Processed Vegetables Market Size

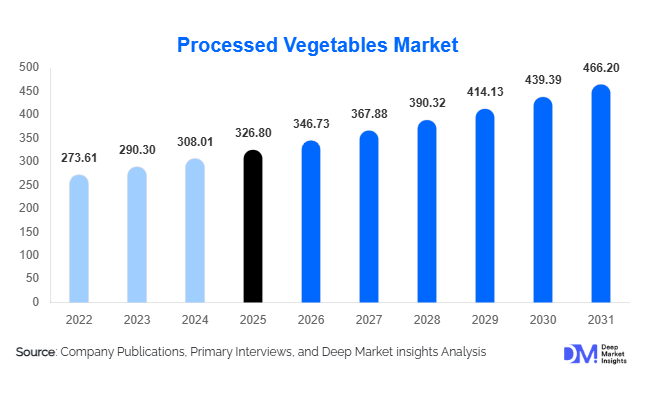

According to Deep Market Insights, the global processed vegetables market size was valued at USD 326.8 billion in 2025 and is projected to grow from USD 346.73 billion in 2026 to reach USD 466.20 billion by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The processed vegetables market growth is primarily driven by rising demand for convenient food products, expanding cold-chain infrastructure, increasing foodservice consumption, and growing adoption of shelf-stable and ready-to-cook vegetable products across both developed and emerging economies. As consumers seek healthier convenience foods with longer shelf life and minimal preparation requirements, processed vegetables have become an essential component of household consumption, food manufacturing, institutional catering, and restaurant operations worldwide.

Key Market Insights

- Frozen vegetables remain the largest product category, accounting for over 40% of global market revenue due to superior nutrient retention, convenience, and expanding cold-chain networks.

- Foodservice demand is accelerating globally, with restaurants, quick-service chains, hotels, and institutional kitchens increasingly utilizing processed vegetables to improve operational efficiency.

- Asia-Pacific dominates the global processed vegetables market, supported by large-scale vegetable production, urbanization, and growing consumption of packaged food products.

- India is emerging as one of the fastest-growing markets, driven by government support for food processing, retail modernization, and increasing consumer demand for convenience foods.

- Technological advancements in freezing, dehydration, and packaging are improving product quality, shelf life, and supply-chain efficiency across the industry.

- Clean-label, organic, and minimally processed vegetable products are gaining popularity as consumers increasingly prioritize health, sustainability, and transparency.

Processed Vegetables Market Latest Trends

Premium and Clean-Label Vegetable Products Gaining Momentum

Consumer preferences are increasingly shifting toward healthier processed food alternatives that offer transparency, natural ingredients, and minimal preservatives. As a result, food manufacturers are investing heavily in organic frozen vegetables, low-sodium canned vegetables, preservative-free vegetable blends, and sustainably sourced products. Retailers across North America and Europe continue expanding shelf space for premium processed vegetable offerings, while consumers demonstrate greater willingness to pay for products carrying organic certifications, non-GMO labels, and sustainability credentials. The trend is encouraging manufacturers to strengthen farm-to-fork traceability and invest in regenerative agricultural sourcing programs that enhance product differentiation and consumer trust.

Advanced Processing Technologies Enhancing Product Quality

The industry is witnessing widespread adoption of advanced preservation technologies such as Individually Quick Frozen (IQF) processing, high-pressure processing (HPP), automated sorting systems, and AI-driven quality inspection solutions. These technologies improve nutrient retention, texture, appearance, and shelf life while reducing food waste and operational costs. Smart packaging solutions that monitor freshness and optimize storage conditions are also gaining traction. Food processors are increasingly investing in automation and digital manufacturing systems to improve throughput, enhance quality consistency, and address labor shortages, particularly in major processing hubs across Europe, North America, and Asia-Pacific.

Processed Vegetables Market Drivers

Growing Demand for Convenience Foods

Rapid urbanization, rising workforce participation, and increasingly busy lifestyles are driving global demand for convenient food products. Consumers are seeking meal solutions that require minimal preparation while delivering nutritional value and affordability. Processed vegetables address these requirements by offering ready-to-cook, ready-to-eat, and shelf-stable options suitable for modern households. Frozen vegetables, in particular, continue gaining popularity due to their convenience and ability to maintain nutritional content over extended storage periods.

