Kitchen Sinks Market Size

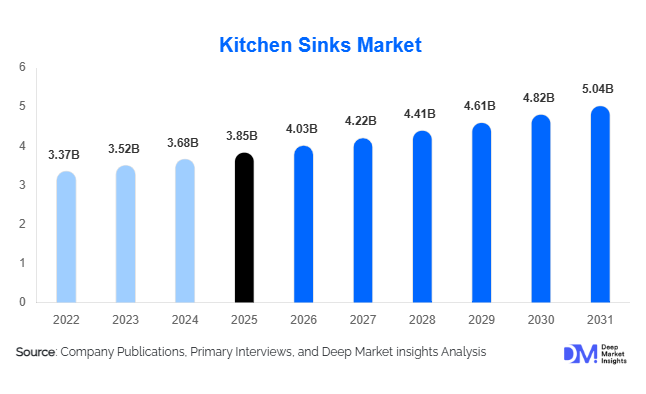

According to Deep Market Insights, the global kitchen sinks market size was valued at USD 3.85 billion in 2025 and is projected to grow from USD 4.03 billion in 2026 to reach USD 5.04 billion by 2031, expanding at a CAGR of 4.6% during the forecast period (2026–2031). Market growth is being driven by rising residential construction activity, increasing kitchen renovation spending, growing consumer preference for premium and multifunctional kitchen fixtures, and expanding adoption of smart and workstation sinks. Kitchen sinks remain an essential component of modern residential and commercial kitchens, with demand increasingly influenced by aesthetics, durability, hygiene standards, and water-efficiency requirements.

Key Market Insights

- Stainless steel remains the dominant material segment, accounting for over 45% of global demand owing to durability, affordability, and corrosion resistance.

- Undermount sink installations continue gaining popularity as homeowners increasingly adopt premium countertop materials such as quartz, granite, and engineered stone.

- Asia-Pacific dominates the global kitchen sinks market, supported by large-scale residential construction activity across China, India, and Southeast Asia.

- North America represents the highest-value renovation market, driven by kitchen remodeling and premium home improvement spending.

- Workstation and multifunctional sinks are emerging as the fastest-growing product category, supported by urbanization and compact kitchen designs.

- Manufacturers are increasingly incorporating antimicrobial coatings, smart water management systems, and sustainable materials to differentiate products in highly competitive markets.

What are the latest trends in the kitchen sinks market?

Rise of Workstation and Multifunctional Sinks

Kitchen sink manufacturers are increasingly focusing on workstation sink designs that integrate cutting boards, drying racks, colanders, and food preparation accessories into a single unit. Consumers are seeking efficient space utilization, particularly in urban apartments and compact homes. Multifunctional sinks help maximize kitchen productivity while reducing countertop clutter. Premium homeowners and professional chefs are increasingly favoring workstation configurations that enhance workflow efficiency. This trend has accelerated particularly in North America, Europe, and developed Asian markets where kitchen remodeling activities remain strong.

Smart and Sustainable Kitchen Solutions

The adoption of smart kitchen technologies is gradually expanding into the sink segment. New products incorporate touchless faucets, integrated water filtration systems, leak detection sensors, and water consumption monitoring capabilities. Sustainability has also become a major purchasing criterion. Manufacturers are introducing recycled stainless steel products, water-efficient sink systems, and environmentally friendly manufacturing processes. Increasing consumer awareness regarding hygiene and resource conservation is driving investments in smart and sustainable kitchen sink innovations globally.

What are the key drivers in the kitchen sinks market?

Growth in Residential Construction Activity

Rapid urbanization and rising housing demand continue to drive kitchen sink installations worldwide. Emerging economies, particularly China, India, Indonesia, Vietnam, and several Middle Eastern countries, are witnessing significant residential construction investments. Every newly constructed housing unit requires kitchen fixtures, directly supporting sink demand. Government-backed affordable housing projects and urban development initiatives are further strengthening installation volumes across both developed and developing markets.

Expansion of Home Renovation and Remodeling Spending

Kitchen remodeling remains one of the largest categories within residential improvement spending globally. Consumers increasingly view kitchens as lifestyle and entertainment spaces rather than purely functional areas. Renovation projects frequently include sink replacement, countertop upgrades, and integrated kitchen redesigns. Premium materials such as granite, quartz, and solid-surface countertops are boosting demand for undermount and designer sinks. This trend is particularly pronounced in North America and Western Europe.

What are the restraints for the global market?

