Pork Pig Market Size

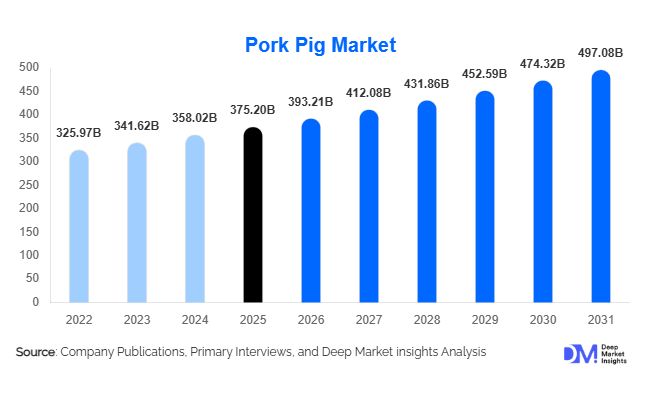

According to Deep Market Insights, the global pork pig market size was valued at USD 375.2 billion in 2025 and is projected to grow from USD 393.21 billion in 2026 to reach USD 497.08 billion by 2031, expanding at a CAGR of 4.8% during the forecast period (2026–2031). The pork pig market growth is primarily driven by increasing global protein consumption, rising demand for pork products across Asia-Pacific, modernization of commercial pig farming operations, and continued expansion of processed meat industries worldwide. Technological advancements in livestock management, including precision livestock farming, automated feeding systems, genetic improvement programs, and AI-enabled herd monitoring solutions, are further enhancing productivity and profitability across the value chain.

Key Market Insights

- Asia-Pacific dominates the global pork pig market, accounting for nearly 57% of global demand, driven primarily by China, Vietnam, Japan, South Korea, and the Philippines.

- Large integrated industrial farms represent the leading production model, benefiting from economies of scale, advanced biosecurity systems, and automated production technologies.

- Hybrid commercial pig breeds continue gaining market share due to superior feed conversion efficiency, disease resistance, and faster growth cycles.

- Latin America is emerging as the fastest-growing production region, supported by Brazil's expanding export-oriented pork industry.

- Precision livestock farming technologies are accelerating industry modernization, enabling real-time herd monitoring, predictive disease management, and improved operational efficiency.

- Processed pork products are becoming an increasingly important demand driver, supported by rising consumption of bacon, sausages, ham, and ready-to-eat meat products globally.

Pork Pig Market Latest Trends

Precision Livestock Farming Reshaping Commercial Production

The adoption of precision livestock farming technologies is transforming commercial pig production globally. Large-scale producers are increasingly deploying IoT-enabled sensors, AI-powered disease detection platforms, automated feeding systems, climate-controlled housing, and predictive analytics tools to optimize herd performance. These technologies enable producers to improve feed conversion ratios, reduce mortality rates, enhance animal welfare, and lower production costs. Smart farming investments are particularly prominent in China, the United States, Canada, Denmark, and the Netherlands, where producers are pursuing greater efficiency and scalability. As labor shortages intensify across several agricultural economies, automation technologies are becoming essential for maintaining production competitiveness and ensuring long-term operational sustainability.

Growing Demand for Premium and Antibiotic-Free Pork

Consumer preferences are increasingly shifting toward premium-quality pork products that emphasize animal welfare, traceability, sustainability, and food safety. Antibiotic-free, organic, free-range, and welfare-certified pork categories are experiencing faster growth than conventional pork production in North America, Europe, Japan, and South Korea. Retailers and foodservice operators are expanding premium pork offerings to address evolving consumer expectations. Producers are responding through investments in enhanced traceability systems, specialized breeding programs, and sustainable production practices. This trend is creating opportunities for market participants to improve profit margins while differentiating their products in increasingly competitive markets.

Pork Pig Market Drivers

Rising Global Demand for Animal Protein

Growing population levels, increasing urbanization, and rising disposable incomes continue to support long-term growth in global meat consumption. Pork remains one of the most widely consumed animal proteins worldwide, particularly across Asia-Pacific and Europe. As emerging economies experience income growth and dietary diversification, demand for affordable protein sources continues to expand. Countries including China, Vietnam, the Philippines, Indonesia, and several Latin American markets are witnessing sustained increases in pork consumption. This structural demand growth is expected to remain one of the most important drivers supporting market expansion through the forecast period.

Expansion of Processed Meat Manufacturing

The rapid growth of processed meat industries is generating substantial demand for pork pigs globally. Products such as sausages, bacon, ham, salami, cured meats, and ready-to-eat food products rely heavily on pork as a primary raw material. Urban lifestyles, changing consumer preferences, and growing demand for convenience foods are contributing to rising processed meat consumption across developed and emerging markets. Expansion of foodservice chains, quick-service restaurants, and modern retail channels is further accelerating pork demand throughout the supply chain.

