Smoked Eel Market Size

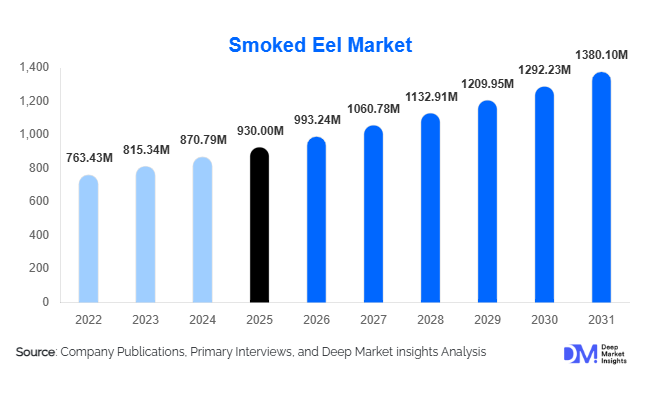

According to Deep Market Insights, the global smoked eel market size was valued at USD 930 million in 2025 and is projected to grow from USD 993.24 million in 2026 to reach USD 1,380.10 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The smoked eel market growth is primarily driven by increasing demand for premium seafood products, expanding consumption of ready-to-eat smoked fish, rising popularity of gourmet and ethnic cuisines, and growing adoption of sustainable aquaculture practices. Smoked eel remains a highly valued seafood delicacy across Europe and East Asia, while emerging demand from North America, the Middle East, and selected Asia-Pacific markets continues to broaden the consumer base. Improvements in cold-chain logistics, vacuum packaging technologies, and international seafood trade networks are further supporting market expansion globally.

Key Market Insights

- Hot-smoked eel remains the largest product category, accounting for nearly 60% of global market revenue due to its broad consumer acceptance and ready-to-eat convenience.

- Europe dominates the global smoked eel market, contributing approximately 48% of global demand, led by the Netherlands, Germany, Denmark, and France.

- Asia-Pacific is the fastest-growing regional market, supported by expanding premium seafood consumption in China, Japan, South Korea, and Singapore.

- Vacuum-packed smoked eel products account for nearly 68% of sales, reflecting growing demand for extended shelf life and export-friendly packaging.

- Retail channels generate approximately 69% of market revenues, driven by premium supermarket offerings and online seafood retail platforms.

- Sustainable sourcing and aquaculture certification programs are becoming increasingly important purchasing criteria among retailers and consumers.

- Ready-to-eat and value-added smoked eel products are creating new growth opportunities within convenience food and gourmet meal categories.

Smoked Eel Market Latest Trends

Growing Demand for Premium and Ready-to-Eat Seafood Products

The global seafood industry is witnessing a significant shift toward premium and convenience-oriented products, and smoked eel is benefiting directly from this trend. Consumers increasingly seek high-protein, nutrient-rich seafood products that require minimal preparation while delivering restaurant-quality experiences at home. As a result, manufacturers are expanding portfolios to include pre-sliced smoked eel, portion-controlled packs, gourmet seafood platters, and meal-kit ingredients. Retailers across Europe, North America, and Asia are dedicating greater shelf space to premium smoked seafood categories, helping improve product visibility and accessibility. This trend is particularly pronounced among affluent urban consumers who value convenience, traceability, and premium food experiences.

Sustainability and Traceability Becoming Core Competitive Differentiators

Environmental sustainability has emerged as one of the most influential factors shaping the smoked eel market. Growing concerns regarding wild eel populations and regulatory restrictions on harvesting are driving increased investments in certified aquaculture systems and traceable supply chains. Producers are adopting digital monitoring platforms, blockchain-enabled traceability systems, and sustainability certification programs to meet retailer requirements and consumer expectations. Large seafood processors are also investing in responsible sourcing initiatives and stock replenishment programs to ensure long-term raw material availability. These developments are strengthening consumer confidence while helping manufacturers secure premium pricing in international markets.

Smoked Eel Market Drivers

Rising Consumption of Premium Seafood Products

The increasing preference for premium seafood products represents one of the strongest growth drivers for the smoked eel market. Consumers across developed economies are prioritizing seafood products that combine nutritional value with distinctive flavor profiles. Smoked eel is particularly attractive due to its rich taste, omega-3 content, and gourmet positioning. Rising disposable incomes and expanding premium food consumption in Europe, Japan, South Korea, China, and North America continue to support long-term market growth.

Expansion of Foodservice and Fine Dining Applications

Restaurants, luxury hotels, catering operators, and sushi chains are increasingly incorporating smoked eel into premium menu offerings. Fine dining chefs frequently utilize smoked eel in appetizers, sushi preparations, seafood platters, and fusion cuisine concepts. The growing popularity of Japanese and European seafood cuisine globally has further accelerated foodservice demand. Premium menu pricing allows operators to maintain attractive margins while promoting smoked eel as a specialty ingredient.

