Salted Fish Market Size

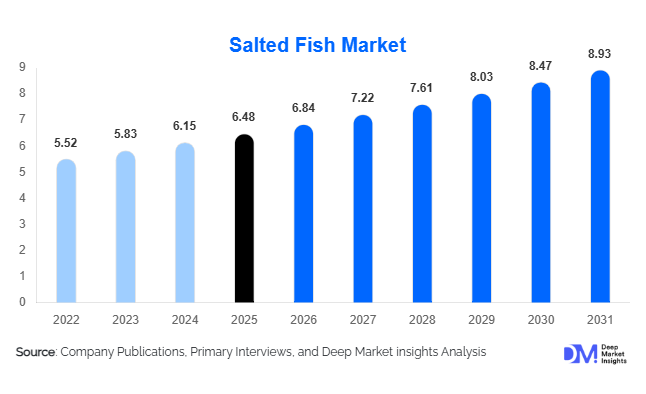

According to Deep Market Insights, the global salted fish market size was valued at USD 6.48 billion in 2025 and is projected to grow from USD 6.84 billion in 2026 to reach USD 8.93 billion by 2031, expanding at a CAGR of 5.5% during the forecast period (2026–2031). The salted fish market growth is primarily driven by rising demand for shelf-stable protein products, increasing consumption of traditional seafood-based cuisines, and the expansion of global seafood trade networks. Salted fish remains a critical food category across Asia-Pacific, Europe, Latin America, and Africa, where preservation methods continue to play a vital role in food security, affordability, and culinary heritage. Improvements in industrial processing, vacuum packaging, food safety compliance, and export-oriented production are further strengthening market growth. The increasing popularity of ethnic foods among migrant populations in North America and Europe is also contributing to sustained demand for premium salted fish products, particularly salted cod, anchovies, mackerel, and herring.

Key Market Insights

- Dry salted fish remains the dominant product category, accounting for approximately 46% of the global market due to its extended shelf life and lower logistics costs.

- Asia-Pacific dominates global consumption, supported by strong demand from China, Indonesia, Philippines, Vietnam, Thailand, and India.

- Africa is emerging as the fastest-growing consumption region, driven by rising protein demand and growing seafood imports.

- Cod continues to lead among fish species, representing nearly 28% of global salted fish revenues due to strong demand in Europe and Latin America.

- Vacuum packaging and modified atmosphere packaging (MAP) are becoming increasingly important for premium retail and export markets.

- Sustainability certifications and seafood traceability systems are reshaping procurement decisions among major retailers and foodservice operators globally.

Salted Fish Market Latest Trends

Premiumization of Traditional Seafood Products

Consumer preferences are increasingly shifting toward premium seafood products that combine traditional preservation methods with modern quality standards. Salted fish manufacturers are introducing high-grade salted cod, artisanal anchovies, sustainably sourced mackerel, and region-specific specialty products targeting affluent consumers. Premium packaging, origin labeling, sustainability certifications, and enhanced traceability are becoming important differentiators. Retailers across Europe, North America, Japan, and South Korea are allocating additional shelf space to premium seafood products, allowing producers to achieve higher margins while preserving traditional culinary authenticity.

Growth of Sustainable and Traceable Seafood Supply Chains

Sustainability has become a major focus across the global seafood industry. Large buyers increasingly require suppliers to demonstrate responsible fishing practices, traceability compliance, and environmental stewardship. Salted fish producers are investing in digital traceability systems, sustainable fishery certifications, blockchain-enabled supply chain monitoring, and improved procurement practices. These initiatives help manufacturers access premium export markets while meeting evolving consumer expectations. Sustainable sourcing has become particularly important among European retailers and foodservice chains that increasingly prioritize certified seafood products within their procurement strategies.

Salted Fish Market Drivers

Growing Demand for Shelf-Stable Protein Sources

Salted fish offers a highly practical solution for protein preservation, particularly in regions where refrigeration infrastructure remains limited. Consumers in emerging economies continue to rely on preserved seafood as an affordable and accessible protein source. Population growth, urbanization, and rising food security concerns are driving increased consumption of shelf-stable seafood products. Salted fish also maintains nutritional value while significantly extending storage life, making it attractive for households, institutions, and foodservice operators seeking cost-effective protein solutions.

