Potato Market Size

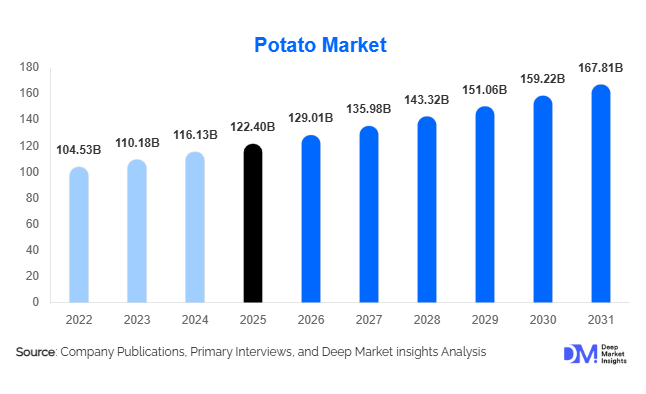

According to Deep Market Insights, the global potato market size was valued at USD 122.40 billion in 2025 and is projected to grow from USD 129.01 billion in 2026 to reach USD 167.81 billion by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The potato market growth is primarily driven by rising global demand for processed potato products, increasing consumption of convenience foods, expansion of quick-service restaurant chains, and growing investments in cold-chain and food processing infrastructure worldwide.

Key Market Insights

- Processed potato consumption is increasing globally, particularly frozen fries, chips, and dehydrated potato products driven by urban lifestyles and convenience food demand.

- Asia-Pacific dominates the global potato market, led by large-scale production and consumption in China and India.

- Frozen potato products represent the fastest-growing category, supported by expansion of fast-food chains and organized foodservice industries.

- Precision agriculture and smart farming technologies are transforming potato cultivation, improving yields, reducing water usage, and minimizing crop losses.

- Potato starch applications are expanding across industrial sectors, including food processing, paper manufacturing, textiles, and biodegradable materials.

- Sustainability-focused cultivation and organic potato production are gaining traction, especially across North America and Europe.

potato market latest trends

Rapid Expansion of Processed Potato Consumption

The global potato market is increasingly shifting toward value-added processed products such as frozen French fries, wedges, hash browns, potato flakes, and chips. Rising urbanization, changing dietary habits, and growing consumer preference for convenience foods are accelerating demand across both developed and emerging economies. International quick-service restaurant chains continue expanding aggressively across Asia-Pacific, Latin America, and the Middle East, significantly boosting demand for processing-grade potatoes. Food manufacturers are also introducing premium and flavored potato-based snacks, healthier baked variants, and ready-to-cook frozen potato meals to capture evolving consumer preferences. Growth in organized retail and e-commerce grocery channels is further improving the availability and accessibility of processed potato products globally.

Technology Integration in Potato Farming and Processing

Advanced agricultural technologies are increasingly being adopted across the potato value chain. Precision farming solutions including AI-based crop monitoring, satellite imagery, automated irrigation systems, GPS-enabled tractors, and soil analytics are improving productivity while reducing operational costs. Automated harvesting and grading systems are helping growers minimize post-harvest losses and improve supply consistency. In processing facilities, investments in energy-efficient freezing technologies, robotic sorting systems, and smart packaging solutions are increasing production efficiency. Sustainability initiatives including water recycling systems, low-carbon processing plants, and biodegradable packaging are also becoming major industry trends as manufacturers focus on reducing environmental impact.

potato market drivers

Growing Demand from Quick-Service Restaurants and Foodservice

The rapid expansion of global quick-service restaurant chains remains one of the strongest drivers for the potato market. French fries continue to represent one of the most consumed fast-food side dishes globally, creating sustained demand for high-starch processing potatoes. Rising disposable incomes, urbanization, and increasing consumer preference for convenience dining are fueling foodservice expansion across emerging economies including India, Indonesia, Saudi Arabia, Brazil, and Vietnam. Large restaurant chains are increasingly entering long-term procurement contracts with potato processors and growers to ensure stable supply and quality consistency. Additionally, growth in cloud kitchens, delivery-focused restaurants, and café chains is further strengthening institutional potato demand globally.

