Lactose Free Yogurt Market Size

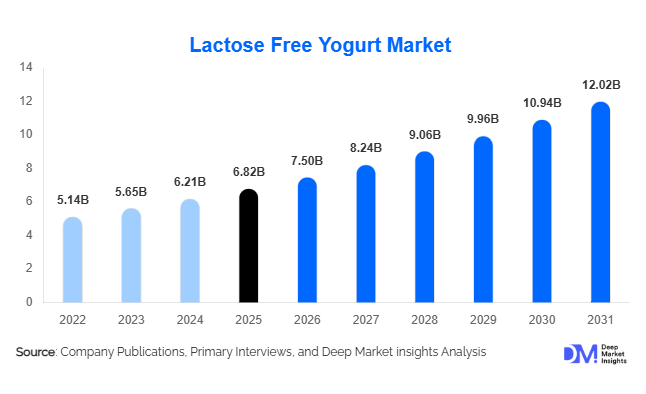

According to Deep Market Insights, the global lactose free yogurt market size was valued at USD 6.82 billion in 2025 and is projected to grow from USD 7.50 billion in 2026 to reach USD 12.02 billion by 2031, expanding at a CAGR of 9.9% during the forecast period (2026–2031). The lactose free yogurt market growth is primarily driven by increasing lactose intolerance awareness, rising demand for probiotic-rich functional foods, growing adoption of digestive wellness products, and expanding consumer preference for clean-label and plant-based dairy alternatives.

Key Market Insights

- Lactose free yogurt is increasingly transitioning from a niche dietary product to a mainstream functional food category, supported by rising consumer focus on digestive health and preventive nutrition.

- High-protein and probiotic-enriched lactose free yogurt variants are gaining significant traction, particularly among fitness-oriented consumers and aging populations.

- Europe dominates the global lactose free yogurt market, driven by strong dairy processing infrastructure, premium yogurt consumption, and high consumer awareness.

- Asia-Pacific is the fastest-growing regional market, supported by high lactose intolerance prevalence, rapid urbanization, and expanding middle-class spending.

- Plant-based lactose free yogurt products are witnessing accelerated growth, particularly oat-, almond-, and coconut-based formulations targeting vegan and flexitarian consumers.

- Technological advancements in enzyme processing, fermentation systems, and probiotic stabilization are improving product quality, shelf life, and nutritional functionality.

Lactose Free Yogurt Market Latest Trends

Growing Demand for Plant-Based Lactose Free Yogurt

Plant-based lactose free yogurt has emerged as one of the strongest growth segments within the broader functional dairy industry. Consumers are increasingly seeking products that combine digestive comfort, sustainability, and clean-label nutrition. Oat-based and almond-based yogurt products are witnessing particularly strong demand due to their creamy texture, lower environmental footprint, and compatibility with vegan and flexitarian diets. Manufacturers are launching innovative formulations with added probiotics, protein fortification, and reduced sugar content to improve nutritional value and taste parity with conventional yogurt. The trend is especially prominent among younger consumers in North America and Europe who prioritize sustainability and animal-free food consumption. Companies are also investing in recyclable packaging, carbon-neutral manufacturing, and ethical ingredient sourcing to strengthen brand positioning in the premium digestive wellness segment.

Functional and High-Protein Yogurt Innovation

Consumers increasingly view lactose free yogurt as a multifunctional health product rather than simply a dairy alternative. High-protein Greek-style yogurt, probiotic-rich formulations, immunity-support blends, and low-sugar functional yogurt products are becoming mainstream across retail shelves. Manufacturers are integrating ingredients such as collagen peptides, omega-3 fatty acids, vitamins, and prebiotics to appeal to preventive healthcare-focused consumers. Sports nutrition applications are also expanding rapidly, with fitness consumers adopting lactose free yogurt as a protein-rich snack and meal replacement option. Personalized nutrition and gut microbiome awareness are further accelerating innovation, prompting companies to develop targeted formulations for digestive health, immunity support, and metabolic wellness.