Advancements in Packaging and Cold-Chain Infrastructure

Improvements in vacuum packaging technologies, modified atmosphere packaging systems, and temperature-controlled logistics have significantly expanded market accessibility. These innovations enable producers to distribute smoked eel products across international markets while preserving freshness, quality, and food safety standards. E-commerce seafood platforms have further increased consumer access, supporting direct-to-consumer sales and premium seafood subscriptions.

Smoked Eel Market Restraints

Raw Material Supply Constraints and Sustainability Challenges

The availability of eel remains one of the industry's primary challenges. Conservation concerns, regulatory restrictions, and declining wild eel populations continue to limit raw material supply. Compliance with sustainability standards often increases operational costs and may restrict production volumes, particularly for smaller processors with limited sourcing capabilities.

Price Volatility Across the Value Chain

Smoked eel manufacturers face persistent pricing pressures arising from fluctuations in eel procurement costs, feed prices, energy expenses, transportation charges, and labor costs. Since raw eel often accounts for more than half of finished product production costs, supply disruptions can significantly impact profitability. This volatility creates challenges for both producers and retailers when establishing long-term pricing strategies.

Smoked Eel Industry Key Opportunities

Expansion into Premium Asian Seafood Markets

Asia-Pacific represents the most attractive growth opportunity for smoked eel manufacturers. While eel consumption is already deeply integrated into Japanese, Chinese, and Korean cuisine, smoked eel remains relatively underpenetrated compared to grilled and fresh eel products. Growing middle-class populations, increasing disposable incomes, and rising demand for premium seafood products are creating substantial opportunities for both domestic producers and exporters. International suppliers that develop region-specific product offerings and distribution partnerships are expected to benefit significantly from rising consumption trends.

Development of Value-Added and Convenience-Oriented Products

Manufacturers are increasingly focusing on higher-margin value-added products, including ready-to-eat smoked eel slices, gourmet meal kits, smoked eel spreads, sushi ingredients, and seafood snack products. These formats appeal to younger consumers seeking convenience without sacrificing quality. Expansion into online retail channels and premium foodservice applications further enhances the commercial potential of these products. As convenience food consumption continues to rise globally, value-added smoked eel products are expected to become a major growth engine for the industry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 930.00 Million |

| Market Size in 2026 | USD 993.24 Million |

| Market Size in 2031 | USD 1380.10 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The hot-smoked eel segment continues to dominate the global smoked eel market, accounting for approximately 60% of total revenue in 2025. Its market leadership is primarily attributed to widespread consumer acceptance, fully cooked convenience, longer shelf-life characteristics, and strong integration into traditional European seafood consumption patterns. Hot-smoked eel is extensively preferred by both household consumers and foodservice operators due to its ready-to-eat nature, ease of preparation, and versatility across multiple culinary applications. The segment further benefits from increasing demand for premium convenience seafood products as consumers seek high-protein, minimally processed food options that offer both taste and nutritional value. In addition, manufacturers are expanding product portfolios through flavored variants, wood-smoking innovations, and region-specific seasoning profiles, further strengthening segment growth.Cold-smoked eel occupies a premium niche within the market and remains highly valued among gourmet consumers, luxury retailers, and fine dining establishments. The segment is characterized by its refined texture, delicate flavor profile, and strong appeal in premium seafood platters, sushi preparations, and upscale culinary applications. Rising consumer willingness to spend on artisanal and specialty seafood products, particularly across Europe and developed Asia-Pacific markets, continues to support demand. Growing penetration of premium seafood counters, gourmet e-commerce platforms, and specialty delicatessens is also contributing to the expansion of cold-smoked eel sales globally.

Species Source Insights

European eel represents the largest species segment, accounting for approximately 46% of global smoked eel market revenue in 2025. The segment benefits from centuries-old consumption traditions across major European markets including the Netherlands, Germany, Denmark, France, and the United Kingdom. Strong consumer familiarity, established processing infrastructure, and premium product positioning continue to reinforce the dominance of European eel within the global value chain. Furthermore, increasing investments in eel aquaculture and stock conservation initiatives are helping improve long-term supply stability while supporting sustainable sourcing requirements.Japanese eel constitutes a significant share of the Asia-Pacific smoked eel market owing to its deep cultural significance and widespread consumption across Japan and neighboring East Asian countries. Demand remains supported by strong culinary traditions, premium seafood consumption patterns, and the popularity of eel-based dishes in both retail and restaurant channels. American eel primarily serves North American demand centers and selected export markets. Across all species categories, the growing emphasis on traceability, responsible sourcing, and aquaculture-based production is becoming increasingly important as industry participants seek to address resource constraints, regulatory requirements, and sustainability concerns associated with wild eel populations.

