Linen Fabric Market Size

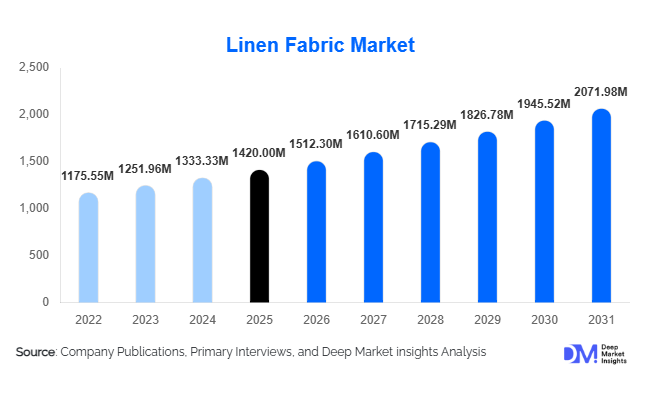

According to Deep Market Insights, the global linen fabric market size was valued at USD 1,420 million in 2025 and is projected to grow from USD 1,512.30 million in 2026 to reach USD 2,071.98 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The linen fabric market growth is primarily driven by rising consumer preference for sustainable and natural textiles, increasing adoption of eco-friendly materials in apparel and home furnishings, and growing demand from premium hospitality and interior décor sectors. Linen fabric, derived from flax fibers, has gained significant popularity due to its durability, breathability, moisture-wicking properties, and lower environmental footprint compared with synthetic alternatives. The growing emphasis on sustainable fashion, coupled with advancements in textile processing technologies and increasing investments in premium home textile products, continues to strengthen market expansion globally.

Key Market Insights

- Sustainable fashion trends are accelerating global linen fabric demand, with apparel brands increasingly incorporating natural and biodegradable fibers into their collections.

- Premium home textile applications are expanding rapidly, particularly in bedding, upholstery, curtains, and luxury interior furnishings.

- Europe dominates the global linen fabric market, supported by strong flax cultivation, established textile manufacturing infrastructure, and premium product demand.

- Asia-Pacific is the fastest-growing regional market, driven by expanding textile production capacity, export-oriented manufacturing, and rising disposable incomes.

- Hospitality and commercial interior sectors are increasing linen fabric procurement, particularly for bedding, table linens, and decorative applications.

- Technological advancements in fabric finishing and sustainable processing are improving linen softness, durability, wrinkle resistance, and consumer acceptance.

Linen Fabric Market Trends

Sustainable and Eco-Friendly Textile Adoption Accelerating

Environmental awareness among consumers, retailers, and governments is significantly increasing the adoption of linen fabrics across multiple industries. Linen is increasingly recognized as one of the most sustainable textile materials due to its low water consumption, biodegradability, and minimal requirement for pesticides during flax cultivation. Fashion brands are expanding linen-based product portfolios to meet sustainability goals and comply with emerging environmental regulations. Demand for certified organic linen, traceable sourcing, and circular textile solutions continues to increase globally. Consumers are actively shifting toward premium natural fibers, creating long-term opportunities for manufacturers focused on sustainable production practices and environmental certifications.

Growth of Premium Home Furnishing Applications

The home furnishing sector is emerging as one of the strongest growth areas for linen fabrics. Rising consumer spending on luxury home décor, increased residential renovation activity, and premium interior design trends are supporting demand for linen bedding, curtains, upholstery, and decorative textiles. Linen's natural texture, aesthetic appeal, and durability make it a preferred material for high-end residential and hospitality applications. Manufacturers are introducing stone-washed, soft-finished, and wrinkle-resistant linen products to improve comfort and expand appeal among mainstream consumers. The trend toward minimalist and sustainable interior designs is expected to further accelerate linen fabric adoption throughout the forecast period.

Linen Fabric Market Drivers

Growing Demand for Sustainable Fashion

The global fashion industry is undergoing a significant transformation toward environmentally responsible production and consumption. Consumers increasingly prefer apparel made from renewable and biodegradable materials, driving demand for linen fabrics across premium and mid-range clothing segments. Linen's sustainability profile aligns with environmental, social, and governance (ESG) commitments adopted by major apparel brands. Increasing implementation of sustainable sourcing programs and eco-label certifications is further supporting market growth. As brands seek alternatives to resource-intensive textile materials, linen continues to gain market share within global apparel manufacturing.

