Knitting Yarn Market Size

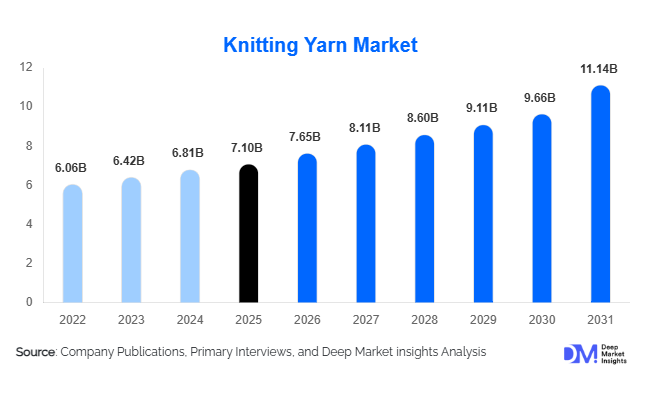

According to Deep Market Insights, the global knitting yarn market size was valued at USD 7.1 billion in 2025 and is projected to grow from USD 7.65 billion in 2026 to reach USD 11.14 billion by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The knitting yarn market growth is primarily driven by increasing global apparel production, growing consumer interest in hand knitting and DIY crafts, rising adoption of sustainable textile materials, and expanding applications of knitted fabrics in technical textiles and healthcare products. The industry is witnessing significant transformation through the introduction of recycled fibers, bio-based yarns, advanced spinning technologies, and digital distribution channels. Growing demand for premium knitwear, home furnishing products, and functional textiles is further strengthening market expansion across both developed and emerging economies.

Key Market Insights

- Apparel manufacturing remains the largest application segment, accounting for more than 55% of global knitting yarn demand.

- Sustainable and recycled yarn products are gaining substantial market traction, driven by environmental regulations and consumer preference for eco-friendly textiles.

- Asia-Pacific dominates the global market, supported by extensive textile manufacturing infrastructure in China, India, Bangladesh, and Vietnam.

- India is emerging as the fastest-growing country market, fueled by textile exports, government incentives, and expanding domestic apparel consumption.

- E-commerce platforms are transforming yarn distribution, enabling direct-to-consumer sales and expanding access to hobby knitting communities worldwide.

- Technical textile applications are creating new growth opportunities, particularly in healthcare, automotive, industrial filtration, and performance apparel sectors.

Knitting Yarn Market Trends

Sustainable and Recycled Yarn Adoption Accelerating

The knitting yarn industry is undergoing a sustainability-driven transformation as apparel brands, retailers, and consumers increasingly prioritize environmentally responsible products. Recycled polyester yarns, recycled cotton yarns, organic cotton, bamboo fibers, and bio-based materials are witnessing significant adoption across textile manufacturing value chains. Textile producers are investing heavily in circular economy initiatives, including fiber recycling technologies and traceability systems that enable verification of sustainable sourcing practices. Sustainability certifications such as GOTS, OEKO-TEX, and Textile Exchange standards are becoming critical differentiators in premium market segments. As global brands commit to reducing carbon emissions and waste generation, sustainable knitting yarns are expected to capture a growing share of total industry demand.

Digital Retail and DIY Craft Communities Driving Consumption

The rapid expansion of online crafting communities and digital retail channels is reshaping the knitting yarn market landscape. Social media platforms, virtual knitting workshops, subscription yarn clubs, and online pattern-sharing ecosystems have expanded consumer participation in knitting activities globally. Younger demographics are increasingly engaging with knitting as a creative hobby, driving demand for specialty yarns, hand-dyed products, and premium fibers. Manufacturers are leveraging direct-to-consumer e-commerce models to improve margins, enhance brand visibility, and build stronger customer relationships. The growing influence of digital content creators and crafting influencers continues to support yarn sales across North America, Europe, and Asia-Pacific.

Knitting Yarn Market Drivers

Expansion of Global Apparel Manufacturing

The continued growth of the global apparel industry remains a major driver for knitting yarn demand. Knitwear products including sweaters, activewear, socks, sportswear, and fashion garments account for a substantial share of textile production worldwide. Rising disposable incomes, urbanization, and evolving fashion trends are increasing apparel consumption across emerging economies. Major textile manufacturing hubs such as China, India, Bangladesh, Vietnam, and Turkey continue to expand production capacities, supporting long-term demand for knitting yarn. The growing popularity of athleisure and performance apparel is also driving demand for specialized yarn blends offering comfort, durability, and moisture management properties.

