Linen Clothing Market Size

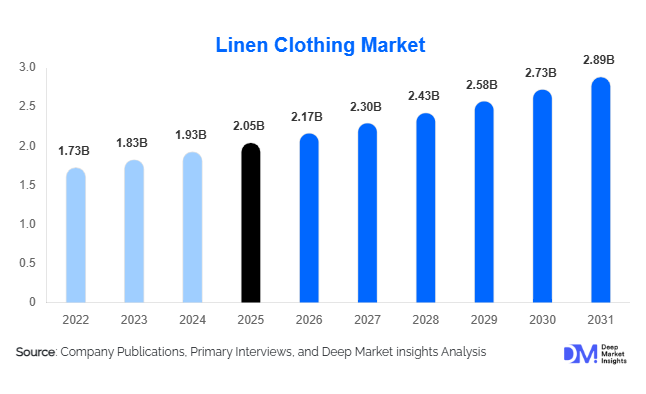

According to Deep Market Insights, the global linen clothing market size was valued at USD 2.05 billion in 2025 and is projected to grow from USD 2.17 billion in 2026 to reach USD 2.89 billion by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The linen clothing market growth is primarily driven by increasing consumer preference for sustainable apparel, rising demand for breathable and natural-fiber garments, and growing adoption of premium casual fashion across developed and emerging economies. Linen clothing continues to gain traction among environmentally conscious consumers due to its biodegradable nature, low water consumption during cultivation, and durability compared to synthetic alternatives. The expansion of e-commerce platforms, direct-to-consumer apparel brands, and sustainable fashion collections has further accelerated market penetration globally.

Key Market Insights

- Sustainable fashion remains the primary growth driver, with consumers increasingly shifting toward natural and eco-friendly textile materials.

- Premium casual wear dominates linen clothing demand, supported by hybrid work trends and relaxed dress codes across corporate environments.

- Europe accounts for the largest market share of approximately 36%, driven by strong consumer awareness of sustainability and long-established linen consumption traditions.

- Asia-Pacific is the fastest-growing regional market, led by rising disposable incomes and premium apparel demand in China and India.

- Women's linen apparel represents the largest gender segment, accounting for nearly 48% of global revenue in 2025.

- Digital commerce is transforming the market, with e-commerce and direct-to-consumer channels becoming key sales drivers for premium linen brands.

Linen Clothing Market Trends

Sustainable and Circular Fashion Adoption Accelerating

Sustainability has become one of the most influential trends shaping the global linen clothing market. Consumers are increasingly evaluating apparel purchases based on environmental impact, supply-chain transparency, and material sourcing practices. Linen, derived from flax fibers, requires significantly less water and pesticide use compared to many conventional textile crops, positioning it as a preferred material within sustainable fashion initiatives. Global fashion brands are introducing dedicated eco-friendly collections featuring certified linen fabrics, recycled packaging, and traceable sourcing practices. The increasing implementation of circular fashion models, including garment recycling programs and resale platforms, is further supporting linen adoption due to the fiber's durability and biodegradability. As governments strengthen sustainability regulations and consumers prioritize environmentally responsible products, linen apparel is expected to capture a larger share of premium apparel spending worldwide.

Premium Resort Wear and Summer Fashion Expansion

Linen clothing is increasingly becoming a staple fabric for resort wear, vacation apparel, and premium summer collections. Rising global tourism activity and growing expenditure on leisure travel are supporting demand for lightweight, breathable garments suitable for warm-weather destinations. Luxury resorts, cruise operators, and premium lifestyle brands are expanding linen-based product offerings, including shirts, dresses, trousers, coordinated sets, and outerwear. Fashion designers are also introducing wrinkle-resistant linen blends that improve garment functionality while maintaining the premium aesthetic associated with natural fibers. Social media-driven fashion trends, particularly in Mediterranean, tropical, and coastal destinations, continue to elevate consumer demand for linen apparel, creating sustained opportunities across premium and luxury segments.

