Solar Water Heater Market Size

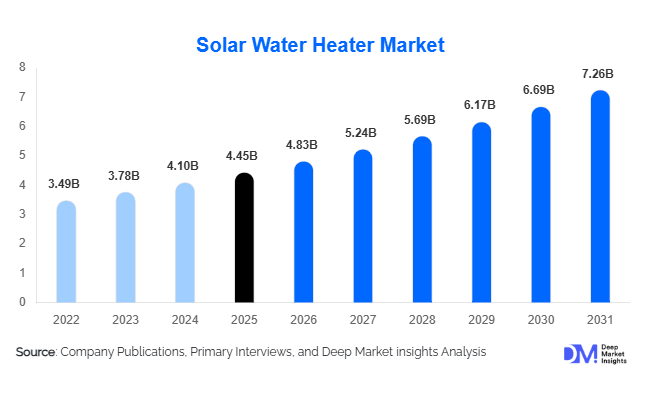

According to Deep Market Insights, the global solar water heater market size was valued at USD 4.45 billion in 2025 and is projected to grow from USD 4.83 billion in 2026 to reach USD 7.26 billion by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The solar water heater market growth is primarily driven by increasing demand for energy-efficient water heating solutions, rising electricity costs, supportive renewable energy policies, and growing adoption of sustainable building technologies across residential, commercial, and industrial sectors.

Key Market Insights

- Solar water heating is increasingly becoming a mainstream energy-efficiency solution, supported by rising utility costs and global decarbonization initiatives.

- Evacuated tube collector systems account for the largest technology share, owing to their superior thermal efficiency and performance in diverse climatic conditions.

- Asia-Pacific dominates the global market, led by large-scale adoption across China and India supported by government incentives and favorable solar resources.

- The Middle East & Africa represents the fastest-growing regional market, driven by abundant solar irradiation and increasing investments in renewable infrastructure.

- Industrial process heating applications are emerging as a major growth opportunity, particularly across food processing, textiles, pharmaceuticals, and chemical industries.

- Smart monitoring technologies and hybrid solar-electric systems are improving system efficiency, operational visibility, and long-term return on investment.

Solar Water Heater Market Trends

Industrial Decarbonization Driving Solar Thermal Adoption

Industrial facilities are increasingly deploying solar water heating systems to reduce fossil fuel dependence and achieve sustainability targets. Industries including food and beverage processing, pharmaceuticals, textiles, pulp and paper, and chemical manufacturing are integrating solar thermal technologies into low- and medium-temperature heating processes. Rising carbon pricing mechanisms, stricter environmental regulations, and corporate net-zero commitments are accelerating this trend. Industrial users are increasingly combining solar thermal systems with thermal energy storage technologies, enabling greater operational flexibility and improving energy resilience while reducing long-term utility expenditures.

Smart and Hybrid Solar Water Heating Systems Gaining Popularity

Manufacturers are increasingly incorporating IoT-enabled controls, smart sensors, and remote monitoring capabilities into solar water heating systems. These technologies allow users to monitor energy generation, optimize performance, and schedule maintenance proactively. Hybrid systems combining solar thermal technology with electric or gas backup heating are becoming particularly popular in regions with seasonal solar variability. Smart integration with building energy management systems is further enhancing adoption among commercial and institutional users seeking comprehensive sustainability solutions.

Solar Water Heater Market Drivers

Rising Global Energy Prices

Escalating electricity and natural gas prices have significantly improved the economic attractiveness of solar water heating systems. Households and businesses are increasingly seeking alternatives that can reduce recurring utility expenses. Solar water heaters offer attractive lifecycle savings, often enabling users to recover installation costs through lower energy bills over the system's operational lifespan. This economic advantage continues to support adoption across both developed and developing economies.

Government Incentives and Renewable Energy Policies

Governments worldwide are implementing supportive measures to encourage solar thermal adoption. Subsidies, tax credits, renewable energy rebates, low-interest financing programs, and energy-efficiency mandates are making solar water heaters more accessible. Countries including China, India, Germany, Spain, Australia, and several Middle Eastern nations continue to expand renewable energy initiatives, creating favorable conditions for market growth. Building regulations increasingly require renewable energy integration, further supporting installations across residential and commercial projects.