Growing Popularity of Hand Knitting and Craft Activities

Consumer interest in hand knitting, crocheting, and DIY crafting activities has increased significantly over the past decade. Knitting is increasingly viewed as both a recreational activity and a form of creative self-expression. Online tutorials, crafting communities, and social media engagement have introduced knitting to younger consumer groups, supporting demand for premium yarns, luxury fibers, and artisanal products. The trend has strengthened sales of hand-dyed yarns, wool blends, and specialty knitting materials, particularly across North America and Europe.

Knitting Yarn Market Restraints

Volatility in Raw Material Prices

Fluctuations in cotton, wool, polyester, acrylic, and other fiber prices continue to challenge knitting yarn manufacturers globally. Weather disruptions, geopolitical uncertainties, supply chain constraints, and crude oil price volatility significantly impact production costs. Frequent raw material price fluctuations create uncertainty for both manufacturers and buyers, often compressing profit margins and limiting long-term pricing visibility. Smaller producers are particularly vulnerable due to limited procurement scale and lower bargaining power.

Intense Market Competition and Margin Pressure

The knitting yarn industry remains highly fragmented, with numerous regional and international manufacturers competing across commodity and specialty product categories. Price competition is particularly intense in standard cotton and synthetic yarn segments, where excess manufacturing capacity periodically creates downward pricing pressure. While premium and sustainable yarn categories offer higher margins, companies must continuously invest in innovation, certifications, and brand differentiation to maintain competitiveness in increasingly crowded markets.

Knitting Yarn Market Opportunities

Expansion of Technical Textile Applications

Technical textiles represent one of the most attractive growth opportunities for knitting yarn manufacturers. Applications in medical compression garments, orthopedic supports, filtration products, automotive interiors, industrial fabrics, and protective apparel are growing at rates above traditional textile segments. Demand for antimicrobial, flame-retardant, conductive, and high-strength yarns is creating opportunities for product innovation and premium pricing. As industrial sectors increasingly adopt knitted textile solutions, technical applications are expected to become a significant contributor to future market growth.

Growth of Sustainable Premium Yarn Segments

Consumers are demonstrating a willingness to pay premium prices for environmentally responsible textile products. Recycled polyester yarns, organic cotton yarns, traceable wool products, and biodegradable fibers offer manufacturers opportunities to improve margins while meeting sustainability objectives. The adoption of circular textile policies across Europe and North America is expected to accelerate demand for certified sustainable yarns. Companies investing in recycling technologies, sustainable sourcing partnerships, and environmental certifications are well-positioned to capitalize on this long-term market trend.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.1 Billion |

| Market Size in 2026 | USD 7.65 Billion |

| Market Size in 2031 | USD 11.14 Billion |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Fiber Type Insights

Cotton yarn dominated the global knitting yarn market, accounting for approximately 32% of total market revenue in 2025. The segment continues to maintain leadership due to its extensive use across apparel, home textiles, and hand-knitting applications. Cotton offers superior breathability, moisture absorption, softness, and skin comfort, making it the preferred fiber for knitted garments in both developed and emerging economies. Demand is particularly strong across Asia-Pacific, Latin America, and the Middle East, where climatic conditions favor lightweight and breathable textile products. The increasing consumption of casual wear, athleisure apparel, children's clothing, and summer garments has further strengthened cotton yarn demand globally. Additionally, the expansion of organic cotton cultivation and sustainable textile initiatives among leading apparel brands has reinforced cotton yarn's market position.

Synthetic yarns, primarily acrylic and polyester yarns, represent the second-largest fiber segment, benefiting from their affordability, durability, color retention properties, and suitability for mass-market knitwear production. These fibers are witnessing increasing adoption in sportswear, performance apparel, and fast-fashion garments due to their lower production costs and versatility. Meanwhile, recycled and sustainable yarns are emerging as the fastest-growing fiber category, supported by growing regulatory pressure to reduce textile waste, rising consumer awareness regarding sustainability, and corporate commitments toward circular economy practices. Recycled polyester, recycled cotton, bamboo, and bio-based yarns are expected to outperform traditional fiber categories over the forecast period as apparel brands accelerate their sustainable sourcing strategies.

