Snack Bars Market Size

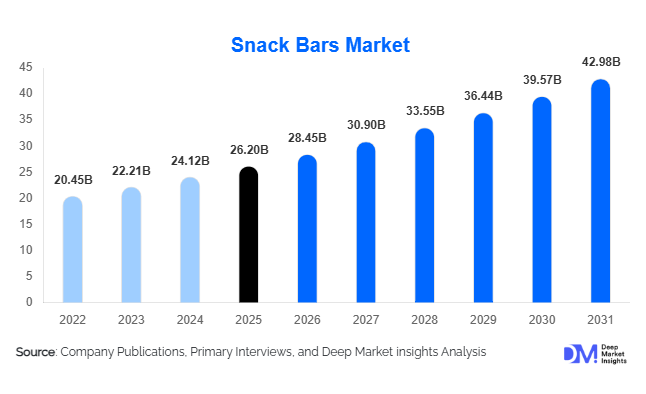

According to Deep Market Insights, the global snack bars market size was valued at USD 26.2 billion in 2025 and is projected to grow from USD 28.45 billion in 2026 to reach USD 42.98 billion by 2031, expanding at a CAGR of 8.6% during the forecast period (2026–2031). The snack bars market growth is primarily driven by increasing consumer demand for convenient and nutritious on-the-go food options, rising health and wellness awareness, expanding sports nutrition consumption, and growing adoption of functional food products. Manufacturers are continuously introducing high-protein, low-sugar, clean-label, and plant-based snack bars to meet evolving consumer preferences, further accelerating market expansion globally.

Key Market Insights

- High-protein and functional snack bars are witnessing the fastest growth, driven by increasing fitness participation, weight management programs, and demand for meal-replacement solutions.

- Clean-label and natural ingredient formulations are becoming industry standards, with consumers actively seeking products free from artificial preservatives, colors, and sweeteners.

- North America dominates the global snack bars market, accounting for approximately 44% of global revenue due to strong consumer awareness and high penetration of health-oriented packaged foods.

- Asia-Pacific is the fastest-growing regional market, supported by rising urbanization, growing disposable incomes, expanding retail infrastructure, and increasing health consciousness.

- E-commerce and direct-to-consumer sales channels are transforming product distribution, enabling brands to expand market reach while improving customer engagement.

- Plant-based proteins, gut-health ingredients, and personalized nutrition solutions are emerging as major innovation areas across the global snack bars industry.

Snack Bars Market Latest Trends

Functional Nutrition and Health-Focused Innovation

Consumers increasingly expect snack bars to deliver benefits beyond basic nutrition. Manufacturers are responding by incorporating functional ingredients such as probiotics, prebiotics, adaptogens, vitamins, minerals, collagen peptides, and plant-based proteins into product formulations. High-protein bars targeting muscle recovery, digestive health bars promoting gut wellness, and low-sugar formulations supporting weight management have become some of the fastest-growing categories within the market. Brands are also investing heavily in scientific validation and health claims to differentiate products in an increasingly competitive marketplace. This trend reflects the broader convergence between food, nutrition, and wellness, positioning snack bars as functional health products rather than simple convenience snacks.

Plant-Based and Sustainable Product Development

The growing popularity of vegan and environmentally conscious lifestyles is accelerating demand for plant-based snack bars. Manufacturers are increasingly utilizing ingredients such as pea protein, soy protein, chickpea protein, nuts, seeds, and oats to develop sustainable alternatives to traditional whey-based products. Sustainability initiatives now extend beyond ingredients to include eco-friendly packaging, responsible sourcing practices, carbon footprint reduction programs, and regenerative agriculture partnerships. Consumers, particularly younger demographics, are actively evaluating environmental and ethical considerations when making purchasing decisions, prompting manufacturers to integrate sustainability into both product development and brand positioning strategies.

