Plantains Market Size

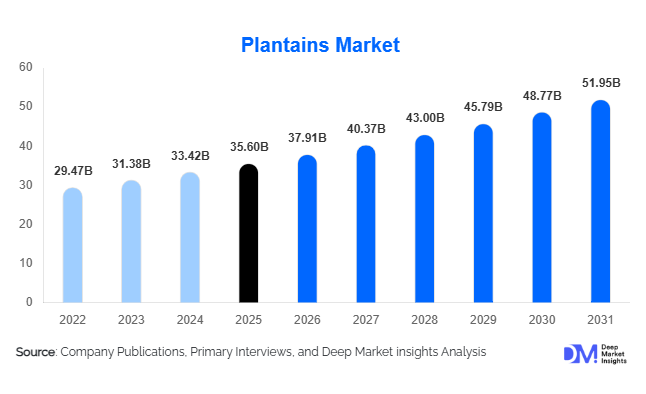

According to Deep Market Insights, the global plantains market size was valued at USD 35.6 billion in 2025 and is projected to grow from USD 37.91 billion in 2026 to reach USD 51.95 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The plantains market growth is primarily driven by rising global demand for healthy snack alternatives, increasing consumption of gluten-free and functional food ingredients, and expanding international trade of tropical agricultural commodities. The market is also benefiting from the globalization of ethnic cuisines, rapid urbanization across developing economies, and growing investments in food processing infrastructure.

Key Market Insights

- Plantain-based snacks and gluten-free food products are witnessing rapid adoption globally, driven by changing dietary preferences and rising health consciousness.

- Processed plantain products are expanding beyond traditional consumption markets, with increasing penetration into premium retail, frozen food, and nutraceutical applications.

- Latin America dominates the global plantains market, supported by strong cultivation infrastructure, export-oriented agriculture, and high domestic consumption.

- Asia-Pacific is emerging as the fastest-growing regional market, fueled by urbanization, rising disposable incomes, and growing demand for tropical food products.

- Africa remains a major production and consumption hub, where plantains continue to serve as an essential staple food across multiple economies.

- Technological integration across farming and processing operations, including AI-enabled crop monitoring, automated food processing, and advanced cold-chain logistics, is transforming the global plantains industry.

plantains market latest trends

Growth of Healthy Snack and Functional Food Applications

Plantain-based snacks are rapidly gaining popularity among consumers seeking healthier alternatives to traditional processed snacks. Manufacturers are increasingly introducing baked, air-fried, organic, and minimally processed plantain chips targeted at health-conscious consumers across North America and Europe. The high fiber content, resistant starch properties, and gluten-free positioning of plantains are supporting their integration into sports nutrition, digestive wellness products, and functional food applications. Food companies are also launching plantain flour-based bakery products, protein bars, and infant nutrition formulations to capitalize on rising demand for clean-label ingredients. The trend is particularly strong among vegan, paleo, and gluten-intolerant consumer groups seeking alternative carbohydrate sources with natural nutritional value.

Expansion of Export-Oriented Tropical Agriculture Supply Chains

Global trade in fresh and processed plantains is expanding steadily as tropical food consumption becomes increasingly mainstream across developed markets. Export-focused countries such as Ecuador, Colombia, Costa Rica, Ghana, and Cameroon are investing heavily in plantation modernization, cold-chain infrastructure, and logistics optimization to improve international competitiveness. Advanced packaging technologies, smart ripening systems, and refrigerated transportation networks are reducing post-harvest losses and enabling longer shipment cycles. Retail chains and foodservice operators are also increasing shelf allocation for tropical produce categories due to rising multicultural demand. Governments across Latin America and Africa are strengthening agricultural export strategies to diversify foreign exchange earnings and support rural economic development.

plantains market drivers

Rising Demand for Ethnic and Tropical Food Products

The globalization of food culture and the rapid growth of multicultural populations are significantly boosting demand for plantains across international markets. Consumers in North America and Europe are increasingly incorporating African, Caribbean, and Latin American cuisines into mainstream dining habits, driving demand for both fresh and processed plantain products. Restaurants, quick-service chains, and frozen meal manufacturers are expanding tropical menu offerings to cater to evolving consumer tastes. Diaspora-driven demand continues to remain a major contributor to import growth across developed economies, particularly in the United States, Canada, Spain, France, and the United Kingdom.