Expansion of Home Textile and Interior Design Markets

Growth in residential construction, home renovation activities, and luxury furnishing expenditure is contributing significantly to linen fabric consumption. Linen's durability, breathability, and premium appearance make it highly suitable for bedding, table linens, curtains, and upholstery applications. Demand from luxury residential projects, premium hotels, and commercial interiors continues to increase globally. Rising urbanization and growing disposable incomes across emerging economies are also creating favorable conditions for the linen textile market expansion.

Linen Fabric Market Restraints

Fluctuating Flax Supply and Raw Material Costs

The linen fabric industry remains highly dependent on flax cultivation concentrated within a limited number of European countries. Climate variability, harvest disruptions, and changing agricultural conditions can significantly affect flax production volumes and pricing. Raw material shortages periodically impact fabric manufacturers through increased procurement costs and supply chain uncertainties. These fluctuations create challenges for maintaining stable profit margins and competitive pricing structures across global markets.

Higher Cost Relative to Alternative Fabrics

Linen fabrics typically command higher prices than cotton and synthetic alternatives due to labor-intensive cultivation, harvesting, and processing requirements. While premium consumers readily accept higher pricing, cost-sensitive segments often favor lower-cost substitutes. This pricing gap limits penetration into mass-market applications and creates competitive challenges for manufacturers seeking broader market adoption. Continued investment in production efficiency and blended fabric innovations remains essential to improving affordability.

Linen Fabric Market Opportunities

Expansion of Sustainable Textile Regulations and ESG Initiatives

Governments and multinational corporations are increasingly implementing sustainability targets that encourage the adoption of environmentally friendly materials. Textile manufacturers that invest in certified flax sourcing, low-impact processing technologies, and circular production systems are expected to benefit from growing regulatory support and consumer preference. Sustainability-driven procurement policies among global apparel brands are creating long-term demand opportunities for linen fabric suppliers.

Growth of Technical and Industrial Linen Applications

Beyond traditional apparel and home textile applications, linen fabrics are increasingly being utilized in industrial and technical sectors. Automotive manufacturers are incorporating natural fiber composites into vehicle interiors to improve sustainability and reduce weight. Demand is also growing for linen-based composite reinforcement materials, filtration products, and specialty industrial textiles. These applications typically offer higher profit margins and greater product differentiation compared with conventional textile markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1420 Million |

| Market Size in 2026 | USD 1512.30 Million |

| Market Size in 2031 | USD 2071.98 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pure linen fabric accounted for approximately 58% of global linen fabric market revenue in 2025, making it the leading product segment worldwide. The segment's dominance is primarily driven by increasing consumer preference for premium, sustainable, and natural textile materials across apparel, home furnishing, and hospitality applications. Pure linen offers superior breathability, moisture absorption, durability, and biodegradability compared to synthetic alternatives, making it highly attractive to environmentally conscious consumers. The growing adoption of sustainable fashion initiatives by luxury apparel brands and premium retailers across Europe and North America has significantly accelerated demand for pure linen products.

Additionally, rising demand for high-end bedding, luxury table linens, and premium upholstery products continues to support market expansion. The increasing willingness of consumers to pay premium prices for environmentally responsible products has strengthened the market position of pure linen fabrics. While pure linen remains dominant, linen blend fabrics represent the fastest-growing product category, supported by their improved wrinkle resistance, enhanced softness, lower production costs, and broader adoption in mass-market apparel. Among blended variants, linen-cotton blends continue to lead due to their balance of comfort, affordability, durability, and ease of maintenance, making them particularly attractive for everyday clothing and household textile applications.

Fabric Weight Insights

Medium-weight linen fabrics accounted for approximately 47% of global market demand in 2025, making them the largest fabric-weight segment. The leadership of this category can be attributed to its versatility across multiple end-use industries, including apparel, home textiles, hospitality, and commercial furnishing applications. Medium-weight linen offers an optimal balance between comfort, durability, drape, and structural integrity, allowing manufacturers to utilize a single fabric category across a broad range of products.

The segment is benefiting from rising demand for premium shirts, dresses, bedding products, curtains, and upholstery materials. Furthermore, advancements in fabric finishing technologies have improved softness and wrinkle resistance, enhancing consumer acceptance of medium-weight linen products. Lightweight linen fabrics are experiencing rapid growth, particularly in warm-weather apparel, resort wear, and sustainable fashion collections, due to increasing demand for breathable and moisture-regulating garments. Meanwhile, heavyweight linen remains a specialized segment catering primarily to upholstery, luxury furniture coverings, decorative textiles, and commercial interior applications where durability and longevity are critical purchasing factors.

