Fresh Food Preservation Gases Market Size

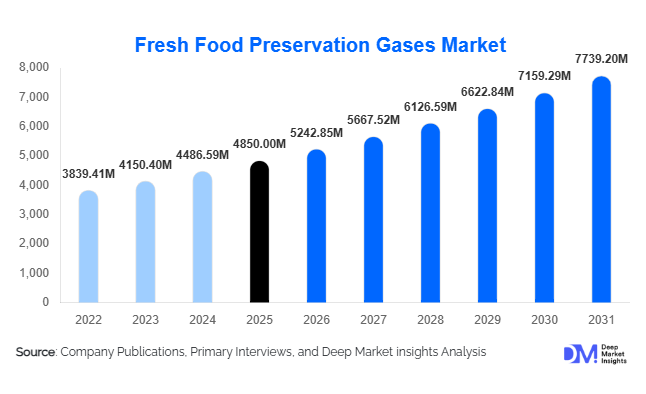

According to Deep Market Insights,the global fresh food preservation gases market size was valued at USD 4,850 million in 2026 and is projected to grow from USD 5,242.85 million in 2026 to reach USD 7,739.20 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for extended shelf-life solutions, increased global trade of perishable food products, and expanding adoption of modified atmosphere and controlled atmosphere storage technologies in both developed and emerging economies.

Key Market Insights

- Carbon dioxide and nitrogen dominate as preferred preservation gases, used extensively across meat, poultry, seafood, and fresh produce to prevent microbial growth and maintain product freshness.

- Modified atmosphere packaging (MAP) is the leading technology, widely adopted in retail-ready packaging, large-scale processing, and export-oriented supply chains.

- Food processing companies represent the largest end-use industry, relying on continuous gas supply for large-scale packaging and cold storage operations.

- Europe and North America lead market share, supported by advanced cold chain infrastructure, stringent food safety regulations, and high per capita meat and fresh produce consumption.

- Asia-Pacific is the fastest-growing region, driven by rising export demand, expanding retail infrastructure, and increasing awareness of food quality and safety standards.

- Technological adoption, including on-site nitrogen generation, gas blending systems, and IoT-enabled atmosphere monitoring, is enhancing operational efficiency and product consistency.

What are the latest trends in the fresh food preservation gases market?

Adoption of Sustainable and Green Gas Solutions

Food processors and gas suppliers are increasingly exploring sustainable production and delivery methods. Green CO₂ captured from bioethanol plants, low-carbon nitrogen generation, and renewable-powered gas production units are becoming mainstream, driven by environmental regulations and corporate sustainability goals. Companies integrating these green solutions can reduce operational carbon footprints while appealing to eco-conscious clients and exporters requiring compliance with global sustainability standards.

IoT-Enabled Gas Monitoring and Smart Packaging

Emerging smart packaging technologies integrated with IoT sensors are transforming fresh food preservation. Sensors continuously monitor oxygen, carbon dioxide, and nitrogen levels within packaging or cold storage units to ensure optimal preservation. This trend improves shelf life, reduces waste, and allows remote monitoring of perishable goods during transportation. Leading processors are adopting these technologies to strengthen quality control and build trust with retailers and international buyers.

What are the key drivers in the fresh food preservation gases market?

Rising Export Demand for Perishable Foods

Increasing international trade of meat, seafood, fruits, and vegetables is a major growth driver. Preservation gases enable extended shelf life and compliance with import quality standards, particularly for long-haul shipments from Asia-Pacific and Latin America to Europe and North America. This trend is amplified by growing demand from e-commerce platforms and organized retail chains requiring consistent freshness during distribution.

Consumer Preference for Clean-Label Foods

Consumers worldwide are seeking preservative-free, minimally processed foods. Fresh food preservation gases such as CO₂ and nitrogen provide an alternative to chemical additives, enabling processors to maintain freshness and natural quality. The clean-label trend encourages adoption across meat, seafood, bakery, and fresh-cut produce segments.

Expansion of Cold Chain Infrastructure

Investments in refrigerated logistics, cold storage warehouses, and controlled atmosphere facilities in emerging economies such as India, China, and Southeast Asia are boosting market growth. These infrastructures ensure the effective application of preservation gases, supporting consistent supply and reduced spoilage rates, thus enhancing profitability for food processors and exporters.

What are the restraints for the global market?

Volatility in Industrial Gas Prices

Fluctuations in CO₂ and specialty gas prices due to production constraints, plant shutdowns, or geopolitical factors can impact operational costs for processors. High price variability limits adoption in cost-sensitive markets, particularly among small and medium-sized enterprises.