Volatility in Raw Material Prices

Kitchen sink manufacturers remain heavily dependent on stainless steel, cast iron, copper, ceramic, and composite materials. Price fluctuations in global steel and metal markets significantly impact production costs and profit margins. Manufacturers often face challenges in passing increased costs to consumers, particularly in highly competitive mid-range product segments.

Intense Competitive Pricing Pressure

The market remains fragmented with strong participation from global brands, regional manufacturers, and local suppliers. Price competition is particularly intense within economy and mid-range categories. The availability of low-cost imports from Asia places additional pressure on established manufacturers, limiting pricing flexibility and profitability across multiple regions.

What are the key opportunities in the kitchen sinks industry?

Premiumization and Luxury Kitchen Adoption

Rising disposable incomes and increasing consumer focus on kitchen aesthetics are creating significant opportunities in premium sink categories. Luxury homeowners increasingly demand farmhouse sinks, fireclay products, handcrafted copper sinks, and designer composite materials. Premium sinks typically generate higher margins and allow manufacturers to differentiate through design innovation, customization, and advanced functionality.

Smart Kitchen Ecosystem Integration

The expansion of connected home technologies presents new opportunities for sink manufacturers. Integration with smart faucets, water purification systems, IoT-enabled leak monitoring, and touchless operation capabilities can create new revenue streams. Smart kitchen ecosystems are expected to gain traction among premium consumers, luxury residential projects, and commercial foodservice establishments seeking operational efficiency and sustainability improvements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.85 Billion |

| Market Size in 2026 | USD 4.03 Billion |

| Market Size in 2031 | USD 5.04 Billion |

| CAGR | 4.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Insights

Stainless steel sinks remain the leading material segment, accounting for approximately 46% of global kitchen sinks market revenue in 2025. The segment's dominance is primarily driven by its superior balance of durability, corrosion resistance, affordability, ease of maintenance, and compatibility with both residential and commercial applications. Stainless steel sinks are widely preferred by homeowners, contractors, hospitality operators, and foodservice establishments due to their long service life, hygienic properties, and compliance with commercial kitchen standards. The growing popularity of modular kitchens and contemporary kitchen designs further supports adoption, particularly in Asia-Pacific and North America.

The segment also benefits from extensive manufacturing capacity and established supply chains, making stainless steel products readily available across all price categories. Meanwhile, granite composite and quartz composite sinks represent the fastest-growing material categories, supported by increasing consumer preference for premium aesthetics, enhanced scratch resistance, noise reduction properties, and color customization options. Fireclay and ceramic sinks continue to witness robust demand in premium residential renovations, particularly in farmhouse-style and luxury kitchens where design appeal is a major purchasing criterion. Copper, natural stone, and engineered stone sinks occupy niche premium segments, catering to high-end residential projects where exclusivity, craftsmanship, and visual differentiation influence purchasing decisions.

Installation Type Insights

Undermount sinks account for approximately 39% of global market revenue, making them the largest installation type segment. Their market leadership is driven by growing consumer preference for seamless kitchen aesthetics, simplified countertop cleaning, and compatibility with premium countertop materials such as granite, quartz, marble, and engineered stone. As residential remodeling activity continues to increase globally, particularly in developed markets, undermount sinks have become the preferred option for modern kitchen upgrades.

The expansion of premium housing developments and luxury apartment projects is further accelerating demand for undermount installations. The segment also benefits from increasing investments in modular kitchen solutions and integrated interior design concepts. Top-mount sinks continue to maintain strong demand in replacement projects and cost-sensitive housing developments due to lower installation complexity and reduced upfront costs. However, farmhouse (apron-front) sinks are emerging as one of the fastest-growing installation categories, supported by the rising popularity of contemporary, transitional, and rustic kitchen aesthetics. Integrated countertop sinks are also gaining traction in luxury residential, healthcare, and hospitality environments where hygiene, ease of cleaning, and design continuity are prioritized.

Bowl Configuration Insights

Double-bowl sinks dominate the global market with nearly 48% share of total demand in 2025. The segment's leadership is driven by consumer preference for multitasking functionality, allowing users to simultaneously perform food preparation, dishwashing, rinsing, and waste management activities. Double-bowl configurations are particularly popular among medium-to-large households and commercial food preparation environments where workflow efficiency is essential.

