Global Salty Snacks Market Size

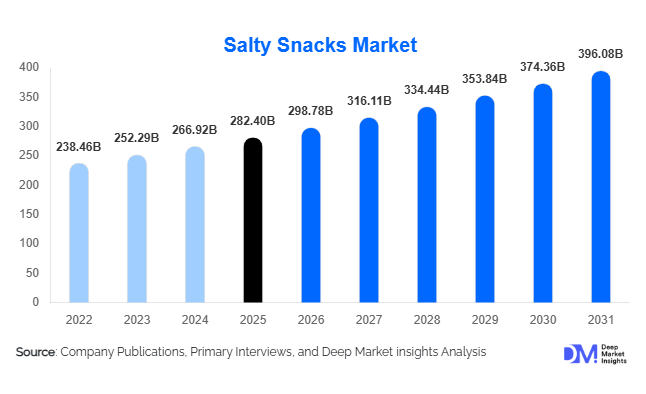

According to Deep Market Insights, the global salty snacks market size was valued at USD 282.4 billion in 2025 and is projected to grow from USD 298.78 billion in 2026 to reach USD 396.08 billion by 2031, expanding at a CAGR of 5.8% during the forecast period (2026–2031). The salty snacks market growth is primarily driven by rising consumer demand for convenient ready-to-eat foods, increasing snack consumption across all age groups, rapid urbanization, expanding retail infrastructure, and continuous product innovation across healthier, premium, and ethnic snack categories. Manufacturers are increasingly investing in clean-label formulations, high-protein snacks, plant-based alternatives, and sustainable packaging solutions to align with evolving consumer preferences. The growing penetration of e-commerce grocery platforms and direct-to-consumer sales channels is further accelerating market expansion globally.

Key Market Insights

- Potato chips remain the largest product category, accounting for approximately 31% of global salty snack revenues due to strong consumer familiarity and continuous flavor innovation.

- Health-focused snack formulations are gaining momentum, with reduced-sodium, baked, high-protein, and plant-based products recording above-market growth rates.

- Asia-Pacific dominates the global market, representing nearly 34% of global demand, driven by rapid urbanization and rising disposable incomes.

- India is emerging as the fastest-growing country market, supported by organized retail expansion, increasing packaged food consumption, and growing middle-class spending.

- E-commerce is transforming distribution channels, enabling manufacturers to reach consumers directly while enhancing product personalization and data-driven marketing.

- Premiumization remains a major industry trend, with consumers increasingly seeking gourmet flavors, artisanal ingredients, and premium snack experiences.

- Sustainable packaging and environmentally responsible sourcing are becoming key differentiators among global snack manufacturers.

Global Salty Snacks Market Latest Trends

Healthier Snacking Driving Product Innovation

Consumers worldwide are increasingly seeking healthier alternatives to traditional salty snacks, prompting manufacturers to invest heavily in product reformulation and nutritional enhancement. Baked chips, air-popped popcorn, protein-enriched snacks, lentil-based chips, vegetable crisps, and reduced-sodium offerings are witnessing robust demand growth across both developed and emerging markets. Clean-label ingredients, non-GMO formulations, organic certifications, and plant-based ingredients are becoming increasingly important purchase considerations. Manufacturers are responding by introducing snacks with improved nutritional profiles without compromising taste or texture. The trend is particularly prominent among millennials, Gen Z consumers, and health-conscious families who continue to drive demand for better-for-you snack alternatives.

Premium and Global Flavor Expansion

The market is witnessing significant premiumization as consumers increasingly seek differentiated snacking experiences. Manufacturers are launching globally inspired flavors such as Korean barbecue, spicy sriracha, peri-peri, truffle, Mediterranean herb blends, and regional ethnic seasonings. Limited-edition products, gourmet snack collections, and artisanal manufacturing processes are helping brands capture higher margins while enhancing consumer engagement. Premium snacks are increasingly positioned as affordable indulgences, enabling consumers to experiment with new taste experiences. This trend has become particularly important in mature markets such as North America and Europe, where product differentiation plays a crucial role in maintaining growth.

Global Salty Snacks Market Drivers

Growth of On-the-Go Consumption

Fast-paced lifestyles and increasing workforce participation continue to drive demand for convenient food options. Salty snacks offer portability, affordability, and ease of consumption, making them ideal for busy consumers. Single-serve packaging formats, resealable pouches, and multipack offerings have expanded consumption occasions across workplaces, schools, travel environments, and leisure activities. Urbanization and longer commuting times are further contributing to increased snack frequency globally. The ability of salty snacks to serve as meal supplements, quick energy sources, and convenient refreshment options continues to support long-term market growth.