Linen Clothing Market Drivers

Growing Consumer Preference for Sustainable Apparel

Environmental awareness is increasingly influencing apparel purchasing decisions across major global markets. Consumers are actively seeking natural fibers that align with sustainability goals, lower carbon footprints, and ethical production practices. Linen's biodegradable properties, reduced water requirements, and long lifecycle make it highly attractive compared to synthetic fabrics. Major apparel brands are expanding linen collections to satisfy consumer demand for eco-friendly clothing options. The trend is particularly strong across Europe, North America, Japan, and Australia, where sustainability has become a critical purchasing criterion for fashion-conscious consumers.

Expansion of Premium Casual and Smart-Casual Fashion

The global shift toward hybrid work arrangements and more relaxed workplace dress codes has accelerated demand for premium casual apparel. Linen shirts, trousers, dresses, and coordinated sets offer consumers a combination of comfort, sophistication, and functionality. As consumers increasingly prioritize versatile garments that can transition between professional and leisure settings, linen clothing has become a preferred option within smart-casual fashion categories. This trend has significantly expanded the addressable market beyond traditional seasonal applications.

Linen Clothing Market Restraints

High Production and Raw Material Costs

Linen manufacturing remains relatively expensive due to the labor-intensive nature of flax processing and the limited geographic concentration of flax cultivation. Processes such as retting, spinning, weaving, and finishing require specialized expertise and infrastructure, resulting in higher production costs compared to cotton and synthetic textiles. These cost structures contribute to premium pricing, limiting broader adoption among price-sensitive consumer segments and restricting growth in certain emerging markets.

Wrinkle Susceptibility and Maintenance Concerns

Despite advancements in textile finishing technologies, linen continues to be associated with wrinkling and higher garment maintenance requirements. Many consumers perceive linen apparel as less practical for daily wear, particularly within formal and professional applications. While wrinkle-resistant treatments and blended fabrics are helping address these concerns, consumer perception remains a barrier to wider market penetration and mass-market adoption.

Linen Clothing Market Opportunities

Expansion of Sustainable Fashion Ecosystems

The continued growth of sustainable fashion presents significant opportunities for linen clothing manufacturers and brands. Companies that invest in certified flax sourcing, traceability platforms, carbon-neutral production, and circular business models are expected to benefit from growing consumer demand for environmentally responsible apparel. Sustainability-focused collaborations between fashion brands, textile producers, and environmental organizations are creating new avenues for product differentiation and premium pricing. As regulatory frameworks around textile sustainability strengthen globally, linen apparel is well positioned to gain further market share within eco-conscious consumer segments.

Growth of Emerging Asian Premium Apparel Markets

Asia-Pacific represents one of the most attractive growth opportunities for linen clothing manufacturers. Rising disposable incomes, urbanization, expanding middle-class populations, and increasing awareness of sustainable fashion are driving demand for premium apparel across China, India, Indonesia, Vietnam, and South Korea. International brands are expanding retail footprints across these markets while local apparel companies are introducing affordable linen collections targeted at aspirational consumers. Growing digital commerce penetration is further accelerating market accessibility and consumer adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.05 Billion |

| Market Size in 2026 | USD 2.17 Billion |

| Market Size in 2031 | USD 2.89 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Shirts represent the largest product category within the linen clothing market, accounting for approximately 31% of global revenue in 2025. Linen shirts are widely adopted across casual, business-casual, and resort wear applications due to their versatility, comfort, and premium appearance. Dresses constitute another significant segment, particularly within women's apparel, supported by growing demand for sustainable summer fashion. Linen trousers and coordinated sets continue gaining popularity among consumers seeking breathable alternatives to conventional office wear. Premium blazers and lightweight outerwear are emerging as high-growth categories as brands increasingly develop year-round linen collections rather than seasonal offerings.

Fiber Composition Insights

Pure 100% linen garments account for approximately 46% of global market revenue and remain the dominant fiber composition segment. Consumers increasingly associate pure linen with authenticity, sustainability, and premium quality. Linen-cotton blends represent the second-largest segment, offering improved wrinkle resistance and enhanced affordability while retaining many of linen's natural characteristics. Linen-viscose and linen-polyester blends are gaining traction among value-conscious consumers seeking improved garment functionality and lower maintenance requirements. The growing adoption of performance-enhanced linen blends is expanding market opportunities across both casual and formal apparel categories.