Application Insights

Apparel remains the largest application segment, accounting for approximately 39% of total global linen fabric revenue in 2025. The segment's leadership is supported by growing consumer demand for sustainable fashion, increasing awareness regarding natural fibers, and the expanding use of linen in premium casual wear, formalwear, resort wear, and luxury fashion collections. Leading apparel brands are increasingly incorporating linen into their product portfolios to align with ESG commitments and consumer preferences for environmentally friendly materials.

The apparel segment is also benefiting from growing demand for lightweight and breathable clothing in regions with warm climates, particularly across Asia-Pacific, Southern Europe, and the Middle East. Linen's moisture-wicking properties, comfort, and durability continue to position it as a preferred material for premium garments.

Home textiles represent the fastest-growing application segment, driven by increasing consumer expenditure on luxury bedding, table linens, curtains, and upholstery products. Rising residential renovation activity, premium home décor trends, and growing demand for sustainable interior furnishing materials are contributing significantly to segment growth. Hospitality textiles are also witnessing strong expansion due to increasing investments in luxury hotels, resorts, and premium accommodation facilities globally. In addition, technical textile applications are emerging as a niche growth area, supported by rising interest in natural-fiber composites, automotive interior materials, and specialty industrial textiles.

Distribution Channel Insights

Direct sales to manufacturers and OEMs account for approximately 45% of global linen fabric distribution, making it the largest distribution channel segment. The dominance of direct procurement is largely driven by large-scale apparel manufacturers, home furnishing producers, and hospitality suppliers seeking long-term sourcing agreements to ensure consistent product quality, supply reliability, and pricing stability. Direct procurement also enables manufacturers to customize fabric specifications according to product requirements while reducing intermediary costs.

Major apparel exporters in China, India, Bangladesh, Vietnam, and Turkey increasingly rely on direct partnerships with linen fabric producers to secure raw material supply and maintain competitive production schedules. Textile wholesalers continue to play a significant role in developing markets where fragmented manufacturing ecosystems require intermediary distribution support. Meanwhile, e-commerce platforms and digital textile marketplaces are experiencing rapid growth, particularly among independent designers, boutique brands, and small-scale manufacturers seeking access to premium linen products without large-volume purchasing commitments.

End-Use Industry Insights

The fashion and apparel industry remains the largest end-use segment, accounting for approximately 36% of global linen fabric consumption in 2025. The segment continues to benefit from strong growth in premium apparel, sustainable fashion collections, luxury resort wear, and environmentally responsible clothing lines. Global fashion brands are increasingly incorporating linen fabrics into seasonal collections as consumers prioritize comfort, breathability, and sustainability.

The segment's growth is further supported by rising disposable incomes, increasing penetration of premium clothing brands, and growing demand for natural-fiber garments across developed and emerging economies. Home furnishing applications represent the fastest-growing end-use industry, driven by rising expenditure on luxury interiors, increasing residential construction activity, and strong demand for premium bedding and upholstery products.

Hospitality, healthcare, and commercial interior sectors are also expanding their linen fabric consumption due to the material's durability, comfort, moisture management properties, and premium appearance. Export-oriented textile manufacturing hubs including China, India, Bangladesh, Vietnam, and Turkey continue to drive substantial demand for linen fabrics as they serve major international apparel and home furnishing brands worldwide.

Explore more data points, trends and opportunities Download Free Sample Report

Linen Fabric Market Segmentations

By Product Type

- Pure Linen Fabric

- Linen-Cotton Blend Fabric

- Linen-Viscose/Rayon Blend Fabric

- Linen-Polyester Blend Fabric

- Linen-Wool Blend Fabric

- Other Linen Blend Fabrics

By Fabric Weight

- Lightweight Linen Fabric

- Medium-Weight Linen Fabric

- Heavyweight Linen Fabric

By Application

- Apparel

- Home Textiles

- Hospitality Textiles

- Commercial & Institutional Textiles

- Industrial & Technical Textiles

By Distribution Channel

- Direct Sales/OEM

- Textile Wholesalers

- Fabric Retail Stores

- E-commerce Platforms

- Specialty Textile Distributors

By End-Use Industry

- Fashion & Apparel

- Home Furnishing

- Hospitality

- Healthcare

- Commercial Interiors

- Industrial Applications

Regional Insights

Europe

Europe accounted for approximately 38% of the global linen fabric market in 2026, maintaining its position as the largest regional market. The region's dominance is underpinned by its leadership in flax cultivation, established textile manufacturing infrastructure, and strong demand for premium sustainable textiles. France, Belgium, and the Netherlands collectively account for the majority of global flax production, providing Europe with a significant competitive advantage in raw material availability and supply chain integration.