Expansion of Global Seafood Trade Networks

The growth of international seafood trade has significantly benefited the salted fish industry. Unlike fresh seafood, salted fish can be transported across long distances with lower spoilage risks and reduced cold-chain requirements. Major exporting countries including Norway, Iceland, China, Vietnam, and India continue to strengthen production capabilities and export infrastructure. Improved logistics, trade agreements, and growing international demand for ethnic foods have enabled producers to expand their global market presence while improving supply chain efficiency.

Strong Cultural and Traditional Food Consumption Patterns

Salted fish remains deeply embedded in traditional cuisines across Asia, Southern Europe, Latin America, and Africa. Dishes utilizing salted cod, anchovies, sardines, and fermented fish products continue to experience stable demand. Cultural preservation, migration patterns, and growing international exposure to ethnic cuisines have strengthened long-term consumption trends. Foodservice operators and specialty retailers are increasingly leveraging traditional seafood products to cater to both diaspora communities and adventurous consumers seeking authentic culinary experiences.

Salted Fish Market Restraints

Raw Material Price Volatility

The industry remains highly exposed to fluctuations in fish availability and procurement costs. Climate change impacts, fishing quota restrictions, seasonal variations, and sustainability regulations can significantly affect raw material supplies. Price volatility creates uncertainty for processors and exporters, potentially compressing profit margins and increasing retail prices. Maintaining stable supply chains remains a critical challenge for market participants.

Stringent Food Safety and Trade Regulations

Export-oriented producers must comply with increasingly complex food safety, traceability, labeling, and sustainability requirements. Compliance costs can be substantial, particularly for smaller processors operating in developing economies. Certification programs, laboratory testing, documentation requirements, and regulatory audits often require significant investments, creating barriers to international market expansion and reducing competitiveness for smaller suppliers.

Salted Fish Industry Key Opportunities

Expansion of Ethnic Food Consumption Globally

Growing migration and multicultural food consumption trends are creating significant opportunities for salted fish producers. Demand for traditional seafood products is increasing among immigrant communities across North America, Europe, and Australia. Retailers are expanding ethnic food offerings, creating new distribution channels for specialty salted fish products. Producers capable of maintaining authenticity while meeting modern food safety standards are well positioned to benefit from this trend.

Growing Demand Across African Markets

Sub-Saharan Africa represents one of the most attractive growth opportunities for the global salted fish industry. Countries such as Nigeria, Ghana, Angola, Côte d'Ivoire, and Senegal continue to experience rising protein demand driven by population growth and urbanization. Salted fish provides an affordable alternative to fresh seafood and meat products, making it increasingly important for food security. Growing imports across the region are expected to support long-term market expansion.

Sustainable Seafood and Premium Product Innovation

Investment in sustainability certifications, eco-labeling, premium packaging, and traceability technologies offers significant opportunities for value creation. Consumers are increasingly willing to pay premium prices for responsibly sourced seafood products. Producers that successfully integrate sustainable sourcing and transparent supply chains can strengthen market positioning while accessing high-value retail and foodservice segments in developed markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.48 |

| Market Size in 2026 | USD 6.84 |

| Market Size in 2031 | USD 8.93 |

| CAGR | 5.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Dry salted fish continues to dominate the global salted seafood market, accounting for approximately 46% of total market share in 2025. Its leadership is primarily driven by its superior preservation efficiency, extended shelf life without refrigeration, and cost-effective logistics, making it highly suitable for long-distance trade and storage in regions with limited cold-chain infrastructure. Strong cultural integration in culinary traditions across Asia-Pacific, parts of Africa, and Southern Europe further reinforces sustained demand. In addition, increasing preference for minimally processed, naturally preserved seafood products is strengthening its position in both retail and wholesale channels.Wet salted fish maintains a stable and significant presence, particularly in Mediterranean countries and Latin American coastal economies where brined and semi-preserved seafood products are deeply embedded in traditional diets. Demand in this segment is further supported by artisanal production methods and strong seasonal consumption patterns linked to cultural festivals and religious observances. Fermented salted fish continues to demonstrate resilient demand in Southeast Asia, where it plays a central role in regional cuisines and is increasingly utilized in industrial food processing for sauces, flavor enhancers, and ready-to-eat meal applications. Meanwhile, smoked and salted fish products are emerging as a higher-value category, driven by premiumization trends, urban lifestyle shifts, and rising consumer interest in gourmet and convenience-oriented seafood offerings.

