Leather Bags Market Size

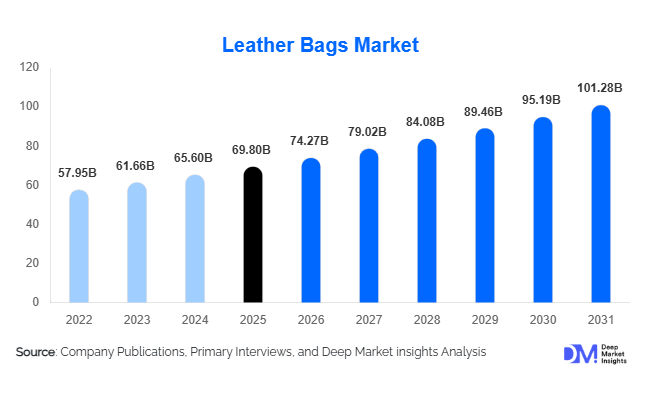

According to Deep Market Insights, the global leather bags market size was valued at USD 69.8 billion in 2025 and is projected to grow from USD 74.27 billion in 2026 to reach USD 101.28 billion by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The leather bags market growth is primarily driven by rising disposable incomes, increasing premiumization in fashion accessories, growing luxury goods consumption, expansion of global tourism, and the rapid growth of digital retail channels. Leather bags continue to represent a blend of functionality, craftsmanship, durability, and status symbolism, making them one of the most resilient categories within the global fashion accessories industry.

Consumer demand is evolving beyond traditional luxury purchases toward sustainable, ethically sourced, and personalized leather products. Premium and luxury brands continue to strengthen their market position through exclusive collections, direct-to-consumer strategies, and omnichannel expansion. Meanwhile, emerging economies in Asia-Pacific, the Middle East, and Latin America are creating new demand centers for both premium and affordable luxury leather bags. Technological advancements in manufacturing, supply chain traceability, and online retailing are further supporting market expansion.

Key Market Insights

- Handbags remain the largest product category, accounting for approximately 34% of global leather bag revenues in 2025.

- Women represent the dominant consumer segment, contributing nearly 57% of total global demand.

- Asia-Pacific dominates the global market, supported by strong consumption growth in China, India, Japan, and South Korea.

- India is among the fastest-growing national markets, benefiting from rising disposable income and increasing premium fashion adoption.

- Sustainable and bio-based leather products are gaining momentum, particularly among younger consumers seeking environmentally responsible alternatives.

- Digital commerce and direct-to-consumer business models are transforming product discovery, customer engagement, and distribution efficiency.

Leather Bags Market Trends

Sustainable and Ethical Leather Sourcing Becoming Mainstream

Sustainability has become a major purchasing consideration within the leather bags industry. Consumers increasingly expect brands to provide transparency regarding sourcing practices, animal welfare standards, tanning processes, and environmental impact. Manufacturers are investing in low-impact tanning technologies, recycled leather materials, bio-based leather alternatives, and traceable supply chains. Luxury and premium brands are incorporating sustainability certifications into product portfolios to strengthen consumer trust and justify premium pricing. As environmental awareness grows globally, sustainability initiatives are expected to become a key differentiator across both luxury and mass-premium segments.

Rise of Personalization and Digital Luxury Retail

Digital transformation is reshaping how leather bags are marketed and sold. Consumers increasingly prefer personalized shopping experiences, custom monogramming services, and limited-edition product offerings. Brands are utilizing artificial intelligence, customer analytics, and virtual shopping technologies to improve engagement and conversion rates. Direct-to-consumer platforms are enabling manufacturers to reduce intermediary costs while strengthening customer relationships. Social media, influencer marketing, and luxury e-commerce marketplaces continue to play a critical role in driving consumer purchasing decisions globally.

Leather Bags Market Drivers

Growing Global Luxury Goods Consumption

The expansion of the affluent and upper-middle-income population globally continues to support demand for premium and luxury leather bags. Consumers increasingly view leather accessories as status symbols and long-term lifestyle investments. Luxury brands have demonstrated strong pricing power despite economic uncertainty, with premium handbags remaining among the most desirable fashion products worldwide. Growth in luxury spending across China, India, Southeast Asia, the Middle East, and North America continues to drive market expansion.