Lactose Free Yogurt Market Drivers

Rising Prevalence of Lactose Intolerance

The increasing prevalence of lactose intolerance globally is one of the primary factors driving lactose free yogurt market growth. Large populations across Asia, Africa, and Latin America experience varying levels of lactose malabsorption, creating strong demand for digestible dairy alternatives. Consumers are increasingly adopting lactose free yogurt because it provides the nutritional benefits of conventional yogurt while minimizing digestive discomfort. The growing diagnosis of food sensitivities and increased awareness regarding digestive health are accelerating category penetration across developed and emerging markets alike.

Increasing Demand for Functional and Probiotic Foods

Global consumers are increasingly prioritizing foods that support gut health, immunity, and overall wellness. Lactose free yogurt has gained strong consumer acceptance because of its probiotic content and digestive health positioning. Functional food trends are encouraging manufacturers to introduce premium yogurt products enriched with probiotics, prebiotics, vitamins, minerals, and protein isolates. The popularity of microbiome-focused nutrition, healthy snacking, and preventive healthcare lifestyles continues to support long-term demand growth for lactose free yogurt products.

Lactose Free Yogurt Market Restraints

High Production and Retail Costs

Lactose free yogurt products typically command premium prices because of higher production costs associated with enzyme-based lactose hydrolysis, premium ingredients, probiotic fortification, and refrigerated distribution requirements. In price-sensitive developing markets, the higher retail pricing compared to conventional yogurt limits mass-market adoption. Additionally, fluctuating dairy prices, plant protein costs, and transportation expenses continue to create margin pressure for manufacturers.

Cold-Chain and Supply Chain Challenges

Maintaining probiotic viability and product freshness requires advanced refrigerated logistics infrastructure, particularly in emerging economies where cold-chain capabilities remain underdeveloped. Transportation disruptions, raw material volatility, and rising energy costs also affect supply chain efficiency and profitability. Companies operating in developing regions must invest heavily in cold storage, regional manufacturing, and distribution optimization to ensure consistent product quality and market availability.

Lactose Free Yogurt Industry Key Opportunities

Expansion Across Asia-Pacific Markets

Asia-Pacific presents one of the largest untapped opportunities for the lactose free yogurt market due to the region’s high lactose intolerance prevalence and rapidly expanding middle-class population. Countries such as China, India, Indonesia, Thailand, and Vietnam are witnessing increasing consumer awareness regarding digestive health and probiotic nutrition. International dairy companies are expanding local production facilities, cold-chain infrastructure, and retail partnerships across the region to capitalize on rising demand. Localization strategies involving tropical fruit flavors, low-sugar formulations, and region-specific packaging formats are expected to accelerate consumer adoption.

Sports Nutrition and Wellness Integration

The growing global sports nutrition industry presents strong opportunities for lactose free yogurt manufacturers to position products as high-protein, recovery-oriented functional foods. Athletes, fitness enthusiasts, and health-conscious consumers increasingly prefer lactose free yogurt because of its digestibility, probiotic benefits, and protein content. Manufacturers are introducing performance-focused yogurt products fortified with whey protein, collagen, electrolytes, and immunity-support ingredients. Partnerships with fitness chains, wellness influencers, and sports nutrition retailers are also creating new marketing and distribution opportunities for premium lactose free yogurt brands.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.82 Billion |

| Market Size in 2026 | USD 7.50 Billion |

| Market Size in 2031 | USD 12.02 Billion |

| CAGR | 9.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Spoonable lactose free yogurt dominates the global market, accounting for nearly 68% of total market revenue in 2025. This dominance is primarily driven by strong consumer familiarity with traditional yogurt consumption formats, particularly for breakfast routines, healthy snacking, and meal replacement occasions. The segment benefits from its versatility in both household and foodservice applications, as well as its strong alignment with satiety-oriented and high-protein dietary preferences.Within this segment, Greek-style lactose free yogurt represents the leading sub-category, supported by rising demand for high-protein and thicker-texture dairy alternatives that align with fitness-oriented and weight-management diets. Its premium positioning is further reinforced by consumer perception of Greek yogurt as a more functional and indulgent product. Drinkable lactose free yogurt is expanding rapidly, driven by increasing demand for convenient, on-the-go nutrition among younger consumers and urban professionals who prioritize portability and quick consumption. Functional yogurt drinks enriched with probiotics, immunity-boosting ingredients, and digestive health formulations are also gaining momentum, particularly in urban retail environments where preventive health consumption is accelerating.