Expansion of Cold-Chain Infrastructure

Significant investments in refrigerated transportation, cold storage facilities, and temperature-controlled retail infrastructure are supporting processed vegetables market growth. Emerging economies such as India, China, Indonesia, Brazil, and Saudi Arabia are expanding cold-chain capacity to reduce food losses and improve food distribution efficiency. This infrastructure development is enabling broader market penetration of frozen vegetable products while improving product availability in secondary and tertiary urban centers.

Rising Foodservice and Institutional Procurement

Restaurants, hotels, hospitals, schools, corporate cafeterias, and catering providers increasingly rely on processed vegetables to reduce labor requirements, improve consistency, and minimize food waste. Standardized quality, predictable inventory management, and cost efficiencies continue driving adoption across commercial kitchens worldwide. The expansion of quick-service restaurants and cloud kitchens further strengthens demand for processed vegetable ingredients used in soups, sauces, prepared meals, and side dishes.

Processed Vegetables Market Restraints

Volatility in Agricultural Raw Material Prices

Vegetable processors remain exposed to fluctuations in crop yields caused by adverse weather events, labor shortages, disease outbreaks, and climate-related disruptions. Variability in agricultural commodity prices can significantly impact production costs and profit margins. Manufacturers must increasingly invest in supply-chain resilience, contract farming arrangements, and diversified sourcing strategies to mitigate procurement risks.

Consumer Preference for Fresh Produce

Although acceptance of processed vegetables continues to increase, a segment of consumers still perceives fresh vegetables as healthier and more natural alternatives. This perception creates challenges for processors, particularly in premium health-conscious consumer segments. Continuous product innovation, nutritional education, and improvements in processing technologies remain critical for addressing these concerns and strengthening market adoption.

Processed Vegetables Industry Key Opportunities

Expansion of Foodservice and Quick-Service Restaurant Networks

The continued growth of global restaurant chains, institutional catering services, cloud kitchens, and food delivery platforms presents significant opportunities for processed vegetable suppliers. Commercial food operators increasingly prioritize standardized ingredients that reduce preparation time and ensure consistent product quality. Manufacturers capable of offering customized vegetable blends, portion-controlled formats, and value-added ingredients are well-positioned to secure long-term supply agreements with major foodservice customers.

Technology-Driven Manufacturing and Premium Product Development

Investments in advanced freezing technologies, smart packaging systems, AI-powered processing facilities, and automation create opportunities for productivity improvement and product differentiation. Companies adopting next-generation processing technologies can improve quality retention, reduce waste, and achieve higher operating margins. Simultaneously, demand for organic, clean-label, and minimally processed vegetables provides attractive growth opportunities for premium product manufacturers seeking higher-value market segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 326.80 |

| Market Size in 2026 | USD 346.73 |

| Market Size in 2031 | USD 466.20 |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Frozen vegetables continue to dominate the global processed vegetables market, contributing approximately 43% of total revenue, primarily driven by accelerating consumer demand for convenience-oriented food solutions, rapid urbanization, and the increasing prevalence of dual-income households with limited cooking time. The strong expansion of cold-chain logistics and retail freezer infrastructure has significantly enhanced product accessibility, further reinforcing category leadership. Individually Quick Frozen (IQF) vegetables are witnessing particularly strong momentum as they offer superior texture preservation, portion flexibility, and minimal wastage, making them highly preferred across both household and foodservice applications where quality consistency is essential. Canned vegetables remain a resilient segment supported by their affordability, extended shelf stability, and critical role in institutional food programs and emergency food supply chains, especially in regions with inconsistent refrigeration access. Dehydrated and dried vegetables are expanding steadily due to rising demand from snack manufacturers, instant meal producers, and industrial ingredient users seeking lightweight, cost-efficient, and long-lasting inputs. Pickled and fermented vegetables are gaining traction under the influence of growing consumer awareness of gut health, functional nutrition, and traditional food revival trends. Meanwhile, vegetable purees, pastes, and concentrates continue to serve as foundational ingredients across sauces, soups, ready meals, and large-scale food manufacturing, driven by the ongoing expansion of processed and convenience food categories globally.