Growth in Gluten-Free and Clean-Label Food Consumption

The increasing prevalence of gluten intolerance and the broader shift toward clean-label food products are accelerating demand for plantain flour and plantain-based ingredients. Consumers are actively seeking natural alternatives to wheat-based products, supporting strong growth in gluten-free bakery, snack, and nutritional applications. Plantains are being marketed as minimally processed, nutrient-rich, and naturally functional ingredients, enabling manufacturers to command premium pricing in health-focused retail categories. Rising awareness regarding digestive health, resistant starch, and dietary fiber is further strengthening demand across wellness-oriented consumer segments.

plantains market restraints

Climate Volatility and Crop Disease Risks

The plantains market remains highly vulnerable to climatic instability, including droughts, excessive rainfall, hurricanes, and temperature fluctuations that directly impact crop productivity. Major producing countries across Latin America and Africa continue to face increasing risks associated with climate change and unpredictable weather cycles. In addition, fungal diseases such as Black Sigatoka and Panama disease create substantial operational challenges by reducing yields and increasing fungicide costs. Smaller farmers often lack access to advanced disease management systems and climate-resilient agricultural technologies, which limits overall production stability.

Supply Chain Fragmentation and Logistics Costs

The global plantains industry remains fragmented, with supply chains spread across multiple developing economies with varying levels of infrastructure quality. Poor transportation networks, limited cold-chain penetration, and fluctuating freight costs continue to affect export profitability and product quality consistency. Since plantains are highly perishable commodities, inefficiencies in storage and transportation can result in substantial post-harvest losses. Rising fuel prices and global shipping disruptions have further increased operational expenses for exporters and food processors, creating ongoing margin pressures throughout the value chain.

plantains industry key opportunities

Expansion of Plantain-Based Processed Foods

The rapid growth of the global healthy snacks and gluten-free food industry presents major opportunities for plantain processors and food manufacturers. Plantain chips, flour, frozen foods, and ready-to-cook products are increasingly penetrating mainstream retail shelves across developed economies. Food companies are investing in advanced dehydration, milling, and vacuum-frying technologies to improve product quality and shelf life while reducing oil content and preserving nutritional value. Premium snack positioning and clean-label branding are allowing companies to target higher-income urban consumers willing to pay premium prices for healthier alternatives.

Export-Led Agricultural Development in Emerging Economies

Governments across Africa and Latin America are actively promoting plantains as strategic export commodities capable of generating foreign exchange earnings and rural employment. Investments in irrigation systems, agricultural extension services, post-harvest infrastructure, and export logistics are improving competitiveness in international markets. Export-oriented farming clusters and public-private partnerships are helping producers comply with international phytosanitary standards and retailer sustainability requirements. Growing diaspora populations and rising global demand for tropical foods continue to create long-term export growth opportunities for producing countries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 35.60 Billion |

| Market Size in 2026 | USD 37.91 Billion |

| Market Size in 2031 | USD 51.95 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fresh plantains dominate the global market, accounting for nearly 58% of total industry revenue in 2025 due to their widespread use as staple foods across Africa, Latin America, and the Caribbean. Strong household consumption and relatively lower processing costs continue to support the dominance of fresh produce distribution through wholesale and retail channels. Processed plantains are emerging as the fastest-growing product segment, particularly within chips, flour, frozen foods, and ready-to-cook applications. Plantain chips are witnessing strong demand within the healthy-snacking category because of their perceived nutritional advantages over traditional potato-based snacks. Plantain flour is also expanding rapidly across gluten-free bakery and infant nutrition applications due to its resistant starch content and clean-label positioning.

Application Insights

Household cooking and staple food consumption remain the largest application segment globally, particularly across developing economies where plantains serve as essential dietary carbohydrate sources. Commercial food preparation within restaurants and hospitality channels is also expanding steadily due to rising demand for ethnic cuisines. Processed food applications are witnessing rapid growth, driven by increasing production of plantain chips, baked snacks, frozen foods, and functional food ingredients. Industrial applications such as starch extraction, fermentation inputs, and animal feed ingredients are gradually emerging as niche growth segments. Nutraceutical applications linked to digestive wellness and gluten-free nutrition are also creating new opportunities for value-added plantain products.

Distribution Channel Insights

Supermarkets and hypermarkets account for the largest share of global retail distribution, representing approximately 34% of organized sales in 2025. Modern retail chains are increasingly expanding tropical produce categories to cater to multicultural and health-conscious consumers. Traditional wholesale produce markets continue to dominate in developing economies where fresh plantains are heavily integrated into daily consumption patterns. Online grocery retail and direct-to-consumer platforms are gradually gaining traction, particularly for processed plantain snacks and specialty flour products. Foodservice distributors also represent an important channel due to growing commercial demand from restaurants, hotels, and institutional buyers.