France alone contributes nearly 12% of global market demand and serves as the backbone of the international linen value chain. Italy remains a major consumer due to its globally recognized luxury fashion industry, while Germany and the United Kingdom continue driving demand through premium home furnishing and sustainable apparel sectors. Regional growth is supported by stringent environmental regulations, increasing adoption of circular textile practices, rising demand for certified sustainable materials, and strong consumer willingness to pay premium prices for eco-friendly products. Growing investments in textile traceability, organic flax cultivation, and low-carbon manufacturing processes further strengthen Europe's market leadership.

Asia-Pacific

Asia-Pacific accounted for approximately 34% of global linen fabric revenue in 2026 and is expected to register the fastest growth rate through 2031. The region benefits from its position as the world's largest textile manufacturing hub and its rapidly expanding consumer base. China remains the largest regional market, representing nearly 15% of global demand, supported by extensive weaving, dyeing, finishing, and export-oriented textile production capabilities.

India accounts for approximately 8% of global demand and is expected to emerge as one of the fastest-growing national markets due to increasing textile exports, expanding domestic fashion consumption, rising disposable incomes, and government initiatives supporting textile manufacturing. Vietnam and Bangladesh continue strengthening their positions as key apparel export centers, driving substantial linen fabric procurement from global suppliers. Japan contributes through demand for premium home textiles and high-quality apparel products. Regional growth is being fueled by urbanization, increasing middle-class spending, expansion of e-commerce retail channels, and growing consumer awareness regarding sustainable fashion products.

North America

North America accounted for approximately 16% of global linen fabric demand in 2026, led primarily by the United States. The region's growth is driven by increasing consumer preference for sustainable and natural fibers, rising demand for premium home furnishings, and strong adoption of environmentally responsible fashion products. The United States remains the largest regional market due to high purchasing power, growing luxury apparel sales, and increasing investments in premium interior design products.

The growing popularity of organic and sustainable textiles among millennials and Gen Z consumers is creating substantial demand for linen-based apparel and household products. Canada is also witnessing rising consumption, supported by increasing home renovation activity and growing awareness regarding eco-friendly textile alternatives. The region's mature retail infrastructure and strong e-commerce penetration further facilitate linen product adoption.

Latin America

Latin America represented approximately 5% of global market demand in 2026, with Brazil and Mexico accounting for the majority of regional consumption. Growth is supported by increasing middle-class purchasing power, expanding urban populations, and growing interest in premium home décor and sustainable apparel products.

Brazil remains the largest market due to its sizable textile industry and rising demand for premium household textiles. Mexico benefits from its proximity to North American apparel supply chains and growing domestic fashion sector. Increasing residential construction activity, modernization of retail channels, and expanding availability of imported premium textile products are contributing to regional market growth.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7% of global linen fabric demand in 2026 and is emerging as an important growth market. Saudi Arabia and the United Arab Emirates are leading regional demand due to significant investments in luxury hospitality infrastructure, tourism development projects, and premium residential construction.

Large-scale tourism initiatives, including Saudi Arabia's Vision 2031 projects and expanding hospitality developments across the UAE, are increasing demand for high-quality bedding, table linens, upholstery, and decorative textiles. South Africa remains a notable market due to its established hospitality sector and growing demand for premium home furnishings. Across the region, rising disposable incomes, expanding luxury retail sectors, and increasing adoption of premium interior décor products are expected to support long-term linen fabric market growth.

Key Players in the Linen Fabric Market

- Libeco

- Welspun India Ltd.

- Xinshen Group

- Zhejiang Golden Eagle Co., Ltd.

- Kingdom Holdings Limited

- China Linen Textile Industry Ltd.

- Huzhou Goldrich Linen Textile Co., Ltd.

- Meriti Group

- Jiangsu Chunlong Flax Textile Co., Ltd.

- Huzhou Jinlongma Linen Textile Co., Ltd.

- Harbin Yanshou Linen Textile Co., Ltd.

- Qichun Dongsheng Textile Co., Ltd.

- Baltic Flax

- Siulas AB

- Limageda UAB