Processing Technology Insights

Freezing technology represents the leading processing segment, accounting for nearly 45% of the global processed vegetable market value, supported by its ability to preserve freshness, nutritional integrity, and sensory quality over extended storage periods. Its dominance is strongly reinforced by the global expansion of refrigerated supply chains, rising demand for ready-to-cook products, and increasing reliance on export-oriented frozen food trade. IQF technology, in particular, is emerging as a preferred sub-segment due to its capability to maintain individual product integrity while reducing food waste and improving portion control efficiency for both retail consumers and commercial kitchens. Thermal processing and canning technologies remain widely adopted owing to their cost efficiency, scalability, and proven shelf-stability benefits, especially in developing economies and institutional foodservice environments. Drying and dehydration technologies are gaining importance in ingredient manufacturing and international trade applications where reduced weight and extended shelf life are critical logistical advantages. Fermentation-based processing is gradually expanding, driven by rising demand for probiotic-rich, functional, and naturally preserved food products. Additionally, advanced technologies such as high-pressure processing and vacuum preservation are increasingly being adopted in premium product segments, supported by consumer interest in minimally processed foods with enhanced nutritional retention and freshness.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels, accounting for nearly half of global processed vegetable sales, driven by their extensive product assortment, strong private-label penetration, and broad geographic reach across urban and semi-urban markets. The continued modernization and consolidation of retail infrastructure globally has significantly strengthened their influence over consumer purchasing behavior. Traditional grocery stores continue to play a critical role in emerging economies where modern retail penetration remains limited and localized purchasing patterns persist. Online grocery platforms are experiencing rapid expansion, fueled by digital transformation, improved last-mile logistics, and increasing consumer preference for home delivery of frozen and packaged foods, particularly in urban centers. Club stores, cash-and-carry formats, and specialty food retailers are also contributing meaningfully to market growth by catering to bulk buyers, institutional customers, and premium consumer segments seeking differentiated and high-quality product offerings.

End-Use Insights

Household consumers represent the largest end-use segment, accounting for approximately 56% of global processed vegetable demand, primarily driven by increasing reliance on convenience foods, time-saving meal preparation solutions, and the widespread adoption of frozen and packaged food products in daily diets. Rising urbanization and changing lifestyle patterns continue to reinforce this dominance. Foodservice is the fastest-growing end-use category, supported by the global expansion of quick-service restaurants, cloud kitchens, institutional catering, and hospitality sectors, all of which depend heavily on processed vegetables for operational efficiency, consistency, and cost control. Food processing manufacturers also form a significant demand base, utilizing processed vegetables as essential inputs in ready meals, soups, sauces, frozen entrees, and snack products, with growth driven by the increasing global consumption of packaged and convenience foods. Institutional buyers, including hospitals, educational institutions, defense organizations, and corporate cafeterias, are increasingly adopting processed vegetables to streamline food preparation processes, improve hygiene standards, and ensure consistent nutritional delivery at scale.

Vegetable Category Insights

Tomato-based products remain the leading vegetable category, contributing approximately 22% of global processed vegetable revenue, driven by their indispensable role in sauces, soups, condiments, and ready-to-eat meal formulations across both household and industrial applications. Their dominance is further reinforced by the global popularity of tomato-based cuisines and the scalability of tomato processing in industrial food manufacturing. Root vegetables, including potatoes, carrots, and beets, maintain strong market presence due to their versatility, long storage life, and extensive usage across frozen, canned, and dehydrated formats. Leafy vegetables are witnessing increasing demand within premium frozen and minimally processed segments as consumers prioritize nutrient-rich and fresh-tasting food options. Legumes and beans are expanding steadily, supported by rising global interest in plant-based nutrition, protein-rich diets, and vegetarian food alternatives. Additionally, peppers, cucumbers, brassica vegetables, and mixed vegetable blends continue to diversify product portfolios across multiple processing formats, enabling manufacturers to cater to evolving consumer taste preferences and convenience-driven demand.