Technological Modernization of Pig Farming

Advancements in genetics, herd management software, automated feeding systems, and disease prevention technologies are improving production efficiency across commercial pig farming operations. Producers are increasingly adopting advanced breeding programs that improve growth rates, feed efficiency, and disease resistance. These technological improvements are helping operators increase output while reducing production costs and environmental impact, supporting overall market growth.

Pork Pig Market Restraints

African Swine Fever and Disease Outbreak Risks

Disease outbreaks remain one of the most significant challenges facing the global pork pig industry. African Swine Fever (ASF) has caused substantial disruptions to production, trade, and pricing across multiple countries over the past decade. Outbreaks often result in herd reductions, movement restrictions, export limitations, and significant financial losses for producers. The need for continuous biosecurity investments increases operational costs and remains a major concern for industry participants.

Volatility in Feed and Input Costs

Feed accounts for approximately 60–70% of total pig production costs, making profitability highly sensitive to fluctuations in grain and oilseed prices. Variations in corn, soybean meal, wheat, and energy prices can significantly impact producer margins. Climate-related disruptions, geopolitical tensions, and supply chain instability further contribute to feed cost volatility, creating uncertainty across the industry and potentially slowing investment activity.

Pork Pig Industry Key Opportunities

Expansion of Export-Oriented Pork Production

Growing pork deficits across several importing countries continue to create significant opportunities for export-focused producers. China, Japan, South Korea, Mexico, and the Philippines remain among the world's largest pork importers. Producers in Brazil, Spain, Canada, Denmark, and the United States are expanding production capacity and processing infrastructure to capitalize on increasing international demand. Investments in export-certified facilities, traceability systems, and disease-free production zones are expected to support long-term growth opportunities.

Digital Agriculture and Smart Farming Solutions

The ongoing digital transformation of agriculture presents substantial opportunities for technology providers and livestock operators. AI-based herd monitoring systems, predictive disease analytics, automated feeding technologies, and environmental control systems are becoming increasingly important across modern pig production facilities. Companies that successfully integrate digital farming solutions can improve operational efficiency, reduce losses, and achieve superior productivity compared with conventional production models.

Premium and Sustainable Pork Production

Rising consumer demand for organic, antibiotic-free, free-range, and welfare-certified pork products is creating new growth avenues across developed markets. Premium pork categories command higher prices and often generate stronger margins for producers. Market participants investing in sustainability certifications, animal welfare standards, and transparent supply chains are well positioned to benefit from this evolving consumer landscape.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 375.20 Billion |

| Market Size in 2026 | USD 393.21 Billion |

| Market Size in 2031 | USD 497.08 Billion |

| CAGR | 4.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Production System Insights

Conventional pork pig production remains the dominant production system globally, accounting for approximately 78% of total market value in 2025. The continued leadership of conventional production systems is supported by lower production costs, established infrastructure, high-volume output capabilities, efficient feed conversion practices, and widespread adoption among large commercial producers. Integrated production models, advanced breeding programs, and standardized management practices further strengthen the competitiveness of conventional systems, particularly in major pork-producing countries across Asia-Pacific, North America, and Europe.Despite the dominance of conventional production, premium production systems such as organic, antibiotic-free, free-range, and welfare-certified pork are gaining increasing commercial significance. Rising consumer awareness regarding animal welfare, food safety, environmental sustainability, and traceability is encouraging retailers, foodservice operators, and processors to expand premium pork offerings. Antibiotic-free and welfare-certified pork categories are witnessing the strongest growth rates, particularly in North America and Europe, where regulatory support and evolving consumer purchasing behavior continue to accelerate adoption. Organic pork production is also expanding in developed markets as consumers increasingly seek clean-label and sustainably produced meat products. Although premium production systems currently account for a smaller share of total market value, their significantly higher growth rates and premium pricing structures are creating attractive opportunities for producers seeking to enhance profitability and diversify product portfolios during the forecast period.

Pig Category Insights

Finisher pigs represent the largest category within the global pork pig market, accounting for approximately 42% of overall market value in 2025. Their market leadership is primarily driven by direct linkage to slaughter operations and commercial pork production, making them the most economically important stage within the production cycle. Demand for finisher pigs continues to increase as processors and meat producers seek consistent supplies of market-ready animals capable of delivering optimal carcass weights, superior meat quality, and improved feed efficiency. The expansion of industrial pork production systems and growing global meat consumption further support segment growth.Grower pigs constitute another significant segment as producers increasingly focus on maximizing growth performance, improving feed utilization, and reducing production costs throughout the rearing cycle. Investments in precision nutrition, health management programs, and genetic advancements are contributing to improved productivity across grower operations. Breeding sows and boars remain critical to long-term herd development, benefiting from ongoing advancements in reproductive technologies, artificial insemination programs, genomic selection, and genetic improvement initiatives aimed at enhancing litter size, disease resistance, growth rates, and carcass characteristics. Meanwhile, piglets and weaners continue to play an essential role within integrated production systems, supporting herd replenishment strategies and enabling producers to optimize throughput, production efficiency, and overall supply chain performance.