Application Insights

Apparel knitting remained the largest application segment, accounting for nearly 55% of global knitting yarn consumption in 2025. The segment's dominance is driven by increasing global demand for knitwear products such as sweaters, activewear, sportswear, socks, leggings, winter garments, and fashion apparel. The growing popularity of athleisure trends, rising disposable incomes, and increasing apparel consumption across emerging economies continue to support yarn demand from garment manufacturers. Furthermore, advancements in seamless knitting technologies and automated knitting systems are enabling manufacturers to improve production efficiency while expanding product customization capabilities.

Home textile applications represent the second-largest market segment, supported by growing consumer spending on knitted blankets, throws, rugs, decorative cushions, and premium furnishing products. The increasing focus on home aesthetics and interior decoration, particularly following the growth of e-commerce furniture and home décor markets, has strengthened knitted textile demand. Technical textile applications are emerging as the fastest-growing application area, creating significant opportunities for yarn manufacturers. Knitted structures are increasingly utilized in medical textiles, automotive interiors, filtration systems, industrial fabrics, geotextiles, and protective equipment. Growing investments in healthcare infrastructure, automotive lightweighting initiatives, and industrial automation are expected to drive accelerated adoption of specialized knitting yarns in these high-value applications.

Distribution Channel Insights

Direct sales to textile and apparel manufacturers accounted for approximately 46% of global knitting yarn distribution revenue in 2025, making it the leading distribution channel. Large garment manufacturers increasingly prefer direct procurement relationships with yarn suppliers to ensure product quality consistency, secure long-term supply contracts, optimize procurement costs, and improve supply chain transparency. Direct sourcing has become particularly important as global brands seek greater traceability and sustainability verification across textile value chains. Textile wholesalers continue to play an important role in supplying small and medium-sized textile producers that lack large-scale procurement capabilities. These intermediaries remain particularly relevant across emerging manufacturing hubs where fragmented textile production ecosystems prevail.

E-commerce is currently the fastest-growing distribution channel, supported by rising online purchases among hobby knitters, independent designers, and small-scale textile businesses. Dedicated crafting platforms, direct-to-consumer brand websites, subscription-based yarn clubs, and digital marketplaces are expanding customer access to premium and specialty yarn products globally. Social media-driven product discovery and influencer-led knitting communities are further accelerating online yarn sales, particularly in North America and Europe.

End-Use Industry Insights

Apparel manufacturing remained the dominant end-use industry, accounting for approximately 48% of global knitting yarn demand in 2025. The sector continues to benefit from expanding global fashion consumption, increasing knitwear penetration, growing activewear demand, and rising apparel exports from Asia-Pacific manufacturing hubs. Fast-fashion production cycles and increasing demand for comfort-oriented garments have further strengthened knitting yarn consumption across apparel supply chains. Home furnishing applications accounted for nearly 18% of market demand, supported by increasing consumer expenditure on decorative and functional textile products. Demand for knitted blankets, throws, upholstery fabrics, and decorative accessories continues to expand alongside growth in residential construction and home renovation activities globally.

Healthcare represents one of the fastest-growing end-use segments, driven by rising adoption of medical textiles including compression garments, orthopedic supports, wound care products, prosthetic liners, and rehabilitation equipment. Aging populations and increasing healthcare expenditure across developed economies are supporting long-term growth within this segment. Industrial and technical textile industries are creating additional demand opportunities through applications in automotive fabrics, filtration systems, protective clothing, aerospace textiles, and industrial reinforcement materials. These sectors generally offer higher profit margins and stronger long-term growth potential compared to conventional textile applications.

Explore more data points, trends and opportunities Download Free Sample Report

Knitting Yarn Market Segmentations

By Fiber Type

- Cotton Yarn

- Wool Yarn

- Silk Yarn

- Acrylic Yarn

- Polyester Yarn

- Nylon Yarn

- Viscose & Regenerated Yarn

- Blended Yarn

- Recycled & Sustainable Yarn

By Application

- Apparel Knitting

- Home Textiles

- Hand Knitting & Hobby Crafts

- Industrial Knitted Textiles

- Technical Textiles

- Medical Knitted Products

By Distribution Channel

- Direct Sales to Manufacturers

- Specialty Yarn Stores

- Textile Wholesalers

- Hypermarkets & Craft Retailers

- E-Commerce Platforms

By End Use

- Consumer/Retail Crafting

- Apparel Manufacturing

- Home Furnishing Industry

- Industrial Textile Industry

- Healthcare & Medical Industry

Regional Insights

Asia-Pacific

Asia-Pacific dominated the global knitting yarn market with approximately 44% of total revenue in 2025 and is expected to remain the fastest-growing regional market throughout the forecast period. China remains both the largest producer and consumer of knitting yarn globally, supported by its extensive textile manufacturing ecosystem, integrated supply chains, and strong export-oriented apparel sector. China continues to benefit from investments in automated spinning technologies, synthetic fiber production, and sustainable textile manufacturing.