High Capital Expenditure Requirements

Advanced gas blending systems, on-site nitrogen generators, and smart packaging technologies require significant initial investment. This can slow market penetration in developing regions where small-scale food processors dominate.

What are the key opportunities in the fresh food preservation gases market?

Expansion into Emerging Retail and E-Commerce Markets

Rapidly growing organized retail and online grocery platforms in India, Southeast Asia, and Latin America present significant opportunities. Establishing local gas supply infrastructure and cold chain integration enables companies to capture untapped regional demand while meeting international export standards.

Premium and Export-Oriented Food Segments

High-value seafood, organic produce, and plant-based protein products require specialized gas mixtures and intelligent packaging solutions. Tailored offerings allow suppliers to tap niche, high-margin markets, while IoT-enabled monitoring services create additional revenue streams through value-added solutions.

Integration of Sustainable Technologies

Green CO₂ capture, renewable-powered nitrogen generation, and carbon-neutral gas solutions offer a strategic advantage. Governments’ sustainability initiatives and corporate ESG targets present opportunities to position environmentally friendly preservation solutions as a competitive differentiator.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4850 Million |

| Market Size in 2026 | USD 5242.85 Million |

| Market Size in 2031 | USD 7739.20 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Carbon dioxide dominates the global food preservation gases market and remains the leading product type due to its strong antimicrobial properties, ability to inhibit bacterial and fungal growth, and effectiveness in extending shelf life across meat, poultry, and bakery applications. Its high solubility in water and fat makes it particularly suitable for modified atmosphere packaging (MAP), where it reduces spoilage and maintains product freshness during transportation and storage. The dominance of carbon dioxide is primarily driven by the expanding global demand for packaged meat and processed protein products, coupled with increasing regulatory emphasis on food safety and waste reduction. Nitrogen follows closely, widely adopted for inert gas flushing and oxygen displacement in fresh produce, seafood, snack foods, and dairy applications. Its non-reactive nature prevents oxidation and rancidity, making it essential for maintaining product texture and flavor integrity. Specialty gas mixtures are gaining traction in premium and export-oriented segments, including high-value seafood, organic produce, and customized packaging solutions that require precise atmospheric control. These blends are tailored to optimize respiration rates, color stability, and microbial control for specific products. Argon and oxygen are selectively utilized in niche markets, particularly for premium meat color retention and enhanced product differentiation strategies, supporting branding initiatives in high-end retail segments.

Application Insights

Meat and poultry applications account for the largest share of the market, representing approximately 34% in 2025, driven by rising global protein consumption, strict food safety standards, and the need for color preservation and extended distribution cycles. The leading driver for this segment is the rapid expansion of organized retail and international meat trade, which requires advanced packaging technologies to maintain freshness across long supply chains. Fresh fruits and vegetables are increasingly adopting preservation gases to minimize post-harvest losses, regulate respiration rates, and extend shelf life, particularly in export-oriented horticulture markets. Dairy and bakery segments are integrating gas-based packaging solutions to prevent mold growth, oxidation, and spoilage, especially for sliced bread, cheese, and ready-to-sell retail packs. Ready-to-eat and processed fresh foods are emerging as high-growth applications, supported by urbanization, rising disposable incomes, and the growing preference for convenience foods. The expansion of e-commerce grocery platforms and meal-kit delivery services further strengthens the demand for reliable preservation gas solutions across diversified food categories.

Distribution Channel Insights

Industrial bulk supply remains the dominant distribution channel, primarily serving large-scale food processing companies operating under long-term volume contracts. This segment’s leadership is driven by continuous production requirements, cost efficiencies in bulk procurement, and centralized processing facilities. On-site gas generation systems are gaining increasing preference among integrated processing plants seeking to reduce logistics dependency, improve supply reliability, and optimize operational costs. This trend is particularly strong in regions with developed food processing clusters. Cylinder and packaged gas supply continues to serve small and medium-sized enterprises and regional food processors, especially in emerging markets where infrastructure limitations restrict bulk storage capabilities. The growth of decentralized food manufacturing units and regional packaging facilities supports steady demand within this channel.

End-Use Insights

Food processing companies represent the largest end-use segment, utilizing preservation gases extensively for modified atmosphere packaging, cold storage management, and extended shelf-life solutions. The segment’s dominance is driven by rising processed food consumption and increasing export volumes of perishable products. Cold storage and logistics providers are the fastest-growing end users, supported by expanding global trade in meat, seafood, dairy, and fresh produce. Investments in refrigerated warehousing and temperature-controlled transportation systems are strengthening demand for preservation gases to maintain product quality throughout transit. Quick service restaurants and cloud kitchens are emerging as important application areas, particularly in rapidly urbanizing economies, where centralized commissaries and bulk procurement models require efficient storage and shelf-life management. Export demand continues to be a major growth driver across end-use categories, with high-value meat, seafood, and horticultural products accounting for a significant portion of overall gas utilization.