Commercial Purpose Insights

Slaughter and fattening pigs dominate the global market, accounting for approximately 68% of total market value in 2025. The segment's leadership is primarily driven by growing global pork consumption, increasing demand from meat processors, expanding foodservice channels, and rising requirements for commercial meat production across both developed and emerging economies. As pork remains one of the most widely consumed animal proteins worldwide, producers continue to prioritize fattening operations that maximize feed efficiency, growth performance, and carcass yield. The increasing scale of industrial pork production and investments in modern feeding technologies further reinforce the segment's dominant position.Breeding stock remains a strategically important segment, particularly among producers investing in herd productivity improvements and long-term genetic enhancement programs. Demand for high-quality breeding animals is increasing as commercial operations seek to improve feed conversion ratios, reproductive efficiency, disease resilience, and meat quality attributes. Specialized genetic improvement stock continues to attract significant investment from large-scale producers aiming to achieve higher productivity and profitability. Export live pigs represent a comparatively smaller yet important market segment, particularly in regions characterized by strong cross-border livestock trade, integrated regional supply chains, and growing international demand for breeding and production animals.

Farm Scale Insights

Large integrated industrial farms account for approximately 61% of global market value and continue to strengthen their competitive position within the pork pig industry. The segment's leadership is driven by substantial economies of scale, advanced automation technologies, vertically integrated supply chains, sophisticated feed management systems, and comprehensive biosecurity protocols. These operations are increasingly leveraging precision livestock farming technologies, artificial intelligence-based monitoring systems, and data-driven production management tools to enhance operational efficiency, reduce disease risks, and improve profitability. Their ability to consistently meet domestic and export market requirements further supports long-term market leadership.Medium-scale commercial farms remain important contributors to regional production, particularly in developing economies undergoing rapid industry modernization and consolidation. These farms often serve as transitional operators between traditional and industrial production models, benefiting from improved access to financing, genetics, veterinary services, and modern management practices. Small-scale farms continue to support rural livelihoods and local pork supply in many countries; however, their market share is gradually declining as industry consolidation, stricter biosecurity requirements, and increasing production costs encourage the shift toward larger commercial operations. Large integrated farms are expected to maintain their dominant position throughout the forecast period due to superior efficiency, greater investment capacity, and stronger export competitiveness.

End-Use Insights

Fresh pork production remains the largest end-use segment, accounting for approximately 58% of global market demand in 2025. The segment's dominance is primarily driven by strong consumer preference for fresh meat products, particularly across major pork-consuming countries such as China, Vietnam, South Korea, Germany, Spain, and several Eastern European nations. Cultural dietary habits, widespread retail availability, and consumer perceptions regarding freshness and quality continue to support robust demand for fresh pork products. The expansion of modern retail channels and cold-chain infrastructure is further strengthening segment growth in emerging markets.Processed pork manufacturing represents the fastest-growing end-use category, supported by rising demand for convenience foods, changing consumer lifestyles, increasing urbanization, and expanding consumption of value-added meat products such as sausages, bacon, ham, salami, and ready-to-eat meals. Growth in organized retailing and food processing industries is creating additional opportunities for processed pork manufacturers. The foodservice and hospitality sectors also serve as important demand generators, benefiting from the continued expansion of restaurant chains, quick-service restaurants, catering services, and tourism-related food consumption. Furthermore, pharmaceutical applications and by-product processing industries are creating additional revenue streams through the utilization of pig-derived materials in healthcare products, industrial applications, and specialty ingredients, supporting broader market value creation.

Explore more data points, trends and opportunities Download Free Sample Report

Pork Pig Market Segmentations

By Production System

- Conventional Pork Pig Production

- Antibiotic-Free Pork Pig Production

- Organic Pork Pig Production

- Pasture-Raised/Free-Range Pork Pig Production

By Pig Category

- Piglets (Weaners)