The growing emphasis on kitchen convenience and multifunctionality continues to support demand for double-bowl products across both developed and emerging markets. In addition, consumers increasingly view kitchen sinks as productivity-enhancing fixtures rather than purely functional installations. Single-bowl sinks are witnessing strong adoption in urban apartments, compact housing units, and minimalist kitchen designs where maximizing usable sink space is prioritized. Multi-bowl configurations remain concentrated within institutional kitchens, restaurants, hotels, healthcare facilities, and food processing establishments requiring high-volume washing and preparation operations.

Functionality Insights

Conventional kitchen sinks continue to account for the majority of global installations due to their affordability, simplicity, and broad application across residential and commercial environments. However, the strongest growth momentum is being observed in workstation sinks, which have emerged as the fastest-growing functionality segment worldwide.

The rapid expansion of workstation sinks is driven by changing consumer lifestyles, urban space constraints, and growing demand for multifunctional kitchen solutions. These products integrate accessories such as cutting boards, drying racks, strainers, and preparation stations directly into the sink structure, maximizing operational efficiency while reducing countertop clutter. The trend is particularly strong in urban households, premium residential developments, and luxury renovation projects.

Smart sinks incorporating touchless controls, water consumption monitoring systems, leak detection sensors, and integrated filtration technologies are gaining traction as smart home adoption accelerates globally. Additionally, water-saving sink systems are witnessing increased demand in regions facing water scarcity challenges and stricter sustainability regulations. Government initiatives promoting water conservation and green building certifications are expected to further support adoption of advanced sink technologies over the forecast period.

End-Use Insights

The residential sector remains the dominant end-use segment, accounting for approximately 74% of global kitchen sinks demand in 2025. The segment's leadership is supported by strong housing construction activity, rising homeownership rates, growing disposable incomes, and increasing consumer spending on kitchen remodeling and interior upgrades. Kitchen renovations continue to rank among the highest-value home improvement projects globally, creating sustained replacement demand for premium and designer sink products.

Residential remodeling activity remains particularly robust across North America and Western Europe, where aging housing stock and rising consumer interest in premium kitchens continue to drive replacement cycles. In emerging economies, rapid urbanization and government-backed housing initiatives are expanding the addressable market for new sink installations.

The commercial segment accounts for the remaining market share and is supported by demand from restaurants, hotels, healthcare facilities, educational institutions, corporate cafeterias, and foodservice establishments. The rapid expansion of cloud kitchens, food delivery infrastructure, quick-service restaurants, and hospitality developments is generating substantial demand for commercial-grade sinks. Furthermore, increasing food safety regulations and hygiene standards are encouraging businesses to invest in higher-quality, durable sink systems capable of supporting intensive daily operations.

Distribution Channel Insights

Offline distribution channels continue to dominate global kitchen sink sales, accounting for nearly 70% of total market revenue. Home improvement retailers, specialty kitchen showrooms, building material suppliers, and wholesale distributors remain the preferred purchasing channels due to the tactile nature of the product and the importance of professional consultation during kitchen design and renovation projects.

The offline channel also benefits from strong relationships with contractors, architects, interior designers, and builders who influence a significant proportion of purchase decisions. However, online distribution is emerging as the fastest-growing sales channel globally. Increasing product transparency, competitive pricing, digital visualization tools, and growing consumer confidence in e-commerce platforms are driving online adoption.

Direct-to-consumer sales strategies are becoming increasingly important among premium manufacturers, allowing brands to improve margins, strengthen customer engagement, and offer customized product configurations. The integration of augmented reality tools, virtual kitchen design platforms, and digital consultation services is expected to further accelerate online sales growth throughout the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Kitchen Sinks Market Segmentations

By Material

- Stainless Steel Sinks

- Granite Composite Sinks

- Quartz Composite Sinks

- Fireclay Sinks

- Ceramic/Porcelain Sinks

- Cast Iron Enameled Sinks

- Natural Stone Sinks

- Solid Surface/Engineered Stone Sinks

- Copper Sinks

- Others

By Installation Type

- Top Mount (Drop-In) Sinks

- Undermount Sinks

- Farmhouse/Apron Front Sinks

- Flush Mount Sinks

- Integrated Countertop Sinks

- Corner Sinks

By Bowl Configuration

- Single Bowl Sinks

- Double Bowl Sinks

- Triple/Multi Bowl Sinks

By Functionality

- Conventional Sinks

- Workstation Sinks

- Smart/Connected Sinks

- Water-Saving Sinks

- Commercial Utility Sinks

Regional Insights

Asia-Pacific

Asia-Pacific leads the global kitchen sinks market with approximately 41% market share in 2025 and is expected to remain the fastest-growing regional market throughout the forecast period. The region's leadership is primarily driven by rapid urbanization, large-scale residential construction activity, rising disposable incomes, and expanding middle-class populations. China remains the largest market globally due to continuous housing development, government-backed urbanization initiatives, and substantial investments in residential infrastructure. The country's large manufacturing base also supports widespread product availability and competitive pricing.