Processing Format Insights

Smoked eel fillets account for approximately 42% of global market revenue, making them the leading processing format segment. Their dominance is driven by convenience, reduced preparation requirements, lower waste generation, and compatibility with a wide range of retail and foodservice applications. Consumers increasingly favor fillet products due to their ease of consumption, portion control benefits, and suitability for modern meal preparation trends. The growing popularity of ready-to-cook and ready-to-eat seafood products continues to accelerate demand for smoked eel fillets across developed and emerging markets.Whole smoked eel remains an important category, particularly in traditional European markets where authenticity and heritage consumption patterns remain deeply rooted. At the same time, sliced smoked eel products are witnessing robust growth as retailers and foodservice operators seek premium, visually appealing, and conveniently packaged offerings. The increasing incorporation of smoked eel ingredients into gourmet prepared meals, sushi products, seafood salads, premium sandwiches, and specialty convenience foods is creating additional growth opportunities across processing formats and expanding the product's addressable consumer base.

Packaging Insights

Vacuum-packed smoked eel products dominate the global market, accounting for nearly 68% of total sales in 2025. The segment's leadership is supported by its ability to significantly extend shelf life, preserve freshness, maintain product quality during transportation, and facilitate international trade. Vacuum packaging also aligns with retailer requirements for food safety, product integrity, and inventory management, making it the preferred packaging solution across both domestic and export markets. The growing expansion of cross-border seafood trade and e-commerce seafood distribution further strengthens demand for vacuum-packaged products.Modified atmosphere packaging is steadily gaining traction among premium seafood brands and retailers due to its enhanced preservation capabilities and attractive product presentation. Meanwhile, frozen retail packaging remains essential for long-distance international shipments and supply chain optimization, particularly in markets with limited local production. Bulk packaging formats continue to play an important role in supporting foodservice establishments, catering operators, seafood processors, and industrial buyers that require larger-volume procurement solutions.

Distribution Channel Insights

Retail remains the largest distribution channel, accounting for approximately 69% of global smoked eel market revenues. The segment benefits from extensive product availability through supermarkets, hypermarkets, specialty seafood retailers, gourmet food stores, delicatessens, and rapidly expanding online seafood platforms. Rising consumer preference for premium packaged seafood products, combined with increasing digital grocery adoption, continues to support retail channel growth. Product visibility, brand differentiation, and premium merchandising strategies within organized retail environments further contribute to channel expansion.Foodservice channels account for approximately 25% of global revenues and represent a significant source of demand growth. Restaurants, luxury hotels, catering operators, sushi chains, and fine dining establishments increasingly utilize smoked eel as a premium menu ingredient capable of generating higher margins and enhancing culinary differentiation. Industrial food processors constitute a smaller but steadily expanding distribution channel, incorporating smoked eel into value-added seafood products, premium ready meals, sushi kits, and gourmet prepared food offerings. The increasing convergence of convenience food trends and premium seafood consumption is expected to support sustained channel development over the forecast period.

End-User Insights

Household consumers represent the largest end-user segment, accounting for approximately 40% of global smoked eel demand. The segment's growth is primarily driven by rising availability of convenient packaged products, increasing awareness of seafood-based nutrition, and growing consumer interest in premium ready-to-eat meal solutions. Modern retail expansion, improved cold-chain infrastructure, and the proliferation of online seafood purchasing platforms have further improved accessibility for household buyers, supporting sustained demand growth across both developed and emerging markets.Restaurants and fine dining establishments constitute the second-largest end-user segment and continue to benefit from growing consumer demand for premium seafood experiences. Smoked eel's distinctive flavor profile, premium positioning, and versatility across international cuisines make it a preferred ingredient within upscale dining environments. Additionally, ready meal manufacturers are emerging as an increasingly important end-user category as smoked eel gains greater incorporation into premium convenience foods, seafood meal kits, sushi products, gourmet frozen meals, and other value-added food applications. The ongoing expansion of premium convenience food consumption globally is expected to further strengthen this segment's contribution to overall market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Smoked Eel Market Segmentations

By Product Type

- Hot-Smoked Eel

- Cold-Smoked Eel

By Species Source

- European Eel

- Japanese Eel

- American Eel

- Other Freshwater Eel Species

By Processing Format

- Whole Smoked Eel

- Smoked Eel Fillets

- Smoked Eel Portions/Steaks

- Ready-to-Eat Sliced Smoked Eel

- Smoked Eel Ingredients for Food Processing

By Packaging Type

- Vacuum-Packed

- Modified Atmosphere Packaging (MAP)