Explore more data points, trends and opportunities Download Free Sample Report

Fresh Food Preservation Gases Market Segmentations

By Gas Type

- Carbon Dioxide (CO₂)

- Nitrogen (N₂)

- Oxygen (O₂)

- Argon (Ar)

- Specialty Gas Mixtures

By Packaging Technology

- Modified Atmosphere Packaging (MAP)

- Controlled Atmosphere (CA) Storage

- Vacuum Packaging with Gas Flushing

- Active Packaging Systems

By Application (Food Category)

- Meat & Poultry

- Seafood

- Fresh Fruits & Vegetables

- Dairy Products

- Bakery & Confectionery

- Ready-to-Eat & Processed Fresh Foods

By Distribution Channel

- Industrial Bulk Supply

- On-Site Gas Generation

- Cylinder/Packaged Gas Supply

By End-Use Industry

- Food Processing Companies

- Retail & Supermarket Chains

- Cold Storage & Logistics Providers

- Quick Service Restaurants (QSRs) & Cloud Kitchens

Regional Insights

North America

North America holds approximately 28% of the global market, led by the United States and Canada. The region benefits from high per capita meat and fresh produce consumption, well-established cold chain infrastructure, and stringent food safety regulations that mandate advanced packaging standards. Widespread adoption of modified atmosphere packaging across retail and food processing sectors further strengthens regional demand. Growth in online grocery platforms, strong export activity in meat and dairy products, and increasing investments in automated food processing facilities are key drivers supporting market expansion in North America. Technological innovation in packaging materials and sustainability initiatives are also enhancing the adoption of optimized gas solutions.

Europe

Europe accounts for nearly 30% of the global market, with Germany, France, the United Kingdom, Italy, and Spain serving as major contributors. The region’s growth is driven by strict regulatory frameworks governing food safety and labeling, high consumer awareness regarding freshness and quality, and increasing adoption of sustainable packaging practices. Europe’s strong intra-regional trade and export-oriented processed food industry create consistent demand for preservation gases. Additionally, the region’s focus on reducing food waste aligns closely with the functional benefits of modified atmosphere packaging, further accelerating adoption across meat, dairy, and bakery segments.

Asia-Pacific

Asia-Pacific represents approximately 27% of the market and is the fastest-growing region, expanding at over 9% CAGR. China, India, Japan, South Korea, and Australia are key growth engines, supported by rapid urbanization, rising disposable incomes, and expanding organized retail networks. Government investments in cold chain infrastructure and food processing modernization programs are major growth drivers. Increasing exports of seafood, meat, and horticultural products from countries such as China and India significantly boost demand for preservation gases. The expansion of quick service restaurant chains, online food delivery platforms, and modern supermarkets further accelerates market penetration across both developed and emerging economies in the region.

Latin America

Latin America accounts for around 7% of the global market, with Brazil, Mexico, Argentina, and Chile serving as primary contributors. The region’s growth is largely driven by export-oriented agriculture, particularly in meat and fresh produce segments. Expanding organized retail networks and improvements in refrigerated logistics infrastructure are enhancing the adoption of modified atmosphere packaging solutions. Rising domestic consumption of packaged foods and growing investments in food processing facilities further support steady market expansion across the region.

Middle East & Africa

The Middle East & Africa collectively represent approximately 8% of the market, with GCC countries and South Africa leading regional demand. Growth is driven by high imports of premium perishables, increasing domestic food processing activities, and expanding retail modernization initiatives. Infrastructure investments in cold storage and logistics networks are strengthening intra-regional trade and supporting the adoption of preservation gases. Rising urban populations and growing demand for packaged and convenience foods are additional factors contributing to sustained market development across the region.

Key Players in the Fresh Food Preservation Gases Market

- Linde plc

- Air Liquide

- Air Products and Chemicals, Inc.

- Messer Group GmbH

- Nippon Sanso Holdings Corporation

- Taiyo Nippon Sanso

- SOL Group

- Matheson Tri-Gas

- Gulf Cryo

- SIAD Group

- Air Water Inc.

- Ellenbarrie Industrial Gases

- Universal Industrial Gases

- National Gases Limited

- Coregas