Fish Species Insights

Cod remains the most dominant species segment, contributing approximately 28% of global market revenues, supported by strong consumption across Portugal, Spain, Brazil, and Nordic countries. The leadership of cod is reinforced by its established role in traditional dishes, particularly salted and dried preparations, along with its strong export-driven trade ecosystem from Northern Europe. Demand stability is further supported by its adaptability across retail, foodservice, and industrial processing applications.Mackerel represents the second-largest species category, benefiting from its affordability, wide availability, and strong consumption base in Africa, Asia, and parts of Europe. Its growth is largely driven by increasing demand for cost-effective protein sources in developing economies and its suitability for bulk preservation methods. Herring and sardines continue to serve mass-market demand, particularly in regions where affordability and nutritional density are key purchasing factors, with strong penetration in canned and salted formats. Anchovies occupy a premium niche segment, driven by their extensive use in Mediterranean cuisine, gourmet foodservice applications, and high-value processed food formulations. Tuna and pollock are experiencing increasing traction in value-added processing industries, supported by rising demand for convenient seafood snacks, packaged meals, and export-oriented premium seafood product lines.

Distribution Channel Insights

Traditional wholesale markets continue to dominate global salted fish distribution, particularly across Asia and Africa, where fragmented retail structures and strong reliance on informal trade networks sustain their leadership. The dominance of this channel is reinforced by bulk purchasing patterns, price sensitivity among consumers, and limited cold-chain penetration in rural and semi-urban areas.Supermarkets and hypermarkets are steadily expanding their share, driven by urbanization, rising disposable incomes, and increasing consumer preference for hygienically packaged and standardized seafood products. Specialty seafood retailers remain important in developed markets, particularly for premium, imported, and artisanal salted fish varieties where product differentiation and origin traceability are key purchasing drivers. Online retail is emerging as the fastest-growing channel, supported by digital adoption, improved cold-chain logistics, and the expansion of direct-to-consumer seafood delivery platforms. Foodservice distributors also continue to play a critical role by ensuring consistent supply to restaurants, hotels, catering services, and institutional kitchens, where demand for bulk and standardized seafood inputs remains strong.

End-Use Insights

Household consumption remains the largest end-use segment, accounting for approximately 54% of total market demand. This dominance is primarily driven by affordability, long storage life, and deep cultural integration of salted fish in home cooking across emerging economies. In rural and coastal regions, salted fish continues to serve as a primary protein source, especially where refrigeration access is limited or inconsistent.The foodservice sector is emerging as the fastest-growing end-use category, supported by rapid expansion of global restaurant chains, increased consumption of ethnic cuisines, and rising demand for seafood-based dishes in urban dining formats. Growth in tourism and hospitality industries is further accelerating consumption in this segment. Food processing applications are also expanding, with salted fish increasingly used as a functional ingredient in ready meals, soups, sauces, seasonings, and packaged snacks, driven by demand for umami-rich flavors and natural preservatives. Institutional demand remains stable, supported by procurement from military organizations, disaster relief programs, and government food security initiatives, where salted fish is valued for its durability, ease of storage, and nutritional reliability in large-scale distribution systems.

Packaging Type Insights

Bulk packaging continues to dominate industrial and wholesale distribution, particularly in emerging markets where large-volume trade and cost efficiency remain key priorities. Its leadership is reinforced by traditional supply chain structures and the need for flexible redistribution across fragmented retail networks.Vacuum packaging is witnessing rapid growth, driven by increasing demand for extended shelf life, improved hygiene standards, and enhanced export competitiveness. It is particularly gaining traction in premium retail and international trade channels where product integrity and freshness preservation are critical. Modified atmosphere packaging (MAP) is becoming increasingly important in high-end retail environments, where visual appeal, shelf stability, and reduced spoilage rates are essential value drivers. Retail-ready pouches and canned formats are also expanding steadily, supported by growing demand for convenience-oriented seafood products aligned with modern urban consumption patterns and on-the-go lifestyles.

