is expanding. New high-growth end-use industries include nutraceuticals, plant-based protein foods, and ready-to-drink health beverages. These industries require advanced packaging technologies for small-batch precision filling, premium packaging aesthetics, and longer shelf life, creating high-margin opportunities for equipment suppliers.

Explore more data points, trends and opportunities Download Free Sample Report

Food Packaging Technology & Equipment Market Segmentations

By Packaging Type

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

By Technology / Equipment Type

- Filling & Dosing Equipment

- Form-Fill-Seal Machines

- Sealing & Capping Equipment

- Labeling & Coding Equipment

- Inspection & Quality Control Systems

By Packaging Material

- Plastic

- Glass

- Metal (Aluminum & Tin)

- Paper & Cardboard

- Biodegradable & Compostable Materials

By Food Type

- Beverages

- Dairy & Frozen Foods

- Bakery & Confectionery

- Meat, Poultry & Seafood

- Fruits & Vegetables

- Ready-to-Eat & Processed Foods

By End-Use Industry

- Food & Beverage Manufacturing

- Retail & Private Label Brands

- HoReCa (Hotels, Restaurants, Catering)

- Nutraceutical & Functional Food Producers

Regional Insights

North America

North America accounts for approximately 28% of the global market in 2025, led by the United States and Canada. Regional growth is primarily driven by stringent food safety regulations, high packaged food consumption per capita, and strong automation penetration across food processing facilities. The U.S. market benefits from advanced technological adoption, including IoT-enabled packaging lines and AI-based inspection systems. Additionally, sustainability mandates and corporate ESG commitments are accelerating investment in recyclable and biodegradable packaging machinery. The presence of leading global equipment manufacturers and strong private CapEx in factory modernization further supports steady growth in the region.

Europe

Europe holds approximately 26% market share, with Germany, France, Italy, and the U.K. as key contributors. Regional growth is strongly driven by strict EU environmental directives, circular economy policies, and sustainability targets. Demand for machinery compatible with compostable and recyclable materials is highest in this region. Europe also has a strong export-oriented food industry, which requires high-precision, quality-controlled packaging solutions. Automation upgrades, robotics integration, and compliance with advanced traceability standards are major growth drivers across Western Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at an estimated 8% CAGR. China, India, Japan, and South Korea lead demand due to rapid urbanization, growing middle-class consumption, and increasing packaged food exports. Government initiatives promoting domestic manufacturing and food processing infrastructure modernization are accelerating equipment investments. Rising foreign direct investment (FDI) in food processing and the expansion of high-speed automated production lines further strengthen regional growth. Export demand from Southeast Asia also drives the adoption of inspection and compliance-focused packaging machinery.

Latin America

Latin America accounts for approximately 10% of the global market, led by Brazil, Mexico, and Argentina. Growth drivers include rising urban packaged food consumption, supermarket expansion, and export of processed foods to North America and Europe. Currency stabilization and modernization of domestic food manufacturing facilities are supporting gradual upgrades to automated packaging lines. The beverage industry in Brazil and Mexico remains a particularly strong demand contributor.

Middle East & Africa

The Middle East & Africa region represents a developing but promising market. The Middle East, particularly the UAE and Saudi Arabia, is witnessing increased investment in premium food processing and packaging to reduce import dependency and support food security initiatives. High disposable income and growing demand for packaged premium foods are boosting machinery imports. In Africa, South Africa, Egypt, and Nigeria are emerging processing hubs, driven by agricultural exports and urban consumption growth. Cold chain expansion and food safety improvements are key regional drivers, encouraging adoption of modern filling, sealing, and inspection technologies.

Key Players in the Food Packaging Technology & Equipment Market

- Tetra Pak

- Bosch Packaging Technology

- Multivac

- Barry-Wehmiller / Hayssen

- Ishida Co.

- Coesia Group

- ProMach

- Krones AG

- Fuji Machinery

- Marchesini Group

- Syntegon Technology

- Optima Packaging Group

- Omori Machinery

- GEA Group

- IMA Group