India is emerging as one of the fastest-growing country markets due to abundant cotton availability, expanding domestic apparel consumption, government initiatives supporting textile modernization, and growing knitwear exports. Bangladesh and Vietnam continue to strengthen their positions as global garment manufacturing hubs, driving significant demand for imported knitting yarns used in export-oriented apparel production. Rising middle-class populations, increasing urbanization, growing disposable incomes, and continued foreign direct investment in textile manufacturing are key drivers supporting long-term regional growth.

Europe

Europe accounted for approximately 25% of global knitting yarn demand in 2025 and remains the leading market for premium, luxury, and sustainable yarn products. Germany, Italy, France, and the United Kingdom are major consumers of wool, cashmere, alpaca, and specialty knitting yarns. The region benefits from strong consumer awareness regarding sustainable fashion, high purchasing power, and advanced textile innovation capabilities.

Growth across Europe is being driven by increasing adoption of recycled yarns, stringent environmental regulations promoting circular textile production, and growing demand for certified sustainable textile products. The region also maintains a strong culture of hand knitting, hobby crafting, and artisanal textile production, supporting demand for premium knitting yarns. Furthermore, European luxury fashion brands continue to drive consumption of high-quality natural fiber yarns for premium apparel manufacturing.

North America

North America represented approximately 18% of global knitting yarn market revenue in 2025, led primarily by the United States. Strong demand for premium knitwear, sustainable apparel, technical textiles, and hobby knitting products supports market growth throughout the region. The U.S. remains a major consumer of specialty yarns used in both commercial apparel production and recreational crafting activities.

Growth is being driven by increasing consumer preference for environmentally responsible textile products, expansion of the DIY crafting community, and growing adoption of advanced knitted materials within healthcare and industrial applications. Canada contributes significantly through premium wool consumption, sustainable textile initiatives, and rising investments in technical textile development. The growing popularity of direct-to-consumer yarn brands and digital retail platforms continues to support regional demand expansion.

Latin America

Latin America accounted for approximately 7% of global knitting yarn demand in 2025, with Brazil and Mexico representing the largest regional markets. Growth is primarily supported by expanding apparel manufacturing activity, increasing domestic textile consumption, and rising urban middle-class populations. Brazil benefits from its large domestic textile industry and growing demand for knitted apparel products, while Mexico continues to leverage its proximity to North American apparel supply chains.

Regional manufacturers are increasingly investing in modern spinning technologies, synthetic fiber production, and textile modernization programs to improve competitiveness and reduce dependence on imports. The rising popularity of affordable knitwear and growth in local fashion industries are expected to further stimulate yarn consumption across the region.

Middle East & Africa

The Middle East and Africa region accounted for approximately 6% of global knitting yarn demand in 2025, offering significant long-term growth potential due to ongoing industrialization and textile sector development. Turkey serves as the region's largest textile manufacturing hub and export center, benefiting from strong integration with European apparel supply chains and advanced textile production capabilities.

Egypt remains a strategically important market due to its globally recognized cotton production industry and expanding textile manufacturing base. The UAE and Saudi Arabia are increasingly investing in textile production facilities, industrial diversification programs, and apparel manufacturing capacity as part of broader economic transformation initiatives. Across Africa, rising population growth, expanding consumer markets, increasing urbanization, and government-led industrial development programs are expected to drive future knitting yarn demand. The emergence of textile manufacturing clusters in countries such as Ethiopia, Kenya, and Morocco is also creating new opportunities for regional market expansion.

Key Players in the Knitting Yarn Market

- Indorama Ventures

- Reliance Industries

- Parkdale Mills

- Südwolle Group

- Filatura di Crosa

- Tollegno 1900

- Coats Group

- Nilit

- Huafu Fashion

- Vardhman Textiles

- Shandong Ruyi

- Erdos Group

- Brown Sheep Company

- Mez Crafts

- Trützschler Group