Explore more data points, trends and opportunities Download Free Sample Report

Processed Vegetables Market Segmentations

By Product Type

- Frozen Vegetables

- Canned Vegetables

- Dehydrated & Dried Vegetables

- Pickled & Fermented Vegetables

- Vegetable Purees, Pastes & Concentrates

- Chilled/Minimally Processed Vegetables

By Processing Technology

- Freezing

- Thermal Processing/Canning

- Drying & Dehydration

- Fermentation

- High Pressure Processing (HPP)

- Vacuum Processing

- Other Preservation Technologies

By Vegetable Category

- Tomato-Based Products

- Root Vegetables

- Leafy Vegetables

- Brassica Vegetables

- Legumes & Beans

- Cucumbers & Gourds

- Peppers & Capsicum

- Mixed Vegetable Products

By Packaging Format

- Cans

- Flexible Pouches

- Glass Jars

- Cartons

- Plastic Trays & Containers

- Bulk Industrial Packaging

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Traditional Grocery Stores

- Online Retail

- Club Stores & Cash-and-Carry

- Specialty Food Retailers

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global processed vegetables market with approximately 34% share, driven by rapid urbanization, expanding middle-class populations, and the strong integration of processed foods into daily diets. China remains the largest producer and consumer, supported by extensive agricultural output, large-scale food processing capabilities, and robust domestic demand from both retail and foodservice sectors. India is emerging as a high-growth market, propelled by government-led food processing initiatives, rapid retail modernization, and significant investments in cold-chain infrastructure that improve distribution efficiency and reduce post-harvest losses. Japan and South Korea continue to demonstrate strong demand for premium, high-quality frozen and convenience-oriented vegetable products, influenced by aging populations and busy urban lifestyles. Southeast Asian countries are also experiencing accelerated growth due to rising disposable incomes, expanding quick-service restaurant chains, and increasing penetration of packaged and frozen food categories.

Europe

Europe accounts for approximately 26% of global demand and functions as both a major consumption hub and a key processing and export region. Growth is strongly supported by stringent food quality regulations, high consumer awareness regarding clean-label and sustainable food products, and advanced food processing technologies that enhance product quality and safety. Countries such as Germany, France, the United Kingdom, Italy, Spain, Poland, and the Netherlands represent core markets with well-established retail ecosystems and high frozen food adoption rates. Sustainability initiatives focused on reducing food waste and carbon emissions are further accelerating demand for processed and frozen vegetables. The Netherlands and Poland serve as strategic manufacturing and export hubs, leveraging advanced logistics infrastructure and efficient agricultural supply chains to distribute processed vegetables across Europe and international markets.

North America

North America represents approximately 24% of global market revenue, with the United States serving as the dominant contributor due to its highly developed cold-chain infrastructure, large-scale foodservice industry, and strong consumer preference for convenience foods. Growth is primarily driven by increasing demand for frozen and ready-to-eat meals, alongside a rising focus on healthier eating habits that support the adoption of vegetable-rich diets. Canada contributes meaningfully through strong household consumption patterns and institutional foodservice demand. The region is also witnessing growing interest in organic, non-GMO, and minimally processed vegetable products, supported by heightened health awareness and evolving dietary preferences among consumers seeking both convenience and nutritional value.

Latin America

Latin America is experiencing steady growth, primarily driven by urbanization, rising disposable incomes, and expanding modern retail infrastructure. Brazil and Mexico are the largest markets, benefiting from increasing consumption of packaged and convenience foods alongside growing foodservice penetration. The expansion of supermarkets and hypermarkets is improving product accessibility and encouraging greater adoption of processed vegetables across urban populations. Additionally, increasing investments by multinational food companies are strengthening regional processing capabilities, while Mexico’s export-oriented vegetable processing industry plays a significant role in supporting regional production and international trade flows.

Middle East & Africa

The Middle East and Africa region is witnessing consistent growth driven by rising food security initiatives, rapid urban population expansion, and significant investments in cold-chain and food distribution infrastructure. Key markets including Saudi Arabia, the United Arab Emirates, Egypt, South Africa, and Morocco are leading regional demand. Gulf countries, in particular, exhibit strong reliance on imports due to limited domestic agricultural output, creating substantial opportunities for international processed vegetable suppliers. Additionally, growth in tourism, hospitality, and institutional foodservice sectors is further accelerating demand, while government-led diversification strategies and food security programs continue to support long-term market expansion.

Key Players in the Processed Vegetables Market

- Bonduelle

- Greenyard

- Del Monte Foods

- Conagra Brands

- McCain Foods

- Seneca Foods

- B&G Foods

- Birds Eye Foods

- Kraft Heinz

- Nestlé

- Ardo

- Dole Food Company

- General Mills

- Ajinomoto

- Campbell Soup Company