Expansion of Travel and Tourism Activities

The recovery of global travel has significantly boosted demand for leather travel bags, backpacks, duffel bags, and premium luggage products. Increased business travel, international tourism, and weekend leisure trips have stimulated purchases of durable and stylish travel accessories. Consumers are increasingly seeking products that combine functionality with luxury aesthetics, supporting growth across travel-oriented leather bag categories.

Growth of E-Commerce and Omnichannel Retailing

The rapid expansion of e-commerce platforms has improved accessibility to premium leather products across emerging and developed markets. Online channels enable brands to reach broader customer bases while offering personalized recommendations and exclusive product launches. Luxury e-commerce adoption has accelerated significantly among younger consumers, contributing to strong market growth and improved brand engagement.

Leather Bags Market Restraints

Raw Material Price Volatility

Leather bag manufacturers remain exposed to fluctuations in leather hide availability, livestock prices, tanning costs, labor expenses, and transportation charges. Variations in raw material costs directly impact profit margins and retail pricing. Small and medium-sized manufacturers are particularly vulnerable to prolonged cost inflation, creating challenges for maintaining competitive pricing strategies.

Environmental and Ethical Concerns

Growing consumer scrutiny regarding animal welfare and environmental sustainability presents challenges for traditional leather production. Regulations concerning wastewater treatment, chemical usage, and carbon emissions are increasing compliance costs for manufacturers. The growing popularity of vegan and alternative materials also creates competitive pressure on conventional leather products, particularly among younger demographics in developed markets.

Leather Bags Market Opportunities

Expansion of Sustainable and Bio-Based Leather Products

The growing market for environmentally responsible fashion presents substantial opportunities for leather bag manufacturers. Companies investing in bio-based leather, recycled materials, and circular economy initiatives are positioned to attract sustainability-focused consumers. These products often command premium pricing while strengthening brand loyalty and differentiation.

Luxury Demand Growth Across Emerging Markets

Emerging economies such as India, Indonesia, Vietnam, Saudi Arabia, and the UAE are witnessing rapid expansion in luxury consumption. Rising disposable incomes, urbanization, and increasing brand awareness are creating significant opportunities for premium and luxury leather bag manufacturers. Expansion into Tier-2 and Tier-3 cities offers additional long-term growth potential.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 69.8 Billion |

| Market Size in 2026 | USD 74.27 Billion |

| Market Size in 2031 | USD 101.28 Billion |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Handbags accounted for approximately 34% of the global leather bags market in 2025 and remain the leading product segment. Their dominance is primarily driven by their dual role as both fashion accessories and functional everyday products. Handbags benefit from high replacement frequency compared to luggage and business bags, allowing brands to generate recurring demand through seasonal collections, limited-edition launches, and fashion-driven product cycles. Growing consumer preference for premium handbags as status symbols, particularly among women and affluent urban consumers, continues to support segment growth.

The segment is also benefiting from increasing demand for versatile designs such as tote bags, crossbody bags, shoulder bags, and mini handbags that cater to multiple usage occasions. Luxury brands continue to prioritize handbags due to their higher profit margins and strong brand-building potential. The expansion of affordable luxury offerings and rising handbag adoption among younger consumers across emerging markets are expected to further strengthen the segment's leadership position throughout the forecast period.

Leather Type Insights

Full-grain leather remains the dominant leather category, accounting for approximately 31% of total market revenue. The segment's leadership is supported by superior durability, premium aesthetics, natural texture retention, and long product lifespan. Full-grain leather is widely preferred by luxury and premium manufacturers because it enhances product exclusivity and craftsmanship perception. Consumers increasingly view full-grain leather products as long-term investments, particularly within premium handbag, luxury travel bag, and executive business bag categories.

The segment also benefits from rising demand for heritage craftsmanship and authentic luxury products. Premium consumers are increasingly willing to pay higher prices for products that offer superior quality and aging characteristics. As luxury brands continue emphasizing artisanal manufacturing and product longevity, demand for full-grain leather is expected to remain robust despite the emergence of alternative materials.