Solar Water Heater Market Restraints

High Initial Installation Costs

Despite strong long-term savings potential, solar water heaters require higher upfront investment compared to conventional electric or gas water heating systems. Equipment costs, installation expenses, and additional requirements such as storage tanks and backup systems can discourage adoption, particularly among price-sensitive consumers and small businesses. Access to affordable financing remains a challenge in several emerging markets.

Performance Dependence on Climatic Conditions

Solar water heater efficiency depends heavily on solar irradiance levels and weather conditions. Regions experiencing prolonged cloudy seasons or limited sunlight often require supplementary heating systems to maintain consistent hot water availability. This dependence can increase system complexity and operating costs, limiting adoption in certain geographical areas and affecting overall project economics.

Solar Water Heater Market Opportunities

Industrial Process Heat Applications

The industrial sector presents one of the most significant opportunities for solar water heater manufacturers. Process heating requirements across food processing, pharmaceuticals, textiles, mining, and chemical manufacturing create substantial demand for renewable thermal energy solutions. As industries increasingly focus on carbon reduction and energy efficiency, solar thermal systems offer a cost-effective alternative to conventional fuel-based heating technologies. Large-scale installations in industrial facilities are expected to become a key growth driver through 2031.

Green Building and Sustainable Housing Development

The rapid expansion of green construction projects worldwide is creating strong demand for solar water heating systems. Sustainable building certifications, net-zero construction targets, and energy-efficient housing programs increasingly require renewable heating technologies. Developers are integrating solar water heaters into residential communities, affordable housing projects, hotels, healthcare facilities, and educational institutions to improve energy performance while reducing operational costs. This trend is expected to generate substantial opportunities for manufacturers and project developers globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.45 Billion |

| Market Size in 2026 | USD 4.83 Billion |

| Market Size in 2031 | USD 7.26 Billion |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Technology Insights

Evacuated tube collectors (ETCs) dominate the solar water heater market, accounting for approximately 45% of global revenue in 2025, making them the leading technology segment worldwide. Their market leadership is primarily driven by superior thermal conversion efficiency, enhanced heat retention capabilities, and strong performance under low ambient temperature conditions. Unlike conventional collector technologies, ETC systems minimize heat loss through vacuum insulation, enabling efficient operation even in regions experiencing cold winters or variable weather conditions. This has resulted in widespread adoption across residential, commercial, and institutional installations in major markets such as China, India, Germany, and Turkey.

Another key factor supporting ETC dominance is the declining manufacturing cost of evacuated tubes, particularly due to large-scale production capacity concentrated in Asia-Pacific. Continuous advancements in selective absorber coatings, anti-freeze technologies, and corrosion-resistant materials have further improved system durability and lifecycle economics. Growing demand for high-efficiency water heating systems in urban residential complexes, hotels, hospitals, and educational institutions continues to reinforce the segment's market position. Flat plate collectors remain the second-largest technology segment and continue to witness strong adoption in Europe and North America due to their robust construction, longer service life, and suitability for moderate climatic conditions. However, the efficiency advantages and lower payback periods offered by ETC systems are expected to sustain their leadership throughout the forecast period.

System Configuration Insights

Thermosyphon systems accounted for approximately 59% of global solar water heater market revenue in 2025, making them the dominant system configuration globally. Their leadership is primarily attributed to their simple operating mechanism, which relies on natural convection rather than pumps or controllers. This significantly reduces installation complexity, maintenance requirements, and overall system costs, making thermosyphon systems highly attractive for residential consumers and small commercial establishments. The segment has particularly benefited from large-scale deployment across China, India, Brazil, Turkey, and several Middle Eastern countries, where affordability remains a key purchasing criterion. In addition, thermosyphon systems offer superior reliability due to fewer moving parts, reducing operational failures and maintenance expenses over the system lifecycle.

The increasing construction of residential housing projects and affordable housing developments across emerging economies continues to drive demand for thermosyphon-based systems. Government incentive programs promoting residential renewable energy adoption have further strengthened the segment's position. While forced circulation systems are gaining momentum in large-scale commercial and industrial installations due to their greater operational flexibility and ability to support larger storage capacities, thermosyphon systems are expected to maintain their dominant market share owing to continued demand from the residential sector, which remains the largest end-user category globally.