Explore more data points, trends and opportunities Download Free Sample Report

Salted Fish Market Segmentations

By Product Form

- Dry Salted Fish

- Wet Salted Fish

- Fermented Salted Fish

- Smoked & Salted Fish

By Fish Species

- Cod

- Mackerel

- Herring

- Sardine

- Anchovy

- Tuna

- Pollock

- Other Marine Species

By Processing Method

- Traditional Salt Curing

- Industrial Salt Curing

- Vacuum Salt Curing

- Hybrid Salting & Drying

By Packaging Type

- Bulk Packaging

- Vacuum Packaging

- Modified Atmosphere Packaging (MAP)

- Retail Pouches

- Canned & Jarred Formats

By Distribution Channel

- Wholesale Markets

- Supermarkets & Hypermarkets

- Specialty Seafood Stores

- Convenience Stores

- Online Retail & E-commerce

- Foodservice Distributors

Regional Insights

Asia-Pacific

Asia-Pacific leads the global salted fish market with approximately 42% market share in 2025, driven by strong cultural integration of preserved seafood in daily diets and extensive coastal consumption patterns. China remains the dominant consumer, supported by its large population base, well-established seafood processing industry, and strong domestic demand for traditional preserved fish products. Indonesia, Vietnam, the Philippines, Thailand, and India are experiencing accelerated growth, driven by rising incomes, rapid urbanization, and expanding middle-class consumption patterns. Regional growth is further reinforced by strong export-oriented seafood industries, increasing investment in cold-chain infrastructure, and the expansion of modern retail formats, which collectively enhance accessibility and product standardization.

Europe

Europe accounted for approximately 24% of global revenues in 2025, supported by long-standing culinary traditions and strong demand for salted cod and other preserved fish varieties. Portugal remains a central consumption hub, with deeply rooted cultural reliance on salted cod in national cuisine. Spain, Italy, Norway, and Iceland also contribute significantly, driven by both domestic consumption and export-oriented seafood processing industries. Regional growth is increasingly influenced by sustainability regulations, traceability requirements, and consumer preference for high-quality, responsibly sourced seafood products. In addition, Europe functions as a major global re-export hub for premium salted cod, supporting international trade flows across multiple regions.

North America

North America’s salted fish market is primarily driven by ethnic food demand, premium seafood consumption, and growing culinary diversification. The United States leads the region, supported by expanding immigrant populations and rising interest in international cuisines that incorporate salted and preserved fish. Canada contributes through both domestic consumption and its well-developed seafood processing sector. Market growth is further supported by increasing demand for sustainably sourced, traceable, and high-quality seafood products, alongside a broader consumer shift toward natural preservation methods and clean-label food offerings.

Latin America

Latin America demonstrates steady growth, with Brazil representing the largest market due to strong seasonal demand for salted cod during cultural and religious celebrations. Consumption patterns are deeply influenced by European culinary heritage, particularly Portuguese traditions. Mexico, Colombia, Peru, and Chile are also witnessing consistent growth, supported by expanding retail penetration and increasing consumer awareness of preserved seafood products. Market expansion is further driven by improving supply chain infrastructure, rising disposable incomes, and the gradual modernization of food retail systems across urban centers.

Middle East & Africa

The Middle East & Africa region is expected to be the fastest-growing market over the forecast period, driven by strong population growth, rapid urbanization, and increasing demand for affordable protein sources. In Africa, countries such as Nigeria, Ghana, Angola, Senegal, and Côte d'Ivoire account for significant consumption, where salted fish plays a critical role in food security due to its affordability, availability, and long shelf life in environments with limited refrigeration infrastructure. In the Middle East, particularly in Saudi Arabia and the UAE, demand is rising for premium imported salted seafood products, supported by growing expatriate populations and expanding foodservice industries. Continued infrastructure development, improvements in cold-chain logistics, and rising retail modernization are expected to further accelerate regional market growth.

Key Players in the Salted Fish Market

- Jacob Bjørge AS

- Lorentz A. Lossius AS

- Fjordlaks AS

- Seacore Seafood

- LSK Fishery

- Royal Greenland

- Grupo Nueva Pescanova

- Iceland Seafood International

- Brim Seafood

- Thai Union Group

- Nissui Corporation

- Maruha Nichiro Corporation

- Austevoll Seafood

- Lerøy Seafood Group

- Biscay Seafood