Distribution Channel Insights

Brand-owned stores represent the largest distribution channel, accounting for approximately 30% of global sales. The segment leads because consumers purchasing premium and luxury leather bags place significant importance on product authenticity, personalized customer service, exclusive collections, and premium brand experiences. Brand-operated stores allow manufacturers to maintain pricing integrity, strengthen customer engagement, and control the overall purchasing journey.

Luxury brands increasingly utilize flagship stores to showcase craftsmanship, heritage, and product exclusivity while enhancing customer loyalty. Although online channels are growing rapidly, brand-owned retail locations continue to serve as critical touchpoints for premium purchases. The integration of omnichannel strategies, appointment-based shopping experiences, and personalized services is further supporting channel growth globally.

Consumer Group Insights

Women account for approximately 57% of total leather bags market demand, making them the largest consumer segment. The segment's dominance is driven by greater product variety, stronger fashion engagement, and higher purchasing frequency compared to other consumer groups. Handbags remain an essential fashion accessory for women across both developed and emerging markets, creating substantial recurring demand.

Luxury and premium brands consistently launch new collections targeted toward female consumers, further accelerating purchase cycles. Rising workforce participation, increasing disposable income among professional women, and growing demand for multifunctional fashion accessories continue to strengthen the segment's leadership. Additionally, social media influence and celebrity endorsements significantly impact purchasing behavior within this demographic.

End-Use Insights

Personal use remains the largest end-use segment, accounting for approximately 61% of total market demand. The segment's leadership reflects the strong positioning of leather bags as lifestyle and fashion products rather than purely functional accessories. Consumers increasingly purchase leather bags to express personal style, social status, and brand preference, driving substantial demand across premium and luxury categories.

The growing influence of fashion trends, rising luxury consumption, and increasing product customization options continue to stimulate purchases for personal use. Meanwhile, social media platforms and influencer-driven marketing have accelerated product awareness and aspiration, particularly among younger consumers. As consumer spending on premium fashion accessories continues to rise globally, personal use is expected to remain the primary demand driver for the leather bags market.

Explore more data points, trends and opportunities Download Free Sample Report

Leather Bags Market Segmentations

By Product Type

- Handbags

- Backpacks

- Travel Bags

- Luggage

- Business Bags

- Specialty Bags

By Leather Type

- Full-Grain Leather

- Top-Grain Leather

- Genuine Leather

- Split Leather

- Bonded Leather

- Exotic Leather

By Consumer Group

- Men

- Women

- Unisex

- Kids & Teens

By Distribution Channel

- Brand-Owned Stores

- Department Stores

- Specialty Fashion Stores

- Hypermarkets & Retail Chains

- Duty-Free Stores

- Online Retail

By End Use

- Personal Use

- Corporate & Business Use

- Travel & Tourism

- Fashion & Luxury

- Sports & Outdoor

- Institutional Procurement

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 38% of the global leather bags market in 2025, making it the largest regional market globally. The region's leadership is supported by a combination of rapidly expanding middle-class populations, rising disposable incomes, growing urbanization, and increasing consumer preference for premium fashion accessories. China remains the largest country market within the region and contributes a substantial share of global luxury leather bag consumption. Strong demand for luxury brands, increasing penetration of international fashion houses, and the growing influence of social media-driven purchasing behavior continue to support market expansion in the country.

India is emerging as one of the fastest-growing leather bags markets globally, driven by increasing household incomes, rapid growth of organized retail, expanding e-commerce penetration, and rising aspirations among younger consumers. The country's large working-age population is creating strong demand for handbags, backpacks, laptop bags, and premium fashion accessories. Japan and South Korea continue to demonstrate robust demand for high-quality leather products, supported by consumer preference for craftsmanship, durability, and premium brand positioning. Additionally, Southeast Asian countries including Indonesia, Vietnam, Thailand, and Malaysia are witnessing increasing consumption of affordable luxury products, further strengthening regional demand. The continued expansion of digital retail platforms, luxury shopping malls, and international brand investments is expected to sustain Asia-Pacific's leadership throughout the forecast period.