End-Use Industry Insights

The food processing industry represents the largest end-use segment in the global plantains market, accounting for nearly 31% of total market demand in 2025. Rising production of plantain chips, flour, frozen foods, and convenience products continues to drive industrial demand globally. The hospitality and foodservice sector remains another major consumer segment, supported by increasing popularity of African, Caribbean, and Latin American cuisines across international markets. The nutraceutical and health-food industry is emerging as a fast-growing application area, particularly for gluten-free and digestive health formulations. Animal feed and industrial starch applications are also gradually expanding, supported by increasing utilization of plantain by-products.

Explore more data points, trends and opportunities Download Free Sample Report

Plantains Market Segmentations

By Product Type

- Fresh Plantains

- Frozen Plantains

- Plantain Flour

- Plantain Chips & Snacks

- Ready-to-Cook Plantain Products

- Plantain Puree & Paste

- Dried & Dehydrated Plantains

By Nature

- Conventional Plantains

- Organic Plantains

- Sustainably Certified Plantains

By Application

- Household Food Consumption

- Commercial Food Preparation

- Bakery & Confectionery

- Healthy Snacks & Functional Foods

- Gluten-Free Food Products

- Infant Nutrition

- Industrial Starch Applications

- Animal Feed Ingredients

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Traditional Retail Markets

- Specialty Grocery Stores

- Online Retail

- Wholesale Produce Markets

By End Use Industry

- Food Processing Industry

- Hospitality & Foodservice Industry

- Retail Food Industry

- Bakery & Confectionery Industry

- Nutraceutical & Health Food Industry

- Animal Feed Industry

Regional Insights

North America

North America accounted for nearly 18% of the global plantains market in 2025, led primarily by the United States. Strong demand from Hispanic, Caribbean, and African diaspora populations continues to support large-scale imports of fresh and processed plantains. The United States remains one of the world’s largest importers due to growing multicultural food consumption and increasing demand for healthy snack alternatives. Canada is also witnessing rising demand for tropical produce, supported by demographic diversification and expanding ethnic grocery retail channels. Processed plantain products, particularly chips and gluten-free flour, are experiencing strong growth among health-conscious consumers across the region.

Europe

Europe represented approximately 16% of the global plantains market in 2025. Spain, France, the United Kingdom, Germany, and the Netherlands are among the leading consuming countries due to strong import infrastructure and rising demand for tropical foods. The United Kingdom and France benefit from substantial African and Caribbean populations, while Germany is emerging as a high-growth market for healthy snacks and functional food ingredients. European consumers are increasingly prioritizing organic and sustainably certified products, encouraging exporters to adopt traceability and sustainability-focused agricultural practices.

Asia-Pacific

Asia-Pacific accounted for around 14% of global market share in 2025 and is projected to remain the fastest-growing regional market during the forecast period. Countries such as India and the Philippines are major production and consumption centers, while China, Japan, South Korea, Singapore, and Australia are witnessing rising imports of processed tropical food products. Urbanization, increasing disposable incomes, and rising health awareness are driving growth in plantain-based snacks and convenience foods. Retail modernization and rapid expansion of e-commerce grocery platforms are further accelerating market penetration across urban consumer markets.

Latin America

Latin America dominates the global plantains market with approximately 32% share in 2025. Ecuador, Colombia, Costa Rica, Guatemala, Peru, and the Dominican Republic are among the world’s largest producers and exporters. Plantains remain deeply integrated into regional diets, supporting strong domestic demand alongside export-oriented agricultural production. Governments and private exporters continue investing in plantation modernization, irrigation systems, and cold-chain infrastructure to improve international competitiveness. Ecuador and Colombia remain among the leading suppliers to North America and Europe.

Middle East & Africa

The Middle East & Africa region accounted for nearly 20% of the global market in 2025. Nigeria, Ghana, Cameroon, Uganda, Côte d’Ivoire, and the Democratic Republic of Congo are among the world’s largest producing and consuming countries. Plantains remain a staple food across multiple African economies due to strong affordability and caloric value. Governments across the region are investing in agricultural modernization programs, export diversification strategies, and disease management initiatives to improve productivity. The Middle East is also emerging as an important import market for premium tropical produce due to increasing expatriate populations and growing demand for ethnic food products.

Key Players in the Plantains Market

- Fresh Del Monte Produce Inc.

- Dole plc

- Chiquita Brands International

- Fyffes

- Favorita Fruit Company

- Reybanpac Group

- Uniban

- Banacol

- Tropicale Foods Manufacturing

- Prime Tropical International

- Pacific Trellis Fruit

- AgroAmérica

- Compagnie Fruitière

- Delindecsa

- Agricom Group