Capacity Insights

The 101–200-liter capacity segment accounted for approximately 32% of global market demand in 2025, making it the largest capacity category within the solar water heater industry. The segment's leadership is primarily driven by its close alignment with the hot water consumption requirements of average urban households consisting of three to five family members. This capacity range offers an optimal balance between storage volume, energy efficiency, installation footprint, and overall affordability. Rapid urbanization, increasing apartment construction, and growing middle-class populations in countries such as China, India, Indonesia, Brazil, and Mexico have significantly supported demand for systems within this capacity category. Manufacturers have also focused product development efforts on this segment due to its broad applicability across both residential homes and small commercial establishments.

Another major growth driver is the increasing adoption of rooftop solar water heating systems in urban residential developments where space optimization is critical. The 101–200-liter segment provides adequate daily hot water requirements without requiring excessive roof area or structural modifications. Meanwhile, systems above 500 liters are witnessing accelerating demand from hotels, hospitals, educational campuses, and industrial facilities. The growth of hospitality infrastructure and commercial building construction is expected to support higher-capacity system adoption over the coming years; however, the residential-driven 101–200-liter category is expected to remain the leading segment throughout the forecast period.

End-Use Insights

The residential sector remains the largest end-use segment in the solar water heater market, accounting for approximately 40% of total market revenue in 2025. The segment's dominance is largely driven by rising household electricity costs, increasing awareness of renewable energy technologies, and government programs promoting energy-efficient home infrastructure. Residential consumers increasingly view solar water heaters as a long-term investment capable of significantly reducing monthly utility expenditures while contributing to sustainability goals. Rapid urban housing development across Asia-Pacific, the Middle East, and Latin America continues to generate substantial demand for residential installations. In many countries, solar water heating systems are now integrated into new residential construction projects to comply with energy-efficiency standards and green building requirements.

The commercial sector represents the second-largest market segment, with hotels, hospitals, educational institutions, office buildings, and sports facilities increasingly adopting solar thermal systems to reduce operational costs and meet ESG objectives. However, the fastest-growing end-use segment is industrial applications. Industries including food processing, pharmaceuticals, textiles, chemicals, and mining are increasingly deploying solar thermal technologies for low- and medium-temperature process heating applications. Growing pressure to decarbonize industrial operations, combined with rising fossil fuel costs, is expected to accelerate industrial adoption and create one of the most attractive growth opportunities within the solar water heater market over the next decade.

Distribution Channel Insights

Direct sales channels accounted for approximately 35% of global market revenue in 2025, making them the leading distribution model within the solar water heater industry. The segment's dominance is driven by the technical nature of solar thermal systems, which often require customized sizing, site assessments, installation services, and after-sales maintenance support. Direct engagement enables manufacturers to provide end-to-end project solutions while maintaining stronger customer relationships and higher profit margins. Large manufacturers increasingly prefer direct sales for commercial and institutional projects because these installations typically involve higher-value contracts, longer service agreements, and greater customization requirements. Direct channels also allow suppliers to educate customers on system performance, return on investment, and available government incentives, which can significantly improve conversion rates.

Meanwhile, EPC contractors and renewable energy integrators continue to gain market share, particularly within large-scale commercial, hospitality, healthcare, and industrial projects where engineering expertise is essential. Dealer and distributor networks remain critical in emerging economies where localized sales support and installation services strongly influence purchasing decisions. The increasing use of digital platforms and online lead-generation tools is further enhancing customer acquisition strategies across all distribution channels.

Explore more data points, trends and opportunities Download Free Sample Report

Solar Water Heater Market Segmentations

By Technology

- Evacuated Tube Collectors (ETC)

- Flat Plate Collectors (FPC)

- Integral Collector Storage (ICS) Systems

- Unglazed Water Collectors

By System Configuration

- Thermosyphon Systems

- Forced Circulation Systems

By Capacity

- Up to 100 Liters

- 101–200 Liters

- 201–300 Liters

- 301–500 Liters

- 501–1,000 Liters

- Above 1,000 Liters

By End Use

- Residential

- Commercial

- Industrial

By Distribution Channel

- Direct Sales

- EPC Contractors

- Renewable Energy Integrators

- Dealers & Distributors

- Online Sales

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global solar water heater market, accounting for approximately 42% of total market revenue in 2025, making it the largest regional market worldwide. The region's leadership is driven by a combination of favorable solar resources, large population base, rapid urbanization, and strong government support for renewable energy adoption. China remains the largest individual market globally, contributing nearly 25% of worldwide demand. Its dominance stems from extensive domestic manufacturing capacity, well-established solar thermal supply chains, supportive government policies, and widespread residential adoption across both urban and rural areas. India represents the fastest-growing major market within the region, driven by rising electricity tariffs, increasing residential construction activity, renewable energy mandates, and government subsidy programs promoting solar thermal technologies.