Increasing Adoption of Modern Agricultural Practices

Farm modernization and precision agriculture adoption are significantly improving potato cultivation productivity worldwide. Governments and private agribusiness companies are investing heavily in mechanized farming, advanced seed varieties, automated irrigation systems, and disease-resistant potato strains. Precision fertilizer application and climate monitoring technologies are helping improve yield per hectare while reducing water and chemical consumption. The growing use of cold storage infrastructure is also reducing spoilage and stabilizing supply chains, particularly in developing economies where post-harvest losses historically remained high. These technological improvements are supporting stable market expansion and improving profitability for growers and processors alike.

global market restraints

Climate Volatility and Water Scarcity

Potato cultivation remains highly sensitive to climate fluctuations, making weather-related risks a major challenge for market participants. Droughts, floods, heatwaves, and irregular rainfall patterns are impacting productivity across major producing regions. Rising temperatures and water scarcity are particularly concerning in regions heavily dependent on irrigation systems. Climate change is also increasing the risk of pest infestations and crop diseases, resulting in higher operational uncertainty for growers. Inconsistent yields can create pricing volatility and disrupt supply chains, particularly for large food processors dependent on stable raw material availability.

Volatile Input Costs and Supply Chain Challenges

Fluctuating fertilizer prices, fuel costs, labor shortages, refrigeration expenses, and transportation costs continue to pressure profit margins across the potato value chain. Rising energy prices have significantly increased operational costs for cold storage and frozen food processing facilities in recent years. Developing economies also continue to face infrastructure limitations related to refrigerated logistics and storage capacity, contributing to quality degradation and post-harvest losses. Additionally, export-oriented suppliers remain exposed to international trade disruptions, tariff changes, and shipping cost volatility, which can affect long-term pricing stability and competitiveness.

potato market industry key opportunities

Expansion of Frozen Potato Processing in Emerging Economies

Emerging economies across Asia-Pacific, Latin America, and the Middle East represent major growth opportunities for frozen potato processing manufacturers. Rising middle-class populations, changing dietary habits, and increasing penetration of international fast-food chains are driving demand for frozen fries and ready-to-cook potato products. Governments in countries such as India and Indonesia are supporting food processing investments through industrial incentives, agricultural modernization programs, and cold-chain infrastructure development. Companies establishing localized processing facilities can significantly reduce logistics costs and improve supply responsiveness while capturing rapidly growing regional demand.

Growth in Sustainable and Specialty Potato Products

Consumer demand for healthier and environmentally sustainable food products is creating new opportunities for organic potatoes, low-oil snacks, premium potato varieties, and biodegradable potato starch applications. Colored potatoes rich in antioxidants and clean-label processed products are gaining traction among health-conscious consumers in North America and Europe. Additionally, industrial demand for potato starch in biodegradable packaging materials, pharmaceuticals, and textile applications is increasing steadily. Companies investing in sustainable cultivation practices, traceability systems, and environmentally friendly packaging solutions are expected to gain competitive advantages over the long term.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 122.40 Billion |

| Market Size in 2026 | USD 129.01 Billion |

| Market Size in 2031 | USD 167.81 Billion |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fresh potatoes continue to dominate the global potato market, accounting for nearly 46% of the total market share in 2025 due to their widespread household consumption and staple food status across major economies. However, frozen potato products represent the fastest-growing product category globally. Frozen French fries remain the leading processed potato product due to rising demand from quick-service restaurants and convenience food manufacturers. Potato chips and snack products also maintain strong demand growth, particularly in Asia-Pacific and Latin America where packaged snack consumption is increasing rapidly. Dehydrated potato products including flakes and powders are witnessing rising utilization in ready-to-eat meals, bakery applications, and institutional foodservice due to their extended shelf life and operational convenience.

Application Insights

Food processing remains the largest application segment in the potato market, accounting for approximately 39% of global market demand in 2025. The segment is driven primarily by frozen foods, snacks, ready-to-eat meals, and industrial food manufacturing applications. Household consumption continues to represent a substantial share of fresh potato demand globally, especially across Asia and Eastern Europe. Industrial applications of potato starch are expanding steadily in paper manufacturing, pharmaceuticals, textiles, adhesives, and biodegradable materials. Animal feed applications are also increasing through the utilization of processing by-products and lower-grade potatoes. Foodservice applications, particularly within quick-service restaurants and hotels, remain among the fastest-growing demand segments globally.

Distribution Channel Insights

Supermarkets and hypermarkets dominate potato distribution globally, accounting for nearly 34% of total retail sales due to their large-scale procurement networks, product variety, and pricing competitiveness. Wholesale agricultural markets remain highly important across developing economies where traditional distribution systems continue to dominate fresh produce trade. Online grocery platforms are rapidly emerging as a key distribution channel, particularly in urban markets where consumers increasingly prefer home-delivery convenience. Foodservice distributors maintain a critical role in supplying institutional buyers including restaurants, hotels, cafés, and catering operators. Direct farm sales and agricultural cooperatives are also growing in importance within organic and premium potato segments where traceability and freshness remain important purchasing factors.