Source Type Insights

Dairy-based lactose free yogurt remains the dominant source segment, representing approximately 64% of the global market in 2025. Its leadership is supported by strong consumer trust in dairy as a natural source of protein, calcium, and probiotic cultures, along with established taste preferences and well-developed dairy processing infrastructure across key markets.However, plant-based lactose free yogurt is experiencing significantly faster growth, driven by the accelerating shift toward vegan, flexitarian, and sustainability-conscious diets. Environmental concerns related to dairy production, combined with rising lactose intolerance awareness and ethical consumption trends, are further supporting this transition. Oat-based yogurt is emerging as a leading plant alternative due to its naturally creamy texture, mild flavor profile, and lower environmental footprint. Almond-based and coconut-based variants are also expanding within premium wellness and specialty nutrition categories, where consumers increasingly seek clean-label, allergen-friendly, and diversified plant-based options.

Flavor Insights

Fruit-flavored lactose free yogurt accounts for nearly 46% of global demand, with strong preference for variants such as strawberry, mixed berry, mango, peach, and blueberry. The segment’s leadership is driven by its broad consumer acceptance, particularly among children and family-oriented households, where fruit flavors help mask tanginess and improve taste appeal while maintaining nutritional positioning.Vanilla and dessert-inspired flavors are gaining traction in premium segments, supported by consumer demand for indulgent yet health-conscious alternatives to traditional desserts. The overall flavor innovation landscape is increasingly shaped by the shift toward natural sweeteners, reduced sugar formulations, and clean-label ingredient systems. This trend is reinforced by growing health awareness and regulatory pressure on sugar reduction, prompting manufacturers to balance taste optimization with functional nutrition benefits.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channels, accounting for approximately 58% of global lactose free yogurt sales in 2025. Their dominance is driven by strong cold-chain infrastructure, wide product assortment, in-store promotional strategies, and high consumer trust in established retail environments where fresh dairy products are perceived as safer and more accessible.Online retail is emerging as the fastest-growing channel, supported by rapid digital grocery adoption, increasing smartphone penetration, and the expansion of subscription-based dairy delivery models. The convenience of home delivery, coupled with personalized product recommendations and promotional pricing, is significantly accelerating online adoption. Specialty health stores and wellness-focused retail chains are also expanding steadily, driven by rising demand for functional, organic, and digestive-health-oriented dairy alternatives among health-conscious consumers.

Consumer Group Insights

Lactose intolerant consumers remain the foundational customer base for lactose free yogurt products, with demand driven by medical necessity and dietary restrictions. However, the market is increasingly expanding beyond this group into broader wellness-driven consumer segments, reflecting a shift from necessity-based consumption to lifestyle-oriented purchasing behavior.Health-conscious consumers represent a major growth driver, as increasing awareness of gut health, protein intake, and clean nutrition encourages regular consumption of lactose free dairy alternatives. Sports nutrition consumers are also contributing significantly to growth, particularly through demand for high-protein yogurt as a post-workout recovery snack. Additionally, elderly populations are adopting lactose free yogurt for its digestive comfort and calcium-rich nutritional profile, while children and teenagers represent a growing segment due to parental preference for healthier, lower-sugar dairy alternatives that support balanced diets.