Rising Demand for Premium and Experiential Foods

Consumers increasingly view snacks as experiential food products rather than simple convenience items. Premium ingredients, artisanal production methods, innovative flavor combinations, and unique textures are helping manufacturers capture higher-value market segments. Younger consumers are particularly receptive to experimental flavors and limited-edition product launches. Social media influence, food culture trends, and digital marketing campaigns have amplified interest in premium snack experiences, encouraging manufacturers to continuously innovate and differentiate their portfolios.

Expansion of Modern Retail and Digital Commerce

The rapid growth of supermarkets, hypermarkets, convenience stores, and online grocery platforms has significantly improved product accessibility worldwide. E-commerce channels allow consumers to access a broader range of snack products while enabling manufacturers to launch products more efficiently and gather valuable consumer insights. Subscription snack services, personalized product recommendations, and direct-to-consumer business models are further supporting category expansion across multiple regions.

Global Salty Snacks Market Restraints

Raw Material Price Volatility

The industry remains highly exposed to fluctuations in the prices of potatoes, corn, edible oils, wheat, nuts, seasonings, and packaging materials. Weather disruptions, geopolitical tensions, transportation costs, and agricultural supply shortages can significantly impact manufacturing costs and profit margins. Price volatility often creates challenges for long-term procurement planning and limits pricing flexibility for manufacturers operating in highly competitive markets.

Increasing Regulatory Pressure on Processed Foods

Governments across North America, Europe, and parts of Asia are implementing stricter regulations related to sodium content, nutritional labeling, food advertising, and health disclosures. Restrictions on marketing products to children and increasing public health concerns regarding obesity and cardiovascular disease are prompting manufacturers to reformulate products. Compliance with evolving regulations often requires substantial investments in research, development, testing, and packaging modifications, creating operational challenges for industry participants.

Global Salty Snacks Industry Key Opportunities

Expansion of Health-Oriented Snack Portfolios

The growing consumer focus on health and wellness presents one of the most attractive opportunities within the salty snacks market. Demand for high-protein snacks, low-fat products, plant-based formulations, gluten-free offerings, and functional snacks continues to increase globally. Manufacturers that successfully combine nutrition, convenience, and taste can capture premium pricing and attract new consumer segments. Functional ingredients such as probiotics, fiber, plant proteins, and micronutrient fortification offer additional opportunities for product differentiation. Health-oriented innovation is expected to remain a key growth driver throughout the forecast period.

Emerging Market Expansion and Localization

Rapidly developing economies including India, Indonesia, Vietnam, Saudi Arabia, Brazil, Mexico, and South Africa offer substantial untapped growth potential. Rising incomes, urban migration, changing dietary habits, and retail modernization are creating favorable conditions for packaged snack consumption. Manufacturers are increasingly localizing flavors, packaging formats, and marketing strategies to address regional preferences. Establishing local production facilities and sourcing networks can improve profitability while strengthening supply chain resilience.

Digital Commerce and Direct-to-Consumer Growth

The continued expansion of e-commerce presents significant opportunities for both established manufacturers and emerging brands. Online channels facilitate product discovery, targeted marketing, subscription models, and personalized customer engagement. Data analytics derived from digital commerce platforms enable manufacturers to respond more quickly to changing consumer preferences and optimize product portfolios. Direct-to-consumer channels also provide higher margins by reducing dependence on traditional retail intermediaries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 282.40 Billion |

| Market Size in 2026 | USD 298.78 Billion |

| Market Size in 2031 | USD 396.08 Billion |

| CAGR | 5.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Potato chips continue to dominate the global savory snacks landscape, accounting for approximately 31% of total market revenues. This leadership is primarily driven by strong consumer familiarity, deeply embedded snacking habits across age groups, continuous flavor innovation, and the product’s affordability and convenience, which makes it a preferred impulse purchase across both developed and emerging markets. Tortilla and corn chips represent the second-largest segment, benefiting from rising global exposure to ethnic cuisines, increased demand for dip-friendly snacks, and the growing popularity of Tex-Mex and Latin American food culture, which has significantly expanded their consumption occasions beyond traditional markets. Extruded snacks are witnessing sustained expansion, driven by advancements in extrusion technology that enable diversified formulations such as cheese-based variants, multigrain blends, and protein-enriched snacks catering to evolving health-conscious yet indulgent consumption preferences. Popcorn continues to gain traction due to its strong association with better-for-you snacking, low-calorie positioning, and versatility in both savory and sweet formats, making it a popular choice in at-home and entertainment consumption settings. Nuts and seeds snacks are experiencing robust growth supported by increasing consumer focus on natural protein sources, satiety benefits, and functional nutrition. Ethnic and regional savory snacks, including namkeen, rice crackers, seaweed snacks, and cassava-based products, are expanding globally as multicultural food preferences rise, driven by urbanization, international travel exposure, and consumer demand for authentic and culturally inspired taste experiences.