India represents one of the fastest-growing national markets, supported by affordable housing programs, increasing modular kitchen penetration, rising household incomes, and rapid urban migration. Japan and South Korea continue generating strong demand for premium and technologically advanced kitchen fixtures, driven by high consumer spending on home upgrades and smart home adoption. Across Southeast Asia, countries such as Vietnam, Indonesia, Thailand, and the Philippines are witnessing robust demand due to expanding construction sectors, increasing foreign direct investment in real estate, and growing consumer preference for modern kitchen designs.

North America

North America accounts for approximately 27% of global market revenue and remains one of the highest-value regional markets. Growth is primarily driven by strong residential remodeling expenditure, premium kitchen renovation trends, and high consumer spending on home improvement projects. The United States dominates regional demand due to an extensive housing renovation market, rising adoption of luxury kitchen fixtures, and growing demand for workstation and farmhouse sinks.

The increasing popularity of open-concept kitchens, premium countertop installations, and smart home technologies continues to support market expansion. Canada contributes significantly through residential renovation investments, increasing housing construction activity, and rising demand for environmentally sustainable kitchen products. The region also benefits from high consumer awareness regarding product quality, design aesthetics, and advanced functionality, supporting premiumization trends across the market.

Europe

Europe represents a mature but highly profitable market characterized by strong demand for premium and sustainable kitchen solutions. Germany, the United Kingdom, France, Italy, and Spain collectively account for the majority of regional demand. Growth is largely driven by kitchen modernization projects, replacement demand from aging housing stock, and increasing consumer preference for designer and composite sink materials.

Germany remains the largest European market due to its established kitchen manufacturing industry, high renovation activity, and strong consumer purchasing power. Sustainability regulations, energy-efficient housing initiatives, and environmentally conscious purchasing behavior are accelerating demand for recycled stainless steel, water-saving sink systems, and eco-friendly manufacturing practices. Premium residential construction and luxury renovation activity across Western Europe continue supporting market growth despite relatively slower new housing construction rates.

Latin America

Latin America is experiencing steady market growth, led primarily by Brazil and Mexico. Regional demand is supported by urban population growth, expanding residential construction activity, and gradual improvements in household purchasing power. Government investments in housing development and infrastructure modernization continue creating opportunities for kitchen fixture installations.

Brazil remains the largest market due to its sizable residential construction sector and growing middle-class consumer base. Mexico benefits from strong housing demand, increasing urbanization, and its proximity to North American manufacturing and supply chains. Although economic fluctuations can periodically impact consumer spending, long-term growth is supported by increasing adoption of modern kitchen concepts, rising renovation activity, and improving living standards across major metropolitan areas.

Middle East & Africa

The Middle East & Africa region represents one of the fastest-growing emerging markets for kitchen sinks. Growth is primarily driven by extensive investments in residential developments, hospitality infrastructure, tourism projects, and mixed-use real estate developments. Saudi Arabia and the United Arab Emirates are the largest regional markets, supported by mega-projects, smart city initiatives, luxury housing developments, and substantial government spending under long-term economic diversification programs.

Saudi Arabia's Vision 2031 initiatives and ongoing investments in residential and hospitality infrastructure are creating significant opportunities for premium kitchen fixtures. The UAE continues benefiting from high-end residential construction and tourism-related developments. In Africa, South Africa remains the largest market due to its relatively developed construction sector, while Egypt and Nigeria are experiencing growing demand driven by urbanization, population growth, and expanding residential infrastructure investments. Rising adoption of modular kitchens and increasing availability of imported premium products are further contributing to regional market expansion.

Key Players in the Kitchen Sinks Market

- Franke Holding AG

- BLANCO Group

- Kohler Co.

- Elkay Manufacturing Company

- Teka Group

- Moen Incorporated

- American Standard Brands

- Ruvati USA

- Kraus USA

- Schock GmbH

- Häfele SE & Co KG

- Reginox B.V.

- Oliveri Solutions

- Astracast International

- Carron Phoenix