Snack Bars Market Drivers

Growing Consumer Focus on Health and Wellness

The increasing prevalence of lifestyle-related health concerns, including obesity, diabetes, and cardiovascular diseases, has significantly influenced consumer food choices. Modern consumers are actively seeking healthier snack alternatives that provide nutritional benefits while maintaining convenience. Snack bars fortified with protein, fiber, vitamins, and functional ingredients have emerged as attractive options for health-conscious consumers. Growing awareness regarding nutritional labels, sugar reduction, and clean-label ingredients continues to support category growth across both developed and emerging markets.

Expansion of Sports Nutrition and Active Lifestyles

Global participation in fitness activities, sports, gym memberships, and outdoor recreation continues to rise. This trend has substantially increased demand for protein bars, energy bars, and performance-focused nutrition products. Athletes, fitness enthusiasts, and active consumers increasingly rely on snack bars as convenient pre-workout, post-workout, and meal-replacement solutions. The integration of sports nutrition into mainstream consumer behavior is expanding the addressable market beyond traditional athletic communities and supporting sustained industry growth.

Snack Bars Market Restraints

Raw Material Price Volatility

The snack bars industry remains highly exposed to fluctuations in the prices of key ingredients including nuts, oats, protein isolates, cocoa, dried fruits, and specialty nutritional additives. Weather disruptions, agricultural supply shortages, geopolitical tensions, and transportation constraints can significantly affect production costs. These fluctuations often compress profit margins and create pricing challenges for manufacturers operating in highly competitive retail environments.

Increasing Regulatory and Labeling Requirements

Governments and regulatory authorities worldwide are implementing stricter requirements related to nutritional labeling, sugar content disclosure, allergen declarations, and health claims. Compliance with varying regional regulations can increase product development costs and extend commercialization timelines. Manufacturers must continuously reformulate products and adapt packaging strategies to comply with evolving standards, creating operational complexity across international markets.

Snack Bars Industry Key Opportunities

Expansion into Emerging Asia-Pacific Markets

Asia-Pacific represents one of the largest untapped growth opportunities within the global snack bars market. Countries such as India, China, Indonesia, Vietnam, and the Philippines are experiencing rapid urbanization, increasing disposable incomes, and growing health awareness among consumers. The expansion of organized retail, digital commerce platforms, and modern food distribution networks is improving product accessibility across these markets. Manufacturers that develop locally relevant flavors, affordable pricing structures, and region-specific marketing strategies are expected to capture significant long-term growth opportunities. India, in particular, is emerging as one of the fastest-growing national markets, supported by increasing demand for healthy snacking products among younger urban populations.

Personalized Nutrition and Direct-to-Consumer Growth

The rise of personalized nutrition platforms and direct-to-consumer distribution channels is creating new opportunities for snack bar manufacturers. Consumers increasingly seek customized nutritional solutions aligned with their dietary goals, fitness objectives, and health conditions. Subscription models, personalized product recommendations, digital wellness integrations, and data-driven product development are enabling brands to strengthen customer engagement and improve retention rates. The continued growth of e-commerce and quick-commerce platforms further enhances opportunities for market penetration while supporting premium product positioning.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 26.20 Billion |

| Market Size in 2026 | USD 28.45 Billion |

| Market Size in 2031 | USD 42.98 Billion |

| CAGR | 8.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Cereal and granola bars continue to dominate the global snack bars market, accounting for approximately 32% of total revenue in 2025. Their leadership is primarily driven by strong consumer trust in whole grain-based nutrition, widespread affordability, and their positioning as a convenient everyday snack that aligns with mainstream dietary habits. The segment benefits from consistent demand across both developed and emerging markets, where convenience, taste familiarity, and perceived health value collectively reinforce repeat purchases.Protein bars represent the fastest-growing product category, supported by a powerful shift toward fitness-oriented lifestyles, sports nutrition, and high-protein dietary preferences. Growth in this segment is further reinforced by increasing gym participation, rising awareness of muscle recovery nutrition, and the expansion of weight management and meal-replacement consumption patterns among urban populations. Continuous product innovation in plant-based and low-sugar protein formulations is further accelerating adoption among both active consumers and mainstream health-conscious individuals.Energy bars maintain steady growth, largely driven by expanding participation in endurance sports, outdoor recreation, and active commuting trends. Their consumption is strongly linked to immediate energy replenishment needs, particularly among athletes and physically active professionals. Functional nutrition bars enriched with probiotics, vitamins, and specialty ingredients are also gaining momentum, driven by rising consumer preference for targeted health benefits beyond basic nutrition. Fruit-based and breakfast bars sustain stable demand, particularly among consumers seeking natural ingredient profiles and convenient morning meal alternatives that align with busy urban routines.