Processing Method Insights

Fried snacks continue to account for approximately 58% of global market value, maintaining dominance due to their superior taste profile, crispy texture, and long-standing consumer acceptance across all major regions. This segment’s leadership is reinforced by scalable production processes, cost efficiency, and strong compatibility with flavor enhancement technologies that enhance sensory appeal. However, the market is witnessing a clear structural shift toward healthier processing alternatives, with baked, roasted, and air-popped snacks gaining momentum at a faster pace. This transition is driven by rising health awareness, increasing concerns over fat intake, and growing demand for guilt-free indulgence among urban consumers. Manufacturers are actively investing in advanced processing technologies that reduce oil absorption while preserving taste and texture integrity, enabling healthier product portfolios without compromising sensory satisfaction. Hybrid processing techniques, including combinations of air frying, vacuum roasting, and low-oil baking, are also emerging as key innovation areas as companies seek to balance indulgence with nutritional expectations.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, contributing approximately 46% of global sales, supported by their extensive product assortment, strategic shelf placement, and promotional pricing strategies that drive high-volume consumer purchases. Their leadership is further strengthened by strong supplier partnerships and the ability to cater to both premium and mass-market snack categories under one retail environment. Convenience stores play a critical role in driving impulse purchases and immediate consumption demand, particularly in urban areas where fast-paced lifestyles increase reliance on quick snack options. Online retail is emerging as one of the fastest-growing channels, fueled by rapid digital transformation, expansion of grocery delivery platforms, subscription-based snack services, and data-driven personalized marketing strategies that enhance consumer engagement. Specialty food retailers are gaining importance within premium, organic, and health-focused segments as consumers increasingly seek curated and differentiated snack experiences. Meanwhile, foodservice and vending channels continue to expand steadily, supported by rising demand across corporate offices, educational institutions, transportation hubs, and hospitality environments, where packaged snacks are increasingly integrated into daily consumption routines.

End-Use Insights

Household consumption remains the largest end-use segment, accounting for approximately 82% of global demand, driven by increasing snacking frequency, evolving family consumption patterns, and the growing preference for at-home entertainment and convenience-based food consumption. This dominance is further supported by expanding retail availability and product diversification across price points, flavors, and health-oriented formulations. The foodservice segment represents the fastest-growing end-use category, driven by rapid urbanization, expansion of quick-service restaurants, and rising demand for grab-and-go packaged snacks across cafés, cinemas, airlines, and casual dining establishments. Institutional demand from corporate offices, educational facilities, healthcare institutions, and vending operators is also expanding as employers and service providers increasingly integrate packaged snacks into workplace and public consumption environments. Additionally, export-oriented demand continues to strengthen across major production hubs, with manufacturers leveraging cost efficiencies, large-scale production capabilities, and competitive pricing to serve international markets across North America, Europe, Southeast Asia, and India.

Nutritional Positioning Insights

Conventional salty snacks continue to dominate the global market with nearly 72% share, supported by strong consumer preference for familiar flavors, widespread availability, and affordability across all income segments. This category’s resilience is largely driven by habitual consumption patterns and its established position as a staple impulse snack worldwide. However, healthier alternatives are gaining significant traction and outperforming the broader market in growth terms, driven by rising awareness of lifestyle-related health concerns and a global shift toward functional nutrition. Reduced-fat, reduced-sodium, high-protein, organic, gluten-free, and plant-based snack segments are experiencing accelerated adoption, particularly among urban and younger demographics. High-protein snacks are increasingly driven by fitness-oriented consumers and active lifestyle trends, while organic and clean-label products are supported by demand for transparency, minimal processing, and natural ingredient sourcing. Plant-based snacks are benefiting from broader sustainability movements and dietary diversification, positioning nutritional innovation as a key competitive differentiator in the global savory snacks industry.