Distribution Channel Insights

E-commerce has emerged as one of the most influential distribution channels in the linen clothing market, accounting for approximately 29% of global sales in 2025. Online platforms enable brands to communicate sustainability credentials, showcase product craftsmanship, and reach consumers across international markets. Direct-to-consumer business models continue gaining momentum, allowing manufacturers to improve margins while strengthening customer relationships. Multi-brand retailers and department stores remain important sales channels, particularly for premium and luxury linen collections. Meanwhile, brand-owned stores continue to play a critical role in delivering experiential retail environments and supporting premium brand positioning.

End-Use Insights

Casual wear remains the largest end-use segment, accounting for approximately 42% of global linen clothing demand in 2025. The segment benefits from increasing consumer preference for comfortable and breathable apparel suitable for everyday use. Resort and vacation wear represents one of the fastest-growing applications, supported by global tourism recovery and rising leisure travel spending. Sustainable fashion collections are also expanding rapidly as apparel brands integrate linen into environmentally focused product portfolios. Hospitality uniforms, luxury fashion collections, and wellness-focused apparel categories are emerging as promising niche applications, contributing to market diversification and long-term growth potential.

Explore more data points, trends and opportunities Download Free Sample Report

Linen Clothing Market Segmentations

By Product Type

- Shirts

- T-Shirts & Tops

- Trousers & Bottomwear

- Dresses

- Skirts

- Jackets & Blazers

- Suits & Coordinated Sets

- Outerwear

- Ethnic & Traditional Linen Wear

- Others

By Fiber Composition

- 100% Linen

- Linen-Cotton Blends

- Linen-Viscose/Rayon Blends

- Linen-Polyester Blends

- Linen-Wool Blends

- Other Linen

By Price Point

- Economy

- Mid-Range

- Premium

- Luxury

By Distribution Channel

- Brand-Owned Retail Stores

- Multi-Brand Apparel Stores

- Department Stores

- Specialty Linen Stores

- E-Commerce Platforms

- Direct-to-Consumer (DTC) Online Channels

By End Use

- Casual Wear

- Formal & Office Wear

- Luxury & Designer Fashion

- Resort & Vacation Wear

- Sustainable Fashion Collections

- Uniforms & Hospitality Apparel

Regional Insights

North America

North America accounts for approximately 24% of the global linen clothing market. The United States represents the dominant country within the region, driven by strong consumer spending on premium apparel, growing sustainability awareness, and rising adoption of resort wear and casual fashion. Increasing penetration of direct-to-consumer brands and online retail platforms is further supporting market expansion. Canada continues to demonstrate steady growth, supported by consumer demand for environmentally responsible apparel and premium fashion products.

Europe

Europe remains the largest regional market, accounting for approximately 36% of global revenue in 2025. France, Italy, Germany, the United Kingdom, Spain, Belgium, and the Netherlands represent key demand centers. Consumers across the region demonstrate strong awareness of sustainable fashion and natural fibers, creating favorable conditions for linen apparel adoption. The presence of established luxury fashion houses, premium textile manufacturers, and stringent environmental regulations continues to strengthen Europe's leadership position within the global market.

Asia-Pacific

Asia-Pacific accounts for approximately 29% of global demand and represents the fastest-growing regional market. China contributes nearly 10% of global consumption, while India accounts for approximately 7%. Rising disposable incomes, rapid urbanization, premiumization trends, and increasing sustainability awareness are driving linen clothing adoption throughout the region. The expansion of domestic fashion brands, coupled with growing investments by international apparel companies, is expected to support strong long-term growth across Asia-Pacific markets.

Latin America

Latin America accounts for approximately 5% of the global market, with Brazil and Mexico representing the largest consumers. Growing middle-class populations, increasing fashion consciousness, and expanding retail infrastructure are contributing to gradual market development. Premium casual wear and resort-focused apparel remain the primary demand drivers across the region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6% of global demand. The United Arab Emirates and Saudi Arabia are key growth markets due to high-income consumer bases and strong demand for premium apparel suitable for warm climates. Linen's breathability and luxury positioning make it particularly attractive within Gulf Cooperation Council countries. South Africa also represents an important market, supported by growing premium apparel consumption and retail modernization.