Japan, South Korea, and Australia continue to witness growing demand for high-efficiency solar water heating systems as building decarbonization initiatives, net-zero targets, and sustainability-focused construction activities gain momentum. The region also benefits from the presence of major global manufacturers, which supports cost competitiveness and product innovation.

Europe

Europe accounted for approximately 26% of global market revenue in 2025, supported by strong climate policies and ambitious carbon reduction objectives. Germany remains the largest market within the region due to extensive adoption of renewable heating technologies and favorable government incentives for building energy efficiency upgrades. Southern European countries including Spain, Italy, Greece, and Portugal benefit from high solar irradiation levels, making solar water heating systems economically attractive for residential and hospitality applications. Rising natural gas prices and energy security concerns following recent geopolitical disruptions have accelerated investment in alternative heating technologies across the continent.

Additionally, stringent European Union regulations regarding building energy performance and renewable heating integration are creating sustained demand for solar thermal installations. The growing renovation of existing building stock to meet decarbonization targets is expected to remain a major growth driver throughout the forecast period.

North America

North America accounted for approximately 15% of global demand in 2025, with the United States representing the majority of regional installations. Growth is being supported by rising consumer awareness of renewable energy solutions, increasing utility costs, and federal as well as state-level clean energy incentives. States such as California, Arizona, Texas, Florida, and Nevada continue to lead adoption due to favorable climatic conditions, high solar irradiance levels, and supportive renewable energy policies. Commercial demand is expanding rapidly as hotels, healthcare facilities, universities, and government institutions seek to reduce operating expenses and improve sustainability performance.

Canada is witnessing increasing adoption within institutional and municipal projects, supported by government investments in energy-efficient infrastructure and climate action initiatives. Growing interest in net-zero buildings and electrification strategies is expected to further strengthen market growth across the region.

Latin America

Latin America accounted for approximately 7% of global market revenue in 2025, with Brazil emerging as the dominant regional market. Strong residential demand, increasing electricity prices, and favorable climatic conditions continue to support widespread adoption of solar water heating systems across the country. Mexico is experiencing growing demand due to rising energy costs, expanding commercial construction activity, and increasing awareness of renewable heating solutions. Chile and Colombia are also emerging as attractive growth markets as governments encourage renewable energy deployment and improve access to sustainable infrastructure financing.

The region benefits from abundant solar resources throughout much of its geography, creating favorable economic conditions for solar thermal investments. Rising urbanization and housing development programs are expected to further support long-term market expansion across Latin America.

Middle East & Africa

The Middle East & Africa region accounted for approximately 10% of global market demand in 2025 and represents the fastest-growing regional market, with forecast growth exceeding 10% annually through 2031. The region's growth is primarily driven by exceptionally high solar irradiation levels, increasing water heating requirements, and growing government investments in renewable energy infrastructure. Saudi Arabia and the United Arab Emirates are leading adoption through national energy diversification strategies aimed at reducing dependence on hydrocarbons. Large-scale sustainability initiatives, green building programs, and smart city developments are creating substantial opportunities for solar thermal deployment.

In Africa, countries including South Africa, Egypt, Morocco, Kenya, and Tunisia are increasingly adopting solar water heating systems to improve energy access, reduce electricity consumption, and address grid reliability challenges. Government subsidy programs, international climate financing, and expanding residential electrification efforts are further accelerating market growth. The combination of abundant solar resources, favorable economics, and strong policy support positions the region as one of the most attractive growth markets globally.

Key Players in the Solar Water Heater Market

- Rheem Manufacturing Company

- A. O. Smith Corporation

- Bosch Thermotechnology

- SUNRAIN Group

- Racold Thermo Ltd.

- Greenonetec Solarindustrie GmbH

- SunEarth Inc.

- V-Guard Industries

- Kodsan

- Chromagen

- Nobel International

- Himin Solar

- Apricus Solar

- Eurostar Solar

- Vaillant Group