Explore more data points, trends and opportunities Download Free Sample Report

Salty Snacks Market Segmentations

By Product Type

- Potato Chips

- Tortilla & Corn Chips

- Extruded Snacks

- Popcorn

- Pretzels

- Nuts & Seeds Snacks

- Crackers & Savory Biscuits

- Meat-Based Salty Snacks

- Ethnic & Regional Salty Snacks

By Processing Method

- Fried

- Baked

- Air-Popped

- Roasted

- Dehydrated/Dried

- Hybrid Processing

By Ingredient Base

- Potato-Based

- Corn-Based

- Wheat-Based

- Rice-Based

- Legume-Based

- Nut & Seed-Based

- Meat-Based

- Vegetable-Based

- Multi-Grain-Based

By Flavor Profile

- Plain Salted

- Cheese

- Barbecue

- Spicy/Chili

- Sour Cream & Onion

- Herb & Seasoning

- Ethnic/Regional Flavors

- Other Innovative Flavors

By Nutritional Positioning

- Conventional

- Reduced Fat

- Reduced Sodium

- High Protein

- Organic

- Gluten-Free

- Clean Label/Natural

- Plant-Based/Vegan

Regional Insights

North America

North America accounts for approximately 28% of global market demand, supported by high per-capita snack consumption, strong brand penetration, and a highly developed retail ecosystem. The region’s growth is primarily driven by continuous product innovation, particularly in protein-enriched, organic, and better-for-you snack categories that align with evolving health-conscious consumer behavior. The United States remains the largest national market due to its established snacking culture and strong purchasing power, while Canada is witnessing increasing demand for premium and clean-label products driven by wellness trends. Mexico contributes to regional expansion through rising packaged food consumption, urbanization, and retail modernization, supported by growing accessibility to branded snack products across urban and semi-urban markets.

Europe

Europe represents approximately 24% of global market value and is characterized by a strong preference for premium, high-quality, and healthier snack alternatives. Market growth across the region is strongly influenced by stringent food regulations that encourage reduced-sodium, clean-label, and transparently sourced ingredients, accelerating product reformulation and innovation. Demand is particularly strong in Germany, the United Kingdom, France, Italy, and Spain, where consumers demonstrate a high willingness to pay for premium and artisanal snack products. Growth is further supported by increasing multicultural influence, which is driving demand for ethnic flavors and globally inspired snack varieties. Sustainability initiatives, packaging innovation, and responsible sourcing practices are also shaping competitive strategies across the European market landscape.

Asia-Pacific

Asia-Pacific is the largest regional market, accounting for nearly 34% of global revenues, and continues to be the fastest-evolving consumption hub for savory snacks. Growth is driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing adoption of Western-style snacking habits alongside traditional preferences. China leads the regional market, supported by strong manufacturing capabilities and large-scale consumption, while India is emerging as the fastest-growing market globally due to retail expansion, rising packaged food penetration, and increasing consumer spending on convenience foods. Japan, South Korea, and Indonesia contribute significantly through demand for innovative flavors, premium snack formats, and convenience-oriented products, reflecting shifting lifestyle patterns and busy urban consumption behaviors.

Latin America

Latin America accounts for approximately 8% of global demand, with Brazil and Mexico serving as the key growth engines for the region. Market expansion is driven by rising urbanization, improving disposable incomes, and increasing penetration of modern retail formats that enhance access to packaged snack products. Growth is further supported by strong consumer preference for bold, localized flavors, which has encouraged manufacturers to invest heavily in regional taste innovation and culturally relevant product development. Affordable packaging formats and value-oriented product positioning are also critical drivers, enabling wider market penetration across diverse income groups and supporting steady long-term consumption growth.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6% of global demand and presents significant long-term growth potential driven by demographic expansion, rapid urbanization, and increasing retail infrastructure development. Key markets such as Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Nigeria are witnessing rising consumption of packaged snacks supported by younger populations and growing demand for convenience-based food options. The region is also experiencing increased demand for premium imported snacks, driven by rising income levels and exposure to international food trends. Simultaneously, investments in local manufacturing capabilities are strengthening supply chain efficiency and improving product accessibility, while tourism, hospitality growth, and modern retail expansion continue to support sustained market development.

Key Players in the Global Salty Snacks Market

- PepsiCo

- Mondelez International

- Kellanova

- Campbell's Company

- The Hershey Company

- Calbee Inc.

- Intersnack Group

- Orkla ASA

- Want Want China Holdings

- Universal Robina Corporation

- ITC Limited

- Grupo Bimbo

- Arca Continental

- Tyrrells

- Lorenz Snack-World