Europe

Europe accounted for nearly 30% of global leather bags market revenue in 2025 and remains one of the most influential regions due to its dual role as both a major manufacturing hub and a premium consumption center. Italy and France continue to dominate the global luxury leather goods industry, housing some of the world's most recognized luxury brands and artisanal leather manufacturing clusters. The region benefits from centuries-old craftsmanship traditions, advanced manufacturing capabilities, and strong export-oriented production ecosystems.

Demand growth across Europe is being supported by increasing consumer preference for premium and sustainable fashion products, rising adoption of circular luxury models, and growing investments in ethically sourced leather products. Germany represents one of the largest consumer markets for business bags, travel bags, and premium accessories, supported by a large professional workforce and strong purchasing power. The United Kingdom remains a significant luxury consumption market, driven by affluent consumers and tourism-related luxury retail spending. Additionally, European consumers are increasingly prioritizing sustainability, prompting manufacturers to invest in traceable supply chains, low-impact tanning processes, and recycled leather materials. These trends are expected to support long-term market growth across the region.

North America

North America accounted for approximately 24% of global leather bags demand in 2025, with the United States representing nearly one-fifth of worldwide consumption. The region benefits from high disposable incomes, mature luxury retail infrastructure, strong brand awareness, and significant consumer spending on fashion and lifestyle products. Leather bags are widely perceived as premium lifestyle accessories, supporting strong demand across luxury, premium, and affordable luxury categories.

The United States remains the dominant market within the region due to its large affluent consumer base, well-developed e-commerce ecosystem, and extensive presence of luxury fashion retailers. Demand is particularly strong for premium handbags, travel bags, backpacks, and business-oriented leather products. Canada contributes stable growth through increasing luxury consumption and rising demand for premium accessories among urban professionals. Market expansion is further supported by growing adoption of direct-to-consumer business models, personalized product offerings, and increasing consumer interest in sustainable fashion. The strong presence of both global luxury brands and domestic premium manufacturers continues to reinforce North America's position as a major revenue-generating market.

Latin America

Latin America represents a smaller but steadily expanding market for leather bags, with Brazil and Mexico accounting for the majority of regional demand. Market growth is being driven by increasing urbanization, expanding middle-class populations, improving access to international brands, and growing consumer expenditure on fashion accessories. While luxury market penetration remains lower compared to North America and Europe, premium and mid-priced leather bags are witnessing increasing adoption among aspirational consumers.

Brazil remains the largest market in the region due to its sizeable consumer base, established leather manufacturing sector, and growing fashion industry. Mexico benefits from strong retail sector development, proximity to North American supply chains, and increasing demand for premium accessories among younger consumers. The growth of e-commerce platforms and social commerce channels is improving product accessibility across the region, enabling international brands to expand their reach. As disposable incomes continue to rise and fashion consciousness increases, Latin America is expected to offer attractive growth opportunities for global leather bag manufacturers.

Middle East & Africa

The Middle East & Africa region is emerging as an important growth market for premium and luxury leather bags, supported by rising luxury spending, expanding tourism activity, and increasing investments in high-end retail infrastructure. The United Arab Emirates and Saudi Arabia remain the largest luxury consumption markets within the region, benefiting from high-income populations, growing numbers of affluent consumers, and strong demand for international luxury brands.

The UAE serves as a major luxury retail hub, attracting significant spending from both residents and international tourists through its world-class shopping destinations and duty-free retail channels. Saudi Arabia is witnessing increasing demand for luxury fashion products as economic diversification initiatives, rising female workforce participation, and changing consumer lifestyles continue to expand the addressable market. South Africa remains an important market due to its developed retail infrastructure and established domestic leather industry. Across the broader region, luxury tourism, rising consumer purchasing power, and growing brand investments are expected to drive sustained market growth. Additionally, international luxury brands are increasingly expanding their presence through flagship stores and regional partnerships, further enhancing market penetration and consumer accessibility.

Key Players in the Leather Bags Market

- Louis Vuitton (LVMH)

- Hermès

- Gucci

- Chanel

- Prada

- Coach

- Michael Kors

- Burberry

- Fendi

- Saint Laurent

- Bottega Veneta

- Longchamp

- Tory Burch

- Mulberry

- Samsonite