- Grower Pigs

- Finisher Pigs

- Breeding Sows

- Breeding Boars

By Commercial Purpose

- Slaughter/Fattening Pigs

- Breeding Stock

- Genetic Improvement Stock

- Export Live Pigs

By Breed Type

- Yorkshire

- Landrace

- Duroc

- Hampshire

- Berkshire

- Pietrain

- Hybrid Commercial Breeds

- Indigenous/Local Breeds

By Farm Scale

- Small-Scale Farms

- Medium Commercial Farms

- Large Integrated Industrial Farms

Regional Insights

Asia-Pacific

Asia-Pacific represents the largest regional market, accounting for approximately 57% of global demand in 2025. The region's dominance is driven by its large population base, high per-capita pork consumption in several countries, expanding middle-class populations, and strong cultural preference for pork as a primary protein source. China remains the world's largest producer and consumer of pork pigs, representing nearly one-third of total global market demand, while Vietnam, Japan, South Korea, and the Philippines contribute significantly to regional consumption and production activities.Key growth drivers across Asia-Pacific include rapid urbanization, rising disposable incomes, increasing demand for animal protein, modernization of livestock production systems, and ongoing investments in large-scale commercial farming operations. Government initiatives supporting food security, improved breeding programs, enhanced disease control measures, and modernization of slaughtering and processing infrastructure are further strengthening regional production capacity. Additionally, recovery and expansion efforts following disease outbreaks, particularly African Swine Fever, are encouraging substantial investments in biosecurity systems, advanced genetics, and integrated production facilities, positioning the region for sustained long-term growth.

Europe

Europe accounts for approximately 22% of global market demand and remains one of the most important pork-producing and exporting regions worldwide. Major producing countries including Spain, Germany, Denmark, France, Poland, and the Netherlands play critical roles in both regional supply and international trade. Spain has emerged as a particularly strong global supplier, benefiting from robust export relationships with Asian markets and a highly competitive production sector.Regional market growth is being supported by increasing demand for premium pork products, growing consumer preference for traceable and sustainably produced meat, and continuous investments in animal welfare standards and environmental sustainability initiatives. Technological advancements in livestock management, precision farming, feed optimization, and disease prevention are improving productivity across the region. Furthermore, Europe's strong export orientation, well-established processing infrastructure, and focus on high-quality pork production continue to enhance its competitiveness within global markets despite evolving regulatory requirements.

North America

North America contributes approximately 13% of global market demand, led primarily by the United States and Canada. The region benefits from highly integrated production systems, advanced genetic programs, efficient feed supply networks, and sophisticated meat processing infrastructure that support large-scale commercial pork production. The United States remains one of the world's leading pork producers and exporters, while Canada continues to strengthen its position through efficient production systems and strong international trade relationships.The primary drivers of regional growth include rising export demand from Asia and Latin America, continued investments in automation and precision livestock technologies, advancements in breeding and herd management practices, and increasing adoption of sustainability-focused production models. Producers are also investing heavily in disease prevention, biosecurity enhancements, and environmental management solutions to improve operational resilience. Growing consumer demand for antibiotic-free, traceable, and welfare-certified pork products is creating additional opportunities for value-added production across the region.

Latin America

Latin America accounts for approximately 6% of global market demand and represents the fastest-growing regional market during the forecast period. Brazil serves as the primary growth engine, benefiting from abundant feed grain availability, competitive production costs, favorable export economics, and strong international demand for pork products. Argentina, Chile, and Mexico are also expanding production capacity to meet growing domestic consumption and export opportunities.Regional growth is being driven by increasing investments in commercial livestock operations, modernization of farming infrastructure, rising adoption of advanced genetics and nutrition programs, and expanding meat processing capabilities. Strengthening trade relationships with Asian markets, growing government support for agricultural exports, and increasing foreign investment in livestock production are further accelerating market expansion. Additionally, improving economic conditions, population growth, and rising protein consumption across several Latin American countries are expected to support strong long-term demand for pork products throughout the forecast period.

Middle East & Africa

The Middle East and Africa region represents approximately 2% of global market demand. While pork consumption remains limited in several countries due to religious and cultural dietary preferences, the region continues to present niche growth opportunities, particularly within selected African markets and countries with diverse consumer populations. South Africa remains the most significant producer and consumer within the region and serves as an important center for commercial pork production.Growth across the region is being supported by increasing urbanization, rising disposable incomes, expanding modern retail infrastructure, and gradual shifts in dietary patterns among certain consumer groups. Investments in livestock modernization, veterinary healthcare services, feed production capabilities, and food security initiatives are helping improve productivity and supply chain efficiency. Furthermore, growing demand from hospitality, tourism, and foodservice sectors in selected markets is contributing to incremental consumption growth, supporting steady long-term expansion despite the region's relatively small share of global demand.

Key Players in the Pork Pig Market

- WH Group

- Muyuan Foods

- New Hope Liuhe

- Wens Foodstuff Group

- Charoen Pokphand Foods (CPF)

- Danish Crown

- JBS S.A.

- BRF S.A.

- Smithfield Foods

- Tönnies Group

- Vion Food Group

- Triumph Foods

- Seaboard Foods

- Genus plc