Ingredient Source Insights

Grain-based snack bars remain the dominant ingredient category, representing approximately 34% of global market revenue, supported by extensive use of oats, cereals, and whole grains. Their leadership is reinforced by strong supply chain availability, cost efficiency, and deep-rooted consumer familiarity with grain-based nutrition formats. The segment’s stability is further strengthened by its versatility in both mainstream and functional product formulations.Plant protein-based formulations are experiencing the fastest growth, driven by the accelerating shift toward vegan, vegetarian, and environmentally sustainable nutrition. This growth is further supported by rising consumer awareness regarding animal protein alternatives, improved taste and texture innovation in plant proteins, and expanding product positioning in sports and lifestyle nutrition categories. Nut-based bars continue to perform strongly in premium segments due to their high nutrient density, natural positioning, and association with clean-label and minimally processed food trends.Fruit-based and mixed-ingredient formulations are expanding steadily, supported by innovations focused on natural sweetness, functional ingredient integration, and clean-label transparency. These formulations are increasingly preferred by consumers seeking indulgent yet healthier snack alternatives that combine taste with nutritional value.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for approximately 58% of global snack bar sales. Their leadership is driven by extensive shelf visibility, strong promotional strategies, and the ability to offer wide product variety under a single retail environment. These formats continue to benefit from high consumer trust and frequent household purchasing behavior, particularly in urban markets.Convenience stores play a critical role in driving impulse purchases and on-the-go consumption, particularly in high-traffic urban locations and transit hubs. Online retail and direct-to-consumer platforms represent the fastest-growing distribution channels, fueled by rapid digital adoption, personalized nutrition offerings, subscription-based delivery models, and the increasing influence of health-focused e-commerce ecosystems. Specialty health stores and pharmacies also contribute significantly to premium and functional snack bar sales, especially in developed regions where consumers actively seek targeted wellness products and medically aligned nutrition solutions.

Consumer Group Insights

Adults represent the largest consumer base, accounting for nearly 72% of global demand in 2025. This dominance is driven by working professionals who increasingly rely on snack bars as convenient meal replacements and healthier alternatives to traditional packaged snacks. The segment benefits from fast-paced urban lifestyles where portability, balanced nutrition, and time efficiency are key purchasing drivers.Athletes and fitness-focused consumers represent a high-growth segment, strongly influencing demand for protein and energy bars. Growth in this group is driven by increasing participation in gym activities, organized sports, endurance training, and structured wellness programs. Children’s snack bars are also gaining traction as parents increasingly prioritize healthier school snack options with reduced sugar content and improved nutritional profiles. Senior consumers are steadily increasing adoption of functional snack bars designed to support healthy aging, improved digestion, and sustained energy, reflecting broader demographic shifts toward preventive nutrition.

Price Tier Insights

The mid-range segment dominates the global market, accounting for approximately 55% of total revenue. Its leadership is driven by a balanced value proposition that combines affordability with acceptable nutritional quality, making it the preferred choice for mass-market consumers. This segment continues to benefit from strong demand in both developed and emerging economies where value-conscious purchasing behavior remains prominent.Premium snack bars are expanding rapidly, supported by rising demand for organic ingredients, high-protein formulations, functional health claims, and sustainable sourcing certifications. This segment’s growth is closely linked to increasing disposable incomes, urban health consciousness, and willingness to pay for differentiated nutritional benefits. Economy-priced products continue to hold relevance in cost-sensitive markets, particularly in developing regions where affordability remains a key determinant of purchase decisions. However, gradual premiumization trends are reshaping long-term demand structures across multiple geographies.