- Frozen Retail Packs

- Bulk Foodservice Packs

By Distribution Channel

- Retail

- Foodservice

- Industrial/B2B Food Processing

Regional Insights

Europe

Europe remains the largest regional market, accounting for approximately 48% of global smoked eel consumption in 2025. The Netherlands, Germany, Denmark, France, and the United Kingdom collectively represent the region's primary demand centers. Strong seafood consumption traditions, advanced fish processing infrastructure, established distribution networks, and high consumer purchasing power continue to support Europe's market leadership. Germany contributes approximately 12% of global demand, while the Netherlands accounts for nearly 10%, reflecting the region's long-standing eel smoking heritage and strong cultural acceptance of smoked eel products.Regional growth is being driven by sustained demand for premium seafood products, increasing consumer preference for artisanal and traditionally prepared foods, and the expansion of specialty seafood retail channels. Growing emphasis on sustainable seafood sourcing, certified aquaculture production, and traceable supply chains is also encouraging product innovation and premiumization. Furthermore, the popularity of gourmet seafood consumption, coupled with rising demand from luxury restaurants and delicatessen retailers, continues to reinforce Europe's dominant position within the global market.

Asia-Pacific

Asia-Pacific accounts for approximately 24% of global demand and represents the fastest-growing regional market, with projected annual growth exceeding 8%. Japan remains the largest individual market within the region, supported by deep-rooted culinary traditions and strong cultural acceptance of eel-based products. China is emerging as the fastest-growing country market due to rising disposable incomes, rapid urbanization, and expanding consumption of premium seafood products. South Korea, Singapore, and Taiwan are also witnessing increased adoption of smoked eel products across both retail and foodservice sectors.Regional growth is being fueled by expanding middle-class populations, increasing expenditure on premium and imported seafood products, and the growing influence of Japanese and international seafood cuisines throughout the region. Rising demand for convenient ready-to-eat seafood products, expanding modern retail infrastructure, and strong development of e-commerce food distribution channels are further accelerating market expansion. Additionally, investments in aquaculture production and seafood processing capabilities are helping improve product availability and support long-term regional demand growth.

North America

North America contributes approximately 15% of global smoked eel market revenues, with the United States representing the dominant share of regional demand. Increasing consumer interest in premium seafood products, growing adoption of Asian cuisines, and broader availability through specialty retailers and gourmet food stores continue to support market expansion. Canada is also experiencing rising consumption levels, particularly within premium grocery chains, upscale restaurants, and specialty food retail channels.Regional growth is being driven by increasing consumer awareness of high-protein seafood products, expanding multicultural food preferences, and rising demand for premium ready-to-eat offerings. The continued popularity of sushi, Japanese cuisine, and gourmet seafood dining experiences is creating new consumption opportunities for smoked eel products. Furthermore, growth in online seafood retailing, improved cold-chain logistics, and increasing premiumization across foodservice channels are contributing to stronger market penetration throughout North America.

Latin America

Latin America accounts for approximately 6% of global demand, with Brazil, Mexico, and Chile emerging as the region's most important markets. Although the market remains relatively small compared to Europe and Asia-Pacific, growing exposure to international cuisines and evolving consumer preferences are creating favorable conditions for market development. Premium seafood consumption is gradually expanding as consumers increasingly seek differentiated food experiences and higher-quality protein sources.Regional growth is supported by rising middle-class incomes, expanding organized retail networks, and increasing penetration of imported specialty food products. The growing popularity of international restaurants, Japanese cuisine, and premium hospitality services is also encouraging broader adoption of smoked eel products. Improvements in seafood import infrastructure and greater availability through specialty retail channels are expected to further strengthen market growth prospects over the coming years.

Middle East & Africa

The Middle East & Africa region represents approximately 7% of global smoked eel demand. The United Arab Emirates and Saudi Arabia serve as the region's primary import markets, supported by affluent consumer demographics, strong tourism activity, and rapidly expanding luxury hospitality sectors. High-end restaurants, luxury hotels, and international catering operators continue to drive demand for imported premium smoked eel products across major metropolitan centers.Regional growth is being driven by increasing premium food consumption, expanding tourism and hospitality investments, and rising demand for luxury dining experiences among both residents and international visitors. The continued development of modern retail infrastructure, growth in gourmet food retailing, and increasing availability of imported specialty seafood products are further supporting market expansion. Additionally, the diversification of foodservice offerings and growing influence of international culinary trends are creating new opportunities for smoked eel suppliers across the region.

Key Players in the Smoked Eel Market

- Dutch Eel Company

- Foppen

- Seagull NV

- Royal Danish Fish

- Dilvis

- Kok Spaarndam B.V.

- S & J Fisheries

- Bos Seafood

- Smiths Smokery

- Seamor

- RYBHAND

- Eden Smokehouse

- W. van Wijk B.V.

- Seafood Connection

- FishPartners International