Explore more data points, trends and opportunities Download Free Sample Report

Lactose Free Yogurt Market Segmentations

By Product Type

- Spoonable Lactose Free Yogurt

- Greek Lactose Free Yogurt

- Drinkable Lactose Free Yogurt

- High-Protein Lactose Free Yogurt

- Probiotic Lactose Free Yogurt

- Low-Fat & Fat-Free Lactose Free Yogurt

By Source Type

- Dairy-Based Lactose Free Yogurt

- Almond-Based Lactose Free Yogurt

- Oat-Based Lactose Free Yogurt

- Coconut-Based Lactose Free Yogurt

- Soy-Based Lactose Free Yogurt

- Mixed Plant Protein-Based Yogurt

By Flavor

- Plain/Unflavored

- Fruit-Flavored

- Vanilla

- Chocolate

- Dessert-Inspired Flavors

By Nature

- Organic

- Conventional

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health Stores

- Online Retail/E-Commerce

- Foodservice Distribution

Regional Insights

North America

North America accounted for approximately 29% of the global lactose free yogurt market in 2025, with growth primarily driven by strong consumer awareness of digestive health and widespread adoption of high-protein dietary patterns. The region benefits from a mature functional food ecosystem, where lactose free products are increasingly positioned as part of mainstream wellness and fitness nutrition. The United States leads demand due to strong retail penetration, innovation in probiotic and protein-enriched formulations, and rising preference for clean-label dairy alternatives. Canada further supports regional growth through increasing demand for organic, natural, and minimally processed lactose free yogurt products, particularly among urban consumers focused on preventive health.

Europe

Europe dominates the global lactose free yogurt market with nearly 34% market share in 2025, supported by advanced dairy processing capabilities, high per capita yogurt consumption, and strong regulatory emphasis on food quality and labeling standards. Growth in the region is driven by increasing consumer preference for functional dairy products enriched with probiotics and reduced sugar content, alongside strong sustainability awareness influencing purchasing decisions. Germany, the United Kingdom, France, Italy, and Nordic countries serve as key consumption hubs, where organic and premium lactose free yogurt products are particularly popular. The region’s strong focus on environmentally responsible production and health-centric diets continues to reinforce long-term market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at a CAGR exceeding 11% during the forecast period. Growth is primarily driven by the high prevalence of lactose intolerance across large populations, combined with rapid urbanization and rising disposable incomes. China and India are expected to generate the highest incremental demand due to expanding modern retail infrastructure and increasing awareness of digestive health and functional foods. Japan and South Korea are driving premiumization trends through strong demand for probiotic-enriched and technologically advanced dairy formulations, while Australia continues to support growth in organic and plant-based yogurt categories. The region’s expansion is further supported by increasing Western dietary influence and rapid growth in convenience-oriented food consumption.

Latin America

Latin America accounted for approximately 7% of the global market in 2025, with growth driven by rising disposable incomes, urbanization, and gradual modernization of retail infrastructure. Brazil, Argentina, and Chile represent key markets where increasing awareness of digestive wellness and functional dairy benefits is supporting product adoption. Demand is particularly strong in urban centers, where consumers are increasingly seeking affordable probiotic-rich dairy alternatives that combine health benefits with accessible pricing. Expansion of supermarket chains and improved cold-chain logistics are further enabling market penetration across the region.

Middle East & Africa

The Middle East & Africa region is emerging as a promising market for lactose free yogurt, driven by rising health awareness, increasing disposable income, and growing demand for premium dairy products. The UAE and Saudi Arabia are key growth hubs, supported by strong consumer preference for functional foods and increasing awareness of lactose intolerance and digestive health. South Africa leads the African market due to expanding dairy processing capabilities and rising adoption of fortified and functional dairy products among urban populations. Overall regional growth is supported by expanding retail modernization, increasing expatriate population demand, and gradual diversification of dairy offerings.

Key Players in the Lactose Free Yogurt Market

- Danone

- Nestlé

- General Mills

- Chobani

- Arla Foods

- Yakult Honsha

- Lactalis

- Valio

- FAGE International

- Yoplait

- Müller Group

- Stonyfield Farm

- Oatly

- Forager Project

- Siggi’s Dairy