End-User Insights

Residential consumers remain the largest end-user segment within the global potato market due to the crop’s role as a staple food across multiple regions. However, quick-service restaurants represent the fastest-growing institutional end-user category, accounting for approximately 28% of processed potato demand globally. Food manufacturers continue expanding their usage of potato ingredients in frozen foods, snacks, bakery products, soups, and ready meals. Industrial starch manufacturers are also increasing potato procurement volumes due to rising demand from paper, textile, and biodegradable material industries. Hotels, restaurants, and cafés are contributing strongly to premium frozen potato demand as global tourism and hospitality sectors continue to recover and expand.

Explore more data points, trends and opportunities Download Free Sample Report

Potato Market Segmentations

By Product Type

- Fresh Potatoes

- Frozen Potato Products

- Potato Chips & Snack Products

- Dehydrated Potato Products

- Potato Starch Products

- Organic & Specialty Potatoes

By Application

- Household Consumption

- Food Processing

- Foodservice & Hospitality

- Industrial Processing

- Animal Feed

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Grocery Platforms

- Foodservice Distributors

- Wholesale Agricultural Markets

- Direct Farm Sales & Cooperatives

By End User

- Residential Consumers

- Food Manufacturers

- Quick-Service Restaurants

- Hotels, Restaurants & Cafés

- Industrial Starch Manufacturers

Regional Insights

North America

North America accounts for approximately 21% of the global potato market, supported by advanced agricultural mechanization, large-scale food processing infrastructure, and strong demand from quick-service restaurant chains. The United States remains one of the world’s largest potato producers and exporters of frozen potato products. Idaho and Washington continue to dominate domestic production due to favorable climatic conditions and advanced irrigation systems. Canada is also strengthening its export position in frozen fries and processed potato products, particularly toward Asian and Middle Eastern markets. Rising consumer demand for premium snacks, frozen foods, and organic potatoes continues to support regional market expansion.

Europe

Europe holds nearly 29% of the global potato market and remains a major center for frozen potato processing and international exports. The Netherlands and Belgium dominate global frozen French fry exports due to highly advanced processing facilities, integrated supply chains, and strong agricultural productivity. Germany, France, and the United Kingdom continue to maintain high per-capita potato consumption rates across both fresh and processed categories. Sustainability-focused cultivation, carbon reduction initiatives, and energy-efficient food processing technologies are becoming increasingly important across the European market. Eastern European countries are also expanding potato production through modernization programs and infrastructure investments.

Asia-Pacific

Asia-Pacific remains the largest regional market with approximately 37% share of global potato consumption in 2025. China continues to lead global production volumes due to extensive cultivation acreage and strong government support for food security programs. India is emerging as one of the fastest-growing potato markets globally, supported by rising snack food demand, expanding cold storage infrastructure, and rapid growth of quick-service restaurant chains. Japan and South Korea maintain strong demand for premium processed potato products and snack applications. Southeast Asian countries including Indonesia, Vietnam, and Thailand are witnessing rapidly increasing imports of frozen potato products as Western-style fast-food consumption expands across urban populations.

Latin America

Latin America is experiencing steady growth in potato consumption due to urbanization, rising packaged food demand, and expanding foodservice industries. Brazil and Argentina represent the largest regional markets supported by increasing investment in food processing infrastructure and organized retail expansion. Peru remains globally recognized for specialty and native potato varieties, supporting niche export opportunities and premium product development. Growing middle-class populations across the region are contributing to higher demand for convenience foods and frozen potato products.

Middle East & Africa

The Middle East & Africa region represents one of the fastest-growing potato markets globally due to increasing food imports, urban population growth, and expanding fast-food industries. Saudi Arabia and the UAE remain major importers of frozen potato products, supported by high disposable incomes and strong foodservice demand. Egypt continues to strengthen its role as a regional potato producer and exporter due to favorable climatic conditions and export-focused cultivation. In Africa, rising urbanization and improving retail infrastructure are contributing to gradual increases in processed potato consumption across countries including South Africa, Kenya, and Nigeria.

Key Players in the Potato Market

- McCain Foods

- Lamb Weston

- J.R. Simplot Company

- Aviko

- Farm Frites

- Agristo

- PepsiCo

- Kraft Heinz

- Basic American Foods

- Intersnack Group

- Calbee

- Herr Foods

- Utz Brands

- Tyrrells Potato Crisps

- Burts Snacks