Explore more data points, trends and opportunities Download Free Sample Report

Snack Bars Market Segmentations

By Product Type

- Cereal & Granola Bars

- Protein Bars

- Energy Bars

- Fruit Bars

- Nutrition & Functional Bars

- Breakfast Bars

- Snack & Indulgence Bars

By Ingredient Source

- Grain-Based

- Nut-Based

- Fruit-Based

- Dairy-Based

- Plant Protein-Based

- Mixed Ingredient Formulations

By Nature

- Conventional

- Organic

By Dietary Positioning

- Regular

- Gluten-Free

- Vegan

- Keto-Friendly

- Sugar-Free/Low Sugar

- High-Protein

- Clean Label/Natural

By Packaging Format

- Single-Serve Packs

- Multipacks

- Family Packs

- Bulk Packs

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 44% of global revenue in 2025, with the United States contributing nearly 36% of total consumption. Regional growth is strongly driven by high consumer awareness of health and wellness, widespread adoption of protein-rich diets, and a mature fitness culture that actively supports sports nutrition consumption. Advanced retail infrastructure and strong product innovation pipelines further enhance market penetration. The region also benefits from continuous demand for meal replacement solutions and functional snack formats tailored to busy lifestyles, while Canada contributes steady growth through increasing preference for clean-label and natural food products.

Europe

Europe accounts for approximately 27% of global market revenue, with key contributions from Germany, the United Kingdom, France, Italy, and Spain. Growth in the region is primarily driven by strong regulatory emphasis on sugar reduction, rising demand for organic and sustainably sourced ingredients, and increasing consumer preference for transparent nutritional labeling. The United Kingdom remains a highly mature market characterized by widespread snack bar adoption across all demographic groups, while Germany leads growth in plant-based and functional nutrition segments. Expanding health-conscious consumption patterns and government-led dietary improvement initiatives continue to reinforce long-term market expansion across the region.

Asia-Pacific

Asia-Pacific accounts for approximately 20% of global revenue and represents the fastest-growing regional market. Growth is strongly supported by rapid urbanization, rising disposable incomes, and increasing exposure to global health and wellness trends. China and India serve as primary growth engines, driven by expanding middle-class populations and growing demand for convenient nutrition solutions. India, in particular, is expected to record the highest global CAGR exceeding 11%, supported by a young population base, increasing fitness awareness, and rapid expansion of modern retail channels. China continues to experience strong premiumization trends and rising adoption of functional nutrition products, while Japan, South Korea, and Australia contribute through mature health-focused consumption ecosystems.

Latin America

Latin America contributes approximately 6% of global market revenue, with Brazil and Mexico serving as the largest and most dynamic markets. Regional growth is primarily driven by rising middle-class income levels, increasing awareness of healthier dietary habits, and gradual expansion of organized retail infrastructure. Demand is further supported by localized product innovation strategies that focus on affordability and flavor adaptation to regional preferences. Growing urbanization and improved distribution networks continue to strengthen market accessibility, enabling steady long-term expansion.

Middle East & Africa

The Middle East and Africa account for approximately 3% of global revenue but represent a high-potential emerging market with strong long-term growth prospects. Demand is concentrated in countries such as the United Arab Emirates, Saudi Arabia, and South Africa, where increasing fitness awareness, rising disposable incomes, and expanding expatriate populations are driving adoption of health-oriented snack products. The region is also experiencing growing availability of imported premium nutrition bars, supported by rapid retail modernization and urban development. Ongoing infrastructure expansion and increasing health consciousness are expected to significantly accelerate market penetration over the coming years.

Key Players in the Snack Bars Market

- Kellanova

- General Mills Inc.

- Mars Incorporated

- Mondelez International Inc.

- Nestlé S.A.

- The Quaker Oats Company

- Weetabix Food Company

- Hero Group

- The Hain Celestial Group Inc.

- Clif Bar & Company

- Post Holdings Inc.

- KIND LLC

- RXBAR

- Barebells Functional Foods

- The Simply Good Foods Company